Arista Networks Q1 Earnings Preview: Strong Growth Expected

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Should l Buy ANET?

Source: seekingalpha

- Strong Earnings Expectations: Arista Networks is projected to see a nearly 25% increase in Q1 earnings, driven by ongoing demand from hyperscale cloud customers and superior Ethernet networking solutions, with an expected EPS of $0.81 and revenue of $2.62 billion, reflecting a 31% year-over-year rise.

- Consistent Historical Performance: Over the past two years, Arista has beaten both EPS and revenue estimates 100% of the time, further enhancing market optimism for this quarter's results, showcasing the company's robust competitive position in the industry.

- Future Guidance Focus: The management previously raised the 2026 fiscal year revenue outlook to $11.25 billion, targeting a 25% growth, while maintaining gross margin guidance between 62% and 64% and operating margin at approximately 46%, indicating strong confidence in future growth.

- Risk Factors Highlighted: Despite the optimistic outlook, analysts caution that a muted or negative reaction could occur if future guidance does not meaningfully increase, particularly if Ethernet-based AI networking adoption does not scale as quickly as anticipated, potentially leading to a sharp de-rating of the stock.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ANET?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ANET

Wall Street analysts forecast ANET stock price to rise

10 Analyst Rating

9 Buy

1 Hold

0 Sell

Strong Buy

Current: 170.220

Low

159.00

Averages

172.88

High

200.00

Current: 170.220

Low

159.00

Averages

172.88

High

200.00

About ANET

Arista Networks, Inc. is a provider of data-driven, client-to-cloud networking for large artificial intelligence (AI), data center, campus and routing environments. Its platforms deliver availability, agility, automation, analytics, and security through an advanced network operating stack. Its platform is its Extensible Operating System (EOS), a modernized publish-subscribe state-sharing networking operating system. Its portfolio of products, services and technologies is grouped into various categories: Core (Data Center, Cloud and AI Networking), Cognitive Adjacencies (Campus and Routing), and Cognitive Network (Software and Services). It offers product portfolios of data-driven, high-speed, cloud and data center Ethernet switches. Its Cognitive Adjacencies include Cognitive Campus Switching, Cloud-Grade Routing and WAN Routing. Its software and services are based on subscription-based models and include various offerings: CloudVision, Arista A-Care Services, CloudEOS and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

U.S. Stock Futures Rise as Investor Sentiment Improves

- Arista Networks Performance: Despite Arista Networks reporting a first-quarter revenue of $2.71 billion, exceeding Wall Street's $2.62 billion estimate, and earnings per share of $0.87, above the $0.81 forecast, its stock fell about 9% in premarket trading, reflecting market concerns over supply constraints.

- Novo Nordisk Optimism: Novo Nordisk's stock rose 5.98% in premarket trading after the company raised its full-year outlook, expecting a contraction in adjusted sales and operating profit to improve from a previous forecast of a 5% to 13% decline to a new range of 4% to 12%, driven by strong early demand for its oral Wegovy pill.

- AMC Entertainment Recovery: AMC Entertainment's stock increased approximately 8% in premarket trading as it reported a smaller quarterly loss, with revenue climbing 21.7% to $1.05 billion, and net loss narrowing from $202.1 million to $117.1 million year-over-year, while adjusted EBITDA turned positive at $38.3 million, indicating a rebound in moviegoing.

- Restaurant Brands International Performance: Restaurant Brands International topped estimates in its first-quarter earnings report, achieving system-wide sales growth of 6.2% and comparable sales growth of 3.2%, exceeding the consensus expectation of 3.0%, primarily driven by a 5.8% increase in the Burger King segment, showcasing strong performance in the fast-food market.

See More

Arista Networks Faces Significant Chip Shortages Amid AI Demand

- Revenue and Earnings Beat: Arista Networks reported first-quarter revenue of $2.70 billion, a 35% increase year-over-year, surpassing the $2.62 billion estimate, with adjusted earnings per share of $0.87 exceeding the $0.81 forecast, demonstrating resilience in a strong demand environment.

