Alphabet: A Resilient Stock for Market Crashes

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy GOOG?

Source: Fool

- Market Share Advantage: Alphabet's Google Search platform boasts a 91% global market share, leveraging strong network effects and economies of scale to maintain advertising revenue stability during economic downturns, making it a focal point for investors.

- Diversified Revenue Sources: Beyond search advertising, Alphabet owns premium digital advertising assets like YouTube, Android, and Chrome, while also leading in cloud computing, particularly as AI drives significant increases in computing capacity, enhancing the company's growth potential.

- Financial Resilience: Alphabet's core advertising business generates tens of billions in cash flow annually, while its emerging segments, such as AI and other innovative projects, provide additional growth opportunities, creating a balance that allows for flexible responses during economic fluctuations.

- Potential Risk Warning: Despite being one of the top companies globally, Alphabet faces challenges, particularly from the rise of AI which could disrupt the digital advertising industry, and with advertising accounting for 72% of its total revenue in Q4 2025, it may experience slower growth during economic downturns.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GOOG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GOOG

Wall Street analysts forecast GOOG stock price to rise

15 Analyst Rating

14 Buy

1 Hold

0 Sell

Strong Buy

Current: 316.370

Low

255.00

Averages

336.08

High

400.00

Current: 316.370

Low

255.00

Averages

336.08

High

400.00

About GOOG

Alphabet Inc. is a holding company. The Company's segments include Google Services, Google Cloud, and Other Bets. The Google Services segment includes products and services such as ads, Android, Chrome, devices, Google Maps, Google Play, Search, and YouTube. The Google Cloud segment includes infrastructure and platform services, collaboration tools, and other services for enterprise customers. Its Other Bets segment is engaged in the sale of healthcare-related services and Internet services. Its Google Cloud provides enterprise-ready cloud services, including Google Cloud Platform and Google Workspace. Google Cloud Platform provides access to solutions such as artificial intelligence (AI) offerings, including its AI infrastructure, Vertex AI platform, and Gemini for Google Cloud; cybersecurity, and data and analytics. Google Workspace includes cloud-based communication and collaboration tools for enterprises, such as Calendar, Gmail, Docs, Drive, and Meet.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

MegazoneCloud Achieves Profitability Turnaround with $1.16B Revenue in 2025

- Significant Revenue Growth: MegazoneCloud achieved $1.16 billion in revenue for 2025, reflecting a 27.9% year-over-year increase, which underscores the strong market demand for digital transformation and the company's ability to expand its business in the cloud computing sector.

- Improved Profitability: The company reported a net profit of $5.4 million and an adjusted EBITDA of $13.8 million, indicating enhanced profit structure and operational efficiency, thereby laying a solid foundation for future investments and expansion.

- New Business Expansion: Revenue from AI and security segments exceeded $292.2 million and $46.5 million, respectively, demonstrating MegazoneCloud's robust growth potential in emerging technologies, while partnerships with NVIDIA and Dell strengthened its domestic AI infrastructure capabilities.

- Capital Operation Plans: The company plans to leverage approximately $398.5 million in available funds to further advance the implementation of its Agentic AI system, aiming for a threefold revenue increase and a 15% operating margin by 2030, showcasing confidence in future market strategies.

