GOOGLE DEVELOPING AI AGENT AS ITS RESPONSE TO OPENAI - BUSINESS INSIDER

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Should l Buy GOOG?

Source: moomoo

Google's New AI Agent: Google is developing an AI agent that may serve as a solution to open legal questions and challenges in the business sector.

Potential Impact on Business: This AI initiative could significantly influence how businesses navigate legal frameworks and compliance issues.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GOOG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GOOG

Wall Street analysts forecast GOOG stock price to fall

15 Analyst Rating

14 Buy

1 Hold

0 Sell

Strong Buy

Current: 395.140

Low

255.00

Averages

336.08

High

400.00

Current: 395.140

Low

255.00

Averages

336.08

High

400.00

About GOOG

Alphabet Inc. is a holding company. The Company's segments include Google Services, Google Cloud, and Other Bets. The Google Services segment includes products and services such as ads, Android, Chrome, devices, Google Maps, Google Play, Search, and YouTube. The Google Cloud segment includes infrastructure and platform services, collaboration tools, and other services for enterprise customers. Its Other Bets segment is engaged in the sale of healthcare-related services and Internet services. Its Google Cloud provides enterprise-ready cloud services, including Google Cloud Platform and Google Workspace. Google Cloud Platform provides access to solutions such as artificial intelligence (AI) offerings, including its AI infrastructure, Vertex AI platform, and Gemini for Google Cloud; cybersecurity, and data and analytics. Google Workspace includes cloud-based communication and collaboration tools for enterprises, such as Calendar, Gmail, Docs, Drive, and Meet.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

S&P 500 Q1 Earnings Exceed Expectations

- Earnings Growth Overview: The S&P 500 reported nearly 25% earnings growth in Q1, although analysts at Goldman Sachs noted that this figure may overstate the overall strength of corporate America, particularly due to significant contributions from investment activities at Amazon and Alphabet.

- Adjusted Earnings Data: After adjustments, Goldman estimates that underlying earnings growth for the S&P 500 is closer to 16%, which still reflects solid corporate profitability but indicates a notably slower pace than the headline data suggests, highlighting the importance of earnings quality.

- Market Influencing Factors: A few mega-cap technology companies heavily influence broader market statistics, especially during earnings season, leading investors to increasingly focus on the quality and sustainability of profit growth to assess future valuations and corporate spending outlook.

- Economic Outlook: As markets evaluate economic momentum and corporate spending prospects, there is a growing investor focus on the sustainability of earnings growth, particularly against a backdrop of global economic uncertainty and inflationary pressures.

See More

DoorDash's Revenue Miss Doesn't Detract from Strong Growth Story

- Significant Revenue Growth: DoorDash's Q1 revenue increased by 33% year-over-year to $4.04 billion, largely driven by the acquisition of Deliveroo, showcasing the company's strong performance in market expansion.

- Order Volume Surge: Total orders rose by 27% to 933 million, with marketplace gross order value jumping 37% to $31.6 billion, indicating that the company is not only adding orders but also capturing larger ones, particularly in the fast-growing grocery and retail categories.

- Profit Pressure Intensifies: Despite revenue growth, diluted EPS fell from $0.44 to $0.42, primarily due to integration costs from Deliveroo and ongoing investments in autonomous delivery, highlighting the profit pressures faced during expansion.

- Optimistic Future Outlook: Management maintained its full-year outlook, expecting modest margin gains, although heavy investment will continue, indicating the company's need to prove that these investments can translate into operational leverage.

See More

SpaceX IPO Could Spark Transformation in Self-Driving Technology

- Valuation Expectations: SpaceX is set to go public with a valuation between $1.5 trillion and $2 trillion, aiming to raise $50 billion to $75 billion in fresh capital through its IPO, which will significantly bolster the company's growth prospects.

- Retail Investor Participation: Founder Elon Musk intends to reserve up to 30% of shares for retail investors, allowing the general public easy access to invest in SpaceX, thereby enhancing market engagement and public awareness.

- Rivian's Potential Gains: Rivian, a direct competitor to Tesla, is expected to benefit from the SpaceX IPO, particularly in its investments in self-driving technology and artificial intelligence, which could accelerate its market growth.

- Increased Industry Competition: Following the SpaceX IPO, Tesla's self-driving ambitions will likely accelerate, prompting competitors like Alphabet and Uber to ramp up their investments, further intensifying competition and technological advancements in the electric vehicle market.

