Klarna Reports Q1 Revenue Exceeding Expectations

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 32 minutes ago

0mins

Should l Buy KLAR?

Source: stocktwits

- Strong Revenue Performance: Klarna reported first-quarter revenue of $1 billion, surpassing Wall Street's expectation of $944.09 million, indicating robust market performance and growth potential.

- Significant User Growth: The number of active consumers reached 119 million, a 21% year-over-year increase, which not only enhances the company's market share but also strengthens the sustainability of future revenues.

- Substantial GMV Increase: The Gross Merchandise Value (GMV) for the quarter was $33.7 billion, reflecting a 33% year-over-year growth, demonstrating strong consumer demand and trust in Klarna's services.

- Shift in Market Sentiment: Retail investor sentiment towards Klarna's stock has shifted from neutral to 'extremely bullish', indicating increased confidence in its future performance, despite the stock having declined over 52% this year.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy KLAR?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on KLAR

Wall Street analysts forecast KLAR stock price to rise

11 Analyst Rating

9 Buy

2 Hold

0 Sell

Strong Buy

Current: 13.690

Low

36.00

Averages

44.36

High

55.00

Current: 13.690

Low

36.00

Averages

44.36

High

55.00

About KLAR

Klarna Group Plc is a United Kingdom-based technology company focused on developing commerce networks. The Company is an artificial intelligence (AI)-powered global payments network and shopping assistant. It provides consumers and merchants with a range of solutions, including payment, advertising and digital retail banking, through several channels. Its online payments solution is designed to bridge uncertainty in the transactions between consumers and merchants by providing short-term credit to consumers interest-free. Its range of payment options allows consumers to purchase what they choose, both online and offline. Its payment solutions include Pay in Full, Pay Later and Fair Financing. Its Pay in Full instantly settles purchases at the time of the transaction. Its Pay Later enables consumers to purchase goods or services at the time of the transaction and pay the full amount at a later date. Its Fair Financing allows consumers to pay for their purchase over a longer duration.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Klarna to Announce Q1 Earnings on May 14

- Earnings Announcement: Klarna is set to release its Q1 earnings on May 14 before market open, with consensus estimates predicting an EPS of -$0.13 and revenue of $943.87 million, indicating ongoing challenges in achieving profitability.

- Profitability Test: Analysts emphasize that Klarna's Q1 results will serve as a critical test of its profitability narrative, prompting investors to closely monitor its ability to achieve profitability in a competitive fintech landscape.

- Google Integration: Klarna and Affirm are to be integrated into Google Search and the Gemini app within Google Pay, a strategic partnership that could enhance user experience and expand market reach, potentially driving business growth.

- Flexible Payment Options: Klarna's partnership with Aven Hospitality introduces flexible payment options for hotel bookings, a move that not only enhances its product offerings but may also attract more consumers to its services.

See More

Klarna Reports Q1 Revenue Exceeding Expectations

- Strong Revenue Performance: Klarna reported first-quarter revenue of $1 billion, surpassing Wall Street's expectation of $944.09 million, indicating robust market performance and growth potential.

- Significant User Growth: The number of active consumers reached 119 million, a 21% year-over-year increase, which not only enhances the company's market share but also strengthens the sustainability of future revenues.

- Substantial GMV Increase: The Gross Merchandise Value (GMV) for the quarter was $33.7 billion, reflecting a 33% year-over-year growth, demonstrating strong consumer demand and trust in Klarna's services.

- Shift in Market Sentiment: Retail investor sentiment towards Klarna's stock has shifted from neutral to 'extremely bullish', indicating increased confidence in its future performance, despite the stock having declined over 52% this year.

See More

Klarna Stock Rises 5.6% After Strong Q1 Earnings Beat Expectations

- Earnings Beat: Klarna reported an adjusted operating profit of $68 million for Q1, significantly surpassing the Visible Alpha estimate of $12 million and up from $47 million in the previous quarter, indicating strong performance in the flexible financing sector.

- Decline in Credit Loss Provisions: The provision for credit losses fell to $166 million, below the Visible Alpha estimate of $220 million and down from $250 million in the prior quarter, reflecting improved risk management capabilities within the company.

- Cautious Q2 Outlook: Klarna expects Q2 revenue between $960 million and $1 billion, lower than the consensus estimate of $1.06 billion, with adjusted operating profit projected at $30 million to $60 million, indicating short-term growth pressures.

