Alibaba Reports Significant Revenue and Profit Misses in Q4

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 19 2026

0mins

Should l Buy BABA?

Source: seekingalpha

- Revenue and Profit Decline: Alibaba's total revenue grew only 1.7% to RMB 284.84 billion in Q4, significantly missing the market expectation of RMB 289.79 billion, indicating a lack of growth momentum amid economic slowdown, which could undermine investor confidence going forward.

- Weak Domestic E-commerce Performance: Revenue from China e-commerce rose 16% to RMB 159.35 billion, yet fell short of Bloomberg's estimate of RMB 165.94 billion, reflecting intensified competition and weak consumer spending challenges in the domestic market.

- Cloud Intelligence Revenue Slightly Up: Cloud intelligence revenue increased by 36% to RMB 43.28 billion, just above the expected RMB 42.36 billion, but analysts noted that Alibaba's cloud performance remains insufficient compared to Microsoft's Azure's 39% growth, potentially impacting its long-term strategy.

- Sharp Net Profit Drop: Net income attributable to ordinary shareholders plummeted 67% to RMB 16.32 billion, with earnings per share at RMB 5.93, significantly lower than last year's RMB 48.95 billion and RMB 20.39 per share, highlighting the pressure from increased marketing expenses in the quick commerce sector.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BABA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BABA

Wall Street analysts forecast BABA stock price to rise

15 Analyst Rating

15 Buy

0 Hold

0 Sell

Strong Buy

Current: 145.810

Low

180.00

Averages

203.09

High

230.00

Current: 145.810

Low

180.00

Averages

203.09

High

230.00

About BABA

Alibaba Group Holding Ltd is an investment holding company mainly engaged in the provision of technology infrastructure and marketing platforms. The Company operates its business through four segments. The Alibaba China E-commerce Group segment is mainly engaged in E-commerce business, including operating Tmall Supermarket and Tmall Global, providing customer management services, product sales, as well as logistics services. It also operates quick commerce business such as Taobao Instant Commerce and Ele.me, as well as the China commerce wholesale business through 1688.com. The Alibaba International Digital Commerce Group segment is mainly engaged in international commerce retail and wholesale business, operating platforms such as AliExpress, Trendyol, Lazada and Alibaba.com. The Cloud Intelligence Group segment mainly provides public and non-public cloud services. The Other segments primarily include the operations of Freshippo, Cainiao, Alibaba Health and other business.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Alibaba Options Pricing Indicates Earnings Volatility Ahead

- Options Market Expectations: Alibaba's (BABA) May 15 options pricing indicates a roughly 6.5% expected volatility post-earnings, reflecting cautious sentiment among investors ahead of the earnings report.

- Key Price Range: The options chain highlights the 135 to 137 dollar range as a critical battleground post-report, with the stock trading near 136 dollars, indicating heightened market focus on short-term price movements.

- Bullish Call Concentration: The 145 dollar call option shows the largest open interest at 30,254 contracts, suggesting strong investor expectations for the stock to rise into the 145 to 150 dollar range.

- Protective Put Positioning: Significant open interest in the 130 and 120 dollar puts, with 9,718 and 12,106 contracts respectively, indicates investor concerns about the earnings report, highlighting a focus on potential downside risks.

See More

Alibaba Declares $1.05 Annual Dividend with 0.72% Yield

- Dividend Announcement: Alibaba has declared an annual dividend of $1.05 per share, payable on July 13, which demonstrates the company's commitment to returning value to shareholders amidst the current economic landscape.

- Yield Metrics: The forward yield of 0.72% is relatively modest, yet it reflects Alibaba's ongoing efforts to maintain profitability and shareholder value creation in a competitive market.

- Record Date: The record date for shareholders is set for June 11, with the ex-dividend date also on June 11, providing investors with a clear timeline for their investment decisions.

- Market Implications: The dividend announcement may attract income-seeking investors, enhancing Alibaba's market appeal, particularly in light of increasing economic uncertainties that could drive demand for stable returns.

See More

US Equity Futures Rise as Tech Stocks Hit Record Highs

- Strong Tech Performance: US equity futures rose pre-bell on Thursday, primarily driven by technology stocks, indicating strong market confidence in the tech sector, which may attract further investor interest.

- Optimistic Market Sentiment: The new highs in tech stocks have led to a generally optimistic investor sentiment, which could stimulate more capital inflows into the stock market, thereby driving overall market gains.

