Applied Materials Analyst Changes Stance; Check Out Wednesday's Top 5 Downgrades

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Aug 20 2025

0mins

Should l Buy AMAT?

Source: Benzinga

Analyst Downgrades: Several Wall Street analysts have downgraded their ratings on various companies, indicating a shift in market outlook.

Agilon Health Inc.: Bernstein analyst Lance Wilkes downgraded Agilon Health from Outperform to Market Perform, reducing the price target from $4 to $1.4.

General Mills and Others: JP Morgan downgraded General Mills from Neutral to Underweight with a new price target of $45, while other companies like Applied Materials and Goodyear also faced downgrades.

Stock Performance: The shares of the downgraded companies closed lower on the respective days, reflecting the analysts' negative outlooks.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AMAT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AMAT

Wall Street analysts forecast AMAT stock price to fall

22 Analyst Rating

18 Buy

4 Hold

0 Sell

Strong Buy

Current: 396.940

Low

190.00

Averages

288.05

High

425.00

Current: 396.940

Low

190.00

Averages

288.05

High

425.00

About AMAT

Applied Materials, Inc. is a materials engineering solution company. The Company provides equipment, services and software to the semiconductor, display, and related industries. It operates in three segments: Semiconductor Systems, Applied Global Services (AGS), and Display. The Semiconductor systems segment designs, develops, manufactures and sells a range of primarily 300 mm equipment used to fabricate semiconductor chips, also referred to as integrated circuits (ICs). The AGS segment provides services, spares and factory automation software to customer fabrication plants globally. The AGS segment also manufactures and sells 200mm and other equipment. The Display segment is comprised primarily of products for manufacturing liquid crystal displays (LCDs), organic light-emitting diodes (OLEDs), and other display technologies for televisions, monitors, laptops, personal computers (PCs), tablets, smartphones, and other consumer-oriented devices.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

US Stocks Dip Slightly as Chipmakers Weigh on Market

- Market Performance: The S&P 500 index fell by 0.15%, the Dow Jones Industrial Average decreased by 0.06%, and the Nasdaq 100 dropped by 0.21%, indicating a slight market pullback after reaching new highs, particularly pressured by weakness in chipmakers.

- Economic Data: Initial jobless claims in the US fell by 11,000 to 207,000, indicating a stronger labor market than the expected 213,000; additionally, the Philadelphia Fed business outlook unexpectedly rose by 8.6 to a 15-month high of 26.7, reflecting potential economic recovery.

- Oil Price Fluctuations: WTI crude oil prices increased by over 1% as the US naval blockade of the Strait of Hormuz enters its fourth day, which could exacerbate global oil and fuel shortages, impacting future energy market stability.

- Earnings Season: Q1 earnings for the S&P 500 are projected to rise by 12% year-over-year, but excluding the technology sector, the earnings growth is only 3%, the lowest in two years, indicating a cautious market outlook on profit growth.

See More

ASML Valuation Anomaly Amid Market Dynamics

- Valuation Anomaly: ASML's relative pricing against US peers has fallen to its lowest level in a decade, currently trading at a forward P/E of 37 times, representing a 17% premium over Applied Materials, indicating a market reassessment of its valuation.

- Market Dynamics Shift: ASML is now priced at about a 5% discount to Lam Research for the first time in 14 years, despite its unique supply position in extreme ultraviolet lithography systems, reflecting cautious market sentiment regarding its future growth.

- Analyst Insights: JPMorgan analyst Sandeep Deshpande highlighted that ASML's valuation may be misaligned with its structural advantages, as the stock has risen 36% year-to-date but lags behind peers like Applied Materials and Lam Research, which have gained over 50%, suggesting that relative underperformance may be driving valuation compression.

- Mixed Market Reaction: Despite ASML raising its full-year sales guidance, the stock declined 4.2% on Wednesday, reflecting concerns over high expectations, while a 2.0% rebound on Thursday suggests that long-term AI-driven demand remains intact, but short-term performance may depend on the relationship between earnings growth and current valuation levels.