See More

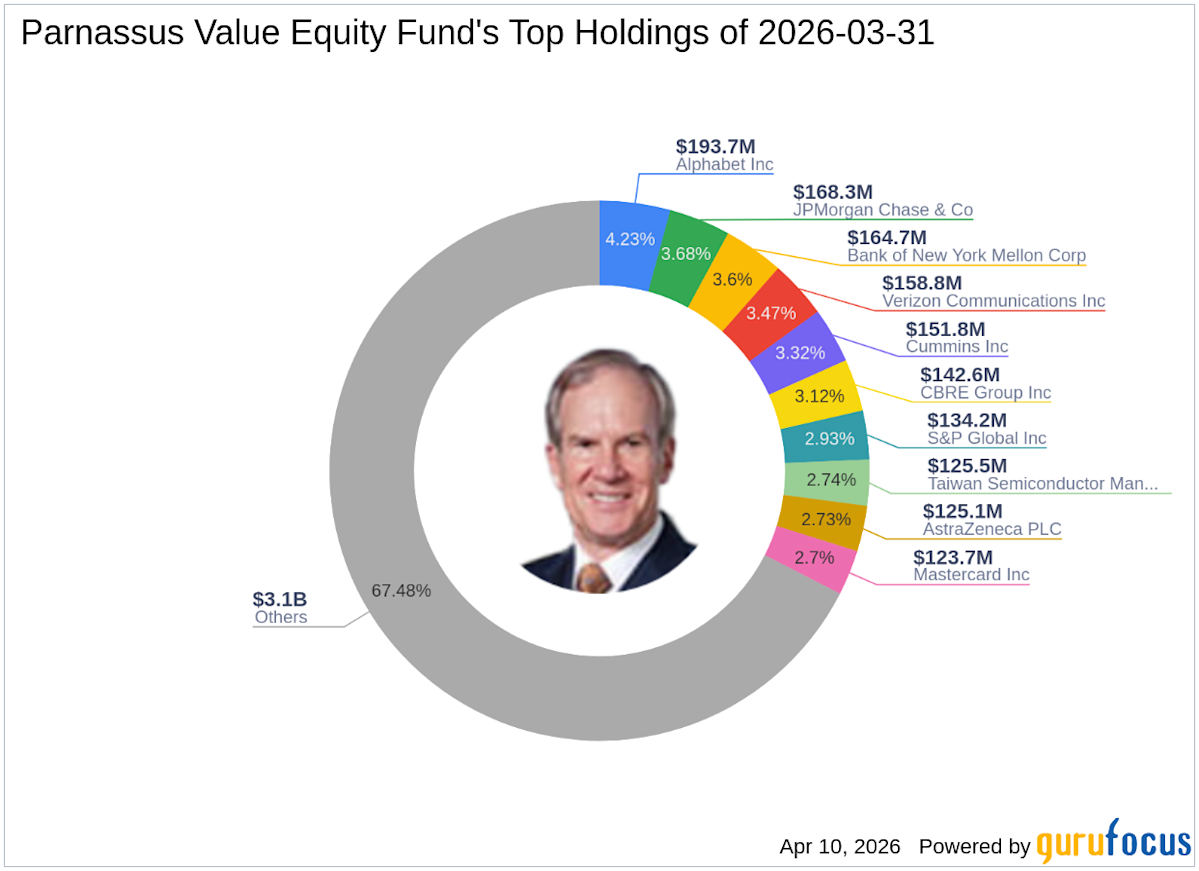

Parnassus Value Equity Fund's Q1 2026 Strategic Investment Moves

- New Investment Highlights: In Q1 2026, Parnassus Value Equity Fund added 634,492 shares of AstraZeneca (NYSE:AZN), representing 2.73% of the portfolio with a total value of $125.13 million, indicating confidence in the biopharmaceutical sector.

- Key Stock Increases: The fund increased its stake in JPMorgan Chase & Co by 72,858 shares, a 14.59% rise, bringing total holdings to 572,217 shares, reflecting optimism in the financial services industry with a current total value of $168.32 million.

- Strategic Reductions: The fund completely exited its position in AstraZeneca by selling 1,227,628 shares, resulting in a -2.37% impact on the portfolio, showcasing its agility in responding to market dynamics.

- Industry Concentration Analysis: As of Q1 2026, the fund's portfolio included 45 stocks, primarily concentrated in 10 industries such as Financial Services, Technology, and Healthcare, indicating a strategic approach to diversified investments.

See More

Alphabet: A Resilient Stock for Market Crashes

- Market Share Advantage: Alphabet's Google Search platform boasts a 91% global market share, leveraging strong network effects and economies of scale to maintain advertising revenue stability during economic downturns, making it a focal point for investors.

- Diversified Revenue Sources: Beyond search advertising, Alphabet owns premium digital advertising assets like YouTube, Android, and Chrome, while also leading in cloud computing, particularly as AI drives significant increases in computing capacity, enhancing the company's growth potential.

- Financial Resilience: Alphabet's core advertising business generates tens of billions in cash flow annually, while its emerging segments, such as AI and other innovative projects, provide additional growth opportunities, creating a balance that allows for flexible responses during economic fluctuations.

- Potential Risk Warning: Despite being one of the top companies globally, Alphabet faces challenges, particularly from the rise of AI which could disrupt the digital advertising industry, and with advertising accounting for 72% of its total revenue in Q4 2025, it may experience slower growth during economic downturns.

See More

Alphabet Demonstrates Resilient Business Model Amid Market Risks

- Market Share Advantage: Alphabet's Google Search platform commands a 91% global market share, leveraging significant network effects and economies of scale to maintain strong cash flow from advertising, despite risks posed by economic fluctuations.

