WMT Overview

-

$

0.000

0.000(0.000%)

At close0.000(0.000%)Aft-market

ET

Loading chart...

The current price of WMT is 113.1 USD — it has increased 1.4

Walmart Inc. is a technology-powered omnichannel retailer. The Company is engaged in the operation of retail and wholesale stores and clubs, as well as eCommerce Websites and mobile applications, located throughout the United States (U.S.), Africa, Canada, Central America, Chile, China, India and Mexico. It operates in three reportable segments: Walmart U.S., Walmart International and Sam's Club U.S. The Walmart U.S. segment includes the Company's mass merchandising concept in the U.S., as well as eCommerce, which includes omni-channel initiatives and certain other business offerings such as advertising services. The Walmart International segment consists of the Company's operations outside of the U.S. through its subsidiaries, as well as eCommerce and omni-channel initiatives. The Sam's Club U.S. segment includes the warehouse membership clubs in the U.S., as well as samsclub.com and omni-channel initiatives.

Wall Street analysts forecast WMT stock price to rise over the next 12 months. According to Wall Street analysts, the average 1-year price target for WMT is125.75 USD with a low forecast of 119.00 USD and a high forecast of 136.00 USD. However, analyst price targets are subjective and often lag stock prices, so investors should focus on the objective reasons behind analyst rating changes, which better reflect the company's fundamentals.

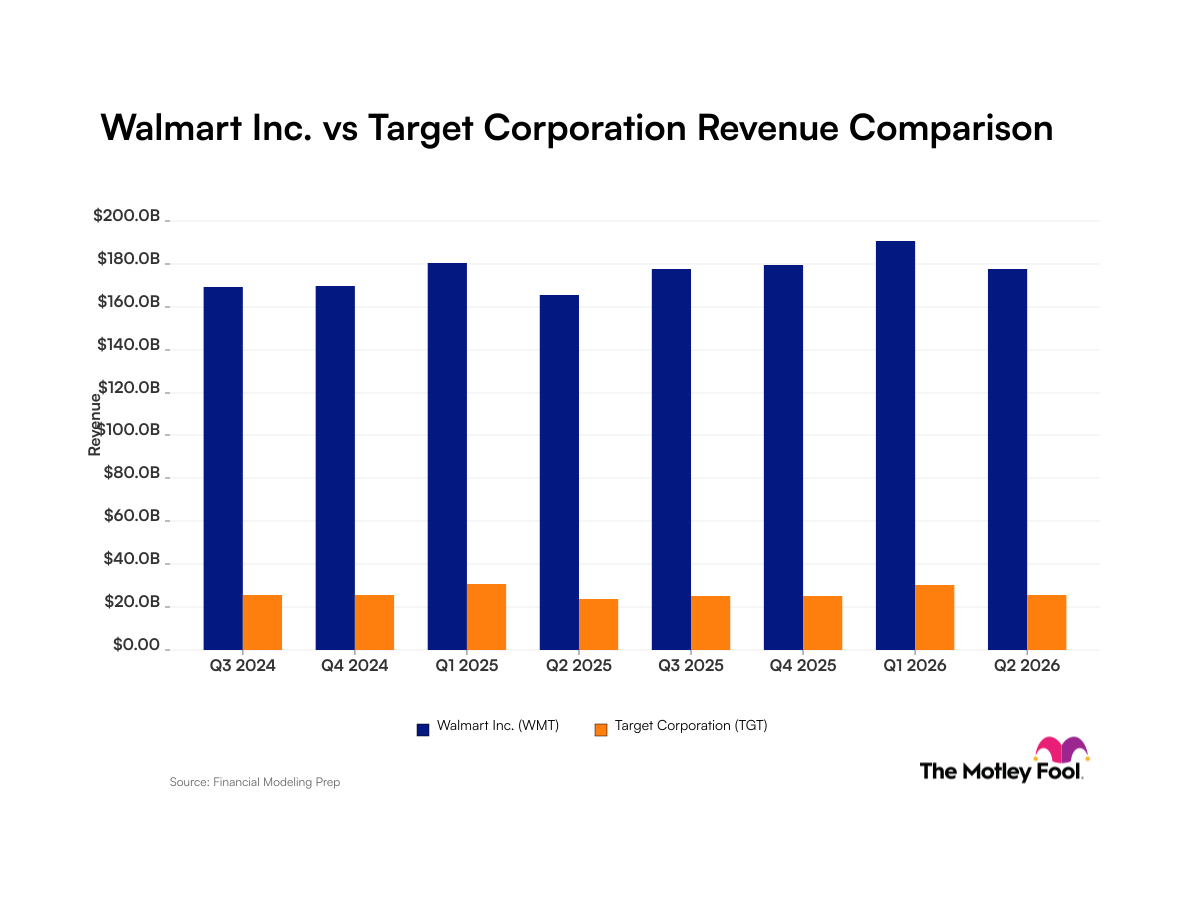

Walmart Inc revenue for the last quarter amounts to 177.75B USD, increased 7.33

Walmart Inc. EPS for the last quarter amounts to 0.67 USD, increased 19.64

Walmart Inc (WMT) has 2100000 emplpoyees as of July 09 2026.

Today WMT has the market capitalization of 900.06B USD.