Broadcom Expands AI Infrastructure Amid Strong Revenue Growth

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 30 2026

0mins

Should l Buy AVGO?

Source: Fool

Broadcom Inc (AVGO) saw its stock rise by 5.00% as it crossed above the 5-day SMA, reflecting positive market conditions. The company announced a significant expansion of its AI infrastructure portfolio, positioning itself for the upcoming 200T AI era. This strategic move comes as Broadcom's AI revenue surged to over $8.4 billion in Q1 2023, more than doubling year-over-year, with expectations to reach $10.7 billion in Q2, showcasing robust market demand.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AVGO?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AVGO

Wall Street analysts forecast AVGO stock price to rise

30 Analyst Rating

29 Buy

1 Hold

0 Sell

Strong Buy

Current: 398.470

Low

370.00

Averages

457.75

High

525.00

Current: 398.470

Low

370.00

Averages

457.75

High

525.00

About AVGO

Broadcom Inc. is a global technology firm that designs, develops, and supplies a range of semiconductors, enterprise software and security solutions. The Company operates through two segments: semiconductor solutions and infrastructure software. Its semiconductor solutions segment includes all of its product lines and intellectual property (IP) licensing. It provides a variety of radio frequency semiconductor devices, wireless connectivity solutions, custom touch controllers, and inductive charging solutions for mobile applications. Its infrastructure software segment includes its private and hybrid cloud, application development and delivery, software-defined edge, application networking and security, mainframe, distributed and cybersecurity solutions, and its FC SAN business. It provides a portfolio of software solutions that enable customers to plan, develop, automate, manage and secure applications across mainframe, distributed, mobile and cloud platforms.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Investment Opportunities in Tech Stocks Amidst Sector Disappointment

- Palantir Financial Performance: Palantir Technologies reported a 66% year-over-year increase in U.S. government revenue to $570 million in Q4 2025, while U.S. commercial revenue surged 137% to $507 million, highlighting the strong market demand driven by its powerful data analytics and AI technologies.

- Nebius Growth Potential: Nebius Group's stock has risen 96% this year, with plans to expand its data centers from seven to sixteen, and projected annual revenue is expected to jump from $529.8 million in 2025 to $3.3 billion, showcasing its critical role in expanding AI computing capacity.

- Broadcom Partnership Agreement: Broadcom signed a deal with Alphabet to provide custom AI hardware for Google's tensor processing units (TPUs), which will enhance its market share in a competitive landscape and is expected to drive further stock price increases.

- Market Rebound Opportunity: Despite the overall underperformance of tech stocks, investors can capitalize on current low prices to increase positions, particularly in companies like Palantir and Broadcom, which are anticipated to deliver significant returns in the coming months.

See More

Analysis of SpaceX IPO Prospects and Investment Recommendations

- Valuation and Fundraising Goals: SpaceX aims for a $1.75 trillion valuation in its IPO, seeking to raise $75 billion, which would position it as the eighth most valuable company globally; however, such a high valuation necessitates substantial profits to justify it.

- Revenue and Profit Data: Reports indicate that SpaceX generated $15 billion to $16 billion in revenue in 2022, with around $8 billion in profit, and projections suggest that by 2026, its rocket launch and Starlink businesses could yield approximately $20 billion in revenue, highlighting its strong market potential.

- Market Risk Warning: While SpaceX's IPO may initially attract investors, a price-to-sales ratio of 87 suggests excessive optimism about future growth, as historically similar IPOs often surge initially before declining, posing risks for retail investors.

- Alternative Investment Options: For those interested in space exploration investments, it is advisable to consider space-themed exchange-traded funds (ETFs) like the Ark Space and Invesco Aerospace & Defense ETF, which mitigate risk through diversified holdings while outperforming the S&P 500.

See More

SpaceX Files for IPO, Eyeing $1.75 Trillion Valuation

- IPO Plans and Valuation: SpaceX has confidentially filed for an IPO aiming for a staggering $1.75 trillion valuation and plans to raise $75 billion, which would position it as the eighth most valuable company globally, though such a high valuation necessitates substantial profits to justify.

- Revenue Sources and Clients: Beyond theoretical space travel, SpaceX collaborates with the U.S. Defense Department and NASA, with projections indicating that its rocket launch and Starlink businesses could generate around $20 billion in revenue by 2026, highlighting strong market demand and profit potential.

- Market Risks and Investment Advice: Despite the excitement surrounding SpaceX's IPO, the astronomical price-to-sales ratio of 87 suggests an overly optimistic market outlook, leading to potential short-term volatility, thus advising investors to consider space-themed ETFs as a safer investment alternative.

- Competition and Alternative Investments: Various space-themed ETFs, such as Ark Space and Invesco Aerospace & Defense ETF, offer diversified exposure to the sector and have outperformed the S&P 500, providing a more stable investment option amidst the speculative nature of SpaceX's IPO.

