AM Best Assigns Excellent Rating to Progressive Corporation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 27 2026

0mins

Should l Buy PGR?

Source: Newsfilter

- Credit Rating Assignment: AM Best has assigned an 'a' (Excellent) Long-Term Issuer Credit Rating to Progressive's $500 million 4.60% and $1 billion 5.15% senior unsecured notes, indicating the company's robust position and financial health in the insurance sector.

- Stable Outlook: The stable outlook for these ratings suggests that AM Best expects Progressive's financial leverage and interest coverage metrics to remain within the guidelines for the assigned ratings, thereby bolstering investor confidence.

- Clear Use of Proceeds: Progressive intends to utilize the proceeds from these bond issuances for general corporate purposes, a strategy that will help the company maintain flexibility and financial stability in its future operations and expansions.

- Unchanged Ratings: The Long-Term Issuer Credit Rating for Progressive and the ratings and outlooks on its other debt issuances remain unchanged, reflecting the company's ongoing competitiveness and sound financial management in the insurance market.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PGR?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PGR

Wall Street analysts forecast PGR stock price to rise

16 Analyst Rating

9 Buy

6 Hold

1 Sell

Moderate Buy

Current: 203.470

Low

214.00

Averages

257.11

High

328.00

Current: 203.470

Low

214.00

Averages

257.11

High

328.00

About PGR

The Progressive Corporation is an insurance holding company, which has insurance and non-insurance subsidiaries and affiliates. The Company's segments include Personal Lines, Commercial Lines and Other indemnity. The Personal Lines segment writes insurance for personal autos and special lines products. Its special lines of products include recreational vehicles, such as motorcycles, RVs, and watercraft. The Company's Personal Lines products are sold through both the agency and direct channels. The Commercial Lines segment writes auto-related liability and physical damage insurance, business-related general liability and commercial property insurance predominately for small businesses, and workers’ compensation insurance primarily for the transportation industry. Its reinsurance activity includes both transactions which are regulated and those that are non-regulated. It offers Snapshot through hardware-based and/or mobile-app versions in all states, other than California.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Investment Opportunities in Insurance Stocks

- Stability in Insurance Sector: Insurance companies generally provide strong cash flow and stability to weather various economic environments; however, Progressive's stock has fallen 30% from its 52-week high, indicating increased market competition pressures.

- AI Advantage of Lemonade: Lemonade leverages artificial intelligence to optimize its business, generating $738 million in revenue last year with a 40% growth, despite a net loss of $166 million; its gross loss ratio improved to 64% in Q4, indicating significant enhancements in risk pricing capabilities.

- Long-Term Performance of Progressive: As a well-established insurance company, Progressive has achieved a 17% annualized return over the past three decades, writing $83 billion in net premiums and generating $11.3 billion in net income in 2022, showcasing its strengths in risk pricing and profitability.

- Intensifying Market Competition: Although Progressive's stock is under pressure due to a softening market with an expected 1% average premium increase in 2026, its current P/E ratio of just 10 times indicates it remains a solid investment choice given its long-term underwriting excellence.

See More

Insurance Stocks: Stability and Cash Flow Potential

- Stability of Insurance Stocks: Insurance stocks typically provide strong cash flow and stability, capable of weathering various economic environments, particularly as rising interest rates and prices create a hedge through their pricing power and large investment portfolios.

- Progressive's Market Performance: Despite Progressive's stock tumbling 30% from its 52-week high, it has delivered an impressive 17% annualized return over the past three decades, demonstrating its excellence in risk pricing and management, with a net income of $11.3 billion last year.

- Lemonade's AI Advantage: Lemonade leverages AI to streamline operations, achieving $738 million in revenue last year, a 40% increase, although it posted a net loss of $166 million; its gross loss ratio improved to 64% in Q4, indicating significant progress in risk pricing.

- Divergent Investment Strategies: For investors looking to diversify their portfolios, Lemonade and Progressive cater to different strategies, with Lemonade still building its foundation and not expected to be profitable until 2028, while Progressive's low valuation and long-term underwriting excellence make it a more attractive buy right now.

See More

Progressive Q4 Earnings Report Exceeds Expectations

- Earnings Performance: Progressive reported a GAAP EPS of $4.80 for Q4, missing expectations by $0.08, indicating potential pressure on profitability that could affect investor confidence.

- Premium Revenue Growth: The company achieved net premiums written of $23.64 billion, a 6% year-over-year increase, beating market expectations by $441 million, demonstrating its competitive strength and expanding customer base.

- Long-Term Growth Potential: Despite the shortfall in EPS, Progressive is still viewed as a long-term compounder due to its strong underwriting discipline and market dominance, suggesting potential for higher profitability in the future.

- Market Reaction Analysis: Investors are cautious regarding the company's strategy of sacrificing margins for revenue growth, which may impact its stock performance, necessitating close monitoring of future profitability recovery.

See More

Progressive Corp. Reports March 2026 Net Income of $712 Million

- Net Income Growth: Progressive Corp. reported a net income of $712 million for March 2026, translating to $1.21 per share, which, while down from $901 million and $1.53 per share in March 2025, still indicates stable profitability for the company.

