Ryman Hospitality Properties Q4 2025 Earnings Call Highlights

- Performance Exceeds Expectations: Ryman Hospitality Properties reported Q4 2025 results that surpassed expectations, with the Entertainment segment and AFFO per share exceeding the upper end of guidance ranges, reflecting strong holiday programming and entertainment demand, thereby reinforcing the company's competitive position in the market.

- Acquisition and Expansion: The acquisition of JW Desert Ridge allows Ryman to enter a top 10 meetings market in the U.S., creating a second rotational pattern within the JW Marriott brand, which is expected to drive future revenue growth and increase market share.

- Liquidity and Financial Health: As of the end of Q4, the company had $471 million in unrestricted cash and total liquidity nearing $1.3 billion, demonstrating robust financial health that supports future investment opportunities.

- 2026 Outlook: Management anticipates a 2.5% growth in RevPAR and nearly 10% growth in Entertainment segment EBITDAre for 2026, with planned capital expenditures of $350 million to $450 million primarily in hospitality, showcasing confidence in future growth and strategic positioning.

Trade with 70% Backtested Accuracy

Analyst Views on RHP

About RHP

About the author

Wall Street's Latest Rating Changes Analysis

- MSG Sports Upgrade: Seaport upgraded Madison Square Garden Sports from neutral to buy, citing a significant 57.5% trading discount versus intrinsic value, suggesting a potential appreciation ahead of the 2025-26 season, particularly with plans to spin off the Knicks and Rangers into standalone entities.

- ServiceNow Downgrade: UBS downgraded ServiceNow from buy to neutral due to weakened confidence in the software sector, projecting a decline in 2026 free cash flow to 15x, reflecting increased budget pressures on non-AI applications that could impact future performance.

- Shake Shack Sales Growth: Mizuho upgraded Shake Shack from neutral to outperform, anticipating upside in same-store sales for Q1, driven by strong demand and improved restaurant-level margins, indicating robust market momentum and growth potential.

- Nvidia Strong Performance: Raymond James reiterated a strong buy rating on Nvidia, based on favorable trends in its Asia supply chain, with suppliers receiving increased forecasts during the quarter, reinforcing Nvidia's position as a market leader.

RYMAN HOSPITALITY PROPERTIES INC: TRUIST SECURITIES INCREASES TARGET PRICE FROM $121 TO $129

Hospitality Properties: Truis Securities has raised the target price for hospitality properties to $129 from $121.

Market Impact: This adjustment reflects a positive outlook on the performance of the hospitality sector.

Investment Opportunities in the Live Music Industry

- Market Dominance: Live Nation sits at the center of the U.S. live music industry, serving nearly 160 million fans last year and holding an 80% market share in primary ticketing, showcasing its strong market influence and investment appeal.

- Venue Expansion: The company has tripled its global venue count to 460 since 2020, enhancing its control over the live music experience and profitability through acquisitions and new venue constructions.

- Financial Recovery: Ryman Hospitality Properties reports an adjusted funds from operations (AFFO) of $8.46 per share and a dividend of $4.65, reflecting a 23% and 29% increase from 2019, indicating strong recovery and stable cash flow post-pandemic.

- High Margin Strategy: Live Nation controls sponsorship revenues through venue ownership, with over 70% of this year's sponsorship deals already booked, projecting double-digit adjusted operating income growth by 2026, highlighting its ongoing investment and growth potential in high-margin businesses.

Live Nation and Ryman Hospitality Dominate Live Entertainment Market

- Market Share Control: Live Nation Entertainment controls approximately 80% of the primary ticketing market through Ticketmaster, serving nearly 160 million fans last year, highlighting its dominant position in the live music industry and attracting investor interest in its growth potential.

- Asset Expansion: Since 2020, Live Nation has increased its global venue count to 460, tripling its footprint, which not only enhances its market share but also strengthens its profitability in ticketing and sponsorship revenue.

- Stable Cash Flow: Ryman Hospitality Properties owns five of the top ten non-gaming convention hotels in the U.S., ensuring stable cash flow through long-term bookings from corporate and association groups; despite a pandemic-induced dividend suspension, its adjusted funds from operations (AFFO) and dividends have grown by 23% and 29% respectively since 2019.

