Rivian's 2025 Deliveries Decline; R2 Models May Provide Turnaround

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 17 2026

0mins

Should l Buy RIVN?

Source: NASDAQ.COM

- Declining Deliveries: Rivian delivered 13,201 vehicles in 2025, fewer than in 2024 or 2023, indicating challenges in scaling production that may impact investor confidence.

- Revenue Growth: Despite the drop in deliveries, Rivian's Q3 revenue grew by 78% year-over-year to approximately $1.56 billion, suggesting ongoing sales potential, though profitability issues remain unresolved.

- R2 Model Launch: Rivian is set to launch its R2 SUVs in the first half of this year, with a starting price of $60,000, aimed at attracting a broader customer base, which could positively impact the company's overall sales mix.

- Margin Challenges: While Rivian has begun posting positive gross margins, its automotive gross profit remains at negative $130 million, highlighting pressures from cost control and market competition, leaving future profitability uncertain.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy RIVN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on RIVN

Wall Street analysts forecast RIVN stock price to rise

18 Analyst Rating

8 Buy

7 Hold

3 Sell

Moderate Buy

Current: 14.690

Low

10.00

Averages

17.78

High

25.00

Current: 14.690

Low

10.00

Averages

17.78

High

25.00

About RIVN

Rivian Automotive, Inc. is an automotive technology company, which is engaged in developing and manufacturing category-defining electric vehicles (EVs) as well as vertically integrated technologies and services. The Company's R1 platform consists of two vehicles: the R1T, a two-row five-passenger pickup truck, and the R1S, a three-row seven-passenger sport utility vehicle (SUV). In the commercial market, the Company offers a Rivian Commercial Vehicle (RCV) platform. The vehicle on this platform is the Electric Delivery Van (EDV), designed and engineered by Rivian in collaboration with Amazon. The Company also offers FleetOS, its proprietary, end-to-end centralized fleet management subscription platform. It also offers a variety of services, including vehicle repair and maintenance, financing, insurance, joint venture, software subscriptions, and vehicle accessories, among others. Its other services include vehicle electrical architecture and software development services, and more.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Rivian Automotive Stock Declines 3.92% Amid Market Fluctuations

- Stock Fluctuation: Rivian Automotive (RIVN) closed at $14.69, reflecting a 3.92% decline from the previous day, underperforming the S&P 500's 0.08% gain, indicating market concerns about its future performance.

- Poor Monthly Performance: Over the past month, Rivian's stock has dropped by 3.65%, exceeding the Auto-Tires-Trucks sector's loss of 7.25%, highlighting the challenges the company faces in a competitive market.

- Earnings Expectations: Rivian is set to release its earnings on April 30, 2026, with analysts forecasting a loss of -$0.59 per share, a 43.9% year-over-year decline, while revenue is expected to be $1.34 billion, an 8.06% increase, showcasing potential for revenue growth.

- Analyst Ratings: Rivian currently holds a Zacks Rank of #3 (Hold), with a 2.15% downward revision in the EPS estimate over the past month, suggesting investors should closely monitor analyst perspectives on the company's future performance for informed investment decisions.

See More

EV Stocks Poised to Lead Autonomous Driving Revolution

- Market Potential: Experts predict that by 2030, a large-scale rollout of robotaxis will occur globally, marking the first commercial application for L4 autonomy, highlighting the critical role of the EV sector in future mobility.

- Rivian's New Launch: Rivian plans to begin shipping its R2 SUV this month, priced under $50,000, catering to about 70% of prospective buyers, which is expected to drive sales growth in 2026 and 2027, enhancing its market competitiveness.

- Tesla's Growth Opportunities: Despite Tesla's high stock valuation, its potential in fully autonomous vehicles and the robotaxi market is significant, with a projected global fleet of 3 million robotaxis by 2035, potentially worth $10 trillion.

- AI Investment Strategy: Rivian's heavy investment in artificial intelligence, while delaying its profitability timeline, positions the company favorably in the race for fully autonomous technology, reflecting its commitment to future market leadership.

See More

Robotic Taxi Market Expected to Surge by 2030

- Robotic Taxi Outlook: A McKinsey report indicates that by 2030, robotic taxis are expected to be widely deployed in the U.S. and other major countries, marking the first commercial application of Level 4 autonomy, which could transform mobility.

- Rivian's Market Opportunity: Rivian plans to begin shipping its R2 SUV this month, priced under $50,000, catering to approximately 70% of prospective buyers, with anticipated sales surges in 2026 and 2027, presenting a buying opportunity for investors at lower prices.

