SpaceX Plans Historic IPO Targeting $1.75 Trillion Valuation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Should l Buy META?

Source: Fool

- IPO Filing: Last month, SpaceX confidentially filed for an initial public offering (IPO) with the SEC, planning to kick off its roadshow on June 8 to pitch the stock to institutional investors and analysts, although a specific IPO date has not been set, trading is expected to commence in late June or early July.

- Valuation Target: The company is aiming for a staggering $1.75 trillion valuation, which would make it the largest IPO in U.S. history; however, historical trends indicate that IPO stocks often underperform in their first year, prompting investors to exercise caution.

- Historical Performance Insights: Data shows that since 1980, around 9,300 companies have gone public on the NYSE or Nasdaq, with IPO stocks gaining an average of 19% on their first trading day, yet those with large market values frequently experience sharp declines after initial excitement fades.

- Long-Term Investment Risks: While SpaceX may perform well in the long run, most large IPO stocks historically have underperformed the S&P 500 post-listing, suggesting that investors might be better off investing in an S&P 500 index fund rather than directly purchasing SpaceX shares.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy META?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on META

Wall Street analysts forecast META stock price to rise

44 Analyst Rating

37 Buy

6 Hold

1 Sell

Strong Buy

Current: 616.810

Low

655.15

Averages

824.71

High

1117

Current: 616.810

Low

655.15

Averages

824.71

High

1117

About META

Meta Platforms, Inc. is building human connections, powered by artificial intelligence and immersive technologies. The Company's products enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality (VR) and mixed reality (MR) headsets, augmented reality (AR), and wearables. It also helps people discover and learn about what is going on in the world around them, enabling people to share their experiences, ideas, photos, videos, and other content with audiences ranging from their closest family members and friends to the public at large. The Company's segments include Family of Apps (FoA) and Reality Labs (RL). FoA segment includes Facebook, Instagram, Messenger, WhatsApp and Threads. RL segment includes its virtual, augmented, and mixed reality related consumer hardware, software and content. Its product offerings in VR include its Meta Quest devices, as well as software and content available through the Meta Horizon Store.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Meta's Profits and Cash Flow Soar

- Profit Surge: Meta's profits saw a significant increase in Q1 2026, indicating strong performance in the digital advertising market, which is expected to further drive stock price growth.

- Strong Cash Flow: The company's cash flow continues to rise, demonstrating a notable improvement in operational efficiency and profitability, providing ample funding for future investments and expansions.

- Positive Market Reaction: On May 3, 2026, Meta's stock price rose during trading, reflecting increased investor confidence in the company's financial health.

- Optimistic Strategic Outlook: With the growth in profits and cash flow, Meta is poised to increase investments in new technologies and market expansion, thereby solidifying its leadership position in the tech industry.

See More

Linde's Strategic Positioning with SpaceX's IPO

- Market Opportunity: Linde's space business is rapidly growing, with expectations that SpaceX's IPO could double its commercial aerospace business to over $1 billion, highlighting its significance in emerging markets.

- Investment Expansion: Linde is investing $100 million in a new plant in Texas to enhance its gas supply capabilities for SpaceX, ensuring timely deliveries and strengthening its competitive position in the space industry.

- Historical Legacy: Founded in 1879, Linde has over 60 years of experience in the space sector, contributing to key missions from the Apollo program to Artemis II, showcasing its deep-rooted involvement in aerospace.

- Future Outlook: With SpaceX planning to significantly increase launch frequencies in the coming years, Linde anticipates benefiting from this trend, further solidifying its market position as an indispensable gas supplier in the space industry.