- Economic Recovery Signals: The robust performance of tech stocks is viewed as a positive signal for economic recovery, suggesting that consumer and business confidence in future growth is strengthening, potentially benefiting other sectors as well.

- Investor Focus: As tech stocks continue to rise, investors may pay closer attention to earnings reports and market developments related to these companies to capitalize on potential investment opportunities.

See More

Xi Jinping Welcomes Deeper Cooperation with U.S. Companies

- Market Access Commitment: Xi Jinping stated during a meeting with Trump and American CEOs that China will further open its market, emphasizing the mutual benefits of U.S. companies' involvement in China's reform, which is expected to attract more American investors to the Chinese market.

- Executives at the Banquet: Tesla and SpaceX CEO Elon Musk, Nvidia CEO Jensen Huang, and Apple CEO Tim Cook were among the tech leaders accompanying Trump to China, indicating the importance of the Chinese market to U.S. companies and their willingness to deepen cooperation.

- AI Technology Competition: Both China and the U.S. are rapidly advancing in artificial intelligence; despite U.S. attempts to restrict technology exports to China, local semiconductor firms in China are stepping in to fill the gap, demonstrating China's commitment to technological self-sufficiency.

- Prospects for Cooperation: The White House noted that both sides discussed ways to enhance economic cooperation, including expanding market access for American businesses in China, which is expected to facilitate investment flows between the two countries and further promote mutually beneficial economic development.

See More

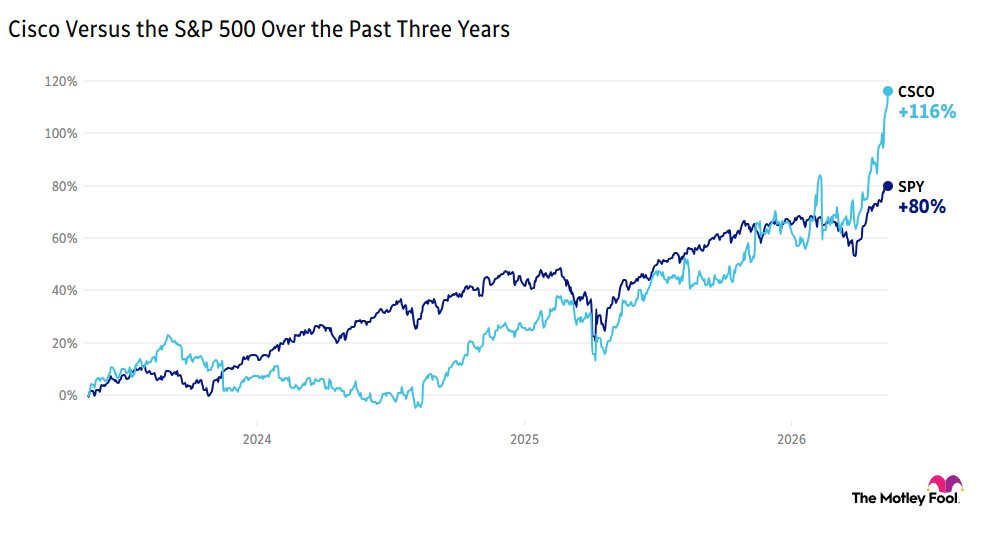

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

China Accelerates Chip Production Amid AI Growth

- Chip Production Boost: Tencent's Chief Strategy Officer indicated a substantial increase in the availability of China-designed chips in the second half of the year, which is expected to drive record revenues for domestic chip companies and enhance China's competitiveness in the global semiconductor market.

- Self-Developed Chip Advantage: Alibaba's T-Head GPU chips have achieved mass production, with executives highlighting that in a semiconductor-scarce environment, these self-designed chips will favorably impact revenue growth and gross margins.

- Shifting Market Demand: As Chinese firms pivot towards 'agentic AI', the demand for more advanced chips is rising, with analysts suggesting that Nvidia's H200 chips will be welcomed, potentially playing a key role in a hybrid AI inferencing infrastructure combining Chinese and U.S. chips.

- Policy Dynamics Impact: Despite reports of U.S. approval for Alibaba and Tencent to purchase Nvidia's H200 chips, no deliveries have occurred yet, reflecting the complexities of U.S.-China tech competition and its potential implications for China's semiconductor industry.

