U.S. Stocks Decline Amid Geopolitical Tensions

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Should l Buy OXY?

Source: Fool

- Oil Price Surge Impact: Geopolitical tensions have driven WTI crude oil prices up by 3% to around $105 per barrel, leading to increased market volatility and pressure on major U.S. stocks, prompting investors to consider the long-term economic implications of sustained high oil prices.

- Energy Stocks Rally: Amid rising oil prices, energy producers such as Occidental Petroleum, APA Corporation, and Diamondback Energy saw their stock prices increase, indicating strong market demand for energy and a recovery in investor confidence in the sector.

- Travel Sector Decline: Shares in travel firms, particularly Norwegian Cruise Line, plummeted due to missed Q1 expectations, reflecting market concerns about the recovery of the travel industry and potentially impacting future investment decisions.

- Cryptocurrency Market Rebound: Reports of lawmakers possibly reaching a compromise on key digital asset legislation have led to strong performances from crypto-linked firms like Coinbase Global, Circle Internet Group, and Robinhood Markets, with Bitcoin surpassing $80,000 for the first time, signaling renewed investor interest in crypto assets.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy OXY?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on OXY

Wall Street analysts forecast OXY stock price to fall

16 Analyst Rating

4 Buy

9 Hold

3 Sell

Hold

Current: 59.340

Low

38.00

Averages

47.27

High

64.00

Current: 59.340

Low

38.00

Averages

47.27

High

64.00

About OXY

Occidental Petroleum Corporation is an international energy company with assets primarily in the United States, the Middle East and North Africa. The Company is an oil and gas producer in the United States, including a producer in the Permian and DJ basins, and the offshore Gulf of Mexico. Its segments include oil and gas, and midstream and marketing. The oil and gas segment explores for, develops, and produces oil (which includes condensate), natural gas liquids (NGL) and natural gas. The Company's midstream and marketing segment purchases, markets, gathers, processes, transports, and stores oil (which includes condensate), NGL, natural gas, carbon dioxide (CO2) and power. The midstream and marketing segment provides flow assurance and maximizes the value of its oil and gas. It also optimizes its transportation and storage capacity and invests in entities that conduct similar activities. This segment also includes low-carbon venture businesses.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

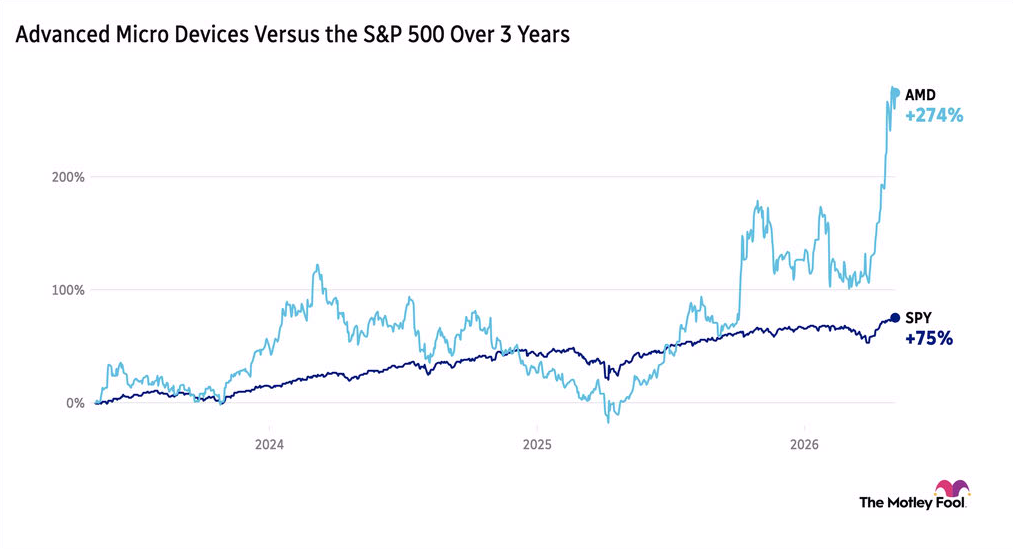

AMD Shares Surge 17% on Surge in Chip Demand

- Earnings Beat: AMD reported a 38% year-over-year revenue increase and a 43% rise in non-GAAP EPS for Q1 2026, exceeding market expectations and driving a 17% pre-market stock surge, highlighting the company's robust performance amid soaring AI infrastructure demand.

