Oppenheimer Upgrades Airbnb to Outperform, Sees Revenue Growth Potential

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Should l Buy ABNB?

Source: seekingalpha

- Rating Upgrade: Oppenheimer upgraded Airbnb (ABNB) from Perform to Outperform, anticipating that new product initiatives will drive sustainable revenue growth that is not fully reflected in market consensus.

- Hotel Market Progress: Analyst Jed Kelly highlighted encouraging developments in test markets, particularly in Manhattan, where Airbnb is offering site credits and discounts compared to competitors, enhancing its market competitiveness.

- AI Search Opportunity: Kelly believes that Airbnb's conversational search will leverage design and supply scale to boost conversion rates, with the potential to introduce sponsored listings using natural language, simplifying visibility for all host types and enhancing user experience.

- Price Target Assessment: Oppenheimer set a price target of $180 for ABNB, equating to 17 times the 2027 EBITDA, which is justified by a higher margin structure and a more predictable business model, positioning it at the high end of the peer range.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ABNB?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ABNB

Wall Street analysts forecast ABNB stock price to rise

29 Analyst Rating

12 Buy

16 Hold

1 Sell

Moderate Buy

Current: 139.880

Low

107.00

Averages

144.85

High

180.00

Current: 139.880

Low

107.00

Averages

144.85

High

180.00

About ABNB

Airbnb, Inc. operates a global platform for stays and experiences. The Company’s marketplace model connects hosts and guests online or through mobile devices to book spaces and experiences around the world. The Company has built its platform to onboard new hosts, especially those who previously had not considered hosting. It partners with hosts throughout the process of setting up their listing and provides them with a suite of tools to manage their listings, including scheduling, merchandising, integrated payments, community support, host protection, pricing guidance, and feedback from reviews. Its Website and mobile applications provide its guests with a way to explore a variety of homes and experiences and an easy way to book them. Its technology platform powers its two-sided marketplace and enables its global network of hosts and guests. It owns a trademark portfolio with protection in 220 countries in which it operates for its primary brands, AIRBNB, and its Belo logo.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Airbnb Set to Announce Q1 Earnings with Strong Growth Expectations

- Earnings Expectations: Airbnb is expected to report Q1 EPS of $0.31 and revenue of $2.62 billion, reflecting a growth of 14% to 16% compared to last year, surpassing the market estimate of $2.53 billion, indicating strong performance in the market.

- Booking Growth: Gross bookings are anticipated to grow in the low teens, driven by high-single-digit growth in nights and stays booked, suggesting sustained consumer demand that further solidifies Airbnb's market position.

- Analyst Ratings: Oppenheimer upgraded Airbnb from Perform to Outperform with a price target of $180, reflecting optimism about the company's product innovations and AI search capabilities, which could drive accelerated revenue growth in the future.

- Market Performance: Although Airbnb's stock has risen 3.8% this year, it underperforms the S&P 500's 6% gain, indicating cautious market sentiment regarding its future growth, especially as management focuses on platform improvements and expanding service areas.