See More

Broadcom and AMD: Competition and Collaboration

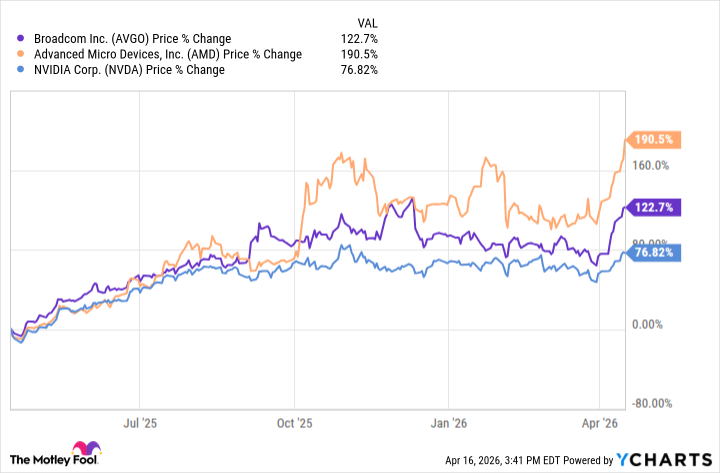

- Revenue Growth Comparison: Broadcom achieved a 28% year-over-year revenue growth in Q4 2025, while AMD reported a 34% increase during the same period, indicating AMD's superior growth despite Broadcom's better profit margins, showcasing the competitive dynamics between the two companies.

- Margin Discrepancy: Broadcom's net profit margin stood at 47.3% in Q4 2025, compared to AMD's 14.7%, highlighting Broadcom's stronger revenue retention capabilities; however, if AMD can improve its margins, it could see significant profit increases.

- Deepening Strategic Partnerships: AMD's collaboration with Meta Platforms to deploy 6 gigawatts of GPUs is expected to yield

See More

AI Chip Market Outlook Remains Positive

- Market Growth Potential: Grandview Research projects a 29% compound annual growth rate for the AI chip industry from 2024 to 2030, indicating that AI chip stocks still have upside potential, attracting investor interest.

- Deepening Partnerships: AMD's collaboration with Meta Platforms to deploy 6 gigawatts of GPUs is expected to yield 'substantial multiyear revenue growth', while Broadcom has also expanded its partnerships with Meta and Alphabet to supply custom AI chips, further solidifying its market position.

- Financial Performance Comparison: In Q4 of fiscal year 2025, Broadcom achieved a 28% year-over-year revenue growth, while AMD led with a 34% growth, showcasing a competitive landscape in revenue growth between the two companies.

- Margin Discrepancies: Although AMD outperforms in revenue growth, Broadcom's net profit margin reached 47.3% in Q4 2025, significantly higher than AMD's 14.7%, giving Broadcom a clear advantage in profitability.

See More

Intensifying Competition in AI Chip Market

- Market Growth Potential: Grandview Research projects a 29% compound annual growth rate for the AI chip industry from 2024 to 2030, indicating significant upside potential that attracts investor interest in related stocks.

- Deepening Partnerships: AMD has partnered with Meta Platforms to deploy 6 gigawatts of AMD GPUs, which is expected to yield “substantial multiyear revenue growth,” showcasing its competitive edge in a high-demand market.

- Financial Performance Comparison: In Q4 of fiscal year 2025, Broadcom achieved a 28% year-over-year revenue growth, while AMD led with a 34% growth, suggesting AMD's stronger performance in revenue growth may attract more investors.

- Margin Discrepancies: Although Broadcom excels in profit margins with a net profit margin of 47.3% in Q4 2025 compared to AMD's 14.7%, AMD has greater room for margin improvement, which could lead to significant profit growth if realized.

See More

Investment Opportunities in Tech Stocks Amidst Sector Disappointment

- Palantir Financial Performance: Palantir Technologies reported a 66% year-over-year increase in U.S. government revenue to $570 million in Q4 2025, while U.S. commercial revenue surged 137% to $507 million, highlighting the strong market demand driven by its powerful data analytics and AI technologies.

- Nebius Growth Potential: Nebius Group's stock has risen 96% this year, with plans to expand its data centers from seven to sixteen, and projected annual revenue is expected to jump from $529.8 million in 2025 to $3.3 billion, showcasing its critical role in expanding AI computing capacity.

- Broadcom Partnership Agreement: Broadcom signed a deal with Alphabet to provide custom AI hardware for Google's tensor processing units (TPUs), which will enhance its market share in a competitive landscape and is expected to drive further stock price increases.

- Market Rebound Opportunity: Despite the overall underperformance of tech stocks, investors can capitalize on current low prices to increase positions, particularly in companies like Palantir and Broadcom, which are anticipated to deliver significant returns in the coming months.

