Wells Fargo Maintains Equal Weight on Truist Financial with $55 Price Target

Commenting on Truist Financial's quarterly results, Wells Fargo notes the company's 2026 guide seems below consensus and closer to its numbers on net interest income despite better loan growth. The 2026 guide seems not as good as peer given a midpoint of core operating leverage of 165bp and net interest income up 3%-4%. This does, however, imply better fee growth given a revenue guide of 4%-5%, the firm adds. Wells believes the headline number seems to understate Q4 225 results, which would seem closer to in line excluding legal and severance mitigated by a low tax rate and low regulatory costs. Expenses were above, and remain Wells' main question in a period of such high investments by competitor banks. The firm has an Equal Weight rating on the stock with a price target of $55.

Trade with 70% Backtested Accuracy

Analyst Views on TFC

About TFC

About the author

Truist Financial Q1 2026 Earnings Highlights

- Net Income Performance: Truist Financial reported a net income of $1.4 billion for Q1 2026, translating to $1.09 per diluted share, despite a 1.9% decline in revenue linked to lower net interest income, showcasing the company's success in diversifying its revenue streams through strong growth in investment banking and wealth management.

- Long-Term Profitability Goals: Management has established a long-term ROTCE target of 16% to 18% and reaffirmed a 15% ROTCE target for 2027, indicating a strong commitment to enhancing capital returns and reflecting confidence in future profitability.

- Shareholder Return Plan: Truist has increased its share repurchase target for 2026 from $4 billion to $5 billion, demonstrating a focus on capital management and optimism about future cash flows, which is expected to bolster investor confidence.

- Interest Income Outlook Adjustment: While net interest income is projected to grow by 2% to 3% in 2026, the management has revised its expectations downward due to the unchanged federal funds rate, highlighting increased market competition and changes in the interest rate environment.

Salesforce Rated as One of the Top Stocks for Next 5 Years

- Buy Rating Reaffirmed: On April 10, Truist Securities reaffirmed its Buy rating on Salesforce, Inc. (NYSE:CRM) with a price target of $280, reflecting confidence in the company's growth prospects, particularly in the second half of fiscal year 2027.

- Growth Potential Analysis: Truist highlighted that Salesforce is poised to benefit from the agentic AI innovation cycle, new customer opportunities, and changes in pricing and packaging related to AI agents, which will drive accelerated growth and strengthen its market position.

- Share Repurchase Program: Salesforce recently announced a $25 billion accelerated share repurchase program, indicating confidence in its own valuation, while also reflecting its strong competitive position in the agentic AI space, with the stock trading at about 9.5 times its estimated free cash flow for calendar year 2027, suggesting significant undervaluation.

- Slackbot Innovation Potential: Truist also pointed out the potential of agentic AI within Slackbot, which it believes is not fully recognized, and expects further updates and innovations related to Agentforce at the upcoming TDX developer conference, which could further propel the company's business development.

Truist (TFC) Q1 2026 Earnings Call Transcript

Truist Financial Q1 Earnings Analysis

- Adjusted Revenue Growth: Truist Financial reported Q1 adjusted revenue of $5.20 billion, surpassing the analyst estimate of $5.18 billion, although it decreased from $5.30 billion in the previous quarter, indicating increasing competitive pressures in the market.

- Expense Outlook Increase: The bank now expects noninterest expenses to rise by approximately 1.75% for the year, up from the previous guidance of 1.25%-2.25%, which could impact future profitability and cost control strategies.

- Enhanced Share Buyback Plan: Truist has raised its share repurchase guidance to about $5 billion from the prior $4 billion, reflecting the company's confidence in future cash flows and shareholder returns.

- Credit Loss Provision Changes: The provision for credit losses in Q1 was $479 million, lower than the consensus estimate of $456 million, indicating improvements in the company's credit risk management practices.

Truist Financial Q1 Earnings Exceed Expectations

- Earnings Beat: Truist Financial reported a Q1 GAAP EPS of $1.09, surpassing expectations by $0.09, which reflects the company's solid profitability despite market caution regarding its valuation and technical indicators.

