IBM Fails to Raise Full-Year Guidance, Shares Drop

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 17 hours ago

0mins

Should l Buy IBM?

Source: CNBC

- IBM Earnings Miss: IBM reported Q1 earnings of $1.91 per share, beating the $1.81 forecast, yet failed to raise its full-year guidance, resulting in a 6% drop in shares, indicating market concerns over future growth prospects.

- Tesla's Mixed Results: Tesla's Q1 adjusted earnings were 41 cents per share, surpassing the 37 cents expected by analysts, but its revenue of $22.39 billion fell short of the $22.64 billion consensus, reflecting cautious market sentiment regarding sales growth.

- Texas Instruments Strong Outlook: Texas Instruments forecasts current-quarter earnings between $1.77 and $2.05 per share, significantly above the $1.57 consensus, leading to a 10% increase in shares, showcasing robust demand in the semiconductor sector.

- United Rentals Sales Forecast Boost: United Rentals raised its full-year sales forecast to a range of $16.9 billion to $17.4 billion, with shares jumping over 15%, indicating strong market momentum heading into the busy season.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy IBM?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on IBM

Wall Street analysts forecast IBM stock price to rise

16 Analyst Rating

11 Buy

4 Hold

1 Sell

Moderate Buy

Current: 251.860

Low

210.00

Averages

315.80

High

375.00

Current: 251.860

Low

210.00

Averages

315.80

High

375.00

About IBM

International Business Machines Corporation is a provider of global hybrid cloud and artificial intelligence (AI) and consulting expertise. The Company’s segments include Software, Consulting, Infrastructure and Financing. The Software segment includes hybrid cloud and AI platforms, which allow clients to realize their digital and AI transformations across the applications, data, and environments in which they operate. The Consulting segment focuses on integrating skills on strategy, experience, technology and operations by domain and industry. The Infrastructure segment is focused on the hybrid cloud infrastructure market, providing on-premises and cloud-based server and storage solutions. In addition, it offers a portfolio of life-cycle services for hybrid cloud infrastructure deployment. The Financing segment provides client and commercial financing, facilitating its clients’ acquisition of hardware, software and services. It helps clients in more than 175 countries.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Netflix Authorizes $25 Billion Buyback Program to Boost Shareholder Confidence

- Strategic Shift: Netflix has authorized a $25 billion share buyback program, marking a strategic pivot from mega-mergers to shareholder returns, aimed at boosting investor confidence in light of a tepid Q2 forecast.

- Strong Cash Reserves: The company currently holds $12.3 billion in cash, bolstered by a $2.8 billion breakup fee from Paramount Skydance, providing robust funding for the buyback plan and reflecting management's belief that shares are undervalued.

- Advertising Revenue Potential: Analysts expect Netflix's ad-supported segment to double revenue to $3 billion by 2026, effectively offsetting slowing subscriber growth in mature markets like the U.S. and Canada, thereby enhancing the company's long-term profitability.

- Price Recovery Expectations: Following a 10% post-earnings dip, Netflix's stock price is around $94, and the management's buyback plan is seen as a strong signal for price recovery, likely attracting more investor interest.

See More

Latest Wall Street Rating Updates

- Tesla Buy Rating: Bank of America reiterates Tesla as a buy, viewing the company as a leader in consumer autonomy and expecting it to quickly become a leader in robotaxi services, highlighting its strong potential in the future mobility market.

- Nvidia Market Leadership: TD Cowen maintains Nvidia as a buy despite Google's launch of competing AI chips, believing Nvidia remains the market leader in performance and software ecosystem breadth, indicating its sustained competitive advantage in the AI sector.

- Berkshire Target Price Increase: UBS raises Berkshire Hathaway's price target from $578 to $581, noting that the stock is trading at a discount to its intrinsic value and anticipating continued share repurchases, which could influence investor sentiment positively.

- IBM Defensive Investment: Bank of America reiterates IBM as a buy, citing its high exposure to recurring sales and solid balance sheet as factors that make it a defensive investment, demonstrating stability and growth potential in an uncertain market environment.