See More

Analysis of SpaceX IPO Prospects and Investment Recommendations

- Valuation and Fundraising Goals: SpaceX aims for a $1.75 trillion valuation in its IPO, seeking to raise $75 billion, which would position it as the eighth most valuable company globally; however, such a high valuation necessitates substantial profits to justify it.

- Revenue and Profit Data: Reports indicate that SpaceX generated $15 billion to $16 billion in revenue in 2022, with around $8 billion in profit, and projections suggest that by 2026, its rocket launch and Starlink businesses could yield approximately $20 billion in revenue, highlighting its strong market potential.

- Market Risk Warning: While SpaceX's IPO may initially attract investors, a price-to-sales ratio of 87 suggests excessive optimism about future growth, as historically similar IPOs often surge initially before declining, posing risks for retail investors.

- Alternative Investment Options: For those interested in space exploration investments, it is advisable to consider space-themed exchange-traded funds (ETFs) like the Ark Space and Invesco Aerospace & Defense ETF, which mitigate risk through diversified holdings while outperforming the S&P 500.

See More

SpaceX Files for IPO, Eyeing $1.75 Trillion Valuation

- IPO Plans and Valuation: SpaceX has confidentially filed for an IPO aiming for a staggering $1.75 trillion valuation and plans to raise $75 billion, which would position it as the eighth most valuable company globally, though such a high valuation necessitates substantial profits to justify.

- Revenue Sources and Clients: Beyond theoretical space travel, SpaceX collaborates with the U.S. Defense Department and NASA, with projections indicating that its rocket launch and Starlink businesses could generate around $20 billion in revenue by 2026, highlighting strong market demand and profit potential.

- Market Risks and Investment Advice: Despite the excitement surrounding SpaceX's IPO, the astronomical price-to-sales ratio of 87 suggests an overly optimistic market outlook, leading to potential short-term volatility, thus advising investors to consider space-themed ETFs as a safer investment alternative.

- Competition and Alternative Investments: Various space-themed ETFs, such as Ark Space and Invesco Aerospace & Defense ETF, offer diversified exposure to the sector and have outperformed the S&P 500, providing a more stable investment option amidst the speculative nature of SpaceX's IPO.

See More

Broadcom and AMD: Competition and Collaboration

- Revenue Growth Comparison: Broadcom achieved a 28% year-over-year revenue growth in Q4 2025, while AMD reported a 34% increase during the same period, indicating AMD's superior growth despite Broadcom's better profit margins, showcasing the competitive dynamics between the two companies.

- Margin Discrepancy: Broadcom's net profit margin stood at 47.3% in Q4 2025, compared to AMD's 14.7%, highlighting Broadcom's stronger revenue retention capabilities; however, if AMD can improve its margins, it could see significant profit increases.

- Deepening Strategic Partnerships: AMD's collaboration with Meta Platforms to deploy 6 gigawatts of GPUs is expected to yield

See More

AI Chip Market Outlook Remains Positive

- Market Growth Potential: Grandview Research projects a 29% compound annual growth rate for the AI chip industry from 2024 to 2030, indicating that AI chip stocks still have upside potential, attracting investor interest.

- Deepening Partnerships: AMD's collaboration with Meta Platforms to deploy 6 gigawatts of GPUs is expected to yield 'substantial multiyear revenue growth', while Broadcom has also expanded its partnerships with Meta and Alphabet to supply custom AI chips, further solidifying its market position.

- Financial Performance Comparison: In Q4 of fiscal year 2025, Broadcom achieved a 28% year-over-year revenue growth, while AMD led with a 34% growth, showcasing a competitive landscape in revenue growth between the two companies.

- Margin Discrepancies: Although AMD outperforms in revenue growth, Broadcom's net profit margin reached 47.3% in Q4 2025, significantly higher than AMD's 14.7%, giving Broadcom a clear advantage in profitability.

See More

Intensifying Competition in AI Chip Market

- Market Growth Potential: Grandview Research projects a 29% compound annual growth rate for the AI chip industry from 2024 to 2030, indicating significant upside potential that attracts investor interest in related stocks.

- Deepening Partnerships: AMD has partnered with Meta Platforms to deploy 6 gigawatts of AMD GPUs, which is expected to yield “substantial multiyear revenue growth,” showcasing its competitive edge in a high-demand market.

- Financial Performance Comparison: In Q4 of fiscal year 2025, Broadcom achieved a 28% year-over-year revenue growth, while AMD led with a 34% growth, suggesting AMD's stronger performance in revenue growth may attract more investors.

- Margin Discrepancies: Although Broadcom excels in profit margins with a net profit margin of 47.3% in Q4 2025 compared to AMD's 14.7%, AMD has greater room for margin improvement, which could lead to significant profit growth if realized.

See More