Wall Street Retreats as Tech Stocks Weaken, Nasdaq Drops Over 1.5%

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 14 2026

0mins

Should l Buy AVGO?

Source: Benzinga

- Tech Stock Pullback: The Nasdaq 100 index fell over 1.5% during midday trading in New York, marking its worst performance in nearly a month, primarily dragged down by declines in tech giants like Broadcom, Oracle, and Nvidia, which dropped approximately 5%, 4.5%, and 2.5%, respectively.

- Bank Stocks Under Pressure: Shares of Citigroup and Wells Fargo fell by 4% each following disappointing earnings reports, exacerbating market concerns regarding financial stocks and negatively impacting overall market sentiment.

- Energy Sector Strength: Energy stocks rose over 2.4%, reaching their highest level since November 2024, with West Texas Intermediate crude climbing more than 1% to $62 a barrel, reflecting ongoing geopolitical risks that continue to shape the global energy market.

- Precious Metals and Crypto Rally: Gold prices increased by 0.5% to $4,610 per ounce, while silver surged above $90, gaining 4%, and Bitcoin rose for the fourth consecutive day to $97,000, indicating a growing demand for safe-haven assets amid market volatility.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AVGO?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AVGO

Wall Street analysts forecast AVGO stock price to rise

30 Analyst Rating

29 Buy

1 Hold

0 Sell

Strong Buy

Current: 399.630

Low

370.00

Averages

457.75

High

525.00

Current: 399.630

Low

370.00

Averages

457.75

High

525.00

About AVGO

Broadcom Inc. is a global technology firm that designs, develops, and supplies a range of semiconductors, enterprise software and security solutions. The Company operates through two segments: semiconductor solutions and infrastructure software. Its semiconductor solutions segment includes all of its product lines and intellectual property (IP) licensing. It provides a variety of radio frequency semiconductor devices, wireless connectivity solutions, custom touch controllers, and inductive charging solutions for mobile applications. Its infrastructure software segment includes its private and hybrid cloud, application development and delivery, software-defined edge, application networking and security, mainframe, distributed and cybersecurity solutions, and its FC SAN business. It provides a portfolio of software solutions that enable customers to plan, develop, automate, manage and secure applications across mainframe, distributed, mobile and cloud platforms.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Netflix's Long-Term Growth Potential Remains Significant

- User Engagement Growth: Netflix's management highlighted that, despite holding only about 5% of global TV viewership, its audience is nearing 1 billion, showcasing its strong appeal in a rapidly changing entertainment landscape and significant future growth potential.

- Market Penetration Opportunities: As of the end of 2025, Netflix's penetration in broadband households is less than 45%, indicating ample room for expansion in the global market, which can enhance market share through improved user experience.

- Long-Term Investment Value: The management emphasized Netflix's commitment to being a 'must-have service' for users, which not only aids in increasing retention rates but also solidifies its leadership position in a competitive market, attracting more investor attention.

- Strategic Development Focus: Netflix aims to enhance user engagement and content quality for sustainable growth, planning to tackle industry challenges through innovation and technology investments to ensure its competitive edge in the future.