See More

Stock Futures Dip Modestly After Record Highs; Texas Instruments Shines

- Texas Instruments Earnings Surge: Texas Instruments has eliminated the overhang on its industrial business, with its data center segment growing 90% year-over-year, and a strong second-quarter guide has led to a premarket share price increase of over 10%, reflecting market confidence in its growth trajectory.

- Honeywell's Disappointing Quarter: Honeywell reported a messy quarter, causing its shares to drop over 5% in premarket trading; however, the upcoming aerospace spin-off scheduled for June 29 keeps long-term investors optimistic about its future potential.

- ServiceNow Shares Plummet: Following a noisy earnings report, ServiceNow's shares fell nearly 14% in premarket trading, as the market expressed concerns over slowed growth and high AI costs, prompting KeyBanc and Jefferies to lower their price targets significantly.

- IBM Revenue Growth Deceleration: IBM's first-quarter revenue growth slowed to 9% from 12% in the previous quarter, raising investor concerns about its future prospects, leading to a premarket decline of over 7% in its stock price, as doubts linger about the effectiveness of its AI tools in maintaining revenue streams.

See More

IBM Shares Drop 8% on Prudent Guidance Despite Strong Earnings Report

- Earnings Beat: IBM reported its FY1Q26 results with both revenue and earnings per share exceeding expectations, while maintaining its guidance for FY26 revenue and free cash flow, indicating a prudent approach amidst macroeconomic pressures.

- Price Target Reduction: Wedbush maintained its Outperform rating on IBM but lowered the price target from $340 to $320, reflecting considerations of approximately $600 million in Confluent dilution and near-term softness in consulting services.

- Software Growth Outlook: IBM anticipates a 10% year-over-year growth in its software vertical for 2026, and analysts noted the company's strong positioning to capitalize on AI demand, leveraging its diversified portfolio and innovation investments to expand margins.

- Market Reaction: Despite the strong earnings report, analysts indicated that investor expectations for upward pressure on full-year estimates did not materialize, leading to an approximately 8% drop in premarket trading, reflecting market caution regarding future growth.

See More

IBM Shares Drop Amid Inflation and Geopolitical Concerns

- Strong Earnings but Cautious Outlook: IBM's quarterly results exceeded revenue and earnings expectations; however, the stock fell over 7% pre-market due to cautious full-year guidance, with CEO Arvind Krishna attributing this to broader geopolitical uncertainties, indicating market concerns about future performance.

- Inflation's Impact on Client Spending: Krishna highlighted that inflation could lead to reduced consumer spending at clients like Walmart, indirectly affecting IBM's business activity, reflecting the potential threats economic conditions pose to tech companies.

- Dual Impact of AI Tools: IBM's consulting business faces threats from more sophisticated AI tools, although TMF's CIO Andy Cross noted that mainframes remain essential infrastructure for complex computing systems, suggesting that AI's impact on the industry is multifaceted.

