Microsoft Cuts Xbox Game Pass Prices Amid Industry Trends

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Should l Buy MSFT?

Source: Yahoo Finance

- Price Adjustment: Microsoft has announced a reduction in the Xbox Game Pass Ultimate monthly fee from $29.99 to $22.99, while the PC version will drop from $16.49 to $13.99, a move that counters the broader industry trend of price increases, aiming to attract more users and enhance market competitiveness.

- Game Availability Change: Despite the price cuts, Microsoft stated that future 'Call of Duty' titles will no longer be available on the subscription service on their release day, instead launching about a year later, which may affect players' immediate access to new games and potentially impact the attractiveness of the subscription service.

- Management Change Impact: This price adjustment marks the first major decision from new Microsoft Gaming CEO Asha Sharma, aimed at winning goodwill from gamers, especially following the departure of the beloved former CEO Phil Spencer, and Sharma's decisions may influence the company's brand image moving forward.

- Market Environment Comparison: In a context where game consoles and games are generally becoming more expensive, Microsoft's pricing strategy stands out, particularly as competitors like Sony and Nintendo are also raising prices, which may help Microsoft differentiate itself and attract price-sensitive consumers.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 432.920

Low

500.00

Averages

631.36

High

678.00

Current: 432.920

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company. The Company develops and supports software, services, devices, and solutions. The Company’s segments include Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services. This segment primarily comprises: Office Commercial, Office Consumer, LinkedIn, and Dynamics business solutions. The Intelligent Cloud segment consists of server products and cloud services, including Azure and other cloud services, SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), and Nuance and GitHub; and Enterprise Services, including enterprise support services, industry solutions and Nuance professional services. The More Personal Computing segment primarily comprises Windows, Devices, Gaming, and search and news advertising.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft Explores Cursor Acquisition but Holds Off on Bid

- Acquisition Interest: Microsoft recently considered acquiring AI coding startup Cursor for $60 billion but ultimately did not make an offer, indicating competitive pressure in the rapidly evolving AI tools market.

- Market Competition: Despite GitHub Copilot gaining 4.7 million paying subscribers, a 75% increase year-over-year, Cursor and its rivals Anthropic and OpenAI continue to dominate the market, highlighting Microsoft's insufficient investment in the AI sector.

- SpaceX Acquisition: SpaceX announced it has secured the right to acquire Cursor for $60 billion, with a $10 billion penalty if the deal does not close, reflecting Elon Musk's strong interest and investment intentions in the AI space.

- Financing Dynamics: Cursor was valued at $50 billion during its fundraising process, underscoring the strong demand for tools that facilitate rapid website and application development, while also indicating ongoing investor interest in the AI sector.

See More

France Selects Scaleway to Host Health Data Hub, Replacing Microsoft

- Provider Transition: The French government has opted to replace Microsoft Azure with domestic cloud provider Scaleway for hosting the Health Data Hub, a decision that not only addresses concerns over data sovereignty but also enhances the market position of local enterprises.

- Contract Value and Market Impact: The signing of this contract signifies Scaleway's further expansion in the European market, particularly following its acquisition of a €180 million ($210 million) cloud services contract in April, showcasing its growth potential in a competitive cloud computing landscape.

- Legal and Compliance Context: With the passage of a new law in 2024 mandating that sensitive data be hosted on sovereign-guaranteed infrastructure, Scaleway's selection aligns with this legal requirement, ensuring the security of health records for French citizens.

- Technical Evaluation and Capability: Scaleway emerged as the chosen host after being evaluated against over 350 technical criteria, taking on the critical responsibility of safeguarding health records for tens of millions of French citizens, thereby reinforcing its technical strength and credibility in the cloud computing sector.

See More

Tesla Increases Investment in Self-Driving Technology

- Significant Capex Increase: Tesla has raised its 2026 capital expenditure plan to over $25 billion, nearly tripling last year's $8.53 billion, reflecting the company's ambition in self-driving technology and robotics, yet raising concerns about its profitability.