See More

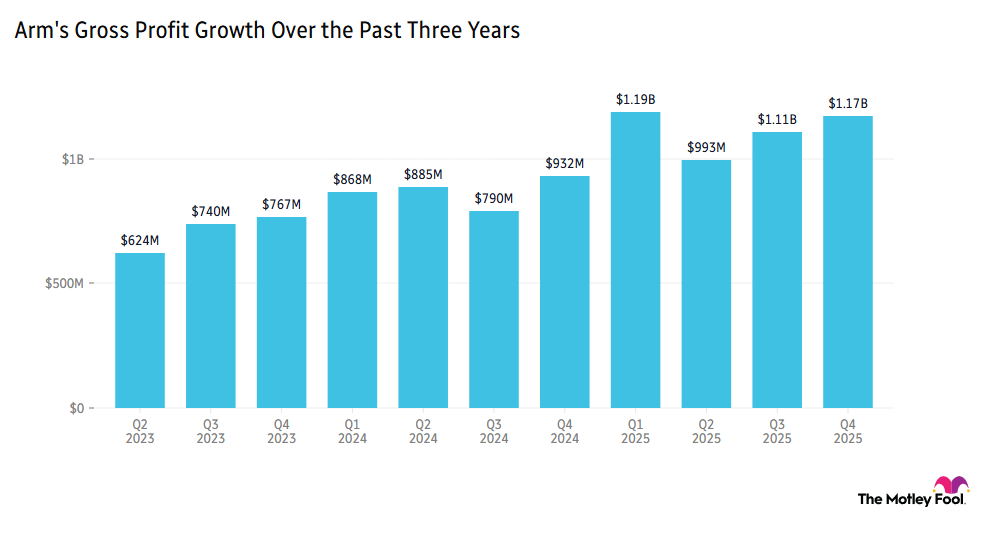

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More

Earnings Reports and Economic Data Preview for Tomorrow

- McDonald's Earnings Preview: McDonald's is set to report its Q1 earnings on May 7, with analysts expecting a same-store sales increase of up to 4%, primarily due to easy comparisons from last year's E. coli-related slowdown, indicating potential recovery in consumer confidence.

- Coinbase Trading Volume Decline: Analysts anticipate a softer quarter for Coinbase as trading volumes cool alongside declining crypto prices, likely pressuring transaction revenue and reflecting the volatility of the crypto market's direct impact on company performance.

- Shell and Airbnb Earnings: Shell and Airbnb will also release earnings on the same day, with investors keen to assess their performance amid inflationary pressures and shifts in consumer spending, evaluating their future growth potential in the current economic landscape.

- Initial Jobless Claims Data: Economists forecast initial jobless claims to rise to 205,000 this week, providing further insights into the health of the labor market, which could influence market confidence in economic recovery.

See More

FDN ETF 52-Week Price Fluctuation Analysis

- Price Range Analysis: FDN ETF's 52-week low is $224.465 per share, with a high of $287.81, while the last trade was at $267.32, indicating relative stability and volatility in the current market.

- Technical Analysis Tool: Comparing the current share price to the 200-day moving average provides valuable insights for investors, helping to assess market trends and potential buying opportunities.

- ETF Unit Trading Mechanism: ETFs trade similarly to stocks, where investors buy and sell 'units' that can be created or destroyed based on investor demand, impacting liquidity and market performance.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding helps identify ETFs experiencing significant inflows or outflows, allowing investors to capture market dynamics and investment opportunities.

See More

SpaceX Plans Historic IPO Targeting $1.75 Trillion Valuation

- IPO Filing: Last month, SpaceX confidentially filed for an initial public offering (IPO) with the SEC, planning to kick off its roadshow on June 8 to pitch the stock to institutional investors and analysts, although a specific IPO date has not been set, trading is expected to commence in late June or early July.

- Valuation Target: The company is aiming for a staggering $1.75 trillion valuation, which would make it the largest IPO in U.S. history; however, historical trends indicate that IPO stocks often underperform in their first year, prompting investors to exercise caution.

- Historical Performance Insights: Data shows that since 1980, around 9,300 companies have gone public on the NYSE or Nasdaq, with IPO stocks gaining an average of 19% on their first trading day, yet those with large market values frequently experience sharp declines after initial excitement fades.

- Long-Term Investment Risks: While SpaceX may perform well in the long run, most large IPO stocks historically have underperformed the S&P 500 post-listing, suggesting that investors might be better off investing in an S&P 500 index fund rather than directly purchasing SpaceX shares.

See More

SpaceX Aims for $1.75 Trillion IPO Record

- IPO Market Value Target: SpaceX is targeting a $1.75 trillion valuation for its IPO, which would make it the largest in U.S. history; however, historical data shows that the top 10 IPOs have seen a median decline of 31% in their first year, potentially undermining investor confidence.

- Listing Timeline: SpaceX confidentially filed its IPO paperwork with the SEC last month and plans to kick off its IPO roadshow on June 8, with shares expected to start trading in late June or early July, providing an opportunity to attract institutional investors.

- Historical Performance Warning: Data indicates that seven out of the ten largest IPOs have underperformed the S&P 500 since their listings, with Alibaba's market value of $169 billion at IPO being significantly lower than SpaceX's target, highlighting the risks associated with high-value IPOs.

- Investor Caution Advice: Despite the excitement surrounding SpaceX's IPO, historical trends suggest that investors should be cautious when purchasing high-value stocks, as most similar companies tend to perform poorly post-IPO, recommending that investors wait for more favorable buying opportunities.

See More

Airbnb Set to Announce Q1 Earnings with Strong Growth Expectations

- Earnings Expectations: Airbnb is expected to report Q1 EPS of $0.31 and revenue of $2.62 billion, reflecting a growth of 14% to 16% compared to last year, surpassing the market estimate of $2.53 billion, indicating strong performance in the market.

