American Airlines Rejects United Airlines Merger Proposal as Anti-Competitive

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 4 hours ago

0mins

Should l Buy TSM?

Source: Fool

- Merger Proposal Rejected: American Airlines shares fell in pre-market trading on Monday after firmly rejecting United Airlines' merger proposal, citing significant antitrust hurdles that would give the combined entity a 40% domestic market share, negatively impacting competition.

- Regulatory Scrutiny Pressure: Legal experts suggest that a merger would face unprecedented scrutiny, as the 'Big Four' airlines already control 80% of U.S. capacity, potentially dominating key hubs like Chicago and Dallas by up to 70%.

- Strategic Shift Possible: Despite the rejection, United Airlines may pivot towards smaller acquisitions or asset divestitures to satisfy an administration favoring landmark deals while avoiding concerns over consumer pricing monopolies, thereby maintaining competitive positioning.

- Market Reaction: Following the merger proposal rejection, American Airlines' stock dropped 3.13% and United Airlines' stock fell 3.04%, reflecting market pessimism regarding the merger prospects and potentially influencing future strategic decisions for both companies.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TSM?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on TSM

Wall Street analysts forecast TSM stock price to fall

8 Analyst Rating

7 Buy

1 Hold

0 Sell

Strong Buy

Current: 370.500

Low

63.24

Averages

313.46

High

390.00

Current: 370.500

Low

63.24

Averages

313.46

High

390.00

About TSM

Taiwan Semiconductor Manufacturing Co Ltd is a Taiwan-based integrated circuit foundry service provider. The Company is primarily engaged in integrated circuit manufacturing services. It offers advanced process technologies, specialised process solutions, advanced photomask and silicon stacking, and packaging-related technologies, while supporting a comprehensive design ecosystem. The Company's products serve diverse electronic sectors including artificial intelligence, high-performance computing, wired and wireless communications, automotive and industrial equipment, personal computing, information applications, consumer electronics, smart internet of things, and wearable devices.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

TSMC Reports Strong Q1 Results Driven by AI Demand

- Significant Earnings Growth: TSMC's net income soared to $18.1 billion in Q1, reflecting a nearly 59% year-over-year increase, while sales surged 41% to $35 billion, showcasing the company's robust performance driven by AI-related demand and solidifying its market leadership.

- Advanced Chip Sales Dominance: In the first quarter, approximately 74% of TSMC's processor sales came from advanced chips, with 25% from the cutting-edge 3-nanometer processors, indicating not only the rising demand for AI processors but also the industry's reliance on higher technological standards.

- Accelerated Expansion Plans: TSMC anticipates continued strong demand support moving into Q2 2026, with management planning to expand manufacturing capacity in Taiwan and Arizona to meet the growing AI demand, reflecting the company's confidence in future market trends.

- Increased Capital Expenditure: Due to the ongoing growth of AI, TSMC expects its capital expenditures to exceed the high end of its previous estimate of $52 billion to $56 billion for this year, representing a 37% increase from 2025, highlighting the company's commitment to the AI trend and its long-term investment potential.

See More

American Airlines Rejects United Airlines Merger Proposal as Anti-Competitive

- Merger Proposal Rejected: American Airlines shares fell in pre-market trading on Monday after firmly rejecting United Airlines' merger proposal, citing significant antitrust hurdles that would give the combined entity a 40% domestic market share, negatively impacting competition.

- Regulatory Scrutiny Pressure: Legal experts suggest that a merger would face unprecedented scrutiny, as the 'Big Four' airlines already control 80% of U.S. capacity, potentially dominating key hubs like Chicago and Dallas by up to 70%.

- Strategic Shift Possible: Despite the rejection, United Airlines may pivot towards smaller acquisitions or asset divestitures to satisfy an administration favoring landmark deals while avoiding concerns over consumer pricing monopolies, thereby maintaining competitive positioning.