- Negative Cash Flow Outlook: Despite posting a surprise $1.44 billion cash flow surplus in Q1, Tesla expects to face negative cash flow for the remainder of the year, which could impact its stock performance and investor confidence.

- Competitive Market Pressure: Unlike tech giants like Alphabet, Microsoft, and Amazon, Tesla lacks stable cash flow from high-margin businesses, making its large-scale investments riskier, especially in areas still under development.

- Robotaxi Business Prospects: Tesla's robotaxi service is gradually expanding across select U.S. cities, but is not expected to generate meaningful revenue before 2027, leading to investor skepticism regarding its long-term profitability.

See More

IBM Shares Drop Amid Inflation and Geopolitical Concerns

- Strong Earnings but Cautious Outlook: IBM's quarterly results exceeded revenue and earnings expectations; however, the stock fell over 7% pre-market due to cautious full-year guidance, with CEO Arvind Krishna attributing this to broader geopolitical uncertainties, indicating market concerns about future performance.

- Inflation's Impact on Client Spending: Krishna highlighted that inflation could lead to reduced consumer spending at clients like Walmart, indirectly affecting IBM's business activity, reflecting the potential threats economic conditions pose to tech companies.

- Dual Impact of AI Tools: IBM's consulting business faces threats from more sophisticated AI tools, although TMF's CIO Andy Cross noted that mainframes remain essential infrastructure for complex computing systems, suggesting that AI's impact on the industry is multifaceted.

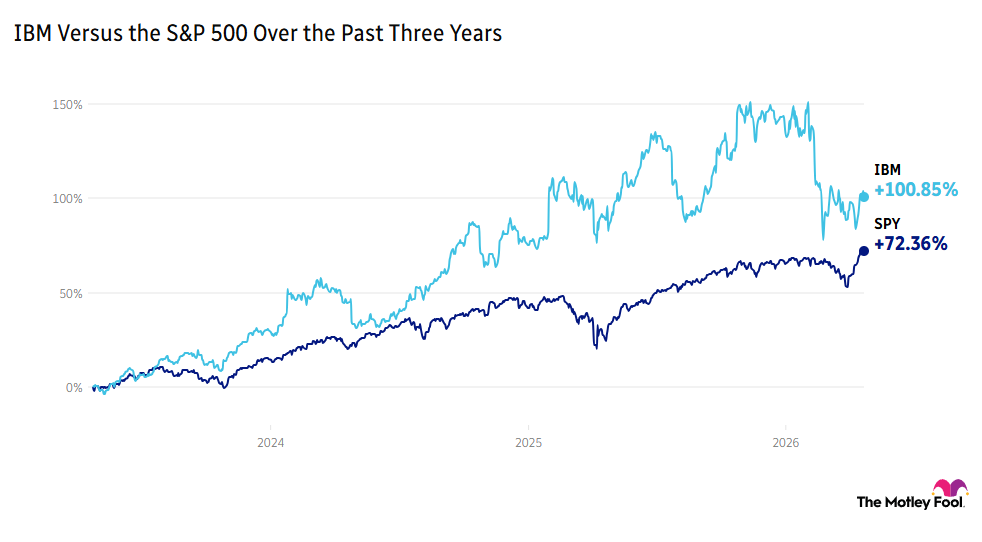

- Long-term Performance vs. Market Comparison: While IBM has risen 85% over the past five years, outperforming the S&P 500's 70% increase, the stock is down 15% this year, including its worst single-day drop in over 25 years, indicating that advancements in AI may be fundamentally altering the investment case.

See More

SpaceX and Others Set to Launch Historic IPOs Amid Unprecedented Losses

- IPO Market Outlook: SpaceX, OpenAI, and Anthropic are projected to create a combined market value of $3 trillion, despite all three being unprofitable, which is unprecedented in U.S. IPO history and could significantly impact investor confidence in high-growth tech stocks.