- Supply Chain Pressures: CEO Ullal highlighted significant wafer fab shortages due to rapid AI infrastructure buildout, resulting in lead times of 52 weeks for chip replenishment, which hampers the company's ability to fulfill commitments to customers.

- Cautious Future Outlook: While the second-quarter revenue is projected at $2.8 billion, slightly below the $2.81 billion estimate, and adjusted earnings per share at $0.88, just above the $0.87 estimate, the company anticipates near-term gross margin pressure due to higher procurement costs to meet demand.

- Market Sentiment Shift: On Stocktwits, retail sentiment for ANET shifted from 'bullish' to 'extremely bullish', with message volumes surging nearly 20 times in the last 24 hours, as some users view the current dip as a buying opportunity, reflecting confidence in the company's long-term growth prospects.

See More

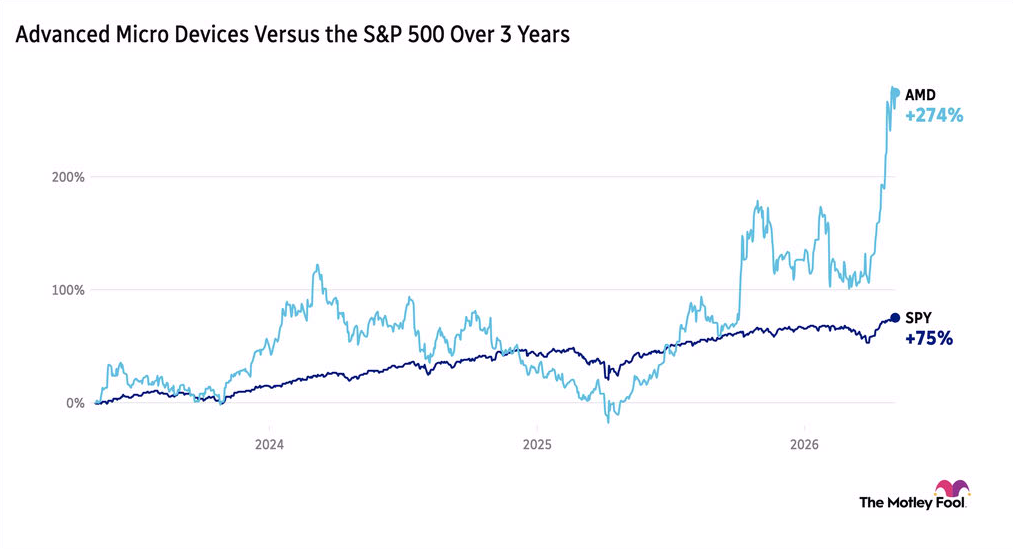

AMD Shares Surge 17% on Surge in Chip Demand

- Earnings Beat: AMD reported a 38% year-over-year revenue increase and a 43% rise in non-GAAP EPS for Q1 2026, exceeding market expectations and driving a 17% pre-market stock surge, highlighting the company's robust performance amid soaring AI infrastructure demand.

- Strategic Partnership: The collaboration with Meta is set to deploy 6 gigawatts of Instinct GPUs, which not only enhances AMD's competitive edge in the AI market but also lays a solid foundation for future revenue growth.

- Future Guidance: Management forecasts Q2 revenue to reach $11.2 billion, a 9% increase from Q1, translating to a 46% year-over-year growth, reflecting sustained growth potential and market confidence in AMD's AI initiatives.

- Market Reaction: Despite AMD's strong performance, Arista Networks saw a 9% drop in stock price due to cost pressures, indicating that supply chain challenges and rising costs in the semiconductor industry may affect overall market sentiment.

See More

Significant Stock Movements for AMD and Others

- AMD Strong Guidance: AMD shares surged 20% after issuing a second-quarter revenue forecast of $11.2 billion, exceeding the analyst estimate of $10.52 billion, with first-quarter results also surpassing expectations, indicating robust performance in the semiconductor market.

