Tesla Shares Decline Amid Oil Price Surge and Chip Supply Concerns

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 09 2026

0mins

Should l Buy TSLA?

Source: Benzinga

- Oil Price Pressure: As the U.S.-Israel-Iran conflict continues, crude oil prices surged past $100 a barrel on Monday, and while Tesla vehicles do not rely on gasoline, rising energy costs could strain household budgets and dampen demand for electric vehicles.

- Chip Supply Concerns Resurface: China's commerce ministry is considering export controls on semiconductors from Dutch chipmaker Nexperia, which could disrupt production schedules in the auto industry, particularly affecting power management chips and basic integrated circuits.

- Bearish Technical Indicators: Tesla's stock is currently trading below key moving averages, with the 20-day SMA down 5.3%, the 50-day SMA down 9.2%, and the 100-day SMA down 10.6%, indicating bearish market pressure and caution for investors.

- Stock Performance Review: Despite a 74.93% gain in Tesla's stock over the past 12 months, its current positioning at 61.2% within the 52-week range suggests significant growth but ongoing challenges in maintaining upward momentum.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TSLA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

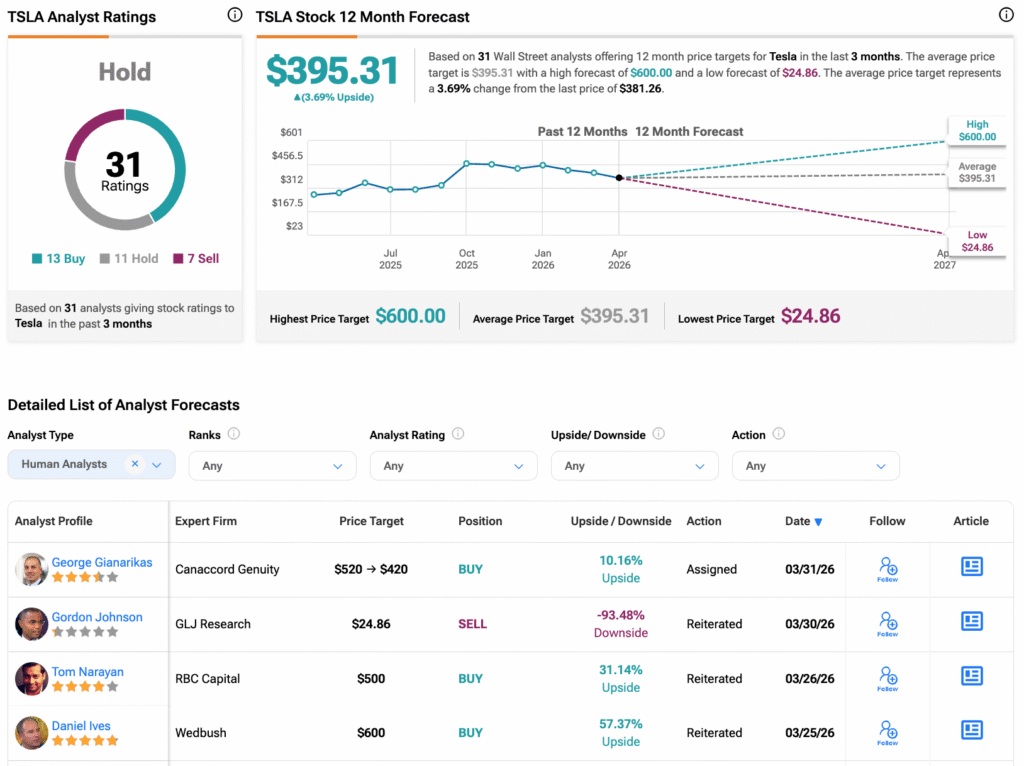

Analyst Views on TSLA

Wall Street analysts forecast TSLA stock price to rise

30 Analyst Rating

12 Buy

11 Hold

7 Sell

Hold

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

About TSLA

Tesla, Inc. designs, develops, manufactures, sells and leases high-performance fully electric vehicles and energy generation and storage systems, and offers services related to its products. Its segments include automotive, and energy generation and storage. The automotive segment includes the design, development, manufacturing, sales and leasing of high-performance fully electric vehicles, and sales of automotive regulatory credits. It also includes sales of used vehicles, non-warranty maintenance services and collisions, part sales, paid supercharging, insurance services revenue and retail merchandise sales. The energy generation and storage segment include the design, manufacture, installation, sales and leasing of solar energy generation and energy storage products and related services and sales of solar energy systems incentives. Its consumer vehicles include the Model 3, Y, S, X and Cybertruck. Its lithium-ion battery energy storage products include Powerwall and Megapack.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

Rivian Automotive Sales Decline for Fourth Consecutive Month Ahead of R2 Launch

- Sales Decline: Rivian's sales fell by over 26.5% year-over-year in Q1 2026, with only 8,141 vehicles sold compared to 11,070 last year, indicating a significant drop in market demand.

