Jacobs Secures Two Water Contracts in Virginia to Enhance Infrastructure Capacity

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 14 2026

0mins

Should l Buy J?

Source: PRnewswire

- Infrastructure Upgrade: Jacobs has secured two contracts with the City of Suffolk, Virginia, aimed at expanding and modernizing water and wastewater infrastructure to meet rising demand and environmental standards, ensuring long-term regional growth.

- Sanitary Overflow Control: One contract will continue to support the city's program to reduce sanitary sewer overflows, enhancing public health and water quality, thereby improving residents' quality of life.

- Water Treatment Capacity Expansion: The second contract involves planning, design, and construction management for expanding surface water treatment capacity, which is expected to improve water distribution systems and pump station evaluations in response to tightening groundwater withdrawal limits.

- Long-term Partnership: Jacobs has been serving Suffolk's water systems for over 20 years, and its expertise and responsiveness have been crucial in achieving full regulatory compliance, enhancing the reliability and efficiency of the city's infrastructure.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy J?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on J

Wall Street analysts forecast J stock price to rise

12 Analyst Rating

7 Buy

5 Hold

0 Sell

Moderate Buy

Current: 136.550

Low

137.00

Averages

157.40

High

180.00

Current: 136.550

Low

137.00

Averages

157.40

High

180.00

About J

Jacobs Solutions Inc. provides end-to-end services in advanced manufacturing, cities and places, energy, environmental, life sciences, transportation and water. The Company’s segments include Infrastructure and Advanced Facilities (I&AF) and PA Consulting. The I&AF segment provides end-to-end solutions for its client’s complex challenges related to climate change, energy transition, connected mobility, buildings and infrastructure, integrated water management and biopharmaceutical manufacturing. It uses data science and technology-enabled expertise to deliver outcomes for its clients and communities. Its clients include national, state and local governments in Europe, the Middle East, and others. The PA Consulting segment has a diverse mix of private and public sector clients. Private sector clients include global household names like Unilever, Microsoft, and Pret A Manger, and start-ups like PulPac, which converts plant fibers into sustainable packaging to reduce single-use plastic.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Significant Stock Movements for AMD and Others

- AMD Strong Guidance: AMD shares surged 20% after issuing a second-quarter revenue forecast of $11.2 billion, exceeding the analyst estimate of $10.52 billion, with first-quarter results also surpassing expectations, indicating robust performance in the semiconductor market.

- Super Micro Earnings Beat: Super Micro's stock jumped nearly 15% as fourth-quarter profit expectations range from 65 to 79 cents per share, significantly above Wall Street's call for 55 cents, with third-quarter adjusted earnings of 84 cents per share showcasing its competitiveness in the server market.

- CVS Health Performance Boost: CVS Health shares gained 4% after reporting first-quarter adjusted earnings of $2.57 per share and revenue of $100.43 billion, both exceeding analyst expectations, while the company raised its full-year earnings outlook, reflecting strong performance in the pharmacy benefits sector.

- Lucid Group Worsening Losses: Lucid Group shares fell 3% as the company reported a first-quarter loss of $3.46 per share, significantly worse than the expected loss of $2.64, with revenue of $282.5 million missing the $440.4 million target, highlighting challenges in the electric vehicle market.

