Microsoft's New Xbox CEO Appoints Executives

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 2 days ago

0mins

Should l Buy MSFT?

Source: Newsfilter

- Executive Appointments: New Xbox CEO Asha Sharma is bringing in four executives from the CoreAI engineering group to enhance Xbox's technical and consumer expertise, addressing the challenge of four revenue declines in the past six quarters.

- Organizational Change: In a memo, Sharma emphasized the need to evolve work methods and organizational structure to accelerate product delivery and reduce internal communication time, thereby enhancing Xbox's market competitiveness through better community engagement.

- Market Competition Pressure: Data from VGChartz indicates that Xbox Series X and Series S were outsold by Nintendo Switch and Sony PlayStation 5 in Q1, highlighting Xbox's insufficient market competitiveness and the urgent need for strategic adjustments to attract gamers.

- Team Restructuring: Newly appointed executives include Jared Palmer, who will oversee product, engineering, and developer tools, and Tim Allen, who will lead design, reflecting Sharma's focus on team capabilities to drive Xbox's growth and innovation.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 420.770

Low

500.00

Averages

631.36

High

678.00

Current: 420.770

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company. The Company develops and supports software, services, devices, and solutions. The Company’s segments include Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services. This segment primarily comprises: Office Commercial, Office Consumer, LinkedIn, and Dynamics business solutions. The Intelligent Cloud segment consists of server products and cloud services, including Azure and other cloud services, SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), and Nuance and GitHub; and Enterprise Services, including enterprise support services, industry solutions and Nuance professional services. The More Personal Computing segment primarily comprises Windows, Devices, Gaming, and search and news advertising.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft's Strong Earnings Amidst Stock Slump Suggests Potential Comeback

- Strong Earnings Report: Microsoft reported an 18% year-over-year revenue increase and a 20% rise in operating income for Q3 of fiscal 2026, indicating robust performance in the AI sector, despite a declining stock price.

- Cloud Computing Growth: Azure's revenue surged by 40% this quarter as clients utilize its computing power for AI model training, solidifying Microsoft's position as a key player in the cloud market and driving significant revenue growth.

- Booming AI Business: Microsoft's non-cloud AI segment achieved a $37 billion annual run rate with a staggering 123% year-over-year growth, showcasing the substantial returns from its AI investments, even as the stock price fails to reflect this success.

- Attractive Valuation: With an operating price-to-earnings ratio of about 21, Microsoft is trading at its lowest valuation in a decade, and given its strong business fundamentals, a stock rebound is anticipated, presenting a compelling buying opportunity for investors.

See More

Microsoft: A Blue-Chip Stock for Generations

- Financial Robustness: Microsoft reported $82.9 billion in revenue for the most recent quarter, surpassing the combined revenues of Broadcom, Lenovo, and IBM over the past four quarters, demonstrating its strong profitability and market leadership, which ensures resilience during economic fluctuations.

- Diversified Business Model: As the world's largest enterprise software provider, Microsoft's operations span operating systems, cloud platforms, hardware, and social media, creating a robust ecosystem that businesses heavily rely on for daily operations, enhancing its strategic significance.

- Stable Dividend Growth: Although Microsoft has a modest dividend yield of 0.8%, it has increased its dividend by 152% over the past decade and has raised its dividend for 21 consecutive years, showcasing its stable cash flow and commitment to shareholders, positioning it to potentially become a Dividend King.

- Cash Reserve Advantage: With $78.3 billion in cash reserves, Microsoft has a safety net that allows it to navigate economic uncertainties while actively pursuing new technologies, particularly in artificial intelligence, thereby enhancing its competitive edge in the tech industry.

See More

Signs of Recovery in Software Stocks Market

- ETF Performance Recovery: The iShares Expanded Tech-Software ETF (IGV) has risen nearly 14% over the past month, rebounding over 4% in April and ending a three-month decline, indicating a gradual restoration of market confidence in the software sector.

- Year-to-Date Weakness: Despite the recent uptick, IGV is still down 14% year-to-date, as investor concerns about artificial intelligence potentially eroding market share from software-as-a-service companies persist, leading to fears of a 'SaaSpocalypse.'

- Individual Stock Breakouts: Jason Hunter, a technical strategist at JPMorgan, noted that software stocks are less correlated than semiconductors recently, with several stocks breaking out from multi-week base patterns, including Palo Alto Networks, Oracle, Microsoft, and CrowdStrike.

- Oracle's Strong Performance: Among these stocks, Oracle has been the standout performer, surging over 35.5% in the past month to close at $194.59 on Thursday, nearing levels last seen in January, while Microsoft, after breaking back above $400 in April, closed at $420.77 on Thursday, indicating strong upward momentum.

See More

Consumer Confidence Decline Impacts Stock Market

- Market Volatility: Shares of several consumer-focused companies plummeted yesterday, with Planet Fitness down over 30%, marking its largest one-day loss ever, indicating market concerns about consumer health that could hinder overall economic recovery.

- Shake Shack Earnings Miss: Shake Shack's stock dropped more than 28% following an operating loss and earnings miss in Q1, reflecting weak consumer spending that may pressure future performance.