See More

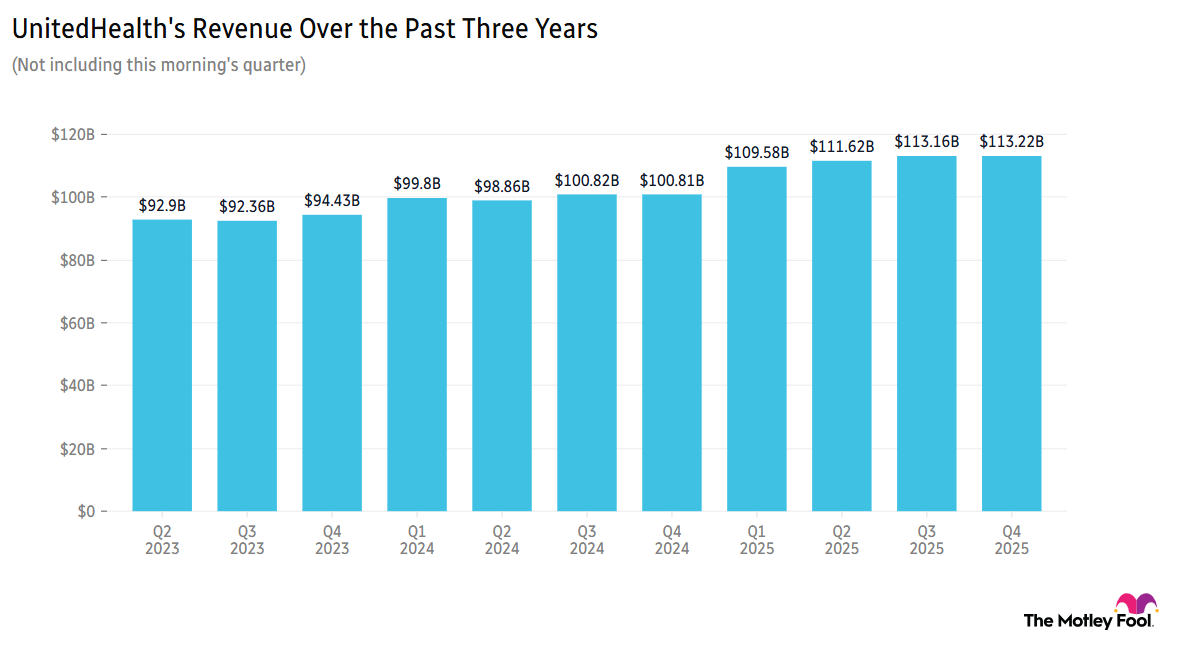

UnitedHealth Group Raises Profit Outlook Following Strong Earnings Report

- Profit Outlook Raised: UnitedHealth Group (UNH) saw its stock jump over 5% ahead of the market open, driven by profits exceeding analyst expectations and revenue rising from $109.58 billion in the prior year to $111.72 billion, with a full-year 2026 profit outlook now exceeding $18.25 per share, up from $17.75.

- Rising Operating Costs: The operating cost ratio increased from 12.4% in 2025 to 13.8%, yet investors remained unfazed as this was seen as necessary incremental investments in personnel, processes, and technology, including AI, indicating a strategic focus on future growth.

- Semiconductor Sector Surge: The Philadelphia Semiconductor Sector Index (SOX) has rallied 30% over the past 13 days, marking its largest increase since 2002, fueled by positive earnings momentum and optimism surrounding AI, suggesting a robust recovery in the sector.

- Earnings Reports on the Horizon: Tractor Supply (TSCO) and Quest Diagnostics (DGX) are set to report earnings soon, with investors eager to see if they can outperform last quarter's results, particularly amid pressures from high-ticket sales and technology investments, while EQT (EQT) will report after market close, focusing on the impact of natural gas price volatility on its performance.

See More

Nvidia Faces Emerging AI Chip Competition

- Market Leadership: Nvidia continues to lead in the AI chip sector, reporting a 65% revenue increase to over $215 billion last year, with a forecasted 72% growth this year, reflecting strong demand and innovation in the AI market.

- Emerging Competitors: Cerebras has recently filed for an IPO, with chips 58 times larger than Nvidia's, offering higher memory bandwidth and faster inference speeds, potentially posing a threat to Nvidia's dominance.

- Major Partnership Deals: Cerebras has secured a deal worth over $20 billion with OpenAI and a global distribution agreement with Amazon Web Services, enhancing its competitive position and challenging Nvidia's market share.

- Ongoing Innovation Investment: Nvidia invests over $18 billion annually in R&D, focusing on technology updates and system integration, ensuring customers can seamlessly upgrade, thereby solidifying its market leadership.

See More

Nvidia's Dominance in the AI Chip Market

- Market Leadership: Nvidia's dominance in the AI chip market is attributed to its ongoing focus on innovation, with a 65% revenue increase last year to over $215 billion, and a projected 72% growth this year, indicating strong market demand and technological superiority.

- Rising Competition: Emerging player Cerebras has announced plans to go public, boasting chips 58 times larger than Nvidia's, with higher memory bandwidth, and has secured a partnership with OpenAI worth over $20 billion, posing a potential threat to Nvidia.

- Funding Dynamics: European AI chip companies Euclyd and Optalysys are actively seeking funding, with Euclyd discussing approximately $118 million and Optalysys aiming for at least $100 million, highlighting intensifying competition as more players enter the field.