- Strategic Partnership: The collaboration with Meta is set to deploy 6 gigawatts of Instinct GPUs, which not only enhances AMD's competitive edge in the AI market but also lays a solid foundation for future revenue growth.

- Future Guidance: Management forecasts Q2 revenue to reach $11.2 billion, a 9% increase from Q1, translating to a 46% year-over-year growth, reflecting sustained growth potential and market confidence in AMD's AI initiatives.

- Market Reaction: Despite AMD's strong performance, Arista Networks saw a 9% drop in stock price due to cost pressures, indicating that supply chain challenges and rising costs in the semiconductor industry may affect overall market sentiment.

See More

California Gas Prices Surge Amidst Energy Dynamics

- High Gas Prices: California's gasoline tax stands at $0.70 per gallon, approximately 280% higher than Hawaii, making it the highest in the nation and directly impacting consumer travel costs and living expenses.

- Increased Import Dependency: Despite having over 1.5 billion barrels of proven oil reserves, California's reliance on imports has intensified due to refinery closures, with a recent tanker bringing over 530,000 barrels of fuel oil from Algeria, highlighting the state's energy supply vulnerabilities.

- Uncertain Market Outlook: Analysts warn that oil prices may remain elevated, with Evercore ISI noting that if prices stay between $93 and $98 in the coming months, it could pose risks to stock market recovery, urging investors to remain vigilant.

- Strong Company Performance: California Resources Corp (CRC), the only pure-play oil company in the state, has a favorable analyst target price averaging $80, implying about a 10% upside, reflecting market confidence in its future growth.

See More

Occidental Petroleum's Profit Soars on Asset Sale and Higher Oil Prices

- Profit Surge: Occidental Petroleum has reported a significant profit surge due to asset sales, with specific figures not disclosed; however, market expectations indicate a substantial improvement in financial performance, boosting investor confidence in the company's future growth.

- Impact of Rising Oil Prices: The rebound in global oil prices has benefited Occidental Petroleum through increased sales revenue, which not only enhances its profitability but also provides funding for future investments and expansions.

- Acquisition Strategy: The company's proactive approach to acquisitions, particularly in oil and gas assets, is expected to further strengthen its market competitiveness and lay the groundwork for long-term growth.

- Positive Market Reaction: Investors are optimistic about Occidental Petroleum's outlook, especially with Warren Buffett's backing, leading to expectations of continued stock price increases and attracting more capital inflows.

See More

Occidental Petroleum Reports Surge in Q1 Net Income

- Significant Net Income Growth: Occidental Petroleum's attributable net profit surged to $3.175 billion in Q1, a substantial increase from last year's $766 million, demonstrating strong financial performance following the sale of OxyChem.

- Earnings Per Share Increase: The company's EPS rose from $0.77 last year to $3.13, including a $3.12 billion gain from the OxyChem sale, reflecting successful asset disposal strategies.

- Strong Continuing Operations Performance: Adjusted profit from continuing operations was $1.070 billion, or $1.06 per share, up from $860 million and $0.87 per share last year, indicating robust growth in the company's core business.

- Production Volume Increase: Total production averaged 1,426 MBOE/D in Q1, surpassing last year's 1,391 MBOE/D, showcasing effective strategies in increasing output despite a slight decline in quarterly revenues.