- Profitability Challenges: SpaceX reported a nearly $5 billion loss on over $18.6 billion in revenue last year, highlighting severe profitability challenges, while OpenAI and Anthropic are also preparing for IPOs without profitability, potentially affecting investor decisions.

- Concentration Risk: The planned IPOs of these three companies may exacerbate market concentration risks, especially given that the so-called Magnificent Seven already account for about one-third of the S&P 500 index weight, leading to potential over-reliance on tech stocks by investors.

- Profitability Threshold Impact: According to S&P Dow Jones Indices, companies must achieve four consecutive quarters of profit to be considered for inclusion in the S&P 500, meaning SpaceX, OpenAI, and Anthropic may face years without structural buying support, impacting their long-term stock performance.

See More

Software Stocks Decline Amid AI Disruption Fears

- IBM Performance Decline: International Business Machines (IBM) reported a slowdown in its software business growth to 11.3% in Q1, resulting in a 7.4% drop in share price, indicating increasing market pressure from AI-driven disruptions that are shaking investor confidence.

- ServiceNow Revenue Hit: ServiceNow flagged subscription revenue impacts due to delays in Middle Eastern deals in Q1; despite exceeding analyst expectations for overall revenue and profit, the results failed to alleviate market concerns about the software sector's challenges.

- Market Reaction: In premarket trading, shares of major software companies like Microsoft, Adobe, and CrowdStrike fell, reflecting investor anxiety over the potential long-term impacts of AI technologies, contributing to a more than 13% decline in the overall software and services index.

- Chip Stocks Surge: In stark contrast to software stocks, analog chipmaker Texas Instruments saw an 11.7% increase in share price, highlighting the positive effects of the AI boom on the chip industry, which further intensifies market focus on the divergence between software and hardware sectors.

See More

Microsoft Explores Cursor Acquisition but Holds Off on Bid

- Acquisition Interest: Microsoft recently considered acquiring AI coding startup Cursor for $60 billion but ultimately did not make an offer, indicating competitive pressure in the rapidly evolving AI tools market.

- Market Competition: Despite GitHub Copilot gaining 4.7 million paying subscribers, a 75% increase year-over-year, Cursor and its rivals Anthropic and OpenAI continue to dominate the market, highlighting Microsoft's insufficient investment in the AI sector.

- SpaceX Acquisition: SpaceX announced it has secured the right to acquire Cursor for $60 billion, with a $10 billion penalty if the deal does not close, reflecting Elon Musk's strong interest and investment intentions in the AI space.

- Financing Dynamics: Cursor was valued at $50 billion during its fundraising process, underscoring the strong demand for tools that facilitate rapid website and application development, while also indicating ongoing investor interest in the AI sector.

See More

France Selects Scaleway to Host Health Data Hub, Replacing Microsoft

- Provider Transition: The French government has opted to replace Microsoft Azure with domestic cloud provider Scaleway for hosting the Health Data Hub, a decision that not only addresses concerns over data sovereignty but also enhances the market position of local enterprises.

- Contract Value and Market Impact: The signing of this contract signifies Scaleway's further expansion in the European market, particularly following its acquisition of a €180 million ($210 million) cloud services contract in April, showcasing its growth potential in a competitive cloud computing landscape.

- Legal and Compliance Context: With the passage of a new law in 2024 mandating that sensitive data be hosted on sovereign-guaranteed infrastructure, Scaleway's selection aligns with this legal requirement, ensuring the security of health records for French citizens.

- Technical Evaluation and Capability: Scaleway emerged as the chosen host after being evaluated against over 350 technical criteria, taking on the critical responsibility of safeguarding health records for tens of millions of French citizens, thereby reinforcing its technical strength and credibility in the cloud computing sector.

See More

Tesla Increases Investment in Self-Driving Technology

- Significant Capex Increase: Tesla has raised its 2026 capital expenditure plan to over $25 billion, nearly tripling last year's $8.53 billion, reflecting the company's ambition in self-driving technology and robotics, yet raising concerns about its profitability.