See More

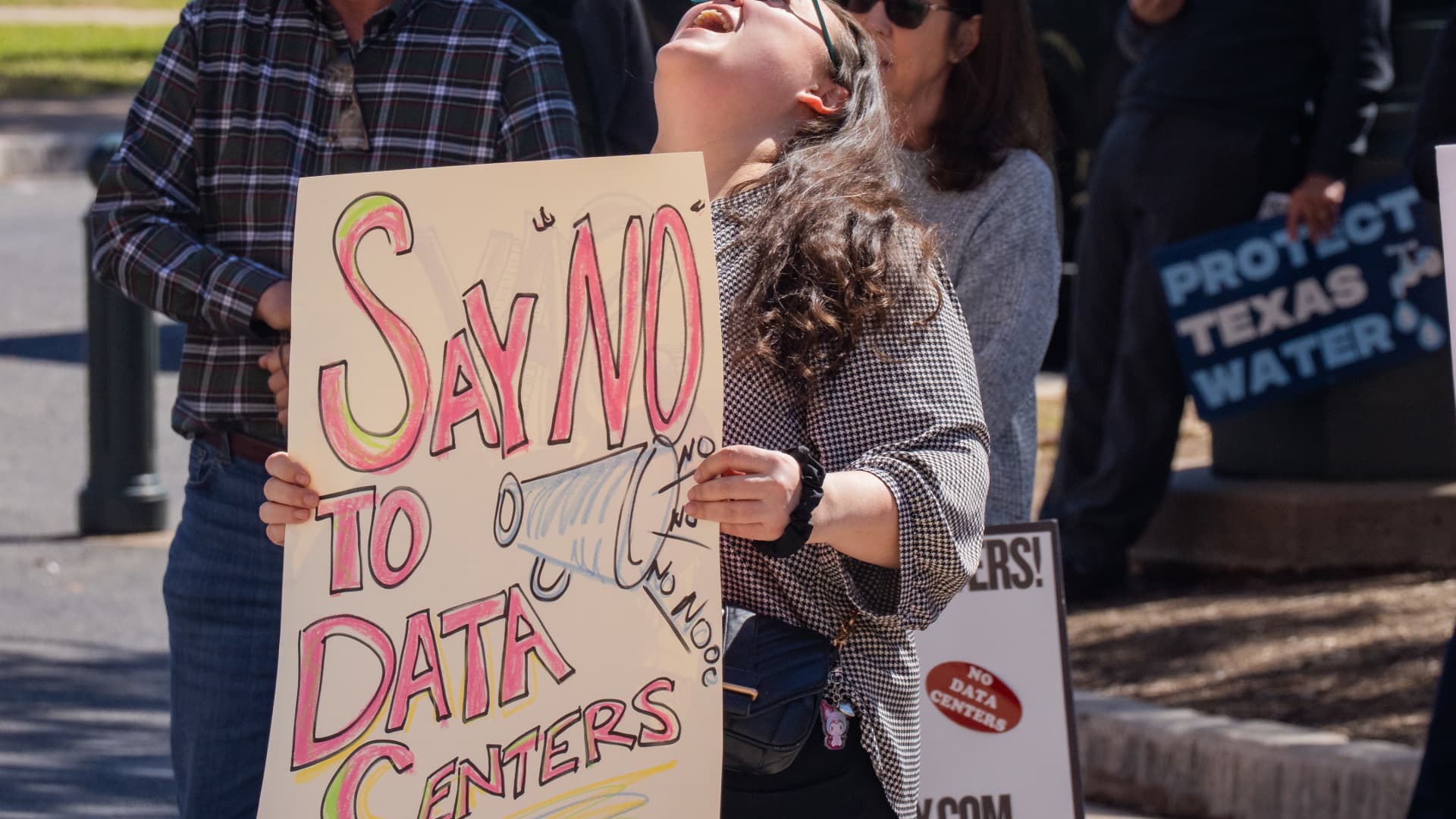

The Rise and Challenges of Home Data Centers

- Legislative Developments: Maine's legislature passed a data center ban, though it failed to override the governor's veto, indicating rising public discontent with data centers, as 14 states consider similar legislation reflecting concerns over big tech's influence.

- Massive Investment Trends: U.S. tech companies are projected to spend up to $1 trillion annually on AI by 2027, with global data center spending expected to reach $7 trillion by 2030, illustrating a significant influx of capital despite public opposition.

- Home Data Center Model: PulteGroup is collaborating with Nvidia and startup Span to test the installation of small data center nodes on new homes' exterior walls, although the scalability and regulatory approval of this model remain uncertain, its potential for energy efficiency and cost savings is noteworthy.

- Technical and Security Challenges: Home data centers face significant technical limitations regarding power density, connectivity, and security, as they may work for specific workloads, but high-density AI training and real-time tasks present major challenges, with experts highlighting concerns over reliability and security in residential settings.

