Spotify Turns Up The Volume On Pricing, Premium Plans See A Hike

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jun 03 2024

0mins

Source: Benzinga

- Spotify Price Increase: Spotify raised prices for its premium plans in the U.S., with individual plan now at $11.99, duo plan at $16.99, and family plan at $19.99.

- Enhancing Profit Margins: The price hike is part of Spotify's efforts to boost profit margins, including reducing marketing expenses and layoffs.

- Competition and Innovation: Facing competition from Apple and Amazon, Spotify emphasizes the need to invest in and innovate its product offerings.

- Subscriber Growth: Spotify reported a 14% increase in premium subscribers to 239 million, with a forecast of 631 million monthly active users for the second quarter.

- Stock Performance: Spotify stock has gained over 99% in the last 12 months, currently trading higher by 4.83% at $311.12.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AMZN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AMZN

Wall Street analysts forecast AMZN stock price to rise

44 Analyst Rating

41 Buy

3 Hold

0 Sell

Strong Buy

Current: 244.390

Low

175.00

Averages

280.01

High

325.00

Current: 244.390

Low

175.00

Averages

280.01

High

325.00

About AMZN

Amazon.com, Inc. provides a range of products and services to customers. The products offered through its stores include merchandise and content it has purchased for resale and products offered by third-party sellers. The Company’s segments include North America, International and Amazon Web Services (AWS). It serves consumers through its online and physical stores and focuses on selection, price, and convenience. Customers access its offerings through its websites, mobile apps, Alexa, devices, streaming, and physically visiting its stores. It also manufactures and sells electronic devices, including Kindle, Fire tablet, Fire TV, Echo, Ring, Blink, and eero, and develops and produces media content. It serves developers and enterprises of all sizes, including start-ups, government agencies, and academic institutions, through AWS, which offers a set of on-demand technology services, including compute, storage, database, analytics, and machine learning, and other services.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Amazon's Data Center Investments Show Massive Potential

- Investment Return Potential: Amazon's investments in data centers are expected to yield massive returns, with AWS contributing 59% of profits despite the stock rising only about 7% in 2026, indicating strong profitability.

- Cloud Computing Growth: AWS's revenue growth of 28% in Q1 marks its best performance in nearly four years, significantly outpacing the 19% and 12% growth in international and North American commerce, highlighting the rapid expansion of its cloud business.

- AI Investment: Amazon is spending $200 billion on artificial intelligence, with CEO Andy Jassy noting that as computing power increases, customer demand rises, suggesting a multi-year growth cycle ahead.

- Valuation Attractiveness: Amazon's operating cash flow valuation is at a historical low, trading at 17 times compared to 32 times for Apple and 26 times for Alphabet, making it an attractive buying opportunity right now.

See More

Target Shareholder Support Hits Record Low Amid Leadership Criticism

- Declining Shareholder Support: At the recent annual meeting, Target's former CEO and current executive chairman Brian Cornell received only 87.2% support, a 4% drop from last year and significantly below the S&P 500 average of 96.6%, indicating growing investor dissatisfaction with leadership.

- Management Transition Backlash: After stepping down as CEO in February 2023, Cornell's transition to executive chair has been criticized, as despite achieving over 44% sales growth during his tenure, the company has faced declining profits and market share losses, resulting in a nearly 50% drop in stock price since its 2021 peak.

- Investor Opposition: Major public pension funds from Florida and New York voted against Cornell, citing “poor long-term performance,” highlighting significant investor discontent with Target's management, particularly regarding brand reputation and workforce management issues.

- Uncertain Future Outlook: Although Target reported a 5.6% increase in comparable sales in the first fiscal quarter, suggesting early signs of recovery, the CFO acknowledged that spending may decline due to reduced tax refunds, leaving investor confidence in management still fragile.

See More

Target Board Support Declines Significantly Amid Criticism

- Declining Shareholder Support: Brian Cornell, former CEO and current executive chairman of Target, received only 87.2% support during the annual meeting, a 4% drop from last year and significantly below his historical average of 95% and the S&P 500's 96.6%, indicating growing investor dissatisfaction with his leadership.

- Poor Performance: Under Cornell's tenure, Target has faced three consecutive years of declining sales and a 50% drop in share price, leading to diminished investor confidence in the company's strategic direction, particularly amid fierce competition from rivals.

- Pressure for Management Change: While Cornell was re-elected to the board, investor concerns about his continued chairmanship have intensified, with many viewing his retention as a “reward for failure” and calling for a complete overhaul of the management team overseeing the company's struggles.

- Increased Opposition from Investors: Major investors, including public pension funds from Florida and New York, have begun to vote against Cornell, citing poor management and its negative impact on brand and shareholder value, reflecting a strong pushback against Target's leadership.

See More

Market Dynamics and Corporate Mergers Overview

- Muted Market Start: The new trading week begins with the S&P 500 indicated flat while the tech-heavy Nasdaq shows slight gains, and WTI crude oil is trading around $76.50 per barrel, reflecting cautious market sentiment regarding economic outlook.