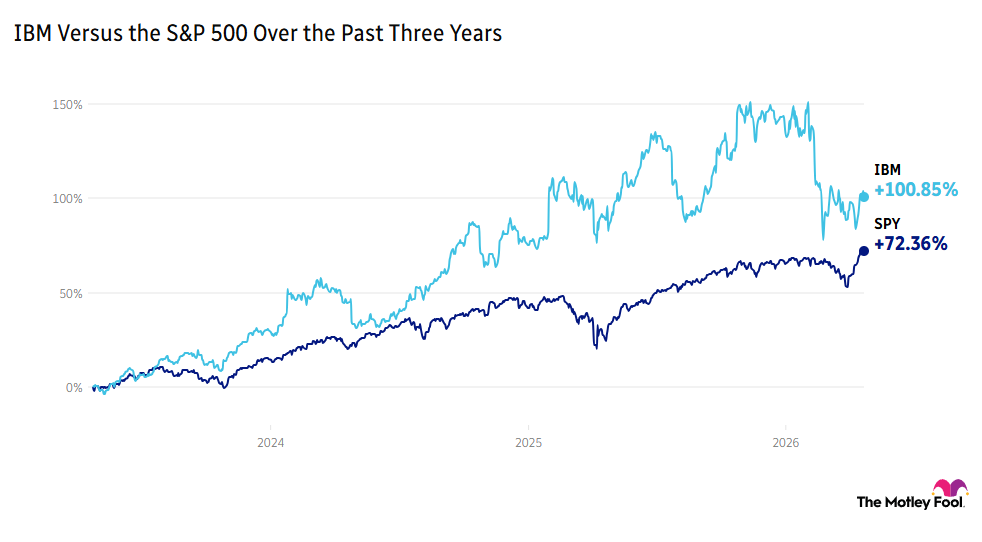

- Long-term Performance vs. Market Comparison: While IBM has risen 85% over the past five years, outperforming the S&P 500's 70% increase, the stock is down 15% this year, including its worst single-day drop in over 25 years, indicating that advancements in AI may be fundamentally altering the investment case.

See More

Analysis of Significant Stock Movements Among Companies

- Netflix Buyback Plan: Netflix authorized an additional $25 billion share buyback, leading to a stock price increase of over 1%, aimed at boosting shareholder confidence and enhancing long-term company value.

- Helix Merger Announcement: Helix Energy Solutions agreed to merge with Hornbeck Offshore Services in an all-stock deal, resulting in a more than 3% rise in stock price, with the merger expected to close in the second half of 2026, enhancing competitive positioning in the offshore services market.

- Honeywell Mixed Earnings: Honeywell reported Q1 adjusted earnings of $2.45 per share, beating expectations, but revenue of $9.1 billion fell short of forecasts, causing a 5.6% drop in stock price, reflecting market concerns over its future guidance.

- Mobileye Strong Performance: Mobileye reported Q1 adjusted earnings of 12 cents per share on revenue of $558 million, both exceeding analyst expectations, resulting in an 11% stock price increase, indicating robust growth potential in the autonomous driving sector.

See More

Netflix Authorizes $25 Billion Buyback Program to Boost Shareholder Confidence

- Strategic Shift: Netflix has authorized a $25 billion share buyback program, marking a strategic pivot from mega-mergers to shareholder returns, aimed at boosting investor confidence in light of a tepid Q2 forecast.

- Strong Cash Reserves: The company currently holds $12.3 billion in cash, bolstered by a $2.8 billion breakup fee from Paramount Skydance, providing robust funding for the buyback plan and reflecting management's belief that shares are undervalued.

- Advertising Revenue Potential: Analysts expect Netflix's ad-supported segment to double revenue to $3 billion by 2026, effectively offsetting slowing subscriber growth in mature markets like the U.S. and Canada, thereby enhancing the company's long-term profitability.

- Price Recovery Expectations: Following a 10% post-earnings dip, Netflix's stock price is around $94, and the management's buyback plan is seen as a strong signal for price recovery, likely attracting more investor interest.

See More

Latest Wall Street Rating Updates

- Tesla Buy Rating: Bank of America reiterates Tesla as a buy, viewing the company as a leader in consumer autonomy and expecting it to quickly become a leader in robotaxi services, highlighting its strong potential in the future mobility market.

- Nvidia Market Leadership: TD Cowen maintains Nvidia as a buy despite Google's launch of competing AI chips, believing Nvidia remains the market leader in performance and software ecosystem breadth, indicating its sustained competitive advantage in the AI sector.

- Berkshire Target Price Increase: UBS raises Berkshire Hathaway's price target from $578 to $581, noting that the stock is trading at a discount to its intrinsic value and anticipating continued share repurchases, which could influence investor sentiment positively.

- IBM Defensive Investment: Bank of America reiterates IBM as a buy, citing its high exposure to recurring sales and solid balance sheet as factors that make it a defensive investment, demonstrating stability and growth potential in an uncertain market environment.

