TSMC Reports Strong AI Demand Driving Financial Performance

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy TSM?

Source: Yahoo Finance

- Robust AI Demand: TSMC CEO C.C. Wei highlighted during the analyst call that AI-related demand remains extremely strong, driving the need for advanced silicon and indicating that the company will benefit from this trend in the coming years.

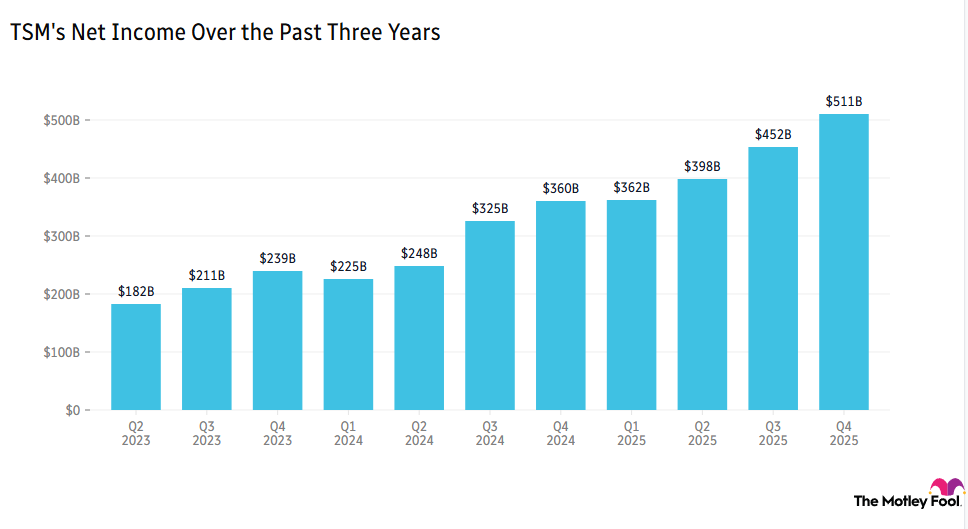

- Impressive Financial Performance: The company reported a record net profit of NT$572.5 billion (approximately $18.15 billion) for Q1, reflecting a 58.3% year-over-year increase, with revenue surging 35% to $35.9 billion, showcasing insatiable global demand for AI infrastructure.

- Significant Margin Expansion: Despite rising memory chip prices, TSMC's gross profit margin expanded to 66.2%, significantly exceeding company guidance, demonstrating strong pricing power and cost control in the market.

- Capital Expenditure Plans: Wei indicated that TSMC is leaning towards the high end of its $56 billion capital expenditure budget to support customers' AI infrastructure buildouts, further solidifying its market leadership.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TSM?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on TSM

Wall Street analysts forecast TSM stock price to fall

8 Analyst Rating

7 Buy

1 Hold

0 Sell

Strong Buy

Current: 379.890

Low

63.24

Averages

313.46

High

390.00

Current: 379.890

Low

63.24

Averages

313.46

High

390.00

About TSM

Taiwan Semiconductor Manufacturing Co Ltd is a Taiwan-based integrated circuit foundry service provider. The Company is primarily engaged in integrated circuit manufacturing services. It offers advanced process technologies, specialised process solutions, advanced photomask and silicon stacking, and packaging-related technologies, while supporting a comprehensive design ecosystem. The Company's products serve diverse electronic sectors including artificial intelligence, high-performance computing, wired and wireless communications, automotive and industrial equipment, personal computing, information applications, consumer electronics, smart internet of things, and wearable devices.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

TSMC Reports Strong Q1 Earnings Exceeding Expectations

- Earnings Beat: TSMC's Q1 GAAP EPS of $3.49 surpassed expectations by $0.11, indicating robust performance in the semiconductor market and likely boosting investor confidence moving forward.

- Significant Revenue Growth: The company reported Q1 revenue of $35.9 billion, a 40.6% year-over-year increase, exceeding market expectations by $410 million, reflecting strong global demand for high-performance computing and AI chips, driving sustained growth.

- Advanced Process Revenue Share: Shipments of 3nm, 5nm, and 7nm technologies accounted for 25%, 36%, and 13% of total wafer revenue, respectively, with advanced technologies (7nm and above) making up 74% of total revenue, showcasing TSMC's competitiveness in the high-end market.

- Optimistic Market Outlook: With ongoing demand for AI, TSMC is expected to continue reporting strong quarterly results, fostering a positive market sentiment that may attract more investor interest.

See More

TSMC Files 2025 Annual Report with SEC

- Annual Report Submission: TSMC today filed its 2025 annual report with the U.S. Securities and Exchange Commission, available on its website, reflecting the company's commitment to transparency and regulatory compliance.

- Technological Strength: By 2025, TSMC deployed 305 distinct process technologies and manufactured 12,682 products for 534 customers, showcasing its leadership and innovation capabilities in the semiconductor industry.