See More

Alphabet Poised to Become World's Most Valuable Company

- Stock Surge: Alphabet's first-quarter results exceeded expectations, leading to a 10% stock price increase and a market cap nearing $4.8 trillion, indicating strong performance in the global market and a potential to surpass Nvidia's market cap of over $5 trillion soon.

- Significant Cloud Growth: Google Cloud achieved a 63% year-over-year growth rate in Q1, a substantial increase from 48% in the previous quarter, with a $460 billion backlog indicating strong revenue visibility, directly contributing to an 81% increase in Alphabet's net income.

- Improved Profitability: Alphabet's revenue for 2025 reached $402.8 billion with a net income of $132.2 billion, both surpassing Nvidia's $215.9 billion and $120.1 billion, suggesting that its profitability is rapidly improving and may allow it to overtake Nvidia in the coming months.

- Diversified Business Potential: Beyond cloud computing, Alphabet's online advertising and emerging businesses like Waymo are also growing rapidly, with Waymo surpassing 500,000 fully autonomous rides per week, indicating its potential in the autonomous driving market and future significant revenue growth for the company.

See More

Alphabet's Soaring Cloud Revenue Reflects Significant AI Investment Returns

- Cloud Growth: Alphabet's Google Cloud achieved a 63% year-over-year growth rate in Q1 2025, a significant increase from 48% in Q4 2025, indicating strong revenue growth potential that is expected to enhance its market share further.

- Profit Surge: Alphabet's net income rose by 81% to $62.6 billion, demonstrating that its revenue growth is directly translating into higher profits, thereby strengthening its financial position in competition with Nvidia.

- Waymo and Gemini Potential: Waymo surpassing 500,000 fully autonomous rides per week and Gemini's 40% growth in enterprise users indicate that these smaller segments could become significant revenue drivers for Alphabet in the long run, despite their current nascent stage.

- Capital Expenditure Flexibility: With $126.8 billion in cash and cash equivalents at the end of Q1, Alphabet's strong financial foundation allows it to continue investing in AI and accelerate market penetration, positioning it to outpace competitors.

See More

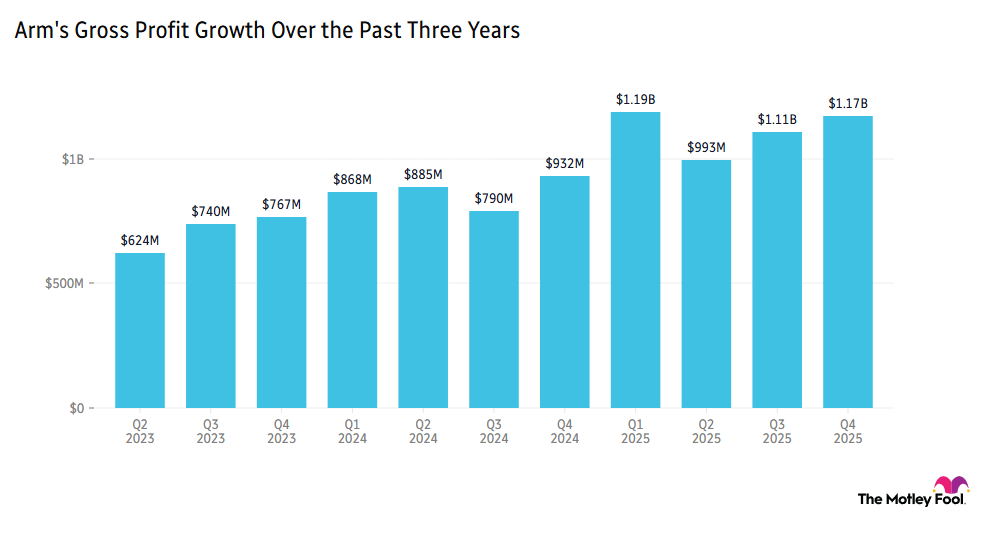

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More

S&P 500 Q1 Earnings Exceed Expectations

- Earnings Growth Overview: The S&P 500 reported nearly 25% earnings growth in Q1, although analysts at Goldman Sachs noted that this figure may overstate the overall strength of corporate America, particularly due to significant contributions from investment activities at Amazon and Alphabet.

- Adjusted Earnings Data: After adjustments, Goldman estimates that underlying earnings growth for the S&P 500 is closer to 16%, which still reflects solid corporate profitability but indicates a notably slower pace than the headline data suggests, highlighting the importance of earnings quality.