- Super Micro Earnings Beat: Super Micro's stock jumped nearly 15% as fourth-quarter profit expectations range from 65 to 79 cents per share, significantly above Wall Street's call for 55 cents, with third-quarter adjusted earnings of 84 cents per share showcasing its competitiveness in the server market.

- CVS Health Performance Boost: CVS Health shares gained 4% after reporting first-quarter adjusted earnings of $2.57 per share and revenue of $100.43 billion, both exceeding analyst expectations, while the company raised its full-year earnings outlook, reflecting strong performance in the pharmacy benefits sector.

- Lucid Group Worsening Losses: Lucid Group shares fell 3% as the company reported a first-quarter loss of $3.46 per share, significantly worse than the expected loss of $2.64, with revenue of $282.5 million missing the $440.4 million target, highlighting challenges in the electric vehicle market.

See More

ARISTA NETWORKS INC: PIPER SANDLER INCREASES TARGET PRICE TO $181, UP FROM $175

Price Increase Announcement: The price of Piper Sandler's target has been raised to $181 from $175.

Market Impact: This adjustment reflects changes in market conditions and expectations for the company's performance.

See More

Arista Networks Q1 2026 Earnings Call Insights

- Market Share Growth: Arista Networks has achieved the number one market share in the over 10G Ethernet category, as CEO Ullal noted, reflecting strong growth in high-speed switching, which is expected to further solidify its market leadership.

- Strong Financial Performance: Total revenues for Q1 reached $2.71 billion with a net income of $1.11 billion, demonstrating the company's ability to achieve substantial profitability despite facing supply chain challenges amid strong demand.

- Optimistic Future Outlook: Management raised the fiscal year 2026 revenue growth outlook to 27.7%, anticipating approximately $11.5 billion in revenue, while increasing the AI business target from $3.25 billion to $3.5 billion, indicating confidence in future growth.

- Ongoing Supply Chain Pressures: Ullal highlighted that industry-wide shortages are expected to persist for 1 to 2 years, and despite anticipated gross margin pressures, the company will prioritize ensuring supply continuity to meet customer demand, a strategy that may impact future profitability.

See More

U.S. Stock Futures Rise as Investor Sentiment Improves

- Arista Networks Performance: Despite Arista Networks reporting a first-quarter revenue of $2.71 billion, exceeding Wall Street's $2.62 billion estimate, and earnings per share of $0.87, above the $0.81 forecast, its stock fell about 9% in premarket trading, reflecting market concerns over supply constraints.

- Novo Nordisk Optimism: Novo Nordisk's stock rose 5.98% in premarket trading after the company raised its full-year outlook, expecting a contraction in adjusted sales and operating profit to improve from a previous forecast of a 5% to 13% decline to a new range of 4% to 12%, driven by strong early demand for its oral Wegovy pill.

- AMC Entertainment Recovery: AMC Entertainment's stock increased approximately 8% in premarket trading as it reported a smaller quarterly loss, with revenue climbing 21.7% to $1.05 billion, and net loss narrowing from $202.1 million to $117.1 million year-over-year, while adjusted EBITDA turned positive at $38.3 million, indicating a rebound in moviegoing.

- Restaurant Brands International Performance: Restaurant Brands International topped estimates in its first-quarter earnings report, achieving system-wide sales growth of 6.2% and comparable sales growth of 3.2%, exceeding the consensus expectation of 3.0%, primarily driven by a 5.8% increase in the Burger King segment, showcasing strong performance in the fast-food market.

See More

Arista Networks Faces Significant Chip Shortages Amid AI Demand

- Revenue and Earnings Beat: Arista Networks reported first-quarter revenue of $2.70 billion, a 35% increase year-over-year, surpassing the $2.62 billion estimate, with adjusted earnings per share of $0.87 exceeding the $0.81 forecast, demonstrating resilience in a strong demand environment.

- Supply Chain Pressures: CEO Ullal highlighted significant wafer fab shortages due to rapid AI infrastructure buildout, resulting in lead times of 52 weeks for chip replenishment, which hampers the company's ability to fulfill commitments to customers.