- Full-Year Guidance Reaffirmed: Klarna reiterated its guidance for GMV exceeding $155 billion for 2026, despite the Visible Alpha estimate of $156.1 billion, demonstrating the company's confidence in long-term growth prospects.

See More

Klarna Q1 Results Exceed Expectations Amid U.S. Growth

- Significant Revenue Growth: Klarna's Q1 revenue surged 44% to $1 billion, surpassing analyst expectations of $945 million, showcasing strong performance in the U.S. market, although the forecast for future revenue falls short of market expectations, potentially impacting investor confidence.

- Return to Operating Profit: The company reported an operating income of $17 million for the quarter, a substantial improvement from a loss of $90 million in the same period last year, exceeding analyst expectations of $9 million, indicating significant progress in profitability.

- Adjusted Profit Surge: Adjusted operating profit skyrocketed from $3 million last year to $68 million, reflecting Klarna's success in cost control and efficiency improvements, despite a previous market value decline due to an excessive focus on growth in Q4.

- GMV Growth Slows: Klarna's gross merchandise volume (GMV) rose 33% to $33.7 billion, but the Q2 GMV forecast of $35.5 billion to $36.5 billion falls below analyst expectations of $38.1 billion, potentially exerting pressure on future performance.

See More

Klarnapress Reports Q1 2025 Financial Results with Significant Growth

- Net Income Reversal: Klarnapress reported a net income of $1 million in Q1 2025, a significant turnaround from a net loss of $99 million in Q1 2025, indicating a substantial improvement in financial health and reflecting the effectiveness of its business model amid recovering market demand.

- Strong Revenue Growth: The company achieved revenue of $1.01 billion in the first quarter, representing a 44.1% year-over-year increase and surpassing market expectations by $66.13 million, demonstrating Klarnapress's significant sales growth and enhanced market share in a competitive landscape.

- GMV Increase: The gross merchandise volume (GMV) reached $33.7 billion, up 33% year-over-year, with the U.S. market growing by 39% and international markets by 31%, showcasing Klarnapress's robust performance and expansion of its customer base globally.

- Active Consumer Growth: The number of active consumers rose to 119 million, a 21% increase year-over-year, while the number of merchants exceeded 1 million, growing by 49%, indicating Klarnapress's success in attracting new users and merchants, further solidifying its market position.

See More

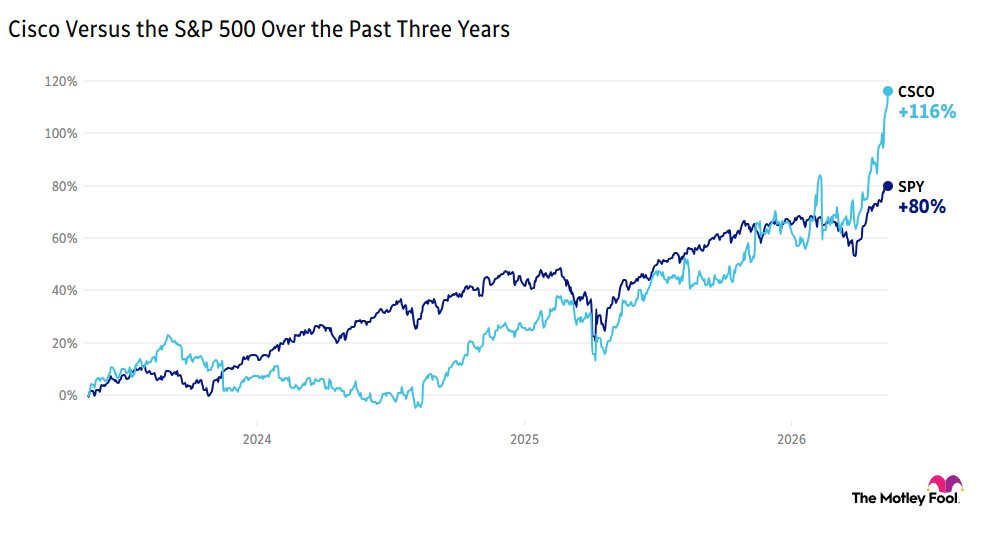

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

Klarna to Announce Q1 Earnings on May 14

- Earnings Announcement: Klarna is set to release its Q1 earnings on May 14 before market open, with consensus estimates predicting an EPS of -$0.13 and revenue of $943.87 million, indicating ongoing challenges in achieving profitability.