- Market Influencing Factors: A few mega-cap technology companies heavily influence broader market statistics, especially during earnings season, leading investors to increasingly focus on the quality and sustainability of profit growth to assess future valuations and corporate spending outlook.

- Economic Outlook: As markets evaluate economic momentum and corporate spending prospects, there is a growing investor focus on the sustainability of earnings growth, particularly against a backdrop of global economic uncertainty and inflationary pressures.

See More

DoorDash's Revenue Miss Doesn't Detract from Strong Growth Story

- Significant Revenue Growth: DoorDash's Q1 revenue increased by 33% year-over-year to $4.04 billion, largely driven by the acquisition of Deliveroo, showcasing the company's strong performance in market expansion.

- Order Volume Surge: Total orders rose by 27% to 933 million, with marketplace gross order value jumping 37% to $31.6 billion, indicating that the company is not only adding orders but also capturing larger ones, particularly in the fast-growing grocery and retail categories.

- Profit Pressure Intensifies: Despite revenue growth, diluted EPS fell from $0.44 to $0.42, primarily due to integration costs from Deliveroo and ongoing investments in autonomous delivery, highlighting the profit pressures faced during expansion.

- Optimistic Future Outlook: Management maintained its full-year outlook, expecting modest margin gains, although heavy investment will continue, indicating the company's need to prove that these investments can translate into operational leverage.

See More

SpaceX IPO Could Spark Transformation in Self-Driving Technology

- Valuation Expectations: SpaceX is set to go public with a valuation between $1.5 trillion and $2 trillion, aiming to raise $50 billion to $75 billion in fresh capital through its IPO, which will significantly bolster the company's growth prospects.

- Retail Investor Participation: Founder Elon Musk intends to reserve up to 30% of shares for retail investors, allowing the general public easy access to invest in SpaceX, thereby enhancing market engagement and public awareness.

- Rivian's Potential Gains: Rivian, a direct competitor to Tesla, is expected to benefit from the SpaceX IPO, particularly in its investments in self-driving technology and artificial intelligence, which could accelerate its market growth.

- Increased Industry Competition: Following the SpaceX IPO, Tesla's self-driving ambitions will likely accelerate, prompting competitors like Alphabet and Uber to ramp up their investments, further intensifying competition and technological advancements in the electric vehicle market.

See More

Alphabet Poised to Become World's Most Valuable Company

- Stock Surge: Alphabet's first-quarter results exceeded expectations, leading to a 10% stock price increase and a market cap nearing $4.8 trillion, indicating strong performance in the global market and a potential to surpass Nvidia's market cap of over $5 trillion soon.

- Significant Cloud Growth: Google Cloud achieved a 63% year-over-year growth rate in Q1, a substantial increase from 48% in the previous quarter, with a $460 billion backlog indicating strong revenue visibility, directly contributing to an 81% increase in Alphabet's net income.

- Improved Profitability: Alphabet's revenue for 2025 reached $402.8 billion with a net income of $132.2 billion, both surpassing Nvidia's $215.9 billion and $120.1 billion, suggesting that its profitability is rapidly improving and may allow it to overtake Nvidia in the coming months.

- Diversified Business Potential: Beyond cloud computing, Alphabet's online advertising and emerging businesses like Waymo are also growing rapidly, with Waymo surpassing 500,000 fully autonomous rides per week, indicating its potential in the autonomous driving market and future significant revenue growth for the company.

See More

Alphabet's Soaring Cloud Revenue Reflects Significant AI Investment Returns

- Cloud Growth: Alphabet's Google Cloud achieved a 63% year-over-year growth rate in Q1 2025, a significant increase from 48% in Q4 2025, indicating strong revenue growth potential that is expected to enhance its market share further.

- Profit Surge: Alphabet's net income rose by 81% to $62.6 billion, demonstrating that its revenue growth is directly translating into higher profits, thereby strengthening its financial position in competition with Nvidia.

- Waymo and Gemini Potential: Waymo surpassing 500,000 fully autonomous rides per week and Gemini's 40% growth in enterprise users indicate that these smaller segments could become significant revenue drivers for Alphabet in the long run, despite their current nascent stage.

- Capital Expenditure Flexibility: With $126.8 billion in cash and cash equivalents at the end of Q1, Alphabet's strong financial foundation allows it to continue investing in AI and accelerate market penetration, positioning it to outpace competitors.

See More

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More