- Revenue Growth: The company achieved Q1 revenue of $5.2 billion, marking a 5.1% year-over-year increase and exceeding market expectations by $20 million, indicating strong growth momentum in a competitive financial services landscape.

- Market Reaction: Despite the strong performance, analysts express concerns over Truist's valuation and technical aspects, which may impact investor confidence and stock performance, necessitating close monitoring of future market developments.

- Future Outlook: Truist Financial is set to present its strategic plans at the upcoming 2026 Financial Services Conference, which is expected to further drive growth and enhance market share in the financial services sector.

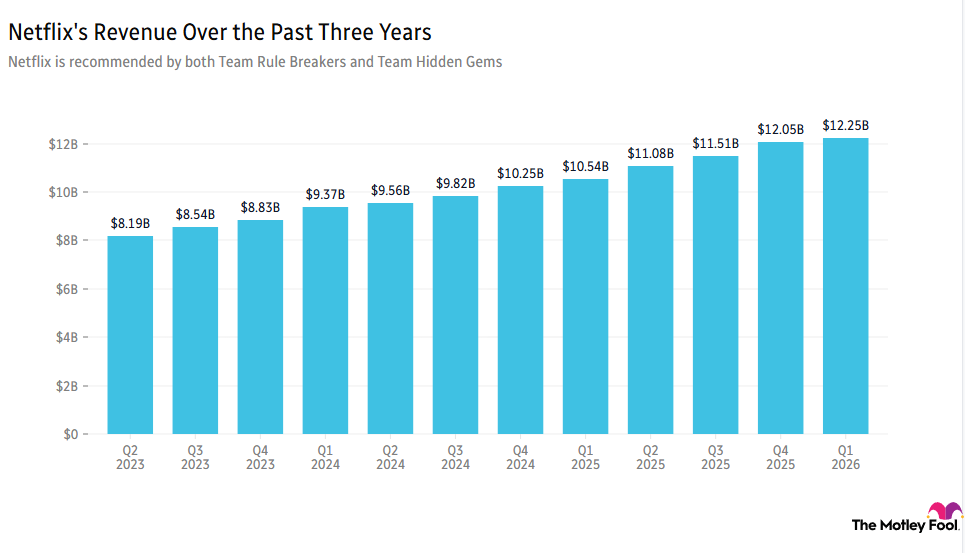

Hastings' Departure Triggers 10% Drop in NFLX Stock

- Hastings' Departure Impact: Netflix (NFLX) saw a 10% drop in pre-market trading following the announcement of co-founder Reed Hastings' resignation, reflecting investor concerns about the company's growth prospects, particularly with underwhelming Q2 revenue and earnings guidance.

- Weak Ad Revenue Growth: Although Netflix maintained its full-year revenue target with a projected growth rate of 12%-14%, market confidence in its advertising revenue and user monetization strategies has weakened, leading to a more cautious outlook on future performance from investors.

- Unrelated to Warner Bros Deal: CEO Ted Sarandos clarified that Hastings' departure was unrelated to the failed acquisition of Warner Bros Discovery, emphasizing that Hastings was a strong advocate for that deal, which indicates stability in the company's strategic direction despite leadership changes.

- Apple's Sales Surge in China: In contrast, Apple (AAPL) achieved a 20% increase in iPhone shipments in China during Q1, despite a 4% decline in overall smartphone shipments, showcasing Apple's strong market appeal in a challenging competitive landscape.

Truist Financial Q1 2026 Earnings Highlights

- Net Income Performance: Truist Financial reported a net income of $1.4 billion for Q1 2026, translating to $1.09 per diluted share, despite a 1.9% decline in revenue linked to lower net interest income, showcasing the company's success in diversifying its revenue streams through strong growth in investment banking and wealth management.

- Long-Term Profitability Goals: Management has established a long-term ROTCE target of 16% to 18% and reaffirmed a 15% ROTCE target for 2027, indicating a strong commitment to enhancing capital returns and reflecting confidence in future profitability.

- Shareholder Return Plan: Truist has increased its share repurchase target for 2026 from $4 billion to $5 billion, demonstrating a focus on capital management and optimism about future cash flows, which is expected to bolster investor confidence.