- Cautious Future Outlook: While the second-quarter revenue is projected at $2.8 billion, slightly below the $2.81 billion estimate, and adjusted earnings per share at $0.88, just above the $0.87 estimate, the company anticipates near-term gross margin pressure due to higher procurement costs to meet demand.

- Market Sentiment Shift: On Stocktwits, retail sentiment for ANET shifted from 'bullish' to 'extremely bullish', with message volumes surging nearly 20 times in the last 24 hours, as some users view the current dip as a buying opportunity, reflecting confidence in the company's long-term growth prospects.

See More

AMD Shares Surge 17% on Surge in Chip Demand

- Earnings Beat: AMD reported a 38% year-over-year revenue increase and a 43% rise in non-GAAP EPS for Q1 2026, exceeding market expectations and driving a 17% pre-market stock surge, highlighting the company's robust performance amid soaring AI infrastructure demand.

- Strategic Partnership: The collaboration with Meta is set to deploy 6 gigawatts of Instinct GPUs, which not only enhances AMD's competitive edge in the AI market but also lays a solid foundation for future revenue growth.

- Future Guidance: Management forecasts Q2 revenue to reach $11.2 billion, a 9% increase from Q1, translating to a 46% year-over-year growth, reflecting sustained growth potential and market confidence in AMD's AI initiatives.

- Market Reaction: Despite AMD's strong performance, Arista Networks saw a 9% drop in stock price due to cost pressures, indicating that supply chain challenges and rising costs in the semiconductor industry may affect overall market sentiment.

See More

Significant Stock Movements for AMD and Others

- AMD Strong Guidance: AMD shares surged 20% after issuing a second-quarter revenue forecast of $11.2 billion, exceeding the analyst estimate of $10.52 billion, with first-quarter results also surpassing expectations, indicating robust performance in the semiconductor market.

- Super Micro Earnings Beat: Super Micro's stock jumped nearly 15% as fourth-quarter profit expectations range from 65 to 79 cents per share, significantly above Wall Street's call for 55 cents, with third-quarter adjusted earnings of 84 cents per share showcasing its competitiveness in the server market.

- CVS Health Performance Boost: CVS Health shares gained 4% after reporting first-quarter adjusted earnings of $2.57 per share and revenue of $100.43 billion, both exceeding analyst expectations, while the company raised its full-year earnings outlook, reflecting strong performance in the pharmacy benefits sector.

- Lucid Group Worsening Losses: Lucid Group shares fell 3% as the company reported a first-quarter loss of $3.46 per share, significantly worse than the expected loss of $2.64, with revenue of $282.5 million missing the $440.4 million target, highlighting challenges in the electric vehicle market.

See More

ARISTA NETWORKS INC: PIPER SANDLER INCREASES TARGET PRICE TO $181, UP FROM $175

Price Increase Announcement: The price of Piper Sandler's target has been raised to $181 from $175.

Market Impact: This adjustment reflects changes in market conditions and expectations for the company's performance.

See More

Arista Networks Q1 2026 Earnings Call Insights

- Market Share Growth: Arista Networks has achieved the number one market share in the over 10G Ethernet category, as CEO Ullal noted, reflecting strong growth in high-speed switching, which is expected to further solidify its market leadership.

- Strong Financial Performance: Total revenues for Q1 reached $2.71 billion with a net income of $1.11 billion, demonstrating the company's ability to achieve substantial profitability despite facing supply chain challenges amid strong demand.

- Optimistic Future Outlook: Management raised the fiscal year 2026 revenue growth outlook to 27.7%, anticipating approximately $11.5 billion in revenue, while increasing the AI business target from $3.25 billion to $3.5 billion, indicating confidence in future growth.

- Ongoing Supply Chain Pressures: Ullal highlighted that industry-wide shortages are expected to persist for 1 to 2 years, and despite anticipated gross margin pressures, the company will prioritize ensuring supply continuity to meet customer demand, a strategy that may impact future profitability.

See More