See More

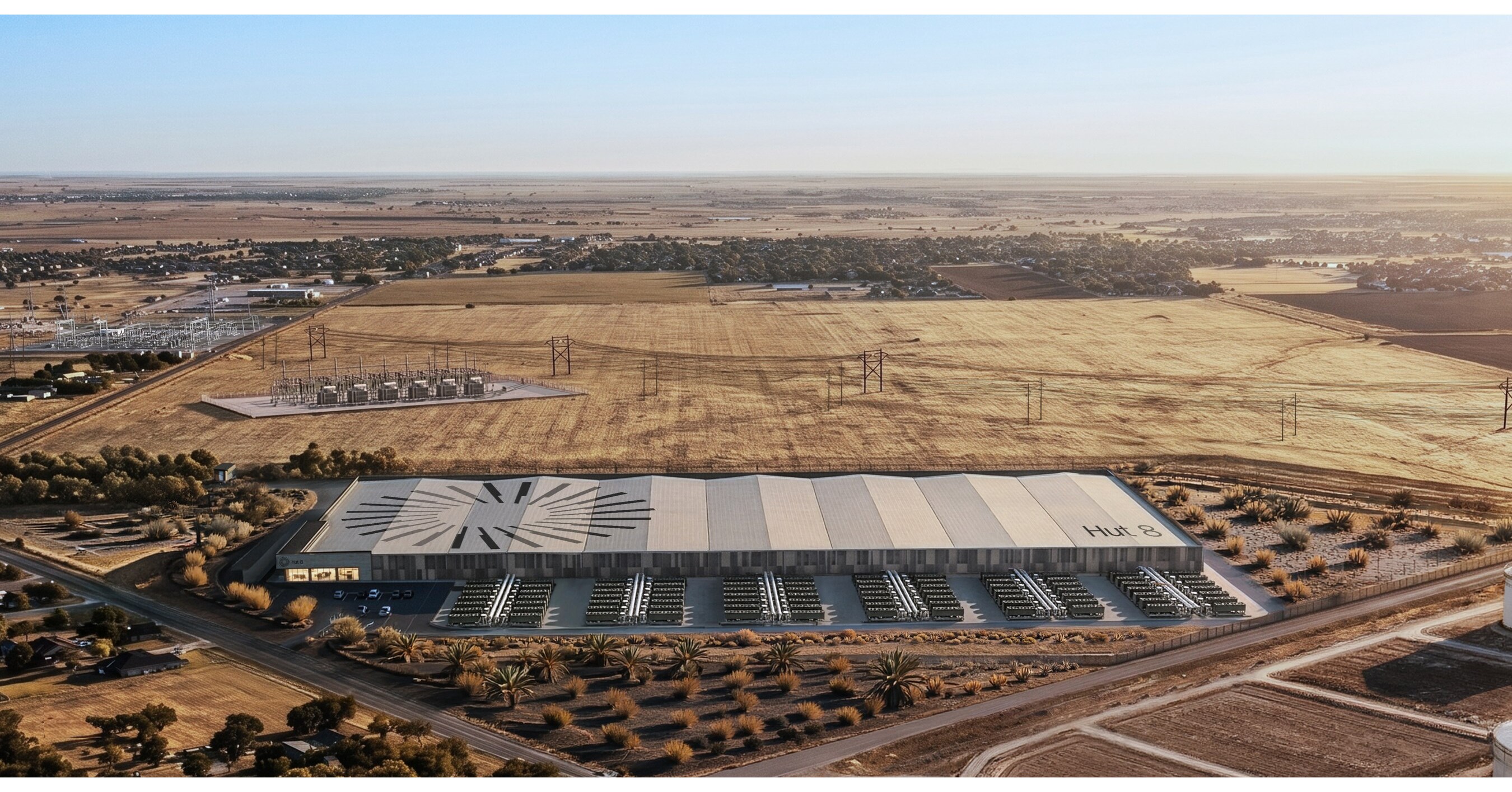

Hut 8 Signs $9.8 Billion Lease for AI Data Center

- Long-Term Lease Agreement: Hut 8 has signed a 15-year lease worth $9.8 billion with an undisclosed tenant, indicating rising demand for AI model infrastructure and expected future revenue growth for the company.

- Capacity Expansion: The agreement covers 352 megawatts of initial project capacity, increasing Hut 8's total contracted AI data center capacity to 597 megawatts and raising the total contract value to approximately $16.8 billion, showcasing the company's strong growth potential in the AI sector.

- Project Construction Timeline: The project, located in Nueces County, Texas, is expected to connect power in early 2027, with the first building scheduled for completion later that year, indicating Hut 8's strategic positioning to meet the growing computing and energy needs of AI firms.

- Strategic Partnerships: The project is being built in collaboration with partners including American Electric Power, Vertiv, and Jacobs, utilizing Nvidia's latest data center systems, reflecting intensified competition in AI infrastructure and Hut 8's proactive expansion in the market.

See More

Hut 8 Signs $25.1 Billion Lease with High-Investment-Grade Tenant

- Significant Lease Value: Hut 8's 15-year lease with a high-investment-grade tenant is valued at $9.8 billion, potentially reaching $25.1 billion if all renewal options are exercised, significantly enhancing the company's financial stability and market competitiveness.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate base-term contract value of approximately $16.8 billion, and an expected annual net operating income of about $1.1 billion, further solidifying its leadership in AI infrastructure.

- Flexible Development Model: Hut 8's power-first development model repositioned the site originally designed for American Bitcoin Corp. to AI infrastructure, showcasing the company's flexibility and innovative capacity in responding to evolving market demands.