- Global Operations: TSMC's global operations across Asia, Europe, and North America support its role as the world's leading dedicated semiconductor foundry, fostering a thriving ecosystem for global customers and partners.

- Corporate Citizenship: As a global enterprise, TSMC is committed to fulfilling its corporate citizenship responsibilities, actively participating in social and environmental sustainability, thereby further solidifying its reputation in the industry.

See More

TSMC Profits Surge 58% Amid AI Chip Demand

- Profit Surge: TSMC reported a 58% year-over-year increase in net profit for the latest quarter, indicating strong demand for AI chips and minimal short-term impact from supply chain disruptions, with the stock slightly rising post-earnings release.

- Advanced Technology Revenue: Advanced technology products accounted for 74% of total wafer revenue, reflecting key customers like Apple’s preference for smaller nanometer products, which enhances the company's market share and competitive edge.

- Capacity Expansion: To meet the growing demand, TSMC plans to add production facilities in Taiwan, with capital expenditures expected to be at the high end of a $52 billion to $56 billion range, representing a 37% increase compared to last year.

- Optimistic Industry Outlook: As market demand for AI technologies continues to rise, TSMC's robust performance not only solidifies its leadership position in the semiconductor industry but also lays a foundation for future investments and technological innovations.

See More

TSMC Reports Strong AI Demand Driving Financial Performance

- Robust AI Demand: TSMC CEO C.C. Wei highlighted during the analyst call that AI-related demand remains extremely strong, driving the need for advanced silicon and indicating that the company will benefit from this trend in the coming years.

- Impressive Financial Performance: The company reported a record net profit of NT$572.5 billion (approximately $18.15 billion) for Q1, reflecting a 58.3% year-over-year increase, with revenue surging 35% to $35.9 billion, showcasing insatiable global demand for AI infrastructure.

- Significant Margin Expansion: Despite rising memory chip prices, TSMC's gross profit margin expanded to 66.2%, significantly exceeding company guidance, demonstrating strong pricing power and cost control in the market.

- Capital Expenditure Plans: Wei indicated that TSMC is leaning towards the high end of its $56 billion capital expenditure budget to support customers' AI infrastructure buildouts, further solidifying its market leadership.

See More

TSMC Raises 2026 Revenue Outlook Amid AI Chip Demand

- Significant Revenue Growth: TSMC's Q1 2026 net revenue surged 40.6% year-over-year to $35.9 billion (NT$1.134 trillion), driven by robust AI chip demand, further solidifying its leadership position in the global semiconductor market.

- Substantial Profit Increase: The company's net income attributable to shareholders soared 58.3% year-over-year to NT$572.48 billion, exceeding analysts' expectations of NT$542.4 billion, reflecting its strong profitability and pricing power in the market.

- Capital Expenditure Plans: TSMC anticipates capital expenditures for 2026 to be at the high end of its guidance, between $52 billion and $56 billion, with Q1 capital spending at $11.1 billion, indicating ongoing investments in technology innovation and capacity expansion to seize future growth opportunities.

- Optimistic Market Outlook: The company expects Q2 revenue to range between $39 billion and $40.2 billion, representing a 10% sequential increase, and forecasts full-year revenue growth of over 30% year-over-year, demonstrating strong confidence in future market demand.

See More

Jensen Huang Highlights Nvidia's Full-Stack AI Ecosystem Advantage

- Strong Market Demand: Despite Big Tech ramping up in-house chip development, demand for Nvidia's chips remains robust, driven by surging AI infrastructure spending, underscoring the company's dominant market position.

- Solid Competitive Moat: Jensen Huang emphasized that building something better than Nvidia is not easy, highlighting the company's role as a middle layer in a complex ecosystem, which makes it difficult for competitors to replicate its business model and further solidifies its market advantage.

- Optimistic Analyst Ratings: According to Koyfin, of the 60 analysts covering Nvidia, 57 have a 'Buy' rating, reflecting strong market confidence in Nvidia's future performance, which is mirrored in the stock price, rising 2% on Wednesday for the 11th consecutive trading day.

- Retail Sentiment Rebounds: Retail sentiment for Nvidia on Stocktwits improved from 'neutral' to 'bullish' this week, aligning with Wall Street's optimistic outlook, indicating investor confidence in Nvidia's future prospects.

See More

TSMC Reports Strong Q1 Earnings Exceeding Expectations

- Earnings Beat: TSMC's Q1 GAAP EPS of $3.49 surpassed expectations by $0.11, indicating robust performance in the semiconductor market and likely boosting investor confidence moving forward.

- Significant Revenue Growth: The company reported Q1 revenue of $35.9 billion, a 40.6% year-over-year increase, exceeding market expectations by $410 million, reflecting strong global demand for high-performance computing and AI chips, driving sustained growth.

- Advanced Process Revenue Share: Shipments of 3nm, 5nm, and 7nm technologies accounted for 25%, 36%, and 13% of total wafer revenue, respectively, with advanced technologies (7nm and above) making up 74% of total revenue, showcasing TSMC's competitiveness in the high-end market.