- Future Growth Outlook: Live Nation anticipates double-digit growth in adjusted operating income by 2026, bolstered by an increase in sponsorship deals, reflecting strong confidence in the ongoing demand for live entertainment.

RYMAN HOSPITALITY PROPERTIES, INC. COMPLETES $700 MILLION OFFERING OF 5.750% SENIOR NOTES MATURING IN 2034

Company Announcement: Ryman Hospitality Properties, Inc. has announced the closing of $700 million in senior notes.

Financial Details: The senior notes have an interest rate of 5.750% and are due in 2034.

Ryman and Lakeland Executives Increase Stock Holdings

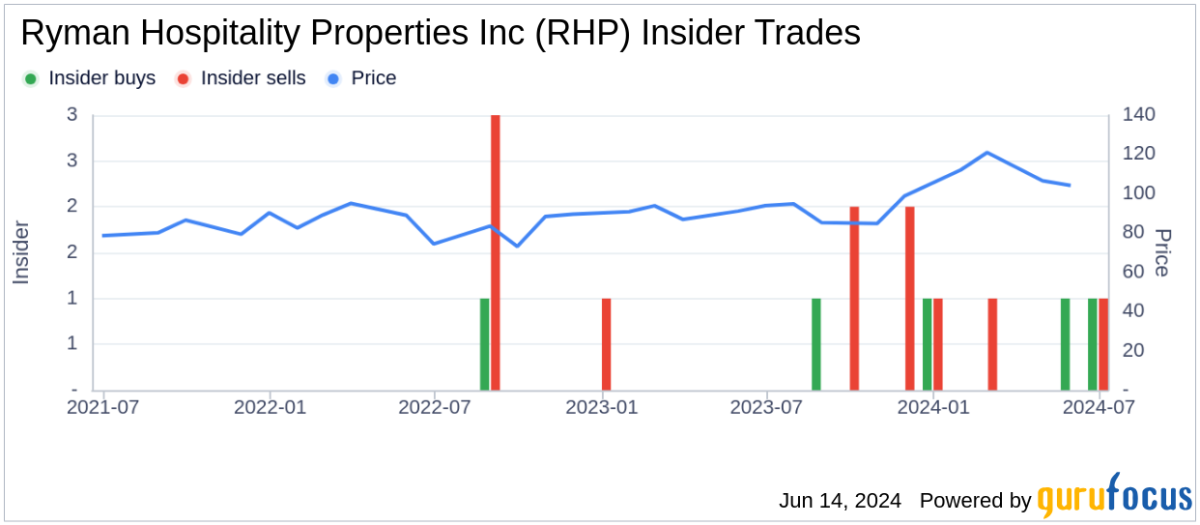

- RHP Stock Purchase: Colin V. Reed, Executive Chairman of Ryman Hospitality Properties, purchased 7,800 shares at $100.67 each on Friday, totaling $785,226, indicating strong confidence in the company's future prospects.

- Market Reaction: Despite Reed's purchase price being higher than Monday's trading low of $97.41, which is 3.2% below his purchase price, RHP's stock still rose about 0.3% on Monday, reflecting market recognition of its fundamentals.

- Welch's LKFN Purchase: M. Scott Welch, Director of Lakeland Financial, bought 10,000 shares at $57.95 each on Friday, totaling $579,500, demonstrating his optimism about the company's outlook.

- Historical Buying Activity: Prior to this latest purchase, Welch had invested a total of $920,374 in LKFN over the past year, with an average price of $61.36 per share, indicating his sustained belief in the company's long-term value.

Wall Street's Latest Rating Changes Analysis

- MSG Sports Upgrade: Seaport upgraded Madison Square Garden Sports from neutral to buy, citing a significant 57.5% trading discount versus intrinsic value, suggesting a potential appreciation ahead of the 2025-26 season, particularly with plans to spin off the Knicks and Rangers into standalone entities.