- Job Data Expectations: The U.S. is expected to add 55,000 jobs in April, with the unemployment rate holding steady at 4.3%, a figure that could sway market sentiment, as JPMorgan's trading desk warns of potential significant market swings.

- Cloudflare Layoffs Impact: Cloudflare announced it would cut over one-fifth of its workforce, leading to a 15% pre-market drop in its stock, despite beating Q1 earnings expectations, indicating the company's cautious outlook on future market conditions.

See More

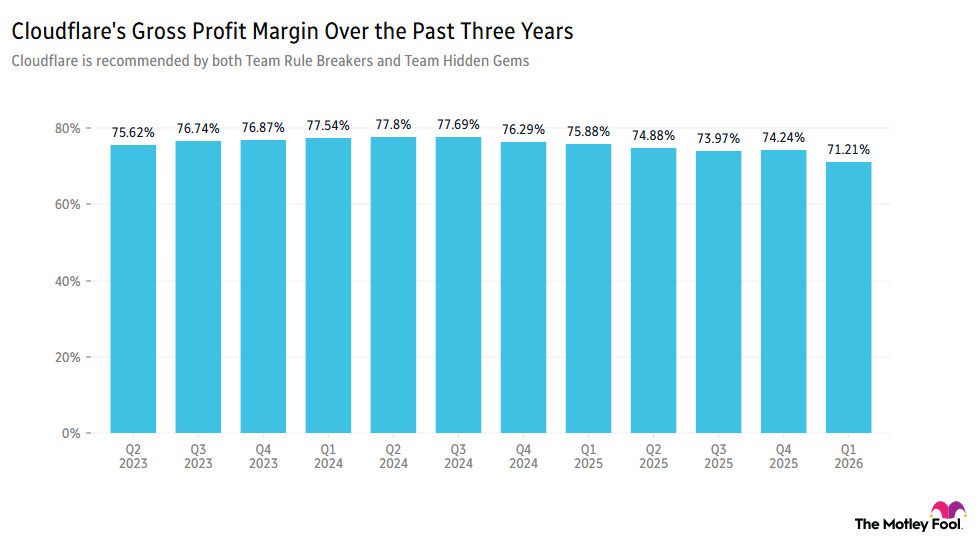

Cloudflare's AI Reform Triggers Stock Plunge

- Significant Stock Drop: Cloudflare's stock plummeted over 18% ahead of the market open as investors perceived the company's late entry into AI as a major concern, despite management's assertion of it being the 'biggest tailwind we've ever seen,' compounded by a 4.67% year-over-year decline in gross profit margins that undermined market confidence.

- Layoff Implementation: The company announced a layoff of 1,100 employees, representing 20% of its current workforce, with management stating in an internal email the need to 'be intentional in how we architect our company for the agentic AI era,' which could impact operational efficiency and employee morale.

- Strong Revenue Growth: Despite the drop in gross margins, Cloudflare reported a 34% year-over-year revenue increase and raised its outlook for fiscal year 2026 revenue and earnings, indicating that investments in AI may yield returns in the future.

- Outstanding Market Performance: Since November 2022, Cloudflare's stock has outperformed the S&P 500 by 285%, suggesting that despite current challenges, investors remain optimistic about the company's long-term potential.

See More

Exploring Tesla's Future Relationship with SpaceXAI

- Diverging Investor Views: Influencer DoctorJack16 suggests that investors may underestimate the significance of SpaceX, Starlink, and xAI infrastructure for Tesla's long-term AI ambitions, potentially impacting Tesla's market positioning and investor confidence.

- Merger Discussions Heat Up: Cern Basher notes that while many Tesla bulls oppose a merger with SpaceXAI, the accelerating AI race may force Tesla deeper into Musk's tech ecosystem, influencing its future strategy.

- Value of Robotaxi and Optimus: Basher argues that Tesla's Robotaxi and Optimus projects are still in their early stages, with many investors hoping for greater value creation in the coming years, reflecting confidence in Tesla's future growth potential.

- Infrastructure Risks Emerge: Basher warns that Tesla may face constraints from AI infrastructure, semiconductors, and regulation, and if it cannot secure sufficient semiconductor capacity, it could impact the global deployment of Cybercab and Optimus, thereby affecting the company's valuation.

See More

Microsoft's Strong Earnings Amidst Stock Slump Suggests Potential Comeback

- Strong Earnings Report: Microsoft reported an 18% year-over-year revenue increase and a 20% rise in operating income for Q3 of fiscal 2026, indicating robust performance in the AI sector, despite a declining stock price.

- Cloud Computing Growth: Azure's revenue surged by 40% this quarter as clients utilize its computing power for AI model training, solidifying Microsoft's position as a key player in the cloud market and driving significant revenue growth.

- Booming AI Business: Microsoft's non-cloud AI segment achieved a $37 billion annual run rate with a staggering 123% year-over-year growth, showcasing the substantial returns from its AI investments, even as the stock price fails to reflect this success.

- Attractive Valuation: With an operating price-to-earnings ratio of about 21, Microsoft is trading at its lowest valuation in a decade, and given its strong business fundamentals, a stock rebound is anticipated, presenting a compelling buying opportunity for investors.