See More

Occidental Petroleum Q1 Earnings Beat Expectations Despite Revenue Miss

- Earnings Beat: Occidental Petroleum reported adjusted earnings of $1.06 per share for Q1, surpassing the consensus estimate of $0.59, indicating enhanced profitability in a high oil price environment, despite revenue falling short of expectations.

- Revenue Miss: The company's Q1 revenue was approximately $5.23 billion, missing Wall Street's estimate of $5.67 billion, reflecting that despite rising oil prices, overall sales did not meet projections, which could impact future investor confidence.

- Production and Cash Flow: Occidental achieved an average production of 1.426 million barrels of oil equivalent per day, exceeding guidance, with operating cash flow of $1.4 billion, showcasing strong operational performance and cash generation capabilities that support future debt repayment plans.

- Debt Reduction Priority: Occidental repaid $7.1 billion in debt by early May, reducing total debt to $13.3 billion, with management emphasizing cost discipline and efficiency gains as central strategies to navigate commodity price cycles and geopolitical risks.

See More

Impact of Soaring Oil Prices on Oil Stocks

- Surging Oil Prices: Over the past three months, WTI crude oil prices have nearly doubled to around $100 per barrel, primarily due to the outbreak of the Iran War, which disrupted global oil deliveries through the Strait of Hormuz, creating challenges for companies reliant on low oil prices while benefiting oil stocks like Chevron and Occidental Petroleum.

- Occidental's Strong Performance: Since the onset of the Iran War, Occidental's stock has surged by 33%, compared to Chevron's 8% increase, largely due to Occidental's focus on upstream operations and its divestment of the downstream OxyChem business, which reduced debt and enhanced market appeal.

- Chevron's Stability: While Chevron's upstream business benefits from high oil prices, its downstream operations face challenges; however, its stock has risen 24% over the past three years, demonstrating resilience through diversification, with a consistent dividend increase for 39 years and a forward yield of 3.7%.

- Investor Sentiment: Although analysts expect Occidental's EPS to more than double by 2026, its lower P/E ratio of 14 compared to Chevron's 19 indicates investor caution regarding Occidental's growth potential, favoring the safer, well-diversified Chevron for long-term investment.

See More

AMD Shares Surge 17% on Surge in Chip Demand

- Earnings Beat: AMD reported a 38% year-over-year revenue increase and a 43% rise in non-GAAP EPS for Q1 2026, exceeding market expectations and driving a 17% pre-market stock surge, highlighting the company's robust performance amid soaring AI infrastructure demand.

- Strategic Partnership: The collaboration with Meta is set to deploy 6 gigawatts of Instinct GPUs, which not only enhances AMD's competitive edge in the AI market but also lays a solid foundation for future revenue growth.

- Future Guidance: Management forecasts Q2 revenue to reach $11.2 billion, a 9% increase from Q1, translating to a 46% year-over-year growth, reflecting sustained growth potential and market confidence in AMD's AI initiatives.

- Market Reaction: Despite AMD's strong performance, Arista Networks saw a 9% drop in stock price due to cost pressures, indicating that supply chain challenges and rising costs in the semiconductor industry may affect overall market sentiment.

See More

California Gas Prices Surge Amidst Energy Dynamics

- High Gas Prices: California's gasoline tax stands at $0.70 per gallon, approximately 280% higher than Hawaii, making it the highest in the nation and directly impacting consumer travel costs and living expenses.

- Increased Import Dependency: Despite having over 1.5 billion barrels of proven oil reserves, California's reliance on imports has intensified due to refinery closures, with a recent tanker bringing over 530,000 barrels of fuel oil from Algeria, highlighting the state's energy supply vulnerabilities.

- Uncertain Market Outlook: Analysts warn that oil prices may remain elevated, with Evercore ISI noting that if prices stay between $93 and $98 in the coming months, it could pose risks to stock market recovery, urging investors to remain vigilant.

- Strong Company Performance: California Resources Corp (CRC), the only pure-play oil company in the state, has a favorable analyst target price averaging $80, implying about a 10% upside, reflecting market confidence in its future growth.