- Three-Year Low: In March 2026, Rivian's sales dropped to 2,925 units, nearly 1,000 fewer than the 3,910 units sold in March 2025, marking the lowest sales level in three years and highlighting increasing competition and market challenges.

- Upcoming R2 SUV: Rivian is set to launch the R2 Crossover SUV, which is expected to boost sales, with a delivery target of 62,000 to 67,000 vehicles in 2026, including 20,000 to 25,000 R2 units priced at $48,490.

- Partnership with Uber: Rivian signed a $1.25 billion deal with Uber to deploy several thousand R2 Robotaxis across multiple cities by 2031, demonstrating the company's strategic positioning in the autonomous driving sector to compete with Tesla's Full Self-Driving system.

See More

The Magnificent Seven Tech Stocks Face Challenges

- Market Performance Decline: The Magnificent Seven tech stocks, which have excelled in the market over the past few years, have recently faced declines or stagnation due to concerns about AI revenue opportunities and uncertainties in the economic and geopolitical landscape, impacting investor confidence.

- AI Chip Market Outlook: While Nvidia leads the AI chip market, Taiwan Semiconductor Manufacturing, as its chip manufacturer, is expected to play a significant role in future AI growth due to its diversified product line and broad market demand, thereby expanding its market opportunities.

- Broadcom's Growth Potential: Broadcom forecasts AI chip revenue exceeding $100 billion by 2027, successfully meeting strong customer demand with its custom chips, indicating robust growth potential in the AI sector.

- Nebius's Rapid Growth: Nebius Group excels in the AI cloud services space, achieving annual recurring revenue of $1.25 billion, with expectations to grow to $7 billion to $9 billion this year, showcasing its competitiveness and future growth potential in the rapidly expanding AI market.

See More

Oracle's Dubai Office Damaged Amid Rising Tensions in the Middle East

- Incident Overview: Oracle's office in Dubai was damaged by debris from an aerial interception, although no injuries were reported, highlighting the escalating tensions in the Middle East.

- Escalating Security Threats: Iran's Revolutionary Guard has designated 18 tech companies, including Oracle, as 'legitimate targets' in retaliation for U.S. and Israeli strikes, indicating the increasing significance of tech assets in conflicts.

- Industry Impact: James Henderson, CEO of risk management firm Healix, noted that the threats against tech companies are part of a sustained pattern, suggesting that future crises may target data centers and cloud platforms as much as traditional strategic sites.

- Historical Context: In March, Iran attacked Amazon Web Services data centers, causing outages in several apps and digital services in the UAE, underscoring the serious cybersecurity landscape in the region.

See More

Iran Threatens Attacks on U.S. Tech Firms Including Oracle

- Incident Overview: Oracle's building in Dubai sustained minor damage from debris due to an aerial interception, with no injuries reported; however, this incident highlights escalating tensions in the Middle East that could impact Oracle's operational safety in the region.

- Threats to Tech Companies: Iran's Revolutionary Guard has designated 18 U.S. tech firms, including Oracle, as 'legitimate targets' in retaliation for U.S. and Israeli strikes, which raises the operational risks for these companies in the Middle East.

- Rising Cybersecurity Risks: As threats against tech companies escalate, risk management expert James Henderson notes that tech assets are now viewed as integral to the conflict, suggesting future attacks may target data centers and cloud platforms, increasing security vulnerabilities in the industry.

- Historical Context: Iran previously attacked Amazon Web Services data centers in early March, causing outages in various apps and digital services in the UAE, and a repeat of such incidents could severely impact Oracle and other tech firms' operations.

See More

Emerging Tech Stars in the Market

- TSMC's AI Potential: Taiwan Semiconductor Manufacturing (TSM), a global leader in chip manufacturing, holds a market cap of $1.8 trillion and is poised to benefit from broad market demand in AI chip production, particularly in smartphones and personal computers over the coming years.

- Broadcom's Custom Chip Advantage: Broadcom (AVGO) forecasts over $100 billion in AI chip revenue by 2027, successfully carving out a niche in the AI market with its custom chips designed for specific tasks, reflecting strong customer demand and market potential.

- Nebius Group's Rapid Growth: Nebius Group (NBIS) focuses on AI workloads, achieving annual recurring revenue of $1.25 billion in the recent year, with expectations to rise to $7 billion to $9 billion this year, showcasing its strong growth potential in the cloud computing sector.

- Market Environment Challenges: Despite concerns about the economy and geopolitical factors affecting the Magnificent Seven tech stocks, emerging companies like TSMC, Broadcom, and Nebius Group demonstrate robust growth potential, positioning themselves as future market leaders.