See More

AI Stocks Rebound: Three Solid Investment Opportunities

- Microsoft's Strong Earnings: In Q3 of fiscal 2026, Microsoft's revenue rose 18% year-over-year to $82.9 billion, with net income increasing by 23%, showcasing robust performance in cloud computing, particularly with Azure's 40% revenue growth, instilling confidence in investors that the stock will rebound.

- Nvidia's Significant Upside: Although Nvidia's stock is only down 2% from its all-time high, it is expected to reach a forward P/E ratio in the mid-30s, indicating a potential 40% upside, especially as major client Alphabet plans to significantly increase capital expenditures in 2027, suggesting strong future demand.

- Meta's Impressive Growth: Meta's revenue surged 33% year-over-year in Q1, leveraging AI for effective ad placements despite its social media dominance, with a current P/E ratio of just over 19, below the S&P 500's 21.7, presenting a compelling investment opportunity.

- Long-Term Investment Outlook: All three companies are poised for strong returns through 2026, particularly as multi-year AI-related growth remains on the horizon, making them excellent long-term stock picks.

See More

Meta Leads AI Growth Among Tech Giants

- Revenue Growth Leader: Meta's quarterly revenue growth was the fastest among the big four, driven by the integration of AI technologies into its advertising business, which solidifies its competitive edge in the AI landscape.

- Cloud Computing Boost: Alphabet's Google Cloud saw a remarkable 63% revenue spike this quarter, primarily fueled by strong demand for cloud services and GPU sales, indicating a solid return on its AI computing investments.

- Cash Flow Valuation Advantage: Meta's cash flow from operations is impressive, trading at less than 13 times its cash flow, highlighting its relative affordability during heavy capital investment cycles, which attracts investor interest in its AI strategy.

- Investment Recommendation: Among the four tech giants, Meta is viewed as the top buy due to its rapid growth and undervalued stock, prompting investors to seize the opportunity before its AI investments yield significant returns.

See More

Investment Opportunities in Microsoft, Nvidia, and Meta

- Microsoft's Strong Earnings: In Q3 of fiscal 2026, Microsoft reported an 18% year-over-year revenue increase to $82.9 billion, with net income rising 23%, showcasing robust performance in cloud computing, particularly with Azure's 40% revenue growth, despite the stock being down 22% from its peak.

- Nvidia's Future Potential: Nvidia's stock is only down about 2%, but it is expected to reach a forward P/E ratio in the mid-30s for 2027, indicating a potential 40% upside, especially as its major client Alphabet plans to significantly increase capital expenditures, reflecting strong market demand.

- Meta's Underestimated Growth: Meta's revenue surged 33% year-over-year in Q1, and while AI integration in its social media platforms remains limited, the effectiveness of its ad placements has driven revenue growth, with a current P/E ratio of just 19, below the S&P 500's 21.7, indicating investment value.

- Long-Term Investment Outlook: All three companies are poised for strong returns over the coming years, particularly with multi-year AI-related growth on the horizon, making them attractive long-term investment options.

See More

Meta's Profits and Cash Flow Soar

- Profit Surge: Meta's profits saw a significant increase in Q1 2026, indicating strong performance in the digital advertising market, which is expected to further drive stock price growth.

- Strong Cash Flow: The company's cash flow continues to rise, demonstrating a notable improvement in operational efficiency and profitability, providing ample funding for future investments and expansions.

- Positive Market Reaction: On May 3, 2026, Meta's stock price rose during trading, reflecting increased investor confidence in the company's financial health.

- Optimistic Strategic Outlook: With the growth in profits and cash flow, Meta is poised to increase investments in new technologies and market expansion, thereby solidifying its leadership position in the tech industry.

See More

Linde's Strategic Positioning with SpaceX's IPO

- Market Opportunity: Linde's space business is rapidly growing, with expectations that SpaceX's IPO could double its commercial aerospace business to over $1 billion, highlighting its significance in emerging markets.

- Investment Expansion: Linde is investing $100 million in a new plant in Texas to enhance its gas supply capabilities for SpaceX, ensuring timely deliveries and strengthening its competitive position in the space industry.

- Historical Legacy: Founded in 1879, Linde has over 60 years of experience in the space sector, contributing to key missions from the Apollo program to Artemis II, showcasing its deep-rooted involvement in aerospace.