- Market Reaction: Following the merger proposal rejection, American Airlines' stock dropped 3.13% and United Airlines' stock fell 3.04%, reflecting market pessimism regarding the merger prospects and potentially influencing future strategic decisions for both companies.

See More

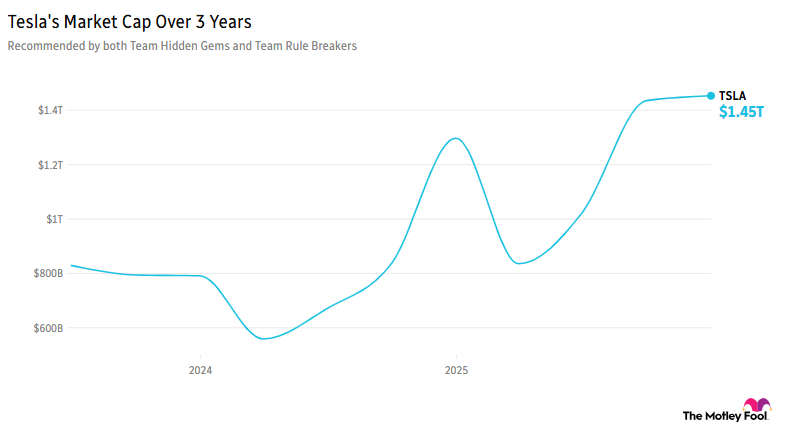

Tesla Set to Report Q1 Earnings Amid Market Surge

- Tesla Earnings Outlook: Tesla is set to report its Q1 fiscal 2026 earnings on Wednesday, with the stock down 11% year-to-date; however, it has shown recovery in April as CEO Elon Musk garners attention for the upcoming SpaceX IPO, and analysts predict profit growth despite vehicle deliveries of 358,000 falling short of the 370,000 expected.

- Terafab Project Acceleration: Musk is urging potential suppliers to expedite the Terafab AI chip-making project, which is estimated to cost over $25 billion and aims to achieve an annual computing capacity of one terawatt, highlighting Tesla's ambitions in the AI sector.

- Market Performance Surge: Despite uncertainties surrounding dealings with Iran, both the S&P 500 and Nasdaq reached new all-time highs, rising 4.5% and 6.8% respectively, while the Dow Jones increased by 3.2%, indicating a robust market recovery.

- Oil Price Impact: Following the U.S. Navy's seizure of an Iranian-flagged ship, benchmark crude prices surged over 6%, with West Texas Intermediate surpassing $88 and Brent crude exceeding $95, which could influence market sentiment.

See More

Semiconductor Firms Challenge Apple's Valuation

- Revenue Growth Comparison: Broadcom achieved a 28% year-over-year revenue growth last quarter, while Apple only grew by 16%, indicating Broadcom's strong performance in high-speed networking hardware and AI accelerators, which could significantly enhance its market value in the coming years.

- AI Chip Demand Outlook: Broadcom anticipates over $100 billion in AI chip revenue by 2027; despite risks from customer concentration, its robust profitability and strong market demand could drive its market cap to double.

- TSMC Market Dominance: Taiwan Semiconductor Manufacturing holds a 72% share of the foundry market, with a 40% year-over-year revenue growth in Q1, and AI chip demand expected to grow over 50% annually, further solidifying its leadership in the semiconductor industry.

- Investor Focus: Broadcom and TSMC stocks trade at 35 and 25 times earnings, respectively, and if they meet analysts' earnings growth expectations, they could surpass Apple's valuation in the coming years, attracting long-term investor interest.

See More

Broadcom and TSMC: Core Players in AI Industry

- Broadcom's Strong Momentum: Broadcom achieved a 28% year-over-year revenue growth last quarter, significantly outpacing Apple's 16%, indicating that its robust performance in the AI semiconductor market could drive its market cap to double in the coming years.