- Strategic Partnerships: Hut 8 collaborates with top-tier partners like NVIDIA, Jacobs, and Vertiv to develop Beacon Point, ensuring efficient execution in technology, engineering, and critical systems delivery, thereby enhancing the company's market reputation and execution capabilities.

See More

Hut 8 Signs $9.8 Billion Lease with High-Investment-Grade Tenant

- Lease Scale: Hut 8 has signed a 15-year lease valued at $9.8 billion with a high-investment-grade tenant for 352 MW of IT capacity, which is expected to significantly enhance the company's revenue streams and market position.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate contract value of approximately $16.8 billion, indicating strong performance in the rapidly growing AI infrastructure market.

- Technical Collaboration: Hut 8 will deliver a 352 MW AI factory designed to NVIDIA's DSX reference architecture, showcasing the company's technical capabilities and market adaptability in high-performance computing, likely attracting more high-end clients.

- Sustainability Strategy: The initial delivery of the project is expected in Q3 2027, and Hut 8 ensures efficient execution and long-term sustainability through collaboration with Tier 1 partners, further solidifying its leadership position in the energy infrastructure sector.

See More

Jacobs Solutions Q2 2026 Earnings: Strong Performance

- Significant Earnings Growth: Jacobs Solutions reported a 22% increase in adjusted EPS to $1.75 for Q2 FY 2026, driven by 9% organic net revenue growth, surpassing the 8% growth rate in Q1, indicating strong market performance and enhanced profitability.

- Record Backlog: The company's backlog grew by 22% to $27 billion, setting a new record with a trailing 12-month book-to-bill ratio of 1.4x, reflecting strong confidence in future project delivery capabilities and market demand.

- Data Center Business Surge: Jacobs reported over 100% year-on-year growth in its data center business for Q2, with a strengthening strategic partnership with NVIDIA, highlighting the company's advantageous position in the rapidly growing AI infrastructure market.

- Optimistic Financial Outlook: The company raised its FY 2026 organic net revenue growth range to 8% to 10.5%, with adjusted EBITDA margin expectations of 14.6% to 14.9%, signaling management's confidence in future performance and providing positive signals to investors.

See More

Jacobs Solutions Raises Annual Profit Forecast Amid Data Center Demand

- Profit Forecast Increase: Jacobs Solutions has raised its annual profit forecast, banking on strong demand for data center infrastructure services, indicating a positive outlook for the company in the market.

- Surge in Data Center Construction: The rapid advancement of artificial intelligence technologies has led to a surge in data center construction demand, significantly increasing Jacobs Solutions' business volume in planning, engineering, and construction management services, further driving revenue growth.

- Demand-Driven Market: The spike in demand for data center infrastructure services reflects the industry's urgent need for high-performance computing capabilities, which is expected to lead to sustained revenue growth and market share expansion for Jacobs Solutions.

- Strategic Positioning Advantage: Jacobs Solutions' expertise and experience in the data center sector enable it to effectively seize market opportunities, thereby maintaining a competitive edge in a challenging environment and enhancing its long-term growth potential.

See More

Significant Stock Movements for AMD and Others

- AMD Strong Guidance: AMD shares surged 20% after issuing a second-quarter revenue forecast of $11.2 billion, exceeding the analyst estimate of $10.52 billion, with first-quarter results also surpassing expectations, indicating robust performance in the semiconductor market.

- Super Micro Earnings Beat: Super Micro's stock jumped nearly 15% as fourth-quarter profit expectations range from 65 to 79 cents per share, significantly above Wall Street's call for 55 cents, with third-quarter adjusted earnings of 84 cents per share showcasing its competitiveness in the server market.

- CVS Health Performance Boost: CVS Health shares gained 4% after reporting first-quarter adjusted earnings of $2.57 per share and revenue of $100.43 billion, both exceeding analyst expectations, while the company raised its full-year earnings outlook, reflecting strong performance in the pharmacy benefits sector.

- Lucid Group Worsening Losses: Lucid Group shares fell 3% as the company reported a first-quarter loss of $3.46 per share, significantly worse than the expected loss of $2.64, with revenue of $282.5 million missing the $440.4 million target, highlighting challenges in the electric vehicle market.

See More

Hut 8 Signs $9.8 Billion Lease for AI Data Center

- Long-Term Lease Agreement: Hut 8 has signed a 15-year lease worth $9.8 billion with an undisclosed tenant, indicating rising demand for AI model infrastructure and expected future revenue growth for the company.