See More

Momentum Stocks Surge as Wall Street Optimism Grows

- Record for Momentum ETF: The iShares MSCI USA Momentum Factor ETF (MTUM) hit a new high on Thursday, marking its tenth consecutive winning session, reflecting strong market confidence in growth stocks and suggesting a potential upward trend for the overall market.

- Market Rebound Signs: MTUM, which was down over 7% year-to-date, has now risen 8%, coinciding with the S&P 500's recovery, indicating that the market may be experiencing a broader rebound as investor sentiment turns optimistic.

- Outstanding Stock Performance: Since the onset of the Iran war, Bloom Energy's stock has surged over 40%, while Intel has also risen more than 40%, showcasing the appeal of momentum stocks, particularly following expanded partnerships with major tech companies.

- Momentum Drives Market: Jeff Kilburg, founder of KKM Financial, emphasized that momentum is the primary driver of market gains, predicting that the S&P 500 will reach new all-time highs, with the return of momentum providing strong support for the market.

See More

Microsoft and Stellantis Forge Strategic AI Partnership

- Strategic Partnership: Microsoft and Stellantis have established a five-year strategic partnership aimed at co-developing AI and cybersecurity tools, with plans to launch over 100 AI initiatives, significantly enhancing technological competitiveness in the automotive sector.

- Cloud Migration: Stellantis is shifting its primary tech focus to Microsoft's Azure cloud platform, aiming for a 60% reduction in its physical data center footprint by 2029, which will streamline operations through modernized infrastructure.

- Digital Security Enhancement: The partnership integrates AI-driven analytics across manufacturing sites and connected vehicles to counter emerging cyber threats, thereby protecting the privacy of millions of drivers and enhancing brand trust.

- Positive Market Reaction: Microsoft's stock has surged 10% over the past three days, marking its strongest short-term rally since 2020, with analysts suggesting this indicates growing market confidence in AI integration.

See More

U.S. Stocks Edge Up as PepsiCo and TSMC Shine

- PepsiCo's Quarter Performance: PepsiCo achieved its first volume growth in North American food business in two years, with CEO Ramon Laguarta addressing the industry's threat from GLP-1 weight-loss drugs, leading to a 1% rise in shares, demonstrating the company's resilience and adaptability in a competitive consumer goods market.

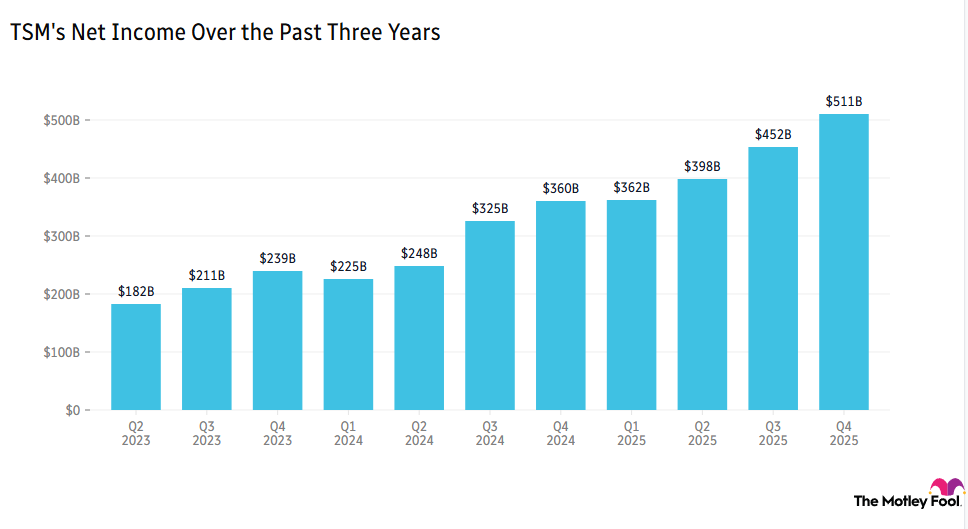

- TSMC Profit Surge: TSMC reported a 58% year-over-year profit increase, despite facing challenges with shortages of industrial gases; management noted a 'little bit softer' memory pricing, indicating ongoing demand and competitive pressures in advanced chip manufacturing that could impact future profitability.

