Coupang Shares Plunge After Disappointing Q1 Results

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 53 minutes ago

0mins

Should l Buy CPNG?

Source: Fool

- Disappointing Earnings: Coupang reported an 8% revenue increase in Q1, but a sharp net loss due to costs from last year's data breach led to a 13.70% drop in share price to $17.91, reducing market cap to $38 billion, highlighting challenges in regaining investor trust.

- Surge in Trading Volume: Trading volume reached 79.9 million shares, approximately 238% above the three-month average of 23.6 million shares, indicating strong market reaction to Coupang's earnings report and heightened investor sentiment volatility.

- Membership Recovery: Management noted that 80% of WOW memberships lost due to the breach had returned by April, suggesting some progress in restoring customer trust, although overall financial performance remains under pressure.

- Growth Potential: Coupang's Developing Offerings segment saw a 25% sales increase, with significant growth from its expansion in Taiwan, while its food delivery service and nascent Japanese operations continue to scale, indicating potential in diversifying its business.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CPNG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CPNG

Wall Street analysts forecast CPNG stock price to rise

6 Analyst Rating

4 Buy

2 Hold

0 Sell

Moderate Buy

Current: 20.760

Low

22.00

Averages

33.83

High

40.00

Current: 20.760

Low

22.00

Averages

33.83

High

40.00

About CPNG

Coupang, Inc. is a technology company that provides retail, restaurant delivery, video streaming, and fintech services to customers around the world under brands, such as Coupang, Coupang Eats, Coupang Play, Farfetch, and Rocket Now. Through its AI cloud computing service as Coupang Intelligent Cloud (CIC), it enhances its services and operations and provides GPU-as-a-Service (GPUaaS), including to external parties. Its Product Commerce segment includes its core Korean retail (owned inventory) and marketplace offerings (third-party merchants) and Rocket Fresh, its fresh grocery offering, as well as advertising products associated with these offerings. Its Developing Offerings include Coupang Eats, its restaurant ordering and delivery service in Korea, Coupang Play, an online content streaming service in Korea, fintech, its retail operations in Taiwan, as well as advertising products associated with these offerings, and also include Farfetch, its global luxury fashion marketplace.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Coupang, Inc. Reports Q1 2026 Earnings Amid Recovery Efforts

- Revenue Recovery Trend: Coupang reported Product Commerce net revenues of $7.2 billion and total net revenues of $8.5 billion in Q1 2026, indicating a gradual improvement in revenue growth month-over-month despite the impacts from last quarter's data incident, showcasing resilient customer behavior.

- Membership Recovery Status: CEO Bom Suk Kim highlighted that WOW membership churn has returned to historical stable levels, with nearly 80% of the decline closed by the end of April, indicating that customer loyalty is crucial for future revenue growth.

- Margin Pressure Factors: CFO Gaurav Anand noted that margin pressures stem from customer vouchers and temporary network inefficiencies, with an expected year-over-year contraction of 300 to 400 basis points in adjusted EBITDA margin for Q2, although margins are anticipated to improve throughout the year.

- Share Repurchase Program: Coupang repurchased 20.4 million shares for $391 million this quarter and received approval for an additional $1 billion in repurchase authorization, reflecting the company's confidence in future growth and commitment to shareholders.

See More

Coupang Shares Plunge After Disappointing Q1 Results

- Disappointing Earnings: Coupang reported an 8% revenue increase in Q1, but a sharp net loss due to costs from last year's data breach led to a 13.70% drop in share price to $17.91, reducing market cap to $38 billion, highlighting challenges in regaining investor trust.

- Surge in Trading Volume: Trading volume reached 79.9 million shares, approximately 238% above the three-month average of 23.6 million shares, indicating strong market reaction to Coupang's earnings report and heightened investor sentiment volatility.

- Membership Recovery: Management noted that 80% of WOW memberships lost due to the breach had returned by April, suggesting some progress in restoring customer trust, although overall financial performance remains under pressure.