See More

Microsoft: A Blue-Chip Stock for Generations

- Financial Robustness: Microsoft reported $82.9 billion in revenue for the most recent quarter, surpassing the combined revenues of Broadcom, Lenovo, and IBM over the past four quarters, demonstrating its strong profitability and market leadership, which ensures resilience during economic fluctuations.

- Diversified Business Model: As the world's largest enterprise software provider, Microsoft's operations span operating systems, cloud platforms, hardware, and social media, creating a robust ecosystem that businesses heavily rely on for daily operations, enhancing its strategic significance.

- Stable Dividend Growth: Although Microsoft has a modest dividend yield of 0.8%, it has increased its dividend by 152% over the past decade and has raised its dividend for 21 consecutive years, showcasing its stable cash flow and commitment to shareholders, positioning it to potentially become a Dividend King.

- Cash Reserve Advantage: With $78.3 billion in cash reserves, Microsoft has a safety net that allows it to navigate economic uncertainties while actively pursuing new technologies, particularly in artificial intelligence, thereby enhancing its competitive edge in the tech industry.

See More

Signs of Recovery in Software Stocks Market

- ETF Performance Recovery: The iShares Expanded Tech-Software ETF (IGV) has risen nearly 14% over the past month, rebounding over 4% in April and ending a three-month decline, indicating a gradual restoration of market confidence in the software sector.

- Year-to-Date Weakness: Despite the recent uptick, IGV is still down 14% year-to-date, as investor concerns about artificial intelligence potentially eroding market share from software-as-a-service companies persist, leading to fears of a 'SaaSpocalypse.'

- Individual Stock Breakouts: Jason Hunter, a technical strategist at JPMorgan, noted that software stocks are less correlated than semiconductors recently, with several stocks breaking out from multi-week base patterns, including Palo Alto Networks, Oracle, Microsoft, and CrowdStrike.

- Oracle's Strong Performance: Among these stocks, Oracle has been the standout performer, surging over 35.5% in the past month to close at $194.59 on Thursday, nearing levels last seen in January, while Microsoft, after breaking back above $400 in April, closed at $420.77 on Thursday, indicating strong upward momentum.

See More

Consumer Confidence Decline Impacts Stock Market

- Market Volatility: Shares of several consumer-focused companies plummeted yesterday, with Planet Fitness down over 30%, marking its largest one-day loss ever, indicating market concerns about consumer health that could hinder overall economic recovery.

- Shake Shack Earnings Miss: Shake Shack's stock dropped more than 28% following an operating loss and earnings miss in Q1, reflecting weak consumer spending that may pressure future performance.

- Job Data Expectations: The U.S. is expected to add 55,000 jobs in April, with the unemployment rate holding steady at 4.3%, a figure that could sway market sentiment, as JPMorgan's trading desk warns of potential significant market swings.

- Cloudflare Layoffs Impact: Cloudflare announced it would cut over one-fifth of its workforce, leading to a 15% pre-market drop in its stock, despite beating Q1 earnings expectations, indicating the company's cautious outlook on future market conditions.

See More

Cloudflare's AI Reform Triggers Stock Plunge

- Significant Stock Drop: Cloudflare's stock plummeted over 18% ahead of the market open as investors perceived the company's late entry into AI as a major concern, despite management's assertion of it being the 'biggest tailwind we've ever seen,' compounded by a 4.67% year-over-year decline in gross profit margins that undermined market confidence.

- Layoff Implementation: The company announced a layoff of 1,100 employees, representing 20% of its current workforce, with management stating in an internal email the need to 'be intentional in how we architect our company for the agentic AI era,' which could impact operational efficiency and employee morale.

- Strong Revenue Growth: Despite the drop in gross margins, Cloudflare reported a 34% year-over-year revenue increase and raised its outlook for fiscal year 2026 revenue and earnings, indicating that investments in AI may yield returns in the future.

- Outstanding Market Performance: Since November 2022, Cloudflare's stock has outperformed the S&P 500 by 285%, suggesting that despite current challenges, investors remain optimistic about the company's long-term potential.

See More

Exploring Tesla's Future Relationship with SpaceXAI

- Diverging Investor Views: Influencer DoctorJack16 suggests that investors may underestimate the significance of SpaceX, Starlink, and xAI infrastructure for Tesla's long-term AI ambitions, potentially impacting Tesla's market positioning and investor confidence.

- Merger Discussions Heat Up: Cern Basher notes that while many Tesla bulls oppose a merger with SpaceXAI, the accelerating AI race may force Tesla deeper into Musk's tech ecosystem, influencing its future strategy.

- Value of Robotaxi and Optimus: Basher argues that Tesla's Robotaxi and Optimus projects are still in their early stages, with many investors hoping for greater value creation in the coming years, reflecting confidence in Tesla's future growth potential.

- Infrastructure Risks Emerge: Basher warns that Tesla may face constraints from AI infrastructure, semiconductors, and regulation, and if it cannot secure sufficient semiconductor capacity, it could impact the global deployment of Cybercab and Optimus, thereby affecting the company's valuation.

See More