- Booking Growth: Gross bookings are anticipated to grow in the low teens, driven by high-single-digit growth in nights and stays booked, suggesting sustained consumer demand that further solidifies Airbnb's market position.

- Analyst Ratings: Oppenheimer upgraded Airbnb from Perform to Outperform with a price target of $180, reflecting optimism about the company's product innovations and AI search capabilities, which could drive accelerated revenue growth in the future.

- Market Performance: Although Airbnb's stock has risen 3.8% this year, it underperforms the S&P 500's 6% gain, indicating cautious market sentiment regarding its future growth, especially as management focuses on platform improvements and expanding service areas.

See More

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More

Earnings Reports and Economic Data Preview for Tomorrow

- McDonald's Earnings Preview: McDonald's is set to report its Q1 earnings on May 7, with analysts expecting a same-store sales increase of up to 4%, primarily due to easy comparisons from last year's E. coli-related slowdown, indicating potential recovery in consumer confidence.

- Coinbase Trading Volume Decline: Analysts anticipate a softer quarter for Coinbase as trading volumes cool alongside declining crypto prices, likely pressuring transaction revenue and reflecting the volatility of the crypto market's direct impact on company performance.

- Shell and Airbnb Earnings: Shell and Airbnb will also release earnings on the same day, with investors keen to assess their performance amid inflationary pressures and shifts in consumer spending, evaluating their future growth potential in the current economic landscape.

- Initial Jobless Claims Data: Economists forecast initial jobless claims to rise to 205,000 this week, providing further insights into the health of the labor market, which could influence market confidence in economic recovery.

See More

FDN ETF 52-Week Price Fluctuation Analysis

- Price Range Analysis: FDN ETF's 52-week low is $224.465 per share, with a high of $287.81, while the last trade was at $267.32, indicating relative stability and volatility in the current market.

- Technical Analysis Tool: Comparing the current share price to the 200-day moving average provides valuable insights for investors, helping to assess market trends and potential buying opportunities.

- ETF Unit Trading Mechanism: ETFs trade similarly to stocks, where investors buy and sell 'units' that can be created or destroyed based on investor demand, impacting liquidity and market performance.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding helps identify ETFs experiencing significant inflows or outflows, allowing investors to capture market dynamics and investment opportunities.

See More

SpaceX Plans Historic IPO Targeting $1.75 Trillion Valuation

- IPO Filing: Last month, SpaceX confidentially filed for an initial public offering (IPO) with the SEC, planning to kick off its roadshow on June 8 to pitch the stock to institutional investors and analysts, although a specific IPO date has not been set, trading is expected to commence in late June or early July.

- Valuation Target: The company is aiming for a staggering $1.75 trillion valuation, which would make it the largest IPO in U.S. history; however, historical trends indicate that IPO stocks often underperform in their first year, prompting investors to exercise caution.

- Historical Performance Insights: Data shows that since 1980, around 9,300 companies have gone public on the NYSE or Nasdaq, with IPO stocks gaining an average of 19% on their first trading day, yet those with large market values frequently experience sharp declines after initial excitement fades.

- Long-Term Investment Risks: While SpaceX may perform well in the long run, most large IPO stocks historically have underperformed the S&P 500 post-listing, suggesting that investors might be better off investing in an S&P 500 index fund rather than directly purchasing SpaceX shares.

See More

SpaceX Aims for $1.75 Trillion IPO Record

- IPO Market Value Target: SpaceX is targeting a $1.75 trillion valuation for its IPO, which would make it the largest in U.S. history; however, historical data shows that the top 10 IPOs have seen a median decline of 31% in their first year, potentially undermining investor confidence.

- Listing Timeline: SpaceX confidentially filed its IPO paperwork with the SEC last month and plans to kick off its IPO roadshow on June 8, with shares expected to start trading in late June or early July, providing an opportunity to attract institutional investors.

- Historical Performance Warning: Data indicates that seven out of the ten largest IPOs have underperformed the S&P 500 since their listings, with Alibaba's market value of $169 billion at IPO being significantly lower than SpaceX's target, highlighting the risks associated with high-value IPOs.

- Investor Caution Advice: Despite the excitement surrounding SpaceX's IPO, historical trends suggest that investors should be cautious when purchasing high-value stocks, as most similar companies tend to perform poorly post-IPO, recommending that investors wait for more favorable buying opportunities.

See More