- Premium Revenue Increase: The net premiums written for March 2026 improved by 10% to $9.91 billion, while net premiums earned grew by 11% to $7.52 billion, demonstrating the company's sustained competitive strength in the market.

- Policy Count Expansion: As of March 31, 2026, the total number of policies in force increased by 9% to 39.57 million from 36.29 million in March 2025, indicating an expansion of the customer base and improved market penetration.

- Quarterly Performance: For the first quarter of 2026, net income reached $2.82 billion, or $4.80 per share, reflecting a 10% increase from $2.57 billion and $4.37 per share in the prior-year quarter, highlighting ongoing improvements in premium revenue and profitability.

See More

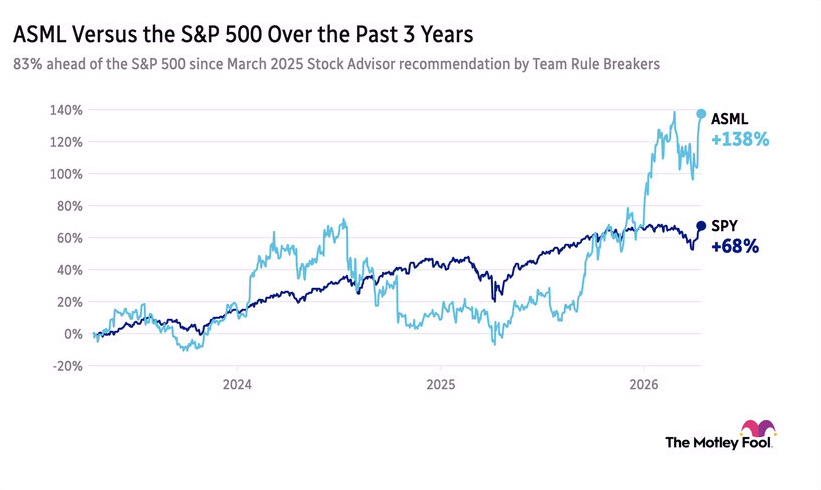

ASML Exceeds Expectations in Q1 Earnings Driven by AI Surge

- ASML Strong Performance: ASML reported first-quarter revenue and earnings that exceeded expectations, raising its full-year net sales guidance to between $42.4 billion and $47.2 billion, reflecting robust growth driven by AI spending in semiconductor production, although weaker Q2 sales forecasts limited pre-market stock gains to around 1%.

- Record Bank Earnings: JPMorgan Chase, Citigroup, and Wells Fargo collectively posted over $25 billion in profits for Q1, benefiting from market volatility due to geopolitical crises, with Citigroup's markets revenue growing 19% YoY, although Wells Fargo's stock fell 5.7% despite a 15% rise in EPS, highlighting investment banks' resilience in turbulent markets.

- Bank of America Steady Performance: Bank of America reported Q1 net income of $8.6 billion, a 17% increase YoY, driven by a 7% rise in revenue, with the CEO noting healthy client activity and stable asset quality, indicating a resilient U.S. economy, leading to a stock increase of about 1%.

- Morgan Stanley Record Revenue: Morgan Stanley announced record revenue of $70.6 billion for the 2025 fiscal year, with expectations that investment banking strength and M&A activity will boost EPS by around 12% this quarter, while also monitoring advancements in AI applications in client services.

See More

Major Earnings Reports Expected Before Wednesday's Open

- Earnings Report Preview: Major earnings reports are expected before the market opens on Wednesday, including Bank of America (BAC), ASML Holding (ASML), Morgan Stanley (MS), and PNC Financial Services Group (PNC), which will provide crucial insights into their financial health.

- Market Focus: Investors will closely monitor these earnings to assess company performance in the current economic climate, particularly under pressures from interest rates and inflation, which could influence market trends.

- Additional Earnings Releases: In addition to the major firms, earnings from FHN, MTB, PGR, and TRX are also slated for release before Wednesday's open, further enriching market information and aiding investors in making informed decisions.

- Earnings Season Calendar: Seeking Alpha offers a comprehensive earnings season calendar, allowing investors to access detailed information on upcoming earnings reports to ensure they do not miss any significant market developments.

See More

Investment Opportunities in Insurance Stocks

- Stability in Insurance Sector: Insurance companies generally provide strong cash flow and stability to weather various economic environments; however, Progressive's stock has fallen 30% from its 52-week high, indicating increased market competition pressures.

- AI Advantage of Lemonade: Lemonade leverages artificial intelligence to optimize its business, generating $738 million in revenue last year with a 40% growth, despite a net loss of $166 million; its gross loss ratio improved to 64% in Q4, indicating significant enhancements in risk pricing capabilities.

- Long-Term Performance of Progressive: As a well-established insurance company, Progressive has achieved a 17% annualized return over the past three decades, writing $83 billion in net premiums and generating $11.3 billion in net income in 2022, showcasing its strengths in risk pricing and profitability.