- Innovation and Acquisitions: Nvidia invests over $18 billion annually in R&D and enhances its inference capabilities through acquisitions like Groq, ensuring its continued advantage in technological innovation and market leadership.

See More

Latest Stock Updates from Analyst Blog

- Broadcom's Strong Growth: Broadcom's shares have risen 19.1% over the past six months, lagging behind the semiconductor industry's 27.3% growth, driven by robust demand for AI semiconductors and successful VMware integration, with Q2 fiscal 2026 AI revenues expected to surge 140% year-over-year to $10.7 billion.

- JPMorgan's Steady Performance: JPMorgan's stock has gained 5.5% in the last six months, below the investment banking industry's 8.6% increase, although its Q1 results showed solid revenue momentum, with 2026 tech spending projected at $19.8 billion despite pressure from declining interest rates.

- Cisco's Market Advantage: Cisco's shares have increased by 23.3% over the past six months, outperforming the computer networking industry's 22.6% growth, benefiting from strong product orders from hyperscalers, with AI infrastructure revenue expected to exceed $3 billion in fiscal 2026, despite intensifying competition.

- CompX International's Stable Performance: CompX International's stock has risen 2.6% over the past six months, outperforming the office supplies industry's -7.8% average, supported by stable demand in government and industrial sectors, although facing inflationary pressures and rising inventory levels.

See More

Chip Stocks Surge with Broadcom Leading the Charge

- Semiconductor Rebound: The iShares Semiconductor ETF (SOXX) is on track for its best month since 2001, driven by significant gains from Marvell and Intel, both surging approximately 49% this month, reflecting strong market confidence in the semiconductor sector.

- Broadcom's Edge: Broadcom's expanded partnership with Google to produce AI chips through 2031 has led analysts to adopt a more bullish outlook, as significant collaborations with major hyperscalers are expected to drive future growth in AI and data centers.

- Intel's Recovery: Intel's stock has rallied amid a shift in AI narratives and deal momentum, with expectations for its upcoming earnings report to show $122.43 billion in revenue, down 2% year-over-year, yet optimism surrounding its turnaround efforts is growing in the market.

- AMD's Growth Potential: AMD is projected to report $9.87 billion in revenue on May 5, a 38% increase year-over-year, with analysts maintaining a positive outlook on its growth potential, particularly in AI-driven data center spending.

See More

Netflix's Long-Term Growth Potential Remains Significant

- User Engagement Growth: Netflix's management highlighted that, despite holding only about 5% of global TV viewership, its audience is nearing 1 billion, showcasing its strong appeal in a rapidly changing entertainment landscape and significant future growth potential.

- Market Penetration Opportunities: As of the end of 2025, Netflix's penetration in broadband households is less than 45%, indicating ample room for expansion in the global market, which can enhance market share through improved user experience.

- Long-Term Investment Value: The management emphasized Netflix's commitment to being a 'must-have service' for users, which not only aids in increasing retention rates but also solidifies its leadership position in a competitive market, attracting more investor attention.

- Strategic Development Focus: Netflix aims to enhance user engagement and content quality for sustainable growth, planning to tackle industry challenges through innovation and technology investments to ensure its competitive edge in the future.

See More

UnitedHealth Group Raises Profit Outlook Following Strong Earnings Report

- Profit Outlook Raised: UnitedHealth Group (UNH) saw its stock jump over 5% ahead of the market open, driven by profits exceeding analyst expectations and revenue rising from $109.58 billion in the prior year to $111.72 billion, with a full-year 2026 profit outlook now exceeding $18.25 per share, up from $17.75.

- Rising Operating Costs: The operating cost ratio increased from 12.4% in 2025 to 13.8%, yet investors remained unfazed as this was seen as necessary incremental investments in personnel, processes, and technology, including AI, indicating a strategic focus on future growth.

- Semiconductor Sector Surge: The Philadelphia Semiconductor Sector Index (SOX) has rallied 30% over the past 13 days, marking its largest increase since 2002, fueled by positive earnings momentum and optimism surrounding AI, suggesting a robust recovery in the sector.