- TSMC's Market Dominance: TSMC holds a 72% share of the foundry market, with first-quarter revenue growth accelerating to 40%, and AI chip demand is expected to grow over 50% annually, further solidifying its market position.

- Significant Earnings Growth Disparity: Analysts project Broadcom's earnings per share to grow at an annualized rate of 41%, compared to Apple's 11%, positioning Broadcom with the potential to surpass Apple's market cap in the coming years.

- Risks and Opportunities: While Broadcom's reliance on six major AI customers poses a risk of spending pauses, its visibility into over $100 billion in future AI chip revenue underscores its critical role in an AI-driven economy.

See More

TSMC Reports Strong Q1 Results Amid AI Chip Demand Surge

- Significant Revenue Growth: TSMC reported a 35% year-over-year revenue increase in Q1, reaching approximately $39 billion, highlighting its strong demand in the AI chip market and reinforcing its leadership position in the semiconductor industry.

- Gross Margin Expansion: The gross margin for Q1 was 66.2%, up 740 basis points from 58.8% a year ago, demonstrating the company's strong pricing power and technological advancements despite cost pressures from new U.S. fabs.

- Capital Expenditure Plans: TSMC anticipates its 2023 capital expenditures will be at the high end of its $52 billion to $56 billion guidance, having spent over $11 billion in Q1 primarily to expand its 3nm technology capacity to meet the growing demand for AI chips.

- Optimistic Future Outlook: The company projects Q2 revenue between $39 billion and $40.2 billion, representing about 32% year-over-year growth, and expects full-year revenue growth of over 30%, reflecting a sustained optimistic outlook on AI chip demand.

See More

TSMC Reports Strong Q1 Results Driven by AI Demand

- Significant Earnings Growth: TSMC's net income soared to $18.1 billion in Q1, reflecting a nearly 59% year-over-year increase, while sales surged 41% to $35 billion, showcasing the company's robust performance driven by AI-related demand and solidifying its market leadership.

- Advanced Chip Sales Dominance: In the first quarter, approximately 74% of TSMC's processor sales came from advanced chips, with 25% from the cutting-edge 3-nanometer processors, indicating not only the rising demand for AI processors but also the industry's reliance on higher technological standards.

- Accelerated Expansion Plans: TSMC anticipates continued strong demand support moving into Q2 2026, with management planning to expand manufacturing capacity in Taiwan and Arizona to meet the growing AI demand, reflecting the company's confidence in future market trends.

- Increased Capital Expenditure: Due to the ongoing growth of AI, TSMC expects its capital expenditures to exceed the high end of its previous estimate of $52 billion to $56 billion for this year, representing a 37% increase from 2025, highlighting the company's commitment to the AI trend and its long-term investment potential.

See More

American Airlines Rejects United Airlines Merger Proposal as Anti-Competitive

- Merger Proposal Rejected: American Airlines shares fell in pre-market trading on Monday after firmly rejecting United Airlines' merger proposal, citing significant antitrust hurdles that would give the combined entity a 40% domestic market share, negatively impacting competition.

- Regulatory Scrutiny Pressure: Legal experts suggest that a merger would face unprecedented scrutiny, as the 'Big Four' airlines already control 80% of U.S. capacity, potentially dominating key hubs like Chicago and Dallas by up to 70%.

- Strategic Shift Possible: Despite the rejection, United Airlines may pivot towards smaller acquisitions or asset divestitures to satisfy an administration favoring landmark deals while avoiding concerns over consumer pricing monopolies, thereby maintaining competitive positioning.

- Market Reaction: Following the merger proposal rejection, American Airlines' stock dropped 3.13% and United Airlines' stock fell 3.04%, reflecting market pessimism regarding the merger prospects and potentially influencing future strategic decisions for both companies.