- Intensifying Market Competition: Although Progressive's stock is under pressure due to a softening market with an expected 1% average premium increase in 2026, its current P/E ratio of just 10 times indicates it remains a solid investment choice given its long-term underwriting excellence.

See More

Insurance Stocks: Stability and Cash Flow Potential

- Stability of Insurance Stocks: Insurance stocks typically provide strong cash flow and stability, capable of weathering various economic environments, particularly as rising interest rates and prices create a hedge through their pricing power and large investment portfolios.

- Progressive's Market Performance: Despite Progressive's stock tumbling 30% from its 52-week high, it has delivered an impressive 17% annualized return over the past three decades, demonstrating its excellence in risk pricing and management, with a net income of $11.3 billion last year.

- Lemonade's AI Advantage: Lemonade leverages AI to streamline operations, achieving $738 million in revenue last year, a 40% increase, although it posted a net loss of $166 million; its gross loss ratio improved to 64% in Q4, indicating significant progress in risk pricing.

- Divergent Investment Strategies: For investors looking to diversify their portfolios, Lemonade and Progressive cater to different strategies, with Lemonade still building its foundation and not expected to be profitable until 2028, while Progressive's low valuation and long-term underwriting excellence make it a more attractive buy right now.

See More

Progressive Q4 Earnings Report Exceeds Expectations

- Earnings Performance: Progressive reported a GAAP EPS of $4.80 for Q4, missing expectations by $0.08, indicating potential pressure on profitability that could affect investor confidence.

- Premium Revenue Growth: The company achieved net premiums written of $23.64 billion, a 6% year-over-year increase, beating market expectations by $441 million, demonstrating its competitive strength and expanding customer base.

- Long-Term Growth Potential: Despite the shortfall in EPS, Progressive is still viewed as a long-term compounder due to its strong underwriting discipline and market dominance, suggesting potential for higher profitability in the future.

- Market Reaction Analysis: Investors are cautious regarding the company's strategy of sacrificing margins for revenue growth, which may impact its stock performance, necessitating close monitoring of future profitability recovery.

See More

Progressive Corp. Reports March 2026 Net Income of $712 Million

- Net Income Growth: Progressive Corp. reported a net income of $712 million for March 2026, translating to $1.21 per share, which, while down from $901 million and $1.53 per share in March 2025, still indicates stable profitability for the company.

- Premium Revenue Increase: The net premiums written for March 2026 improved by 10% to $9.91 billion, while net premiums earned grew by 11% to $7.52 billion, demonstrating the company's sustained competitive strength in the market.

- Policy Count Expansion: As of March 31, 2026, the total number of policies in force increased by 9% to 39.57 million from 36.29 million in March 2025, indicating an expansion of the customer base and improved market penetration.

- Quarterly Performance: For the first quarter of 2026, net income reached $2.82 billion, or $4.80 per share, reflecting a 10% increase from $2.57 billion and $4.37 per share in the prior-year quarter, highlighting ongoing improvements in premium revenue and profitability.

See More

ASML Exceeds Expectations in Q1 Earnings Driven by AI Surge

- ASML Strong Performance: ASML reported first-quarter revenue and earnings that exceeded expectations, raising its full-year net sales guidance to between $42.4 billion and $47.2 billion, reflecting robust growth driven by AI spending in semiconductor production, although weaker Q2 sales forecasts limited pre-market stock gains to around 1%.

- Record Bank Earnings: JPMorgan Chase, Citigroup, and Wells Fargo collectively posted over $25 billion in profits for Q1, benefiting from market volatility due to geopolitical crises, with Citigroup's markets revenue growing 19% YoY, although Wells Fargo's stock fell 5.7% despite a 15% rise in EPS, highlighting investment banks' resilience in turbulent markets.

- Bank of America Steady Performance: Bank of America reported Q1 net income of $8.6 billion, a 17% increase YoY, driven by a 7% rise in revenue, with the CEO noting healthy client activity and stable asset quality, indicating a resilient U.S. economy, leading to a stock increase of about 1%.

- Morgan Stanley Record Revenue: Morgan Stanley announced record revenue of $70.6 billion for the 2025 fiscal year, with expectations that investment banking strength and M&A activity will boost EPS by around 12% this quarter, while also monitoring advancements in AI applications in client services.

See More

Major Earnings Reports Expected Before Wednesday's Open

- Earnings Report Preview: Major earnings reports are expected before the market opens on Wednesday, including Bank of America (BAC), ASML Holding (ASML), Morgan Stanley (MS), and PNC Financial Services Group (PNC), which will provide crucial insights into their financial health.

- Market Focus: Investors will closely monitor these earnings to assess company performance in the current economic climate, particularly under pressures from interest rates and inflation, which could influence market trends.

- Additional Earnings Releases: In addition to the major firms, earnings from FHN, MTB, PGR, and TRX are also slated for release before Wednesday's open, further enriching market information and aiding investors in making informed decisions.

- Earnings Season Calendar: Seeking Alpha offers a comprehensive earnings season calendar, allowing investors to access detailed information on upcoming earnings reports to ensure they do not miss any significant market developments.

See More