- J.B. Hunt Transport Services: J.B. Hunt indicated the start of a new cycle with positive demand signals, reporting a first-quarter earnings beat and a 1% premarket share increase, reflecting potential growth opportunities in the transportation sector.

- Analyst Rating Changes: JPMorgan downgraded Corning to hold and cut its price target from $175 to $115, citing the need for greater earnings visibility to support stock upside, indicating a cautious market outlook on the company's future performance.

See More

TSMC Profits Surge 58% Amid AI Chip Demand

- Profit Surge: TSMC reported a 58% year-over-year increase in net profit for the latest quarter, indicating strong demand for AI chips and minimal short-term impact from supply chain disruptions, with the stock slightly rising post-earnings release.

- Advanced Technology Revenue: Advanced technology products accounted for 74% of total wafer revenue, reflecting key customers like Apple’s preference for smaller nanometer products, which enhances the company's market share and competitive edge.

- Capacity Expansion: To meet the growing demand, TSMC plans to add production facilities in Taiwan, with capital expenditures expected to be at the high end of a $52 billion to $56 billion range, representing a 37% increase compared to last year.

- Optimistic Industry Outlook: As market demand for AI technologies continues to rise, TSMC's robust performance not only solidifies its leadership position in the semiconductor industry but also lays a foundation for future investments and technological innovations.

See More

US Stocks Dip Slightly as Chipmakers Weigh on Market

- Market Performance: The S&P 500 index fell by 0.15%, the Dow Jones Industrial Average decreased by 0.06%, and the Nasdaq 100 dropped by 0.21%, indicating a slight market pullback after reaching new highs, particularly pressured by weakness in chipmakers.

- Economic Data: Initial jobless claims in the US fell by 11,000 to 207,000, indicating a stronger labor market than the expected 213,000; additionally, the Philadelphia Fed business outlook unexpectedly rose by 8.6 to a 15-month high of 26.7, reflecting potential economic recovery.

- Oil Price Fluctuations: WTI crude oil prices increased by over 1% as the US naval blockade of the Strait of Hormuz enters its fourth day, which could exacerbate global oil and fuel shortages, impacting future energy market stability.

- Earnings Season: Q1 earnings for the S&P 500 are projected to rise by 12% year-over-year, but excluding the technology sector, the earnings growth is only 3%, the lowest in two years, indicating a cautious market outlook on profit growth.

See More

ASML Valuation Anomaly Amid Market Dynamics

- Valuation Anomaly: ASML's relative pricing against US peers has fallen to its lowest level in a decade, currently trading at a forward P/E of 37 times, representing a 17% premium over Applied Materials, indicating a market reassessment of its valuation.

- Market Dynamics Shift: ASML is now priced at about a 5% discount to Lam Research for the first time in 14 years, despite its unique supply position in extreme ultraviolet lithography systems, reflecting cautious market sentiment regarding its future growth.

- Analyst Insights: JPMorgan analyst Sandeep Deshpande highlighted that ASML's valuation may be misaligned with its structural advantages, as the stock has risen 36% year-to-date but lags behind peers like Applied Materials and Lam Research, which have gained over 50%, suggesting that relative underperformance may be driving valuation compression.

- Mixed Market Reaction: Despite ASML raising its full-year sales guidance, the stock declined 4.2% on Wednesday, reflecting concerns over high expectations, while a 2.0% rebound on Thursday suggests that long-term AI-driven demand remains intact, but short-term performance may depend on the relationship between earnings growth and current valuation levels.