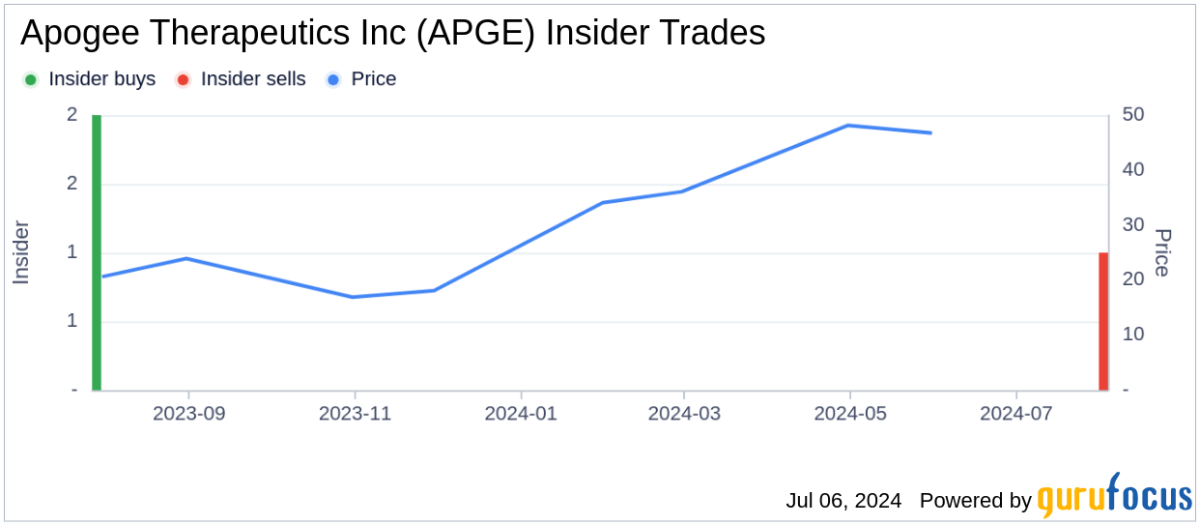

- Abbvie Acquires Apogee: Abbvie is acquiring Apogee Therapeutics for $10.9 billion to strengthen its immunology portfolio, particularly competing with Johnson & Johnson's Tremfya through its top drug Skyrizi, which is expected to enhance Abbvie's competitive edge in the biopharmaceutical market.

- CRH Acquires Arcosa: CRH is acquiring Arcosa for $8.5 billion, stating that the acquisition is highly complementary amid growing demand for energy and utility infrastructure, which is expected to further solidify CRH's position in the construction materials market.

- Estee Lauder Buy Rating Reinstated: Goldman Sachs has reinstated a buy rating for Estee Lauder with a price target of $100, as analysts believe the market is underestimating the company's growth momentum, especially after it walked away from merger talks with Spanish beauty peer Puig.

See More

SpaceX Announces Senior Unsecured Notes Offering Post-IPO

- Bond Offering Announcement: SpaceX has announced a senior unsecured notes offering aimed at raising approximately $20 billion to pay off bridge financing and other general purposes, indicating a pressing need for liquidity following its IPO.

- Cash Reserves: The company disclosed cash reserves of about $100.8 billion; however, shares fell about 5%, reflecting market concerns regarding its future financing strategies.

- Impact of IPO Success: Following its June 12 IPO, which raised nearly $86 billion and made Elon Musk the world's first trillionaire, SpaceX's stock surged, briefly pushing its market value past Amazon.

- Funding AI Initiatives: The bond offering is intended to support SpaceX's expansive AI plans, including the ambitious goal of building data centers in space, showcasing the company's commitment to technological innovation and competitive positioning.

See More

SpaceX Launches Inaugural Bond Sale Following IPO Success

- Inaugural Bond Offering: SpaceX has announced its inaugural senior unsecured notes offering, aiming to raise approximately $20 billion to pay off bridge financing and other general purposes, highlighting the urgency of funding needs post-IPO.

- IPO Success: The recent IPO raised nearly $86 billion, marking a milestone that made Elon Musk the world's first trillionaire, significantly enhancing the company's market valuation.

- Surging Market Value: Since its June 12 IPO, SpaceX's stock has surged, briefly pushing its market value past Amazon, reflecting strong investor confidence in its future growth potential.

- AI and Data Center Plans: SpaceX is advancing an ambitious artificial intelligence and data center buildout plan, which is expected to lay the groundwork for future space-based data centers, further solidifying its leadership position in the tech sector.

See More

Amazon's Data Center Investments Show Massive Potential

- Investment Return Potential: Amazon's investments in data centers are expected to yield massive returns, with AWS contributing 59% of profits despite the stock rising only about 7% in 2026, indicating strong profitability.

- Cloud Computing Growth: AWS's revenue growth of 28% in Q1 marks its best performance in nearly four years, significantly outpacing the 19% and 12% growth in international and North American commerce, highlighting the rapid expansion of its cloud business.

- AI Investment: Amazon is spending $200 billion on artificial intelligence, with CEO Andy Jassy noting that as computing power increases, customer demand rises, suggesting a multi-year growth cycle ahead.

