Micron Stock Hits All-Time High, Analysts Bullish on Future

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 27 2026

0mins

Should l Buy MU?

Source: Fool

- Stock Surge: Micron's stock closed last week at $497 per share and jumped 4.8% on Monday morning, indicating strong market demand and investor confidence, reflecting the company's leadership in the semiconductor industry.

- Analyst Rating: Melius Research rated Micron as a 'buy' with a price target of $700, projecting a 41% increase in stock price over the next 12 months, indicating optimistic expectations regarding its profitability.

- Earnings Potential: Micron has been profitable in four of the last five years, with last year's earnings at $7.59 per share expected to grow by 660% this year, potentially reaching $98 by 2027, showcasing strong earnings growth potential.

- Market Outlook: Despite the cyclical nature of the semiconductor industry, analysts believe that Micron's unusual demand for high-bandwidth memory and profit margins may allow it to sustain growth in the coming years, leading investors to maintain a positive outlook on its future performance.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MU?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MU

Wall Street analysts forecast MU stock price to fall

26 Analyst Rating

24 Buy

2 Hold

0 Sell

Strong Buy

Current: 666.590

Low

235.00

Averages

336.12

High

500.00

Current: 666.590

Low

235.00

Averages

336.12

High

500.00

About MU

Micron Technology, Inc. provides memory and storage solutions. The Company delivers a portfolio of high-performance dynamic random-access memory (DRAM), NAND, and NOR memory and storage products through its Micron and Crucial brands. The Company's products enable advancing in artificial intelligence (AI) and compute-intensive applications. Its segments include Cloud Memory Business Unit (CMBU), Core Data Center Business Unit (CDBU), Mobile and Client Business Unit (MCBU) and Automotive and Embedded Business Unit (AEBU). CMBU is focused on memory solutions for large hyperscale cloud customers, and high bandwidth memory (HBM) for all data center customers. CDBU is focused on memory solutions for mid-tier cloud, enterprise, and OEM data center customers and storage solutions for all data center customers. MCBU is focused on memory and storage solutions for mobile and client segments. AEBU is focused on memory and storage solutions for the automotive, industrial, and consumer segments.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

DoorDash's Revenue Miss Doesn't Detract from Strong Growth Story

- Significant Revenue Growth: DoorDash's Q1 revenue increased by 33% year-over-year to $4.04 billion, largely driven by the acquisition of Deliveroo, showcasing the company's strong performance in market expansion.

- Order Volume Surge: Total orders rose by 27% to 933 million, with marketplace gross order value jumping 37% to $31.6 billion, indicating that the company is not only adding orders but also capturing larger ones, particularly in the fast-growing grocery and retail categories.

- Profit Pressure Intensifies: Despite revenue growth, diluted EPS fell from $0.44 to $0.42, primarily due to integration costs from Deliveroo and ongoing investments in autonomous delivery, highlighting the profit pressures faced during expansion.

- Optimistic Future Outlook: Management maintained its full-year outlook, expecting modest margin gains, although heavy investment will continue, indicating the company's need to prove that these investments can translate into operational leverage.

See More

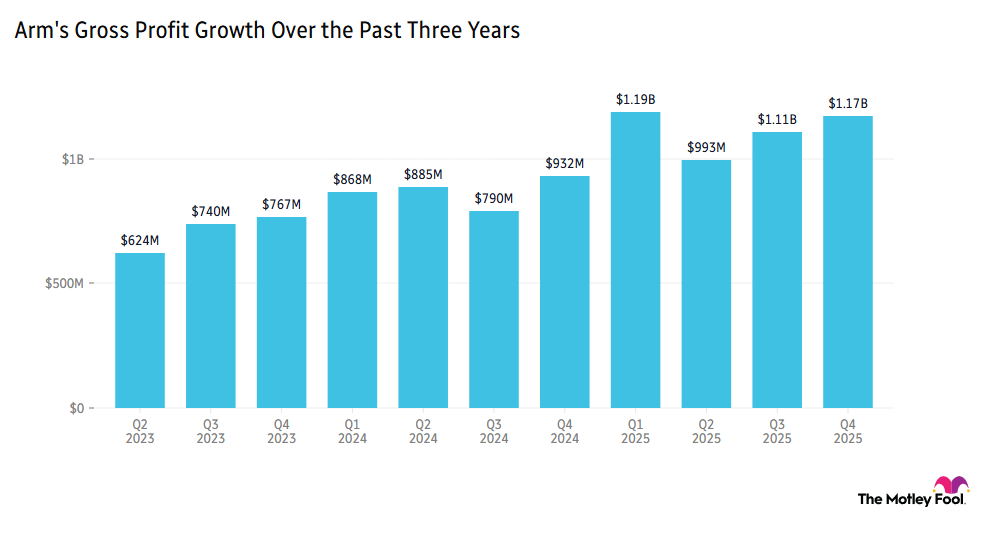

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More

AI Stocks Thrive Amid Market Uncertainty

- Valuation Concerns: The S&P 500 Shiller CAPE ratio has climbed to 40, indicating that stock valuations have reached historical highs similar to the dot-com bubble in 2000; however, the market did not crash, and many tech stocks have significantly rebounded after the first quarter.