See More

Momentum Stocks Surge as Wall Street Optimism Grows

- Record for Momentum ETF: The iShares MSCI USA Momentum Factor ETF (MTUM) hit a new high on Thursday, marking its tenth consecutive winning session, reflecting strong market confidence in growth stocks and suggesting a potential upward trend for the overall market.

- Market Rebound Signs: MTUM, which was down over 7% year-to-date, has now risen 8%, coinciding with the S&P 500's recovery, indicating that the market may be experiencing a broader rebound as investor sentiment turns optimistic.

- Outstanding Stock Performance: Since the onset of the Iran war, Bloom Energy's stock has surged over 40%, while Intel has also risen more than 40%, showcasing the appeal of momentum stocks, particularly following expanded partnerships with major tech companies.

- Momentum Drives Market: Jeff Kilburg, founder of KKM Financial, emphasized that momentum is the primary driver of market gains, predicting that the S&P 500 will reach new all-time highs, with the return of momentum providing strong support for the market.

See More

Microsoft and Stellantis Forge Strategic AI Partnership

- Strategic Partnership: Microsoft and Stellantis have established a five-year strategic partnership aimed at co-developing AI and cybersecurity tools, with plans to launch over 100 AI initiatives, significantly enhancing technological competitiveness in the automotive sector.

- Cloud Migration: Stellantis is shifting its primary tech focus to Microsoft's Azure cloud platform, aiming for a 60% reduction in its physical data center footprint by 2029, which will streamline operations through modernized infrastructure.

- Digital Security Enhancement: The partnership integrates AI-driven analytics across manufacturing sites and connected vehicles to counter emerging cyber threats, thereby protecting the privacy of millions of drivers and enhancing brand trust.

- Positive Market Reaction: Microsoft's stock has surged 10% over the past three days, marking its strongest short-term rally since 2020, with analysts suggesting this indicates growing market confidence in AI integration.

See More

U.S. Stocks Edge Up as PepsiCo and TSMC Shine

- PepsiCo's Quarter Performance: PepsiCo achieved its first volume growth in North American food business in two years, with CEO Ramon Laguarta addressing the industry's threat from GLP-1 weight-loss drugs, leading to a 1% rise in shares, demonstrating the company's resilience and adaptability in a competitive consumer goods market.

- TSMC Profit Surge: TSMC reported a 58% year-over-year profit increase, despite facing challenges with shortages of industrial gases; management noted a 'little bit softer' memory pricing, indicating ongoing demand and competitive pressures in advanced chip manufacturing that could impact future profitability.

- J.B. Hunt Transport Services: J.B. Hunt indicated the start of a new cycle with positive demand signals, reporting a first-quarter earnings beat and a 1% premarket share increase, reflecting potential growth opportunities in the transportation sector.

- Analyst Rating Changes: JPMorgan downgraded Corning to hold and cut its price target from $175 to $115, citing the need for greater earnings visibility to support stock upside, indicating a cautious market outlook on the company's future performance.

See More

TSMC Profits Surge 58% Amid AI Chip Demand

- Profit Surge: TSMC reported a 58% year-over-year increase in net profit for the latest quarter, indicating strong demand for AI chips and minimal short-term impact from supply chain disruptions, with the stock slightly rising post-earnings release.

- Advanced Technology Revenue: Advanced technology products accounted for 74% of total wafer revenue, reflecting key customers like Apple’s preference for smaller nanometer products, which enhances the company's market share and competitive edge.

- Capacity Expansion: To meet the growing demand, TSMC plans to add production facilities in Taiwan, with capital expenditures expected to be at the high end of a $52 billion to $56 billion range, representing a 37% increase compared to last year.

- Optimistic Industry Outlook: As market demand for AI technologies continues to rise, TSMC's robust performance not only solidifies its leadership position in the semiconductor industry but also lays a foundation for future investments and technological innovations.

See More