- ServiceNow Downgrade: UBS downgraded ServiceNow from buy to neutral due to weakened confidence in the software sector, projecting a decline in 2026 free cash flow to 15x, reflecting increased budget pressures on non-AI applications that could impact future performance.

- Shake Shack Sales Growth: Mizuho upgraded Shake Shack from neutral to outperform, anticipating upside in same-store sales for Q1, driven by strong demand and improved restaurant-level margins, indicating robust market momentum and growth potential.

- Nvidia Strong Performance: Raymond James reiterated a strong buy rating on Nvidia, based on favorable trends in its Asia supply chain, with suppliers receiving increased forecasts during the quarter, reinforcing Nvidia's position as a market leader.

RYMAN HOSPITALITY PROPERTIES INC: TRUIST SECURITIES INCREASES TARGET PRICE FROM $121 TO $129

Hospitality Properties: Truis Securities has raised the target price for hospitality properties to $129 from $121.

Market Impact: This adjustment reflects a positive outlook on the performance of the hospitality sector.

Investment Opportunities in the Live Music Industry

- Market Dominance: Live Nation sits at the center of the U.S. live music industry, serving nearly 160 million fans last year and holding an 80% market share in primary ticketing, showcasing its strong market influence and investment appeal.

- Venue Expansion: The company has tripled its global venue count to 460 since 2020, enhancing its control over the live music experience and profitability through acquisitions and new venue constructions.

- Financial Recovery: Ryman Hospitality Properties reports an adjusted funds from operations (AFFO) of $8.46 per share and a dividend of $4.65, reflecting a 23% and 29% increase from 2019, indicating strong recovery and stable cash flow post-pandemic.

- High Margin Strategy: Live Nation controls sponsorship revenues through venue ownership, with over 70% of this year's sponsorship deals already booked, projecting double-digit adjusted operating income growth by 2026, highlighting its ongoing investment and growth potential in high-margin businesses.

Live Nation and Ryman Hospitality Dominate Live Entertainment Market

- Market Share Control: Live Nation Entertainment controls approximately 80% of the primary ticketing market through Ticketmaster, serving nearly 160 million fans last year, highlighting its dominant position in the live music industry and attracting investor interest in its growth potential.

- Asset Expansion: Since 2020, Live Nation has increased its global venue count to 460, tripling its footprint, which not only enhances its market share but also strengthens its profitability in ticketing and sponsorship revenue.

- Stable Cash Flow: Ryman Hospitality Properties owns five of the top ten non-gaming convention hotels in the U.S., ensuring stable cash flow through long-term bookings from corporate and association groups; despite a pandemic-induced dividend suspension, its adjusted funds from operations (AFFO) and dividends have grown by 23% and 29% respectively since 2019.

- Future Growth Outlook: Live Nation anticipates double-digit growth in adjusted operating income by 2026, bolstered by an increase in sponsorship deals, reflecting strong confidence in the ongoing demand for live entertainment.

RYMAN HOSPITALITY PROPERTIES, INC. COMPLETES $700 MILLION OFFERING OF 5.750% SENIOR NOTES MATURING IN 2034

Company Announcement: Ryman Hospitality Properties, Inc. has announced the closing of $700 million in senior notes.

Financial Details: The senior notes have an interest rate of 5.750% and are due in 2034.

Ryman and Lakeland Executives Increase Stock Holdings

- RHP Stock Purchase: Colin V. Reed, Executive Chairman of Ryman Hospitality Properties, purchased 7,800 shares at $100.67 each on Friday, totaling $785,226, indicating strong confidence in the company's future prospects.

- Market Reaction: Despite Reed's purchase price being higher than Monday's trading low of $97.41, which is 3.2% below his purchase price, RHP's stock still rose about 0.3% on Monday, reflecting market recognition of its fundamentals.

- Welch's LKFN Purchase: M. Scott Welch, Director of Lakeland Financial, bought 10,000 shares at $57.95 each on Friday, totaling $579,500, demonstrating his optimism about the company's outlook.

- Historical Buying Activity: Prior to this latest purchase, Welch had invested a total of $920,374 in LKFN over the past year, with an average price of $61.36 per share, indicating his sustained belief in the company's long-term value.