- Optimistic Market Outlook: With ongoing demand for AI, TSMC is expected to continue reporting strong quarterly results, fostering a positive market sentiment that may attract more investor interest.

See More

TSMC Files 2025 Annual Report with SEC

- Annual Report Submission: TSMC today filed its 2025 annual report with the U.S. Securities and Exchange Commission, available on its website, reflecting the company's commitment to transparency and regulatory compliance.

- Technological Strength: By 2025, TSMC deployed 305 distinct process technologies and manufactured 12,682 products for 534 customers, showcasing its leadership and innovation capabilities in the semiconductor industry.

- Global Operations: TSMC's global operations across Asia, Europe, and North America support its role as the world's leading dedicated semiconductor foundry, fostering a thriving ecosystem for global customers and partners.

- Corporate Citizenship: As a global enterprise, TSMC is committed to fulfilling its corporate citizenship responsibilities, actively participating in social and environmental sustainability, thereby further solidifying its reputation in the industry.

See More

TSMC Profits Surge 58% Amid AI Chip Demand

- Profit Surge: TSMC reported a 58% year-over-year increase in net profit for the latest quarter, indicating strong demand for AI chips and minimal short-term impact from supply chain disruptions, with the stock slightly rising post-earnings release.

- Advanced Technology Revenue: Advanced technology products accounted for 74% of total wafer revenue, reflecting key customers like Apple’s preference for smaller nanometer products, which enhances the company's market share and competitive edge.

- Capacity Expansion: To meet the growing demand, TSMC plans to add production facilities in Taiwan, with capital expenditures expected to be at the high end of a $52 billion to $56 billion range, representing a 37% increase compared to last year.

- Optimistic Industry Outlook: As market demand for AI technologies continues to rise, TSMC's robust performance not only solidifies its leadership position in the semiconductor industry but also lays a foundation for future investments and technological innovations.

See More

TSMC Reports Strong AI Demand Driving Financial Performance

- Robust AI Demand: TSMC CEO C.C. Wei highlighted during the analyst call that AI-related demand remains extremely strong, driving the need for advanced silicon and indicating that the company will benefit from this trend in the coming years.

- Impressive Financial Performance: The company reported a record net profit of NT$572.5 billion (approximately $18.15 billion) for Q1, reflecting a 58.3% year-over-year increase, with revenue surging 35% to $35.9 billion, showcasing insatiable global demand for AI infrastructure.

- Significant Margin Expansion: Despite rising memory chip prices, TSMC's gross profit margin expanded to 66.2%, significantly exceeding company guidance, demonstrating strong pricing power and cost control in the market.

- Capital Expenditure Plans: Wei indicated that TSMC is leaning towards the high end of its $56 billion capital expenditure budget to support customers' AI infrastructure buildouts, further solidifying its market leadership.

See More

TSMC Raises 2026 Revenue Outlook Amid AI Chip Demand

- Significant Revenue Growth: TSMC's Q1 2026 net revenue surged 40.6% year-over-year to $35.9 billion (NT$1.134 trillion), driven by robust AI chip demand, further solidifying its leadership position in the global semiconductor market.

- Substantial Profit Increase: The company's net income attributable to shareholders soared 58.3% year-over-year to NT$572.48 billion, exceeding analysts' expectations of NT$542.4 billion, reflecting its strong profitability and pricing power in the market.

- Capital Expenditure Plans: TSMC anticipates capital expenditures for 2026 to be at the high end of its guidance, between $52 billion and $56 billion, with Q1 capital spending at $11.1 billion, indicating ongoing investments in technology innovation and capacity expansion to seize future growth opportunities.

- Optimistic Market Outlook: The company expects Q2 revenue to range between $39 billion and $40.2 billion, representing a 10% sequential increase, and forecasts full-year revenue growth of over 30% year-over-year, demonstrating strong confidence in future market demand.

See More

Jensen Huang Highlights Nvidia's Full-Stack AI Ecosystem Advantage

- Strong Market Demand: Despite Big Tech ramping up in-house chip development, demand for Nvidia's chips remains robust, driven by surging AI infrastructure spending, underscoring the company's dominant market position.

- Solid Competitive Moat: Jensen Huang emphasized that building something better than Nvidia is not easy, highlighting the company's role as a middle layer in a complex ecosystem, which makes it difficult for competitors to replicate its business model and further solidifies its market advantage.

- Optimistic Analyst Ratings: According to Koyfin, of the 60 analysts covering Nvidia, 57 have a 'Buy' rating, reflecting strong market confidence in Nvidia's future performance, which is mirrored in the stock price, rising 2% on Wednesday for the 11th consecutive trading day.

- Retail Sentiment Rebounds: Retail sentiment for Nvidia on Stocktwits improved from 'neutral' to 'bullish' this week, aligning with Wall Street's optimistic outlook, indicating investor confidence in Nvidia's future prospects.

See More