- Growth Potential: Coupang's Developing Offerings segment saw a 25% sales increase, with significant growth from its expansion in Taiwan, while its food delivery service and nascent Japanese operations continue to scale, indicating potential in diversifying its business.

See More

US Stocks Surge to New Highs Led by Tech Earnings

- Tech Stock Rally: The Nasdaq 100 index surged over 1.44% to reach an all-time high, driven by strong earnings from chipmakers and AI infrastructure stocks, reflecting market optimism about sustained investment growth in artificial intelligence.

- Crude Oil Plunge: WTI crude oil prices fell more than 6% to a two-week low as the US nears a peace agreement with Iran, which is expected to lift restrictions on the Strait of Hormuz, thereby reducing energy costs and enhancing profitability prospects for airlines and cruise lines.

- Employment Data Impact: The April ADP employment change report indicated that US companies added 109,000 jobs, below the expected 120,000, yet the market remains optimistic about the Fed's monetary policy, suggesting a lower likelihood of interest rate hikes.

- Earnings Optimism: So far, 84% of the 375 S&P 500 companies that reported earnings have exceeded expectations, with Q1 earnings projected to rise 12% year-over-year, indicating strong corporate profitability that further supports the stock market's upward trend.

See More

US Stocks Reach All-Time Highs as AI Investments Surge

- Market Performance: The S&P 500 index rose by 0.76% and the Nasdaq 100 index increased by 1.19%, reaching all-time highs, reflecting strong market optimism regarding ongoing investments in artificial intelligence, which are expected to continue driving stock prices higher.

- Chipmakers' Strong Earnings: Advanced Micro Devices (AMD) saw its stock price surge over 16% after raising its full-year sales forecast significantly due to robust data center spending, indicating a strong growth trajectory and reinforcing its competitive position in the semiconductor market.

- Crude Oil Price Plunge: WTI crude oil prices fell more than 5% to a two-week low as the US nears a peace agreement with Iran, which may help lower inflation expectations and improve profitability prospects for airlines and cruise operators amid declining fuel costs.

- Employment Data Impact: The April ADP employment change report indicated that US companies added 109,000 jobs, below the expected 120,000, yet the market remains optimistic about the Fed's monetary policy, which is likely to continue supporting stock market gains.

See More

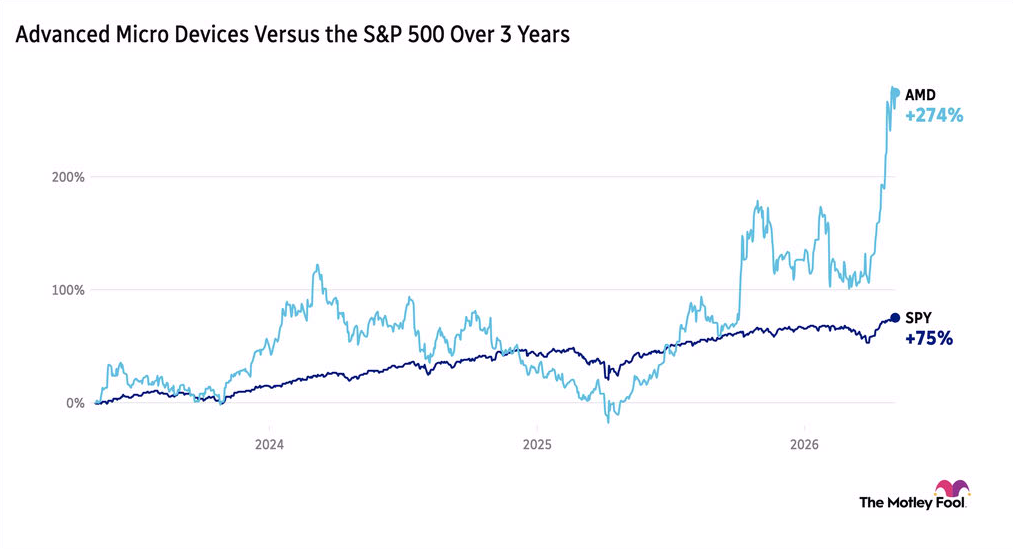

AMD Shares Surge 17% on Surge in Chip Demand

- Earnings Beat: AMD reported a 38% year-over-year revenue increase and a 43% rise in non-GAAP EPS for Q1 2026, exceeding market expectations and driving a 17% pre-market stock surge, highlighting the company's robust performance amid soaring AI infrastructure demand.