See More

Occidental Petroleum's Profit Soars on Asset Sale and Higher Oil Prices

- Profit Surge: Occidental Petroleum has reported a significant profit surge due to asset sales, with specific figures not disclosed; however, market expectations indicate a substantial improvement in financial performance, boosting investor confidence in the company's future growth.

- Impact of Rising Oil Prices: The rebound in global oil prices has benefited Occidental Petroleum through increased sales revenue, which not only enhances its profitability but also provides funding for future investments and expansions.

- Acquisition Strategy: The company's proactive approach to acquisitions, particularly in oil and gas assets, is expected to further strengthen its market competitiveness and lay the groundwork for long-term growth.

- Positive Market Reaction: Investors are optimistic about Occidental Petroleum's outlook, especially with Warren Buffett's backing, leading to expectations of continued stock price increases and attracting more capital inflows.

See More

Occidental Petroleum Reports Surge in Q1 Net Income

- Significant Net Income Growth: Occidental Petroleum's attributable net profit surged to $3.175 billion in Q1, a substantial increase from last year's $766 million, demonstrating strong financial performance following the sale of OxyChem.

- Earnings Per Share Increase: The company's EPS rose from $0.77 last year to $3.13, including a $3.12 billion gain from the OxyChem sale, reflecting successful asset disposal strategies.

- Strong Continuing Operations Performance: Adjusted profit from continuing operations was $1.070 billion, or $1.06 per share, up from $860 million and $0.87 per share last year, indicating robust growth in the company's core business.

- Production Volume Increase: Total production averaged 1,426 MBOE/D in Q1, surpassing last year's 1,391 MBOE/D, showcasing effective strategies in increasing output despite a slight decline in quarterly revenues.

See More

Occidental Petroleum Q1 Earnings Beat Expectations Despite Revenue Miss

- Earnings Beat: Occidental Petroleum reported adjusted earnings of $1.06 per share for Q1, surpassing the consensus estimate of $0.59, indicating enhanced profitability in a high oil price environment, despite revenue falling short of expectations.

- Revenue Miss: The company's Q1 revenue was approximately $5.23 billion, missing Wall Street's estimate of $5.67 billion, reflecting that despite rising oil prices, overall sales did not meet projections, which could impact future investor confidence.

- Production and Cash Flow: Occidental achieved an average production of 1.426 million barrels of oil equivalent per day, exceeding guidance, with operating cash flow of $1.4 billion, showcasing strong operational performance and cash generation capabilities that support future debt repayment plans.

- Debt Reduction Priority: Occidental repaid $7.1 billion in debt by early May, reducing total debt to $13.3 billion, with management emphasizing cost discipline and efficiency gains as central strategies to navigate commodity price cycles and geopolitical risks.

See More

Impact of Soaring Oil Prices on Oil Stocks

- Surging Oil Prices: Over the past three months, WTI crude oil prices have nearly doubled to around $100 per barrel, primarily due to the outbreak of the Iran War, which disrupted global oil deliveries through the Strait of Hormuz, creating challenges for companies reliant on low oil prices while benefiting oil stocks like Chevron and Occidental Petroleum.

- Occidental's Strong Performance: Since the onset of the Iran War, Occidental's stock has surged by 33%, compared to Chevron's 8% increase, largely due to Occidental's focus on upstream operations and its divestment of the downstream OxyChem business, which reduced debt and enhanced market appeal.

- Chevron's Stability: While Chevron's upstream business benefits from high oil prices, its downstream operations face challenges; however, its stock has risen 24% over the past three years, demonstrating resilience through diversification, with a consistent dividend increase for 39 years and a forward yield of 3.7%.

- Investor Sentiment: Although analysts expect Occidental's EPS to more than double by 2026, its lower P/E ratio of 14 compared to Chevron's 19 indicates investor caution regarding Occidental's growth potential, favoring the safer, well-diversified Chevron for long-term investment.

See More