See More

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

Rivian Automotive Sales Decline for Fourth Consecutive Month Ahead of R2 Launch

- Sales Decline: Rivian's sales fell by over 26.5% year-over-year in Q1 2026, with only 8,141 vehicles sold compared to 11,070 last year, indicating a significant drop in market demand.

- Three-Year Low: In March 2026, Rivian's sales dropped to 2,925 units, nearly 1,000 fewer than the 3,910 units sold in March 2025, marking the lowest sales level in three years and highlighting increasing competition and market challenges.

- Upcoming R2 SUV: Rivian is set to launch the R2 Crossover SUV, which is expected to boost sales, with a delivery target of 62,000 to 67,000 vehicles in 2026, including 20,000 to 25,000 R2 units priced at $48,490.

- Partnership with Uber: Rivian signed a $1.25 billion deal with Uber to deploy several thousand R2 Robotaxis across multiple cities by 2031, demonstrating the company's strategic positioning in the autonomous driving sector to compete with Tesla's Full Self-Driving system.

See More

The Magnificent Seven Tech Stocks Face Challenges

- Market Performance Decline: The Magnificent Seven tech stocks, which have excelled in the market over the past few years, have recently faced declines or stagnation due to concerns about AI revenue opportunities and uncertainties in the economic and geopolitical landscape, impacting investor confidence.

- AI Chip Market Outlook: While Nvidia leads the AI chip market, Taiwan Semiconductor Manufacturing, as its chip manufacturer, is expected to play a significant role in future AI growth due to its diversified product line and broad market demand, thereby expanding its market opportunities.

- Broadcom's Growth Potential: Broadcom forecasts AI chip revenue exceeding $100 billion by 2027, successfully meeting strong customer demand with its custom chips, indicating robust growth potential in the AI sector.

- Nebius's Rapid Growth: Nebius Group excels in the AI cloud services space, achieving annual recurring revenue of $1.25 billion, with expectations to grow to $7 billion to $9 billion this year, showcasing its competitiveness and future growth potential in the rapidly expanding AI market.

See More

Oracle's Dubai Office Damaged Amid Rising Tensions in the Middle East

- Incident Overview: Oracle's office in Dubai was damaged by debris from an aerial interception, although no injuries were reported, highlighting the escalating tensions in the Middle East.

- Escalating Security Threats: Iran's Revolutionary Guard has designated 18 tech companies, including Oracle, as 'legitimate targets' in retaliation for U.S. and Israeli strikes, indicating the increasing significance of tech assets in conflicts.

- Industry Impact: James Henderson, CEO of risk management firm Healix, noted that the threats against tech companies are part of a sustained pattern, suggesting that future crises may target data centers and cloud platforms as much as traditional strategic sites.

- Historical Context: In March, Iran attacked Amazon Web Services data centers, causing outages in several apps and digital services in the UAE, underscoring the serious cybersecurity landscape in the region.

See More

Iran Threatens Attacks on U.S. Tech Firms Including Oracle

- Incident Overview: Oracle's building in Dubai sustained minor damage from debris due to an aerial interception, with no injuries reported; however, this incident highlights escalating tensions in the Middle East that could impact Oracle's operational safety in the region.

- Threats to Tech Companies: Iran's Revolutionary Guard has designated 18 U.S. tech firms, including Oracle, as 'legitimate targets' in retaliation for U.S. and Israeli strikes, which raises the operational risks for these companies in the Middle East.

- Rising Cybersecurity Risks: As threats against tech companies escalate, risk management expert James Henderson notes that tech assets are now viewed as integral to the conflict, suggesting future attacks may target data centers and cloud platforms, increasing security vulnerabilities in the industry.

- Historical Context: Iran previously attacked Amazon Web Services data centers in early March, causing outages in various apps and digital services in the UAE, and a repeat of such incidents could severely impact Oracle and other tech firms' operations.

See More

Emerging Tech Stars in the Market

- TSMC's AI Potential: Taiwan Semiconductor Manufacturing (TSM), a global leader in chip manufacturing, holds a market cap of $1.8 trillion and is poised to benefit from broad market demand in AI chip production, particularly in smartphones and personal computers over the coming years.

- Broadcom's Custom Chip Advantage: Broadcom (AVGO) forecasts over $100 billion in AI chip revenue by 2027, successfully carving out a niche in the AI market with its custom chips designed for specific tasks, reflecting strong customer demand and market potential.

- Nebius Group's Rapid Growth: Nebius Group (NBIS) focuses on AI workloads, achieving annual recurring revenue of $1.25 billion in the recent year, with expectations to rise to $7 billion to $9 billion this year, showcasing its strong growth potential in the cloud computing sector.

- Market Environment Challenges: Despite concerns about the economy and geopolitical factors affecting the Magnificent Seven tech stocks, emerging companies like TSMC, Broadcom, and Nebius Group demonstrate robust growth potential, positioning themselves as future market leaders.

See More