- Giant Investments: Tech giants have committed nearly $700 billion in 2023 to support AI infrastructure, with Amazon planning to invest about $200 billion to meet AI customer demands for cloud services, a strategic investment expected to drive future revenue growth.

- Spending vs. Revenue Growth: Amazon's recent shareholder letter indicates that its capital spending will be monetized over the next two years based on solid customer commitments, alleviating investor concerns about spending not matching revenue opportunities and demonstrating strong market demand.

- Market Rebound: Despite uncertainties like the war in Iran, AI stocks have rebounded due to improved valuations and strong earnings; with progress toward a peace agreement, the market outlook is becoming more favorable, further boosting investor confidence in AI stocks.

See More

AI Stocks Rebound Amid Market Challenges

- Valuation Pressure: The S&P 500 Shiller CAPE ratio has climbed to 40, indicating that stock valuations have reached historical highs similar to the dot-com bubble in 2000, which has heightened investor concerns about AI stocks, although the market has not crashed.

- Massive Investment Commitments: Tech giants have pledged nearly $700 billion in 2023 to support AI infrastructure, with Amazon planning to invest about $200 billion to meet AI customer demands, positioning this spending as crucial for driving future revenue growth.

- Revenue Growth Signals: Amazon's recent shareholder letter indicates that much of its 2026 capital spending will be monetized over the next two years based on solid customer commitments, demonstrating the effectiveness of its investments and strong market demand, alleviating investor concerns.

- Improving Market Environment: Despite the uncertainty caused by the war in Iran, which led investors to shift towards safer stocks, AI stocks have rebounded recently as valuations improved and earnings showed strength, highlighting their long-term growth potential and attracting renewed investor interest.

See More

Apple Considers Intel for Future Chip Production

- Apple Chip Collaboration Potential: Apple is considering utilizing Intel's U.S. foundries for future iPhone and Mac chips, which is seen as an endorsement of Intel's manufacturing turnaround strategy and could further enhance Intel's market performance.

- AMD Strong Earnings: AMD reported quarterly revenue of $10.3 billion, a 38% year-over-year increase, with data center revenue reaching $5.8 billion, up 57%, indicating strong demand from enterprise customers for its EPYC processors and Instinct AI accelerators.

- Micron Market Value Surge: Micron's market value surpassed $700 billion for the first time, reflecting tight global supply of memory components driven by sustained AI-related demand, further solidifying its leadership position in the semiconductor industry.

- Chip Sector Rally: Stocks of Intel, AMD, and Micron all reached 52-week highs on Wednesday, as investor enthusiasm surged for chipmakers linked to AI infrastructure, boosting overall positive sentiment across the industry.

See More

Potential Semiconductor Sector Rebound Opportunities

- Semiconductor Sector Dynamics: According to Citrini Research's theory, investors should focus on semiconductor stocks that have not surged yet, particularly those with market caps above $300 million and trading at lower historical valuations, potentially offering profit opportunities.

- Intel's Recovery Signs: Intel reported a 7% revenue increase in its latest earnings report and guided for 11% growth in Q2, indicating market confidence in the semiconductor sector despite its growth numbers not being particularly strong, which has driven a rebound in its stock price.

- Wolfspeed's Financial Improvement: After reducing its debt burden by 70%, Wolfspeed, despite still being in the red, has seen its stock surge over the past month due to growth in its AI data center applications business, suggesting that high-risk stocks may still hold investment potential.

- Skyworks' Market Challenges: Skyworks reported essentially flat revenue growth in its most recent quarter and faces challenges from a weak smartphone market, although its potential growth in Edge AI could present future opportunities, making it a stock to watch for investors.

See More

DoorDash's Revenue Miss Doesn't Detract from Strong Growth Story

- Significant Revenue Growth: DoorDash's Q1 revenue increased by 33% year-over-year to $4.04 billion, largely driven by the acquisition of Deliveroo, showcasing the company's strong performance in market expansion.