- Diversified Revenue Streams: Beyond search advertising, Alphabet owns digital advertising assets like YouTube, Android, and Chrome, and is a leader in cloud computing, particularly as AI drives a surge in computing capacity, showcasing a blend of stability and growth.

- Advertising Dependency Risk: Despite efforts to diversify, advertising accounted for 72% of Alphabet's revenue in Q4 2025, exposing the company to risks of slower growth during economic downturns, particularly given the volatility in the digital advertising market.

- Market Watch Opportunity: While Alphabet may not be the most exciting stock during market downturns, its robust business model provides comfort to investors in uncertain times, making it a potential candidate for watch lists.

See More

Investment Opportunities in Quantum Computing

- IonQ's Leadership: IonQ (IONQ) has achieved a remarkable 99.99% accuracy with its record-holding quantum computing system, positioning itself to scale to millions of qubits by 2030, which could lead to significant market dominance in critical applications.

- Investments by Alphabet and Microsoft: While Alphabet (GOOGL) and Microsoft (MSFT) may not be as flashy in their quantum computing endeavors, they are heavily investing and making breakthroughs, notably Google's algorithm that could break current blockchain encryption by 2029, highlighting the rapid advancement of quantum technology.

- Massive Market Potential: The swift evolution of quantum computing is likely to have profound implications for sectors like cybersecurity and AI, particularly where traditional computers struggle with complex variables, making quantum computing a vital new solution.

- Strategic Investment Approach: By combining IonQ's innovations with the financial strength of Alphabet and Microsoft, investors should maintain exposure to these three stocks to capitalize on significant returns as quantum computing technology matures.

See More

IonQ Sets World Record for Quantum Computing Accuracy

- Quantum Accuracy Breakthrough: IonQ's quantum computing system achieved a fidelity of 99.99% in standard tests, marking a significant advancement in quantum technology that could accelerate its adoption across various applications, thereby enhancing the company's competitive edge in the market.

- Future Development Plans: IonQ aims to scale its technology to millions of qubits by 2030, with a 256-qubit system set to launch this year; if successful, this strategic goal could position IonQ as a leader in quantum computing, particularly in applications requiring high precision.

- Investment from Industry Giants: While Alphabet and Microsoft have been relatively quiet about their quantum advancements, both are heavily investing in the technology, with Alphabet recently announcing an algorithm capable of breaking current blockchain encryption by 2029, highlighting the rapid development of quantum computing and its potential implications for cybersecurity.

- Market Outlook Analysis: As quantum computing technology matures, it is expected to have profound impacts on cloud computing and chemistry, with Microsoft's Marjorana 1 quantum computer already showing promise in drug discovery, further accelerating the growth of cloud computing in the industry.

See More

MegazoneCloud Achieves Profitability Turnaround with $1.16B Revenue in 2025

- Significant Revenue Growth: MegazoneCloud achieved $1.16 billion in revenue for 2025, reflecting a 27.9% year-over-year increase, which underscores the strong market demand for digital transformation and the company's ability to expand its business in the cloud computing sector.

- Improved Profitability: The company reported a net profit of $5.4 million and an adjusted EBITDA of $13.8 million, indicating enhanced profit structure and operational efficiency, thereby laying a solid foundation for future investments and expansion.

- New Business Expansion: Revenue from AI and security segments exceeded $292.2 million and $46.5 million, respectively, demonstrating MegazoneCloud's robust growth potential in emerging technologies, while partnerships with NVIDIA and Dell strengthened its domestic AI infrastructure capabilities.

- Capital Operation Plans: The company plans to leverage approximately $398.5 million in available funds to further advance the implementation of its Agentic AI system, aiming for a threefold revenue increase and a 15% operating margin by 2030, showcasing confidence in future market strategies.

See More

Parnassus Value Equity Fund's Q1 2026 Strategic Investment Moves

- New Investment Highlights: In Q1 2026, Parnassus Value Equity Fund added 634,492 shares of AstraZeneca (NYSE:AZN), representing 2.73% of the portfolio with a total value of $125.13 million, indicating confidence in the biopharmaceutical sector.

- Key Stock Increases: The fund increased its stake in JPMorgan Chase & Co by 72,858 shares, a 14.59% rise, bringing total holdings to 572,217 shares, reflecting optimism in the financial services industry with a current total value of $168.32 million.