- Earnings Reports on the Horizon: Tractor Supply (TSCO) and Quest Diagnostics (DGX) are set to report earnings soon, with investors eager to see if they can outperform last quarter's results, particularly amid pressures from high-ticket sales and technology investments, while EQT (EQT) will report after market close, focusing on the impact of natural gas price volatility on its performance.

See More

Nvidia Faces Emerging AI Chip Competition

- Market Leadership: Nvidia continues to lead in the AI chip sector, reporting a 65% revenue increase to over $215 billion last year, with a forecasted 72% growth this year, reflecting strong demand and innovation in the AI market.

- Emerging Competitors: Cerebras has recently filed for an IPO, with chips 58 times larger than Nvidia's, offering higher memory bandwidth and faster inference speeds, potentially posing a threat to Nvidia's dominance.

- Major Partnership Deals: Cerebras has secured a deal worth over $20 billion with OpenAI and a global distribution agreement with Amazon Web Services, enhancing its competitive position and challenging Nvidia's market share.

- Ongoing Innovation Investment: Nvidia invests over $18 billion annually in R&D, focusing on technology updates and system integration, ensuring customers can seamlessly upgrade, thereby solidifying its market leadership.

See More

Nvidia's Dominance in the AI Chip Market

- Market Leadership: Nvidia's dominance in the AI chip market is attributed to its ongoing focus on innovation, with a 65% revenue increase last year to over $215 billion, and a projected 72% growth this year, indicating strong market demand and technological superiority.

- Rising Competition: Emerging player Cerebras has announced plans to go public, boasting chips 58 times larger than Nvidia's, with higher memory bandwidth, and has secured a partnership with OpenAI worth over $20 billion, posing a potential threat to Nvidia.

- Funding Dynamics: European AI chip companies Euclyd and Optalysys are actively seeking funding, with Euclyd discussing approximately $118 million and Optalysys aiming for at least $100 million, highlighting intensifying competition as more players enter the field.

- Innovation and Acquisitions: Nvidia invests over $18 billion annually in R&D and enhances its inference capabilities through acquisitions like Groq, ensuring its continued advantage in technological innovation and market leadership.

See More

Latest Stock Updates from Analyst Blog

- Broadcom's Strong Growth: Broadcom's shares have risen 19.1% over the past six months, lagging behind the semiconductor industry's 27.3% growth, driven by robust demand for AI semiconductors and successful VMware integration, with Q2 fiscal 2026 AI revenues expected to surge 140% year-over-year to $10.7 billion.

- JPMorgan's Steady Performance: JPMorgan's stock has gained 5.5% in the last six months, below the investment banking industry's 8.6% increase, although its Q1 results showed solid revenue momentum, with 2026 tech spending projected at $19.8 billion despite pressure from declining interest rates.

- Cisco's Market Advantage: Cisco's shares have increased by 23.3% over the past six months, outperforming the computer networking industry's 22.6% growth, benefiting from strong product orders from hyperscalers, with AI infrastructure revenue expected to exceed $3 billion in fiscal 2026, despite intensifying competition.

- CompX International's Stable Performance: CompX International's stock has risen 2.6% over the past six months, outperforming the office supplies industry's -7.8% average, supported by stable demand in government and industrial sectors, although facing inflationary pressures and rising inventory levels.

See More

Chip Stocks Surge with Broadcom Leading the Charge

- Semiconductor Rebound: The iShares Semiconductor ETF (SOXX) is on track for its best month since 2001, driven by significant gains from Marvell and Intel, both surging approximately 49% this month, reflecting strong market confidence in the semiconductor sector.

- Broadcom's Edge: Broadcom's expanded partnership with Google to produce AI chips through 2031 has led analysts to adopt a more bullish outlook, as significant collaborations with major hyperscalers are expected to drive future growth in AI and data centers.

- Intel's Recovery: Intel's stock has rallied amid a shift in AI narratives and deal momentum, with expectations for its upcoming earnings report to show $122.43 billion in revenue, down 2% year-over-year, yet optimism surrounding its turnaround efforts is growing in the market.

- AMD's Growth Potential: AMD is projected to report $9.87 billion in revenue on May 5, a 38% increase year-over-year, with analysts maintaining a positive outlook on its growth potential, particularly in AI-driven data center spending.

See More