- Future Outlook: With SpaceX planning to significantly increase launch frequencies in the coming years, Linde anticipates benefiting from this trend, further solidifying its market position as an indispensable gas supplier in the space industry.

See More

The Rise and Challenges of Home Data Centers

- Legislative Developments: Maine's legislature passed a data center ban, though it failed to override the governor's veto, indicating rising public discontent with data centers, as 14 states consider similar legislation reflecting concerns over big tech's influence.

- Massive Investment Trends: U.S. tech companies are projected to spend up to $1 trillion annually on AI by 2027, with global data center spending expected to reach $7 trillion by 2030, illustrating a significant influx of capital despite public opposition.

- Home Data Center Model: PulteGroup is collaborating with Nvidia and startup Span to test the installation of small data center nodes on new homes' exterior walls, although the scalability and regulatory approval of this model remain uncertain, its potential for energy efficiency and cost savings is noteworthy.

- Technical and Security Challenges: Home data centers face significant technical limitations regarding power density, connectivity, and security, as they may work for specific workloads, but high-density AI training and real-time tasks present major challenges, with experts highlighting concerns over reliability and security in residential settings.

See More

AI Stocks Rebound: Three Solid Investment Opportunities

- Microsoft's Strong Earnings: In Q3 of fiscal 2026, Microsoft's revenue rose 18% year-over-year to $82.9 billion, with net income increasing by 23%, showcasing robust performance in cloud computing, particularly with Azure's 40% revenue growth, instilling confidence in investors that the stock will rebound.

- Nvidia's Significant Upside: Although Nvidia's stock is only down 2% from its all-time high, it is expected to reach a forward P/E ratio in the mid-30s, indicating a potential 40% upside, especially as major client Alphabet plans to significantly increase capital expenditures in 2027, suggesting strong future demand.

- Meta's Impressive Growth: Meta's revenue surged 33% year-over-year in Q1, leveraging AI for effective ad placements despite its social media dominance, with a current P/E ratio of just over 19, below the S&P 500's 21.7, presenting a compelling investment opportunity.

- Long-Term Investment Outlook: All three companies are poised for strong returns through 2026, particularly as multi-year AI-related growth remains on the horizon, making them excellent long-term stock picks.

See More

Meta Leads AI Growth Among Tech Giants

- Revenue Growth Leader: Meta's quarterly revenue growth was the fastest among the big four, driven by the integration of AI technologies into its advertising business, which solidifies its competitive edge in the AI landscape.

- Cloud Computing Boost: Alphabet's Google Cloud saw a remarkable 63% revenue spike this quarter, primarily fueled by strong demand for cloud services and GPU sales, indicating a solid return on its AI computing investments.

- Cash Flow Valuation Advantage: Meta's cash flow from operations is impressive, trading at less than 13 times its cash flow, highlighting its relative affordability during heavy capital investment cycles, which attracts investor interest in its AI strategy.

- Investment Recommendation: Among the four tech giants, Meta is viewed as the top buy due to its rapid growth and undervalued stock, prompting investors to seize the opportunity before its AI investments yield significant returns.

See More

Investment Opportunities in Microsoft, Nvidia, and Meta

- Microsoft's Strong Earnings: In Q3 of fiscal 2026, Microsoft reported an 18% year-over-year revenue increase to $82.9 billion, with net income rising 23%, showcasing robust performance in cloud computing, particularly with Azure's 40% revenue growth, despite the stock being down 22% from its peak.

- Nvidia's Future Potential: Nvidia's stock is only down about 2%, but it is expected to reach a forward P/E ratio in the mid-30s for 2027, indicating a potential 40% upside, especially as its major client Alphabet plans to significantly increase capital expenditures, reflecting strong market demand.

- Meta's Underestimated Growth: Meta's revenue surged 33% year-over-year in Q1, and while AI integration in its social media platforms remains limited, the effectiveness of its ad placements has driven revenue growth, with a current P/E ratio of just 19, below the S&P 500's 21.7, indicating investment value.

- Long-Term Investment Outlook: All three companies are poised for strong returns over the coming years, particularly with multi-year AI-related growth on the horizon, making them attractive long-term investment options.

See More