- Order Volume Surge: Total orders rose by 27% to 933 million, with marketplace gross order value jumping 37% to $31.6 billion, indicating that the company is not only adding orders but also capturing larger ones, particularly in the fast-growing grocery and retail categories.

- Profit Pressure Intensifies: Despite revenue growth, diluted EPS fell from $0.44 to $0.42, primarily due to integration costs from Deliveroo and ongoing investments in autonomous delivery, highlighting the profit pressures faced during expansion.

- Optimistic Future Outlook: Management maintained its full-year outlook, expecting modest margin gains, although heavy investment will continue, indicating the company's need to prove that these investments can translate into operational leverage.

See More

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More

AI Stocks Thrive Amid Market Uncertainty

- Valuation Concerns: The S&P 500 Shiller CAPE ratio has climbed to 40, indicating that stock valuations have reached historical highs similar to the dot-com bubble in 2000; however, the market did not crash, and many tech stocks have significantly rebounded after the first quarter.

- Giant Investments: Tech giants have committed nearly $700 billion in 2023 to support AI infrastructure, with Amazon planning to invest about $200 billion to meet AI customer demands for cloud services, a strategic investment expected to drive future revenue growth.

- Spending vs. Revenue Growth: Amazon's recent shareholder letter indicates that its capital spending will be monetized over the next two years based on solid customer commitments, alleviating investor concerns about spending not matching revenue opportunities and demonstrating strong market demand.

- Market Rebound: Despite uncertainties like the war in Iran, AI stocks have rebounded due to improved valuations and strong earnings; with progress toward a peace agreement, the market outlook is becoming more favorable, further boosting investor confidence in AI stocks.

See More

AI Stocks Rebound Amid Market Challenges

- Valuation Pressure: The S&P 500 Shiller CAPE ratio has climbed to 40, indicating that stock valuations have reached historical highs similar to the dot-com bubble in 2000, which has heightened investor concerns about AI stocks, although the market has not crashed.

- Massive Investment Commitments: Tech giants have pledged nearly $700 billion in 2023 to support AI infrastructure, with Amazon planning to invest about $200 billion to meet AI customer demands, positioning this spending as crucial for driving future revenue growth.

- Revenue Growth Signals: Amazon's recent shareholder letter indicates that much of its 2026 capital spending will be monetized over the next two years based on solid customer commitments, demonstrating the effectiveness of its investments and strong market demand, alleviating investor concerns.

- Improving Market Environment: Despite the uncertainty caused by the war in Iran, which led investors to shift towards safer stocks, AI stocks have rebounded recently as valuations improved and earnings showed strength, highlighting their long-term growth potential and attracting renewed investor interest.

See More

Apple Considers Intel for Future Chip Production

- Apple Chip Collaboration Potential: Apple is considering utilizing Intel's U.S. foundries for future iPhone and Mac chips, which is seen as an endorsement of Intel's manufacturing turnaround strategy and could further enhance Intel's market performance.

- AMD Strong Earnings: AMD reported quarterly revenue of $10.3 billion, a 38% year-over-year increase, with data center revenue reaching $5.8 billion, up 57%, indicating strong demand from enterprise customers for its EPYC processors and Instinct AI accelerators.

- Micron Market Value Surge: Micron's market value surpassed $700 billion for the first time, reflecting tight global supply of memory components driven by sustained AI-related demand, further solidifying its leadership position in the semiconductor industry.

- Chip Sector Rally: Stocks of Intel, AMD, and Micron all reached 52-week highs on Wednesday, as investor enthusiasm surged for chipmakers linked to AI infrastructure, boosting overall positive sentiment across the industry.

See More

Potential Semiconductor Sector Rebound Opportunities

- Semiconductor Sector Dynamics: According to Citrini Research's theory, investors should focus on semiconductor stocks that have not surged yet, particularly those with market caps above $300 million and trading at lower historical valuations, potentially offering profit opportunities.

- Intel's Recovery Signs: Intel reported a 7% revenue increase in its latest earnings report and guided for 11% growth in Q2, indicating market confidence in the semiconductor sector despite its growth numbers not being particularly strong, which has driven a rebound in its stock price.

- Wolfspeed's Financial Improvement: After reducing its debt burden by 70%, Wolfspeed, despite still being in the red, has seen its stock surge over the past month due to growth in its AI data center applications business, suggesting that high-risk stocks may still hold investment potential.

- Skyworks' Market Challenges: Skyworks reported essentially flat revenue growth in its most recent quarter and faces challenges from a weak smartphone market, although its potential growth in Edge AI could present future opportunities, making it a stock to watch for investors.

See More