- Tesla's AI Edge: Despite Tesla's high stock price, its significant investments in full self-driving technology present substantial growth potential, as studies show consumers are willing to pay twice as much for self-driving features compared to other safety enhancements, which could boost Tesla's sales growth.

- Robotaxi Market Value: Boston Consulting Group predicts a global fleet of up to 3 million robotaxis by 2035, with a potential market value of $10 trillion, positioning Tesla to leverage its financial strength and manufacturing capabilities to dominate this competitive landscape.

See More

Rivian vs. Lucid: Analyzing EV Market Prospects

- Rivian Stock Performance: Since its 2021 IPO, Rivian's stock has plummeted approximately 91.5% from its valuation peak, yet despite ongoing significant net losses, the positive contribution from its software and services business has shifted its overall gross margin to positive, indicating potential investment appeal.

- Lucid Recall Incident: Lucid recently announced a recall of over 4,400 Gravity SUVs and initiated a 29-day shipment halt, which, while not signaling imminent bankruptcy, highlights the critical role of the Gravity line in its growth strategy for production and deliveries, potentially impacting future performance.

- Funding Support Outlook: Despite facing weak performance and the threat of stock dilution, Lucid's continued funding injections from its largest shareholder, Saudi Arabia's Public Investment Fund, suggest that the company can sustain operations despite posting significant losses, indicating it won't face an immediate survival crisis.

- Market Competition Analysis: While Rivian is not guaranteed to win in the EV market, it currently presents a better investment opportunity compared to Lucid, particularly as it strives to achieve profitability, making it essential for investors to monitor its future earnings potential and market performance.

See More

Rivian and Lucid Stocks Plummet from All-Time Highs

- Stock Price Collapse: Rivian's stock has plummeted approximately 91.5% from its all-time high, while Lucid has seen an even steeper decline of about 98.5%, indicating a severe drop in investor confidence and valuation for both companies in the electric vehicle market.

- Lucid Recall Crisis: Lucid recently announced a recall of over 4,400 Gravity SUVs and initiated a 29-day shipping halt, which, while not signaling imminent bankruptcy, poses significant challenges to its growth strategy for production and deliveries.

- Rivian's Financial Struggles: Although Rivian's automotive sales gross margins remain negative, contributions from its software and services business have allowed for an overall positive gross margin; however, the company's ability to achieve sustainable profitability remains highly uncertain.

- Investment Outlook Comparison: Despite the risks facing Rivian, it is currently viewed as a more attractive investment compared to Lucid, which is grappling with ongoing stock dilution and weak performance, especially in the increasingly competitive electric vehicle market.