- Negative Cash Flow Outlook: Despite posting a surprise $1.44 billion cash flow surplus in Q1, Tesla expects to face negative cash flow for the remainder of the year, which could impact its stock performance and investor confidence.

- Competitive Market Pressure: Unlike tech giants like Alphabet, Microsoft, and Amazon, Tesla lacks stable cash flow from high-margin businesses, making its large-scale investments riskier, especially in areas still under development.

- Robotaxi Business Prospects: Tesla's robotaxi service is gradually expanding across select U.S. cities, but is not expected to generate meaningful revenue before 2027, leading to investor skepticism regarding its long-term profitability.

See More

IBM Shares Drop Amid Inflation and Geopolitical Concerns

- Strong Earnings but Cautious Outlook: IBM's quarterly results exceeded revenue and earnings expectations; however, the stock fell over 7% pre-market due to cautious full-year guidance, with CEO Arvind Krishna attributing this to broader geopolitical uncertainties, indicating market concerns about future performance.

- Inflation's Impact on Client Spending: Krishna highlighted that inflation could lead to reduced consumer spending at clients like Walmart, indirectly affecting IBM's business activity, reflecting the potential threats economic conditions pose to tech companies.

- Dual Impact of AI Tools: IBM's consulting business faces threats from more sophisticated AI tools, although TMF's CIO Andy Cross noted that mainframes remain essential infrastructure for complex computing systems, suggesting that AI's impact on the industry is multifaceted.

- Long-term Performance vs. Market Comparison: While IBM has risen 85% over the past five years, outperforming the S&P 500's 70% increase, the stock is down 15% this year, including its worst single-day drop in over 25 years, indicating that advancements in AI may be fundamentally altering the investment case.

See More

SpaceX and Others Set to Launch Historic IPOs Amid Unprecedented Losses

- IPO Market Outlook: SpaceX, OpenAI, and Anthropic are projected to create a combined market value of $3 trillion, despite all three being unprofitable, which is unprecedented in U.S. IPO history and could significantly impact investor confidence in high-growth tech stocks.

- Profitability Challenges: SpaceX reported a nearly $5 billion loss on over $18.6 billion in revenue last year, highlighting severe profitability challenges, while OpenAI and Anthropic are also preparing for IPOs without profitability, potentially affecting investor decisions.

- Concentration Risk: The planned IPOs of these three companies may exacerbate market concentration risks, especially given that the so-called Magnificent Seven already account for about one-third of the S&P 500 index weight, leading to potential over-reliance on tech stocks by investors.

- Profitability Threshold Impact: According to S&P Dow Jones Indices, companies must achieve four consecutive quarters of profit to be considered for inclusion in the S&P 500, meaning SpaceX, OpenAI, and Anthropic may face years without structural buying support, impacting their long-term stock performance.

See More

Software Stocks Decline Amid AI Disruption Fears

- IBM Performance Decline: International Business Machines (IBM) reported a slowdown in its software business growth to 11.3% in Q1, resulting in a 7.4% drop in share price, indicating increasing market pressure from AI-driven disruptions that are shaking investor confidence.

- ServiceNow Revenue Hit: ServiceNow flagged subscription revenue impacts due to delays in Middle Eastern deals in Q1; despite exceeding analyst expectations for overall revenue and profit, the results failed to alleviate market concerns about the software sector's challenges.

- Market Reaction: In premarket trading, shares of major software companies like Microsoft, Adobe, and CrowdStrike fell, reflecting investor anxiety over the potential long-term impacts of AI technologies, contributing to a more than 13% decline in the overall software and services index.

- Chip Stocks Surge: In stark contrast to software stocks, analog chipmaker Texas Instruments saw an 11.7% increase in share price, highlighting the positive effects of the AI boom on the chip industry, which further intensifies market focus on the divergence between software and hardware sectors.

See More