- Capacity Expansion: The agreement covers 352 megawatts of initial project capacity, increasing Hut 8's total contracted AI data center capacity to 597 megawatts and raising the total contract value to approximately $16.8 billion, showcasing the company's strong growth potential in the AI sector.

- Project Construction Timeline: The project, located in Nueces County, Texas, is expected to connect power in early 2027, with the first building scheduled for completion later that year, indicating Hut 8's strategic positioning to meet the growing computing and energy needs of AI firms.

- Strategic Partnerships: The project is being built in collaboration with partners including American Electric Power, Vertiv, and Jacobs, utilizing Nvidia's latest data center systems, reflecting intensified competition in AI infrastructure and Hut 8's proactive expansion in the market.

See More

Hut 8 Signs $25.1 Billion Lease with High-Investment-Grade Tenant

- Significant Lease Value: Hut 8's 15-year lease with a high-investment-grade tenant is valued at $9.8 billion, potentially reaching $25.1 billion if all renewal options are exercised, significantly enhancing the company's financial stability and market competitiveness.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate base-term contract value of approximately $16.8 billion, and an expected annual net operating income of about $1.1 billion, further solidifying its leadership in AI infrastructure.

- Flexible Development Model: Hut 8's power-first development model repositioned the site originally designed for American Bitcoin Corp. to AI infrastructure, showcasing the company's flexibility and innovative capacity in responding to evolving market demands.

- Strategic Partnerships: Hut 8 collaborates with top-tier partners like NVIDIA, Jacobs, and Vertiv to develop Beacon Point, ensuring efficient execution in technology, engineering, and critical systems delivery, thereby enhancing the company's market reputation and execution capabilities.

See More

Hut 8 Signs $9.8 Billion Lease with High-Investment-Grade Tenant

- Lease Scale: Hut 8 has signed a 15-year lease valued at $9.8 billion with a high-investment-grade tenant for 352 MW of IT capacity, which is expected to significantly enhance the company's revenue streams and market position.

- Data Center Expansion: This transaction increases Hut 8's total contracted AI data center capacity to 597 MW, with an aggregate contract value of approximately $16.8 billion, indicating strong performance in the rapidly growing AI infrastructure market.

- Technical Collaboration: Hut 8 will deliver a 352 MW AI factory designed to NVIDIA's DSX reference architecture, showcasing the company's technical capabilities and market adaptability in high-performance computing, likely attracting more high-end clients.

- Sustainability Strategy: The initial delivery of the project is expected in Q3 2027, and Hut 8 ensures efficient execution and long-term sustainability through collaboration with Tier 1 partners, further solidifying its leadership position in the energy infrastructure sector.

See More

Jacobs Solutions Q2 2026 Earnings: Strong Performance

- Significant Earnings Growth: Jacobs Solutions reported a 22% increase in adjusted EPS to $1.75 for Q2 FY 2026, driven by 9% organic net revenue growth, surpassing the 8% growth rate in Q1, indicating strong market performance and enhanced profitability.

- Record Backlog: The company's backlog grew by 22% to $27 billion, setting a new record with a trailing 12-month book-to-bill ratio of 1.4x, reflecting strong confidence in future project delivery capabilities and market demand.

- Data Center Business Surge: Jacobs reported over 100% year-on-year growth in its data center business for Q2, with a strengthening strategic partnership with NVIDIA, highlighting the company's advantageous position in the rapidly growing AI infrastructure market.

- Optimistic Financial Outlook: The company raised its FY 2026 organic net revenue growth range to 8% to 10.5%, with adjusted EBITDA margin expectations of 14.6% to 14.9%, signaling management's confidence in future performance and providing positive signals to investors.

See More

Jacobs Solutions Raises Annual Profit Forecast Amid Data Center Demand

- Profit Forecast Increase: Jacobs Solutions has raised its annual profit forecast, banking on strong demand for data center infrastructure services, indicating a positive outlook for the company in the market.

- Surge in Data Center Construction: The rapid advancement of artificial intelligence technologies has led to a surge in data center construction demand, significantly increasing Jacobs Solutions' business volume in planning, engineering, and construction management services, further driving revenue growth.

- Demand-Driven Market: The spike in demand for data center infrastructure services reflects the industry's urgent need for high-performance computing capabilities, which is expected to lead to sustained revenue growth and market share expansion for Jacobs Solutions.

- Strategic Positioning Advantage: Jacobs Solutions' expertise and experience in the data center sector enable it to effectively seize market opportunities, thereby maintaining a competitive edge in a challenging environment and enhancing its long-term growth potential.

See More