- Strategic Reductions: The fund completely exited its position in AstraZeneca by selling 1,227,628 shares, resulting in a -2.37% impact on the portfolio, showcasing its agility in responding to market dynamics.

- Industry Concentration Analysis: As of Q1 2026, the fund's portfolio included 45 stocks, primarily concentrated in 10 industries such as Financial Services, Technology, and Healthcare, indicating a strategic approach to diversified investments.

See More

Alphabet: A Resilient Stock for Market Crashes

- Market Share Advantage: Alphabet's Google Search platform boasts a 91% global market share, leveraging strong network effects and economies of scale to maintain advertising revenue stability during economic downturns, making it a focal point for investors.

- Diversified Revenue Sources: Beyond search advertising, Alphabet owns premium digital advertising assets like YouTube, Android, and Chrome, while also leading in cloud computing, particularly as AI drives significant increases in computing capacity, enhancing the company's growth potential.

- Financial Resilience: Alphabet's core advertising business generates tens of billions in cash flow annually, while its emerging segments, such as AI and other innovative projects, provide additional growth opportunities, creating a balance that allows for flexible responses during economic fluctuations.

- Potential Risk Warning: Despite being one of the top companies globally, Alphabet faces challenges, particularly from the rise of AI which could disrupt the digital advertising industry, and with advertising accounting for 72% of its total revenue in Q4 2025, it may experience slower growth during economic downturns.

See More

Alphabet Demonstrates Resilient Business Model Amid Market Risks

- Market Share Advantage: Alphabet's Google Search platform commands a 91% global market share, leveraging significant network effects and economies of scale to maintain strong cash flow from advertising, despite risks posed by economic fluctuations.

- Diversified Revenue Streams: Beyond search advertising, Alphabet owns digital advertising assets like YouTube, Android, and Chrome, and is a leader in cloud computing, particularly as AI drives a surge in computing capacity, showcasing a blend of stability and growth.

- Advertising Dependency Risk: Despite efforts to diversify, advertising accounted for 72% of Alphabet's revenue in Q4 2025, exposing the company to risks of slower growth during economic downturns, particularly given the volatility in the digital advertising market.

- Market Watch Opportunity: While Alphabet may not be the most exciting stock during market downturns, its robust business model provides comfort to investors in uncertain times, making it a potential candidate for watch lists.

See More

Investment Opportunities in Quantum Computing

- IonQ's Leadership: IonQ (IONQ) has achieved a remarkable 99.99% accuracy with its record-holding quantum computing system, positioning itself to scale to millions of qubits by 2030, which could lead to significant market dominance in critical applications.

- Investments by Alphabet and Microsoft: While Alphabet (GOOGL) and Microsoft (MSFT) may not be as flashy in their quantum computing endeavors, they are heavily investing and making breakthroughs, notably Google's algorithm that could break current blockchain encryption by 2029, highlighting the rapid advancement of quantum technology.

- Massive Market Potential: The swift evolution of quantum computing is likely to have profound implications for sectors like cybersecurity and AI, particularly where traditional computers struggle with complex variables, making quantum computing a vital new solution.

- Strategic Investment Approach: By combining IonQ's innovations with the financial strength of Alphabet and Microsoft, investors should maintain exposure to these three stocks to capitalize on significant returns as quantum computing technology matures.

See More

IonQ Sets World Record for Quantum Computing Accuracy

- Quantum Accuracy Breakthrough: IonQ's quantum computing system achieved a fidelity of 99.99% in standard tests, marking a significant advancement in quantum technology that could accelerate its adoption across various applications, thereby enhancing the company's competitive edge in the market.

- Future Development Plans: IonQ aims to scale its technology to millions of qubits by 2030, with a 256-qubit system set to launch this year; if successful, this strategic goal could position IonQ as a leader in quantum computing, particularly in applications requiring high precision.

- Investment from Industry Giants: While Alphabet and Microsoft have been relatively quiet about their quantum advancements, both are heavily investing in the technology, with Alphabet recently announcing an algorithm capable of breaking current blockchain encryption by 2029, highlighting the rapid development of quantum computing and its potential implications for cybersecurity.

- Market Outlook Analysis: As quantum computing technology matures, it is expected to have profound impacts on cloud computing and chemistry, with Microsoft's Marjorana 1 quantum computer already showing promise in drug discovery, further accelerating the growth of cloud computing in the industry.

See More