- Profitability Test: Analysts emphasize that Klarna's Q1 results will serve as a critical test of its profitability narrative, prompting investors to closely monitor its ability to achieve profitability in a competitive fintech landscape.

- Google Integration: Klarna and Affirm are to be integrated into Google Search and the Gemini app within Google Pay, a strategic partnership that could enhance user experience and expand market reach, potentially driving business growth.

- Flexible Payment Options: Klarna's partnership with Aven Hospitality introduces flexible payment options for hotel bookings, a move that not only enhances its product offerings but may also attract more consumers to its services.

See More

Klarna Reports Q1 Revenue Exceeding Expectations

- Strong Revenue Performance: Klarna reported first-quarter revenue of $1 billion, surpassing Wall Street's expectation of $944.09 million, indicating robust market performance and growth potential.

- Significant User Growth: The number of active consumers reached 119 million, a 21% year-over-year increase, which not only enhances the company's market share but also strengthens the sustainability of future revenues.

- Substantial GMV Increase: The Gross Merchandise Value (GMV) for the quarter was $33.7 billion, reflecting a 33% year-over-year growth, demonstrating strong consumer demand and trust in Klarna's services.

- Shift in Market Sentiment: Retail investor sentiment towards Klarna's stock has shifted from neutral to 'extremely bullish', indicating increased confidence in its future performance, despite the stock having declined over 52% this year.

See More

Klarna Stock Rises 5.6% After Strong Q1 Earnings Beat Expectations

- Earnings Beat: Klarna reported an adjusted operating profit of $68 million for Q1, significantly surpassing the Visible Alpha estimate of $12 million and up from $47 million in the previous quarter, indicating strong performance in the flexible financing sector.

- Decline in Credit Loss Provisions: The provision for credit losses fell to $166 million, below the Visible Alpha estimate of $220 million and down from $250 million in the prior quarter, reflecting improved risk management capabilities within the company.

- Cautious Q2 Outlook: Klarna expects Q2 revenue between $960 million and $1 billion, lower than the consensus estimate of $1.06 billion, with adjusted operating profit projected at $30 million to $60 million, indicating short-term growth pressures.

- Full-Year Guidance Reaffirmed: Klarna reiterated its guidance for GMV exceeding $155 billion for 2026, despite the Visible Alpha estimate of $156.1 billion, demonstrating the company's confidence in long-term growth prospects.

See More

Klarna Q1 Results Exceed Expectations Amid U.S. Growth

- Significant Revenue Growth: Klarna's Q1 revenue surged 44% to $1 billion, surpassing analyst expectations of $945 million, showcasing strong performance in the U.S. market, although the forecast for future revenue falls short of market expectations, potentially impacting investor confidence.

- Return to Operating Profit: The company reported an operating income of $17 million for the quarter, a substantial improvement from a loss of $90 million in the same period last year, exceeding analyst expectations of $9 million, indicating significant progress in profitability.

- Adjusted Profit Surge: Adjusted operating profit skyrocketed from $3 million last year to $68 million, reflecting Klarna's success in cost control and efficiency improvements, despite a previous market value decline due to an excessive focus on growth in Q4.

- GMV Growth Slows: Klarna's gross merchandise volume (GMV) rose 33% to $33.7 billion, but the Q2 GMV forecast of $35.5 billion to $36.5 billion falls below analyst expectations of $38.1 billion, potentially exerting pressure on future performance.

See More

Klarnapress Reports Q1 2025 Financial Results with Significant Growth

- Net Income Reversal: Klarnapress reported a net income of $1 million in Q1 2025, a significant turnaround from a net loss of $99 million in Q1 2025, indicating a substantial improvement in financial health and reflecting the effectiveness of its business model amid recovering market demand.

- Strong Revenue Growth: The company achieved revenue of $1.01 billion in the first quarter, representing a 44.1% year-over-year increase and surpassing market expectations by $66.13 million, demonstrating Klarnapress's significant sales growth and enhanced market share in a competitive landscape.

- GMV Increase: The gross merchandise volume (GMV) reached $33.7 billion, up 33% year-over-year, with the U.S. market growing by 39% and international markets by 31%, showcasing Klarnapress's robust performance and expansion of its customer base globally.

- Active Consumer Growth: The number of active consumers rose to 119 million, a 21% increase year-over-year, while the number of merchants exceeded 1 million, growing by 49%, indicating Klarnapress's success in attracting new users and merchants, further solidifying its market position.

See More

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More