See More

Tesla Set to Report Q1 Earnings Amid Market Surge

- Tesla Earnings Outlook: Tesla is set to report its Q1 fiscal 2026 earnings on Wednesday, with the stock down 11% year-to-date; however, it has shown recovery in April as CEO Elon Musk garners attention for the upcoming SpaceX IPO, and analysts predict profit growth despite vehicle deliveries of 358,000 falling short of the 370,000 expected.

- Terafab Project Acceleration: Musk is urging potential suppliers to expedite the Terafab AI chip-making project, which is estimated to cost over $25 billion and aims to achieve an annual computing capacity of one terawatt, highlighting Tesla's ambitions in the AI sector.

- Market Performance Surge: Despite uncertainties surrounding dealings with Iran, both the S&P 500 and Nasdaq reached new all-time highs, rising 4.5% and 6.8% respectively, while the Dow Jones increased by 3.2%, indicating a robust market recovery.

- Oil Price Impact: Following the U.S. Navy's seizure of an Iranian-flagged ship, benchmark crude prices surged over 6%, with West Texas Intermediate surpassing $88 and Brent crude exceeding $95, which could influence market sentiment.

See More

Semiconductor Firms Challenge Apple's Valuation

- Revenue Growth Comparison: Broadcom achieved a 28% year-over-year revenue growth last quarter, while Apple only grew by 16%, indicating Broadcom's strong performance in high-speed networking hardware and AI accelerators, which could significantly enhance its market value in the coming years.

- AI Chip Demand Outlook: Broadcom anticipates over $100 billion in AI chip revenue by 2027; despite risks from customer concentration, its robust profitability and strong market demand could drive its market cap to double.

- TSMC Market Dominance: Taiwan Semiconductor Manufacturing holds a 72% share of the foundry market, with a 40% year-over-year revenue growth in Q1, and AI chip demand expected to grow over 50% annually, further solidifying its leadership in the semiconductor industry.

- Investor Focus: Broadcom and TSMC stocks trade at 35 and 25 times earnings, respectively, and if they meet analysts' earnings growth expectations, they could surpass Apple's valuation in the coming years, attracting long-term investor interest.

See More

Broadcom and TSMC: Core Players in AI Industry

- Broadcom's Strong Momentum: Broadcom achieved a 28% year-over-year revenue growth last quarter, significantly outpacing Apple's 16%, indicating that its robust performance in the AI semiconductor market could drive its market cap to double in the coming years.

- TSMC's Market Dominance: TSMC holds a 72% share of the foundry market, with first-quarter revenue growth accelerating to 40%, and AI chip demand is expected to grow over 50% annually, further solidifying its market position.

- Significant Earnings Growth Disparity: Analysts project Broadcom's earnings per share to grow at an annualized rate of 41%, compared to Apple's 11%, positioning Broadcom with the potential to surpass Apple's market cap in the coming years.

- Risks and Opportunities: While Broadcom's reliance on six major AI customers poses a risk of spending pauses, its visibility into over $100 billion in future AI chip revenue underscores its critical role in an AI-driven economy.

See More

TSMC Reports Strong Q1 Results Amid AI Chip Demand Surge

- Significant Revenue Growth: TSMC reported a 35% year-over-year revenue increase in Q1, reaching approximately $39 billion, highlighting its strong demand in the AI chip market and reinforcing its leadership position in the semiconductor industry.

- Gross Margin Expansion: The gross margin for Q1 was 66.2%, up 740 basis points from 58.8% a year ago, demonstrating the company's strong pricing power and technological advancements despite cost pressures from new U.S. fabs.

- Capital Expenditure Plans: TSMC anticipates its 2023 capital expenditures will be at the high end of its $52 billion to $56 billion guidance, having spent over $11 billion in Q1 primarily to expand its 3nm technology capacity to meet the growing demand for AI chips.

- Optimistic Future Outlook: The company projects Q2 revenue between $39 billion and $40.2 billion, representing about 32% year-over-year growth, and expects full-year revenue growth of over 30%, reflecting a sustained optimistic outlook on AI chip demand.

See More