See More

Stock Futures Dip Modestly After Record Highs; Texas Instruments Shines

- Texas Instruments Earnings Surge: Texas Instruments has eliminated the overhang on its industrial business, with its data center segment growing 90% year-over-year, and a strong second-quarter guide has led to a premarket share price increase of over 10%, reflecting market confidence in its growth trajectory.

- Honeywell's Disappointing Quarter: Honeywell reported a messy quarter, causing its shares to drop over 5% in premarket trading; however, the upcoming aerospace spin-off scheduled for June 29 keeps long-term investors optimistic about its future potential.

- ServiceNow Shares Plummet: Following a noisy earnings report, ServiceNow's shares fell nearly 14% in premarket trading, as the market expressed concerns over slowed growth and high AI costs, prompting KeyBanc and Jefferies to lower their price targets significantly.

- IBM Revenue Growth Deceleration: IBM's first-quarter revenue growth slowed to 9% from 12% in the previous quarter, raising investor concerns about its future prospects, leading to a premarket decline of over 7% in its stock price, as doubts linger about the effectiveness of its AI tools in maintaining revenue streams.

See More

IBM Shares Drop 8% on Prudent Guidance Despite Strong Earnings Report

- Earnings Beat: IBM reported its FY1Q26 results with both revenue and earnings per share exceeding expectations, while maintaining its guidance for FY26 revenue and free cash flow, indicating a prudent approach amidst macroeconomic pressures.

- Price Target Reduction: Wedbush maintained its Outperform rating on IBM but lowered the price target from $340 to $320, reflecting considerations of approximately $600 million in Confluent dilution and near-term softness in consulting services.

- Software Growth Outlook: IBM anticipates a 10% year-over-year growth in its software vertical for 2026, and analysts noted the company's strong positioning to capitalize on AI demand, leveraging its diversified portfolio and innovation investments to expand margins.

- Market Reaction: Despite the strong earnings report, analysts indicated that investor expectations for upward pressure on full-year estimates did not materialize, leading to an approximately 8% drop in premarket trading, reflecting market caution regarding future growth.

See More

IBM Shares Drop Amid Inflation and Geopolitical Concerns

- Strong Earnings but Cautious Outlook: IBM's quarterly results exceeded revenue and earnings expectations; however, the stock fell over 7% pre-market due to cautious full-year guidance, with CEO Arvind Krishna attributing this to broader geopolitical uncertainties, indicating market concerns about future performance.

- Inflation's Impact on Client Spending: Krishna highlighted that inflation could lead to reduced consumer spending at clients like Walmart, indirectly affecting IBM's business activity, reflecting the potential threats economic conditions pose to tech companies.

- Dual Impact of AI Tools: IBM's consulting business faces threats from more sophisticated AI tools, although TMF's CIO Andy Cross noted that mainframes remain essential infrastructure for complex computing systems, suggesting that AI's impact on the industry is multifaceted.

- Long-term Performance vs. Market Comparison: While IBM has risen 85% over the past five years, outperforming the S&P 500's 70% increase, the stock is down 15% this year, including its worst single-day drop in over 25 years, indicating that advancements in AI may be fundamentally altering the investment case.

See More

Analysis of Significant Stock Movements Among Companies

- Netflix Buyback Plan: Netflix authorized an additional $25 billion share buyback, leading to a stock price increase of over 1%, aimed at boosting shareholder confidence and enhancing long-term company value.

- Helix Merger Announcement: Helix Energy Solutions agreed to merge with Hornbeck Offshore Services in an all-stock deal, resulting in a more than 3% rise in stock price, with the merger expected to close in the second half of 2026, enhancing competitive positioning in the offshore services market.

- Honeywell Mixed Earnings: Honeywell reported Q1 adjusted earnings of $2.45 per share, beating expectations, but revenue of $9.1 billion fell short of forecasts, causing a 5.6% drop in stock price, reflecting market concerns over its future guidance.

- Mobileye Strong Performance: Mobileye reported Q1 adjusted earnings of 12 cents per share on revenue of $558 million, both exceeding analyst expectations, resulting in an 11% stock price increase, indicating robust growth potential in the autonomous driving sector.

See More