- Interest Income Outlook Adjustment: While net interest income is projected to grow by 2% to 3% in 2026, the management has revised its expectations downward due to the unchanged federal funds rate, highlighting increased market competition and changes in the interest rate environment.

Salesforce Rated as One of the Top Stocks for Next 5 Years

- Buy Rating Reaffirmed: On April 10, Truist Securities reaffirmed its Buy rating on Salesforce, Inc. (NYSE:CRM) with a price target of $280, reflecting confidence in the company's growth prospects, particularly in the second half of fiscal year 2027.

- Growth Potential Analysis: Truist highlighted that Salesforce is poised to benefit from the agentic AI innovation cycle, new customer opportunities, and changes in pricing and packaging related to AI agents, which will drive accelerated growth and strengthen its market position.

- Share Repurchase Program: Salesforce recently announced a $25 billion accelerated share repurchase program, indicating confidence in its own valuation, while also reflecting its strong competitive position in the agentic AI space, with the stock trading at about 9.5 times its estimated free cash flow for calendar year 2027, suggesting significant undervaluation.

- Slackbot Innovation Potential: Truist also pointed out the potential of agentic AI within Slackbot, which it believes is not fully recognized, and expects further updates and innovations related to Agentforce at the upcoming TDX developer conference, which could further propel the company's business development.

Truist (TFC) Q1 2026 Earnings Call Transcript

Truist Financial Q1 Earnings Analysis

- Adjusted Revenue Growth: Truist Financial reported Q1 adjusted revenue of $5.20 billion, surpassing the analyst estimate of $5.18 billion, although it decreased from $5.30 billion in the previous quarter, indicating increasing competitive pressures in the market.

- Expense Outlook Increase: The bank now expects noninterest expenses to rise by approximately 1.75% for the year, up from the previous guidance of 1.25%-2.25%, which could impact future profitability and cost control strategies.

- Enhanced Share Buyback Plan: Truist has raised its share repurchase guidance to about $5 billion from the prior $4 billion, reflecting the company's confidence in future cash flows and shareholder returns.

- Credit Loss Provision Changes: The provision for credit losses in Q1 was $479 million, lower than the consensus estimate of $456 million, indicating improvements in the company's credit risk management practices.

Truist Financial Q1 Earnings Exceed Expectations

- Earnings Beat: Truist Financial reported a Q1 GAAP EPS of $1.09, surpassing expectations by $0.09, which reflects the company's solid profitability despite market caution regarding its valuation and technical indicators.

- Revenue Growth: The company achieved Q1 revenue of $5.2 billion, marking a 5.1% year-over-year increase and exceeding market expectations by $20 million, indicating strong growth momentum in a competitive financial services landscape.

- Market Reaction: Despite the strong performance, analysts express concerns over Truist's valuation and technical aspects, which may impact investor confidence and stock performance, necessitating close monitoring of future market developments.

- Future Outlook: Truist Financial is set to present its strategic plans at the upcoming 2026 Financial Services Conference, which is expected to further drive growth and enhance market share in the financial services sector.

Hastings' Departure Triggers 10% Drop in NFLX Stock

- Hastings' Departure Impact: Netflix (NFLX) saw a 10% drop in pre-market trading following the announcement of co-founder Reed Hastings' resignation, reflecting investor concerns about the company's growth prospects, particularly with underwhelming Q2 revenue and earnings guidance.

- Weak Ad Revenue Growth: Although Netflix maintained its full-year revenue target with a projected growth rate of 12%-14%, market confidence in its advertising revenue and user monetization strategies has weakened, leading to a more cautious outlook on future performance from investors.

- Unrelated to Warner Bros Deal: CEO Ted Sarandos clarified that Hastings' departure was unrelated to the failed acquisition of Warner Bros Discovery, emphasizing that Hastings was a strong advocate for that deal, which indicates stability in the company's strategic direction despite leadership changes.

- Apple's Sales Surge in China: In contrast, Apple (AAPL) achieved a 20% increase in iPhone shipments in China during Q1, despite a 4% decline in overall smartphone shipments, showcasing Apple's strong market appeal in a challenging competitive landscape.