- Valuation Attractiveness: Amazon's operating cash flow valuation is at a historical low, trading at 17 times compared to 32 times for Apple and 26 times for Alphabet, making it an attractive buying opportunity right now.

See More

Target Shareholder Support Hits Record Low Amid Leadership Criticism

- Declining Shareholder Support: At the recent annual meeting, Target's former CEO and current executive chairman Brian Cornell received only 87.2% support, a 4% drop from last year and significantly below the S&P 500 average of 96.6%, indicating growing investor dissatisfaction with leadership.

- Management Transition Backlash: After stepping down as CEO in February 2023, Cornell's transition to executive chair has been criticized, as despite achieving over 44% sales growth during his tenure, the company has faced declining profits and market share losses, resulting in a nearly 50% drop in stock price since its 2021 peak.

- Investor Opposition: Major public pension funds from Florida and New York voted against Cornell, citing “poor long-term performance,” highlighting significant investor discontent with Target's management, particularly regarding brand reputation and workforce management issues.

- Uncertain Future Outlook: Although Target reported a 5.6% increase in comparable sales in the first fiscal quarter, suggesting early signs of recovery, the CFO acknowledged that spending may decline due to reduced tax refunds, leaving investor confidence in management still fragile.

See More

Target Board Support Declines Significantly Amid Criticism

- Declining Shareholder Support: Brian Cornell, former CEO and current executive chairman of Target, received only 87.2% support during the annual meeting, a 4% drop from last year and significantly below his historical average of 95% and the S&P 500's 96.6%, indicating growing investor dissatisfaction with his leadership.

- Poor Performance: Under Cornell's tenure, Target has faced three consecutive years of declining sales and a 50% drop in share price, leading to diminished investor confidence in the company's strategic direction, particularly amid fierce competition from rivals.

- Pressure for Management Change: While Cornell was re-elected to the board, investor concerns about his continued chairmanship have intensified, with many viewing his retention as a “reward for failure” and calling for a complete overhaul of the management team overseeing the company's struggles.

- Increased Opposition from Investors: Major investors, including public pension funds from Florida and New York, have begun to vote against Cornell, citing poor management and its negative impact on brand and shareholder value, reflecting a strong pushback against Target's leadership.

See More

Market Dynamics and Corporate Mergers Overview

- Muted Market Start: The new trading week begins with the S&P 500 indicated flat while the tech-heavy Nasdaq shows slight gains, and WTI crude oil is trading around $76.50 per barrel, reflecting cautious market sentiment regarding economic outlook.

- Abbvie Acquires Apogee: Abbvie is acquiring Apogee Therapeutics for $10.9 billion to strengthen its immunology portfolio, particularly competing with Johnson & Johnson's Tremfya through its top drug Skyrizi, which is expected to enhance Abbvie's competitive edge in the biopharmaceutical market.

- CRH Acquires Arcosa: CRH is acquiring Arcosa for $8.5 billion, stating that the acquisition is highly complementary amid growing demand for energy and utility infrastructure, which is expected to further solidify CRH's position in the construction materials market.

- Estee Lauder Buy Rating Reinstated: Goldman Sachs has reinstated a buy rating for Estee Lauder with a price target of $100, as analysts believe the market is underestimating the company's growth momentum, especially after it walked away from merger talks with Spanish beauty peer Puig.

See More

SpaceX Announces Senior Unsecured Notes Offering Post-IPO

- Bond Offering Announcement: SpaceX has announced a senior unsecured notes offering aimed at raising approximately $20 billion to pay off bridge financing and other general purposes, indicating a pressing need for liquidity following its IPO.

- Cash Reserves: The company disclosed cash reserves of about $100.8 billion; however, shares fell about 5%, reflecting market concerns regarding its future financing strategies.

- Impact of IPO Success: Following its June 12 IPO, which raised nearly $86 billion and made Elon Musk the world's first trillionaire, SpaceX's stock surged, briefly pushing its market value past Amazon.

- Funding AI Initiatives: The bond offering is intended to support SpaceX's expansive AI plans, including the ambitious goal of building data centers in space, showcasing the company's commitment to technological innovation and competitive positioning.

See More

SpaceX Launches Inaugural Bond Sale Following IPO Success

- Inaugural Bond Offering: SpaceX has announced its inaugural senior unsecured notes offering, aiming to raise approximately $20 billion to pay off bridge financing and other general purposes, highlighting the urgency of funding needs post-IPO.

- IPO Success: The recent IPO raised nearly $86 billion, marking a milestone that made Elon Musk the world's first trillionaire, significantly enhancing the company's market valuation.

- Surging Market Value: Since its June 12 IPO, SpaceX's stock has surged, briefly pushing its market value past Amazon, reflecting strong investor confidence in its future growth potential.

- AI and Data Center Plans: SpaceX is advancing an ambitious artificial intelligence and data center buildout plan, which is expected to lay the groundwork for future space-based data centers, further solidifying its leadership position in the tech sector.

See More