See More

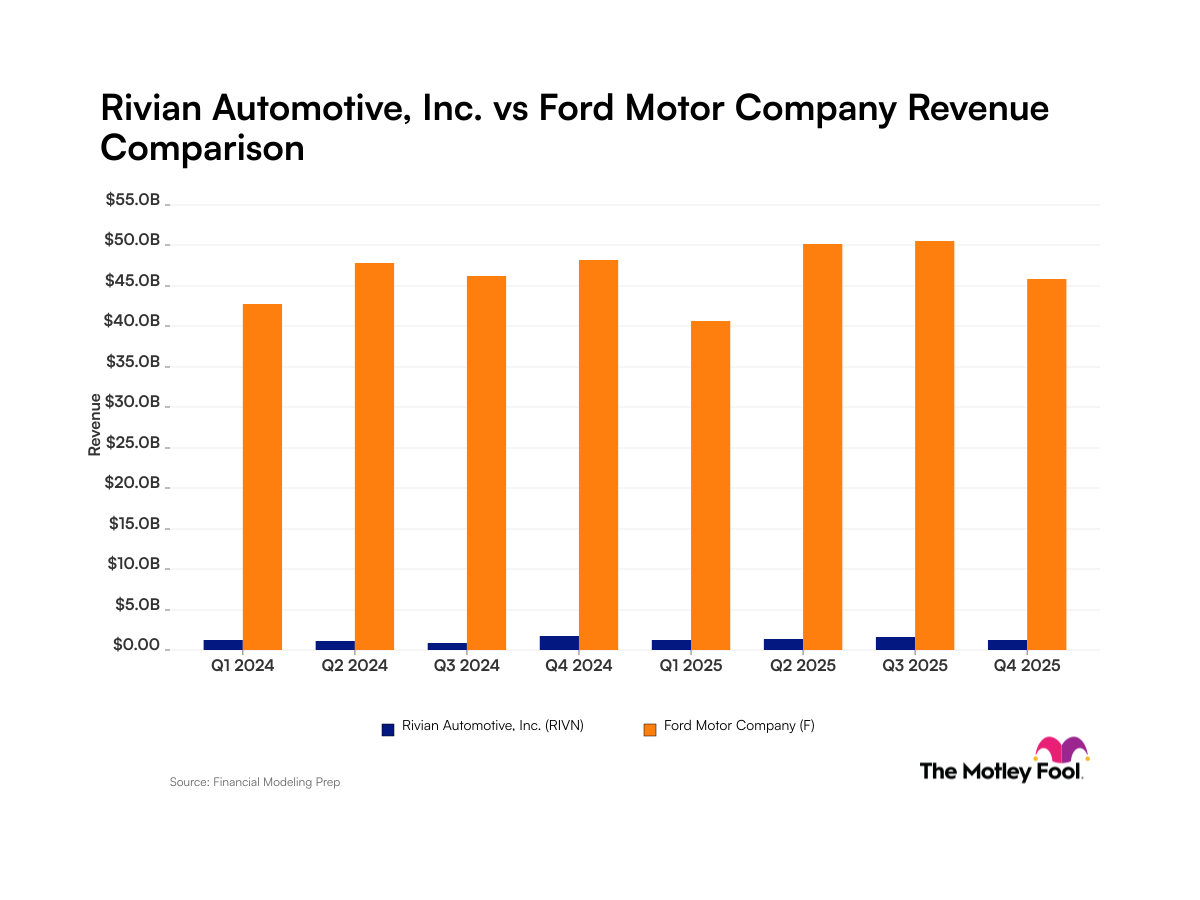

Ford vs. Rivian: The Profitability Race

- Revenue Comparison: Ford's quarterly revenue consistently ranges from $40 billion to $50 billion throughout 2024 and 2025, while Rivian's revenue barely reaches $1.2 billion to $1.7 billion, highlighting Ford's market dominance despite both companies facing losses.

- Rivian's Strategic Moves: Rivian's autonomous deployment agreement with Uber and partnership with Volkswagen could significantly diversify its revenue streams over time, although it reported a concerning net income margin of -63% as of Q4 2025, indicative of its capital-intensive growth phase.

- Ford's Strategic Adjustments: Ford's net income margin stood at -24% in Q4 2025, which, while less severe than Rivian's, reflects the substantial costs associated with its strategic shift towards gas-powered vehicles and the establishment of a new battery division.

- Investor Focus: For retail investors, revenue serves as a foundational measure of a company's sales capability, and the widening gap between Ford and Rivian's revenues underscores potential profitability differences; thus, the next five years will reveal which company can more effectively close the gap between revenue and profitability.

See More

Rivian Automotive Stock Declines 3.92% Amid Market Fluctuations

- Stock Fluctuation: Rivian Automotive (RIVN) closed at $14.69, reflecting a 3.92% decline from the previous day, underperforming the S&P 500's 0.08% gain, indicating market concerns about its future performance.

- Poor Monthly Performance: Over the past month, Rivian's stock has dropped by 3.65%, exceeding the Auto-Tires-Trucks sector's loss of 7.25%, highlighting the challenges the company faces in a competitive market.

- Earnings Expectations: Rivian is set to release its earnings on April 30, 2026, with analysts forecasting a loss of -$0.59 per share, a 43.9% year-over-year decline, while revenue is expected to be $1.34 billion, an 8.06% increase, showcasing potential for revenue growth.

- Analyst Ratings: Rivian currently holds a Zacks Rank of #3 (Hold), with a 2.15% downward revision in the EPS estimate over the past month, suggesting investors should closely monitor analyst perspectives on the company's future performance for informed investment decisions.

See More

EV Stocks Poised to Lead Autonomous Driving Revolution

- Market Potential: Experts predict that by 2030, a large-scale rollout of robotaxis will occur globally, marking the first commercial application for L4 autonomy, highlighting the critical role of the EV sector in future mobility.

- Rivian's New Launch: Rivian plans to begin shipping its R2 SUV this month, priced under $50,000, catering to about 70% of prospective buyers, which is expected to drive sales growth in 2026 and 2027, enhancing its market competitiveness.

- Tesla's Growth Opportunities: Despite Tesla's high stock valuation, its potential in fully autonomous vehicles and the robotaxi market is significant, with a projected global fleet of 3 million robotaxis by 2035, potentially worth $10 trillion.