- Strategic Partnership: The collaboration with Meta is set to deploy 6 gigawatts of Instinct GPUs, which not only enhances AMD's competitive edge in the AI market but also lays a solid foundation for future revenue growth.

- Future Guidance: Management forecasts Q2 revenue to reach $11.2 billion, a 9% increase from Q1, translating to a 46% year-over-year growth, reflecting sustained growth potential and market confidence in AMD's AI initiatives.

- Market Reaction: Despite AMD's strong performance, Arista Networks saw a 9% drop in stock price due to cost pressures, indicating that supply chain challenges and rising costs in the semiconductor industry may affect overall market sentiment.

See More

SpaceX Plans Historic IPO Targeting $1.75 Trillion Valuation

- IPO Filing: Last month, SpaceX confidentially filed for an initial public offering (IPO) with the SEC, planning to kick off its roadshow on June 8 to pitch the stock to institutional investors and analysts, although a specific IPO date has not been set, trading is expected to commence in late June or early July.

- Valuation Target: The company is aiming for a staggering $1.75 trillion valuation, which would make it the largest IPO in U.S. history; however, historical trends indicate that IPO stocks often underperform in their first year, prompting investors to exercise caution.

- Historical Performance Insights: Data shows that since 1980, around 9,300 companies have gone public on the NYSE or Nasdaq, with IPO stocks gaining an average of 19% on their first trading day, yet those with large market values frequently experience sharp declines after initial excitement fades.

- Long-Term Investment Risks: While SpaceX may perform well in the long run, most large IPO stocks historically have underperformed the S&P 500 post-listing, suggesting that investors might be better off investing in an S&P 500 index fund rather than directly purchasing SpaceX shares.

See More

Coupang, Inc. Reports Q1 2026 Earnings Amid Recovery Efforts

- Revenue Recovery Trend: Coupang reported Product Commerce net revenues of $7.2 billion and total net revenues of $8.5 billion in Q1 2026, indicating a gradual improvement in revenue growth month-over-month despite the impacts from last quarter's data incident, showcasing resilient customer behavior.

- Membership Recovery Status: CEO Bom Suk Kim highlighted that WOW membership churn has returned to historical stable levels, with nearly 80% of the decline closed by the end of April, indicating that customer loyalty is crucial for future revenue growth.

- Margin Pressure Factors: CFO Gaurav Anand noted that margin pressures stem from customer vouchers and temporary network inefficiencies, with an expected year-over-year contraction of 300 to 400 basis points in adjusted EBITDA margin for Q2, although margins are anticipated to improve throughout the year.

- Share Repurchase Program: Coupang repurchased 20.4 million shares for $391 million this quarter and received approval for an additional $1 billion in repurchase authorization, reflecting the company's confidence in future growth and commitment to shareholders.

See More

Coupang Shares Plunge After Disappointing Q1 Results

- Disappointing Earnings: Coupang reported an 8% revenue increase in Q1, but a sharp net loss due to costs from last year's data breach led to a 13.70% drop in share price to $17.91, reducing market cap to $38 billion, highlighting challenges in regaining investor trust.

- Surge in Trading Volume: Trading volume reached 79.9 million shares, approximately 238% above the three-month average of 23.6 million shares, indicating strong market reaction to Coupang's earnings report and heightened investor sentiment volatility.

- Membership Recovery: Management noted that 80% of WOW memberships lost due to the breach had returned by April, suggesting some progress in restoring customer trust, although overall financial performance remains under pressure.

- Growth Potential: Coupang's Developing Offerings segment saw a 25% sales increase, with significant growth from its expansion in Taiwan, while its food delivery service and nascent Japanese operations continue to scale, indicating potential in diversifying its business.