See More

Alibaba Options Pricing Indicates Earnings Volatility Ahead

- Options Market Expectations: Alibaba's (BABA) May 15 options pricing indicates a roughly 6.5% expected volatility post-earnings, reflecting cautious sentiment among investors ahead of the earnings report.

- Key Price Range: The options chain highlights the 135 to 137 dollar range as a critical battleground post-report, with the stock trading near 136 dollars, indicating heightened market focus on short-term price movements.

- Bullish Call Concentration: The 145 dollar call option shows the largest open interest at 30,254 contracts, suggesting strong investor expectations for the stock to rise into the 145 to 150 dollar range.

- Protective Put Positioning: Significant open interest in the 130 and 120 dollar puts, with 9,718 and 12,106 contracts respectively, indicates investor concerns about the earnings report, highlighting a focus on potential downside risks.

See More

Alibaba Declares $1.05 Annual Dividend with 0.72% Yield

- Dividend Announcement: Alibaba has declared an annual dividend of $1.05 per share, payable on July 13, which demonstrates the company's commitment to returning value to shareholders amidst the current economic landscape.

- Yield Metrics: The forward yield of 0.72% is relatively modest, yet it reflects Alibaba's ongoing efforts to maintain profitability and shareholder value creation in a competitive market.

- Record Date: The record date for shareholders is set for June 11, with the ex-dividend date also on June 11, providing investors with a clear timeline for their investment decisions.

- Market Implications: The dividend announcement may attract income-seeking investors, enhancing Alibaba's market appeal, particularly in light of increasing economic uncertainties that could drive demand for stable returns.

See More

US Equity Futures Rise as Tech Stocks Hit Record Highs

- Strong Tech Performance: US equity futures rose pre-bell on Thursday, primarily driven by technology stocks, indicating strong market confidence in the tech sector, which may attract further investor interest.

- Optimistic Market Sentiment: The new highs in tech stocks have led to a generally optimistic investor sentiment, which could stimulate more capital inflows into the stock market, thereby driving overall market gains.

- Economic Recovery Signals: The robust performance of tech stocks is viewed as a positive signal for economic recovery, suggesting that consumer and business confidence in future growth is strengthening, potentially benefiting other sectors as well.

- Investor Focus: As tech stocks continue to rise, investors may pay closer attention to earnings reports and market developments related to these companies to capitalize on potential investment opportunities.

See More

Xi Jinping Welcomes Deeper Cooperation with U.S. Companies

- Market Access Commitment: Xi Jinping stated during a meeting with Trump and American CEOs that China will further open its market, emphasizing the mutual benefits of U.S. companies' involvement in China's reform, which is expected to attract more American investors to the Chinese market.

- Executives at the Banquet: Tesla and SpaceX CEO Elon Musk, Nvidia CEO Jensen Huang, and Apple CEO Tim Cook were among the tech leaders accompanying Trump to China, indicating the importance of the Chinese market to U.S. companies and their willingness to deepen cooperation.

- AI Technology Competition: Both China and the U.S. are rapidly advancing in artificial intelligence; despite U.S. attempts to restrict technology exports to China, local semiconductor firms in China are stepping in to fill the gap, demonstrating China's commitment to technological self-sufficiency.

- Prospects for Cooperation: The White House noted that both sides discussed ways to enhance economic cooperation, including expanding market access for American businesses in China, which is expected to facilitate investment flows between the two countries and further promote mutually beneficial economic development.

See More

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

China Accelerates Chip Production Amid AI Growth

- Chip Production Boost: Tencent's Chief Strategy Officer indicated a substantial increase in the availability of China-designed chips in the second half of the year, which is expected to drive record revenues for domestic chip companies and enhance China's competitiveness in the global semiconductor market.

- Self-Developed Chip Advantage: Alibaba's T-Head GPU chips have achieved mass production, with executives highlighting that in a semiconductor-scarce environment, these self-designed chips will favorably impact revenue growth and gross margins.

- Shifting Market Demand: As Chinese firms pivot towards 'agentic AI', the demand for more advanced chips is rising, with analysts suggesting that Nvidia's H200 chips will be welcomed, potentially playing a key role in a hybrid AI inferencing infrastructure combining Chinese and U.S. chips.

- Policy Dynamics Impact: Despite reports of U.S. approval for Alibaba and Tencent to purchase Nvidia's H200 chips, no deliveries have occurred yet, reflecting the complexities of U.S.-China tech competition and its potential implications for China's semiconductor industry.

See More