- AI Investment Strategy: Rivian's heavy investment in artificial intelligence, while delaying its profitability timeline, positions the company favorably in the race for fully autonomous technology, reflecting its commitment to future market leadership.

See More

Robotic Taxi Market Expected to Surge by 2030

- Robotic Taxi Outlook: A McKinsey report indicates that by 2030, robotic taxis are expected to be widely deployed in the U.S. and other major countries, marking the first commercial application of Level 4 autonomy, which could transform mobility.

- Rivian's Market Opportunity: Rivian plans to begin shipping its R2 SUV this month, priced under $50,000, catering to approximately 70% of prospective buyers, with anticipated sales surges in 2026 and 2027, presenting a buying opportunity for investors at lower prices.

- Tesla's AI Edge: Despite Tesla's high stock price, its significant investments in full self-driving technology present substantial growth potential, as studies show consumers are willing to pay twice as much for self-driving features compared to other safety enhancements, which could boost Tesla's sales growth.

- Robotaxi Market Value: Boston Consulting Group predicts a global fleet of up to 3 million robotaxis by 2035, with a potential market value of $10 trillion, positioning Tesla to leverage its financial strength and manufacturing capabilities to dominate this competitive landscape.

See More

Rivian vs. Lucid: Analyzing EV Market Prospects

- Rivian Stock Performance: Since its 2021 IPO, Rivian's stock has plummeted approximately 91.5% from its valuation peak, yet despite ongoing significant net losses, the positive contribution from its software and services business has shifted its overall gross margin to positive, indicating potential investment appeal.

- Lucid Recall Incident: Lucid recently announced a recall of over 4,400 Gravity SUVs and initiated a 29-day shipment halt, which, while not signaling imminent bankruptcy, highlights the critical role of the Gravity line in its growth strategy for production and deliveries, potentially impacting future performance.

- Funding Support Outlook: Despite facing weak performance and the threat of stock dilution, Lucid's continued funding injections from its largest shareholder, Saudi Arabia's Public Investment Fund, suggest that the company can sustain operations despite posting significant losses, indicating it won't face an immediate survival crisis.

- Market Competition Analysis: While Rivian is not guaranteed to win in the EV market, it currently presents a better investment opportunity compared to Lucid, particularly as it strives to achieve profitability, making it essential for investors to monitor its future earnings potential and market performance.

See More

Rivian and Lucid Stocks Plummet from All-Time Highs

- Stock Price Collapse: Rivian's stock has plummeted approximately 91.5% from its all-time high, while Lucid has seen an even steeper decline of about 98.5%, indicating a severe drop in investor confidence and valuation for both companies in the electric vehicle market.

- Lucid Recall Crisis: Lucid recently announced a recall of over 4,400 Gravity SUVs and initiated a 29-day shipping halt, which, while not signaling imminent bankruptcy, poses significant challenges to its growth strategy for production and deliveries.

- Rivian's Financial Struggles: Although Rivian's automotive sales gross margins remain negative, contributions from its software and services business have allowed for an overall positive gross margin; however, the company's ability to achieve sustainable profitability remains highly uncertain.

- Investment Outlook Comparison: Despite the risks facing Rivian, it is currently viewed as a more attractive investment compared to Lucid, which is grappling with ongoing stock dilution and weak performance, especially in the increasingly competitive electric vehicle market.

See More

Ford vs. Rivian: The Profitability Race

- Revenue Comparison: Ford's quarterly revenue consistently ranges from $40 billion to $50 billion throughout 2024 and 2025, while Rivian's revenue barely reaches $1.2 billion to $1.7 billion, highlighting Ford's market dominance despite both companies facing losses.

- Rivian's Strategic Moves: Rivian's autonomous deployment agreement with Uber and partnership with Volkswagen could significantly diversify its revenue streams over time, although it reported a concerning net income margin of -63% as of Q4 2025, indicative of its capital-intensive growth phase.

- Ford's Strategic Adjustments: Ford's net income margin stood at -24% in Q4 2025, which, while less severe than Rivian's, reflects the substantial costs associated with its strategic shift towards gas-powered vehicles and the establishment of a new battery division.

- Investor Focus: For retail investors, revenue serves as a foundational measure of a company's sales capability, and the widening gap between Ford and Rivian's revenues underscores potential profitability differences; thus, the next five years will reveal which company can more effectively close the gap between revenue and profitability.

See More