See More

US Stocks Surge to New Highs Led by Tech Earnings

- Tech Stock Rally: The Nasdaq 100 index surged over 1.44% to reach an all-time high, driven by strong earnings from chipmakers and AI infrastructure stocks, reflecting market optimism about sustained investment growth in artificial intelligence.

- Crude Oil Plunge: WTI crude oil prices fell more than 6% to a two-week low as the US nears a peace agreement with Iran, which is expected to lift restrictions on the Strait of Hormuz, thereby reducing energy costs and enhancing profitability prospects for airlines and cruise lines.

- Employment Data Impact: The April ADP employment change report indicated that US companies added 109,000 jobs, below the expected 120,000, yet the market remains optimistic about the Fed's monetary policy, suggesting a lower likelihood of interest rate hikes.

- Earnings Optimism: So far, 84% of the 375 S&P 500 companies that reported earnings have exceeded expectations, with Q1 earnings projected to rise 12% year-over-year, indicating strong corporate profitability that further supports the stock market's upward trend.

See More

US Stocks Reach All-Time Highs as AI Investments Surge

- Market Performance: The S&P 500 index rose by 0.76% and the Nasdaq 100 index increased by 1.19%, reaching all-time highs, reflecting strong market optimism regarding ongoing investments in artificial intelligence, which are expected to continue driving stock prices higher.

- Chipmakers' Strong Earnings: Advanced Micro Devices (AMD) saw its stock price surge over 16% after raising its full-year sales forecast significantly due to robust data center spending, indicating a strong growth trajectory and reinforcing its competitive position in the semiconductor market.

- Crude Oil Price Plunge: WTI crude oil prices fell more than 5% to a two-week low as the US nears a peace agreement with Iran, which may help lower inflation expectations and improve profitability prospects for airlines and cruise operators amid declining fuel costs.

- Employment Data Impact: The April ADP employment change report indicated that US companies added 109,000 jobs, below the expected 120,000, yet the market remains optimistic about the Fed's monetary policy, which is likely to continue supporting stock market gains.

See More

AMD Shares Surge 17% on Surge in Chip Demand

- Earnings Beat: AMD reported a 38% year-over-year revenue increase and a 43% rise in non-GAAP EPS for Q1 2026, exceeding market expectations and driving a 17% pre-market stock surge, highlighting the company's robust performance amid soaring AI infrastructure demand.

- Strategic Partnership: The collaboration with Meta is set to deploy 6 gigawatts of Instinct GPUs, which not only enhances AMD's competitive edge in the AI market but also lays a solid foundation for future revenue growth.

- Future Guidance: Management forecasts Q2 revenue to reach $11.2 billion, a 9% increase from Q1, translating to a 46% year-over-year growth, reflecting sustained growth potential and market confidence in AMD's AI initiatives.

- Market Reaction: Despite AMD's strong performance, Arista Networks saw a 9% drop in stock price due to cost pressures, indicating that supply chain challenges and rising costs in the semiconductor industry may affect overall market sentiment.

See More

SpaceX Plans Historic IPO Targeting $1.75 Trillion Valuation

- IPO Filing: Last month, SpaceX confidentially filed for an initial public offering (IPO) with the SEC, planning to kick off its roadshow on June 8 to pitch the stock to institutional investors and analysts, although a specific IPO date has not been set, trading is expected to commence in late June or early July.

- Valuation Target: The company is aiming for a staggering $1.75 trillion valuation, which would make it the largest IPO in U.S. history; however, historical trends indicate that IPO stocks often underperform in their first year, prompting investors to exercise caution.

- Historical Performance Insights: Data shows that since 1980, around 9,300 companies have gone public on the NYSE or Nasdaq, with IPO stocks gaining an average of 19% on their first trading day, yet those with large market values frequently experience sharp declines after initial excitement fades.

- Long-Term Investment Risks: While SpaceX may perform well in the long run, most large IPO stocks historically have underperformed the S&P 500 post-listing, suggesting that investors might be better off investing in an S&P 500 index fund rather than directly purchasing SpaceX shares.

See More