Nvidia's 13F Report Reveals Investment Dynamics

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 03 2026

0mins

Should l Buy INTC?

Source: NASDAQ.COM

- Portfolio Adjustment: Nvidia's 13F report for Q4 reveals the complete sale of 1,101,249 shares of Arm Holdings and 7,716,050 shares of Applied Digital, indicating a cautious stance towards high-valuation stocks, especially as Arm's price surged since its IPO, reflecting market optimism about its future.

- Profit-Taking Strategy: With Arm Holdings' P/S ratio at 29 and Applied Digital's exceeding 23, Nvidia's sell-off not only locks in profits but also signals a reaction to perceived market overvaluation, demonstrating a more prudent approach in its investment decisions.

- Massive Intel Investment: Nvidia purchased 214,776,632 shares of Intel at $23.28 each in December, totaling a $5 billion investment, and with Intel's stock doubling since then, this move has generated significant unrealized gains for Nvidia, showcasing its strategic positioning in the semiconductor sector.

- AI Data Center Collaboration: The partnership between Nvidia and Intel aims to advance AI data centers by integrating Nvidia's GPUs with Intel's x86 processors, and if Intel successfully executes a multi-year turnaround, it could yield billions in investment income for Nvidia, further solidifying its leadership in the AI domain.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy INTC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on INTC

Wall Street analysts forecast INTC stock price to fall

29 Analyst Rating

5 Buy

19 Hold

5 Sell

Hold

Current: 43.420

Low

20.00

Averages

39.30

High

52.00

Current: 43.420

Low

20.00

Averages

39.30

High

52.00

About INTC

Intel Corporation is a global designer and manufacturer of semiconductor products. The Company operates through three segments: Intel Products, Intel Foundry, and All Other. Its Intel Products segment includes Client Computing Group (CCG), Data Center and AI (DCAI), Network and Edge (NEX). The CCG is bringing together the operating system, system architecture, hardware, and software application integration to enable PC experiences. DCAI delivers workload-optimized solutions to cloud service providers and enterprises, along with silicon devices for communications service providers, network and edge, and HPC customers. NEX helps networks and edge compute systems from fixed-function hardware to general-purpose compute, acceleration, and networking devices running cloud native software on programmable hardware. The Intel Foundry segment comprises technology development, manufacturing and foundry services. All Other segments include Altera, Mobileye, Other.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Oracle's AI Investment Faces Challenges Ahead of Earnings

- Financing Impact: Oracle's announcement of a $50 billion financing plan in early February, which includes a $5 billion convertible preferred offering and approximately $25 billion in senior notes, highlights strong demand for its data center expansion but raises concerns about the pace of dilution for shareholders.

- Collaboration with OpenAI: Although talks to expand its deal with OpenAI in Texas fell through, Oracle is still on track to deliver eight data centers to OpenAI, ensuring its competitive position in the AI cloud computing space, particularly in maintaining strong relationships with key customers.

- Market Sensitivity: The news of Oracle's $300 billion deal with OpenAI previously boosted its stock by 35% last September, but subsequent debt increases have raised investor concerns about its financial health, leading to a widening of its five-year credit default swaps, reflecting skepticism about its investment-grade credit rating.

- Cost Control Measures: Analysts speculate that Oracle may implement workforce reductions and divestitures to address financing issues, with potential layoffs of 20,000 to 30,000 employees expected to generate $8 to $10 billion in incremental free cash flow, indicating urgency in cost management.

See More

Oracle's Q3 Earnings to Test AI Trade Viability

- Financing Overview: Oracle announced a $50 billion financing plan last month to support its data center buildout, with increasing market concern over the pace of dilution for shareholders, as analysts emphasize the importance of financing cadence.

- Debt Financing Details: The latest financing measures include a $5 billion convertible preferred offering and approximately $25 billion in senior notes with varying maturities, indicating strong market demand for Oracle, although investors remain cautious about its financial health.

- Collaboration with OpenAI: Oracle's relationship with OpenAI is under scrutiny; despite failed negotiations to expand in Texas, the delivery of eight sites to OpenAI remains on schedule, which is crucial for investor confidence.

- Market Reaction and Future Outlook: The news of Oracle's $300 billion deal initially boosted its stock by 35%, but subsequent debt increases raised concerns about its financial stability, leading analysts to speculate that the company may consider layoffs and divestitures to address financing challenges.

See More

Serious Mistake to Avoid with Dogecoin Right Now

- Continuous Supply Increase: Dogecoin mints approximately 5 billion new coins annually, with a current circulation of about 169 billion, resulting in an annual supply expansion rate near 3%, which means investors face value dilution without any demand force to support price increases.

- Lack of Investment Thesis: Despite its ability to periodically attract investors, Dogecoin lacks scarcity and a solid business model, leading investors to buy based solely on speculation, which incurs high opportunity costs and significant long-term holding risks.

- Social Media Influence: For instance, a single social media post by Elon Musk in early 2021 caused Dogecoin's price to surge 80% in one day, but such volatility is extreme and often reverses quickly, prompting investors to be wary of the risks associated with short-term hype.

- Alternative Investment Recommendations: The analyst team has identified 10 stocks deemed better investment choices, with historical data showing these stocks significantly outperform Dogecoin, suggesting investors should consider allocating funds to more promising assets.

See More

Tesla May Drop Out of $1 Trillion Club by 2026

- Declining Sales: Tesla delivered 1.63 million EVs in 2025, a 9% drop from 2024, leading to a 10% decline in automotive revenue and a significant 47% impact on earnings, highlighting the vulnerability of its core business.

- Intensifying Competition: By phasing out the Model X and Model S, Tesla aims to focus on higher-volume models like the Model Y and Model 3 to counter competition from low-cost manufacturers like BYD, which outsold Tesla globally for the first time in 2025.

- Future Product Potential: While Tesla's Cybercab and Optimus robots could generate high-margin revenue streams, regulatory hurdles for FSD technology may delay the Cybercab's rollout, impacting future revenue growth.

- Significant Valuation Risks: With a P/E ratio of 377, Tesla's stock is heavily overvalued compared to other trillion-dollar companies, and if EV sales continue to decline, a 34% drop in stock price could lead to its exit from the trillion-dollar club.

See More

Cardano's 42% Drop: Is It Still a Buy?

- Insufficient Economic Activity: Cardano's total value locked (TVL) stands at approximately $141 million, significantly lower than many lesser-known chains, indicating a lack of appeal in the decentralized finance (DeFi) space and limited future growth potential.

- Poor Chain Revenue: During the 24-hour period ending March 8, Cardano generated only $270 in chain revenue from $1,350 in transaction fees, while Ethereum earned $77,095 in the same timeframe, highlighting its sluggish economic activity.

- Low User Engagement: Cardano's daily active wallet addresses fluctuate between 30,000 and 40,000, compared to Ethereum's 700,000, suggesting a weak user base and an inability to attract developers and capital effectively.

- Bleak Development Outlook: Although Cardano has the potential to develop new features to attract users, its current roadmap lacks innovations of sufficient scale and impact, making it unlikely to change its fortunes in the short term.

See More

Nasdaq-100 Index Faces Challenges Amid AI Concerns

- Market Stagnation: After three consecutive years of significant gains, the Nasdaq-100 index has stagnated in 2026, primarily due to concerns about the negative impact of artificial intelligence on the global economy and valuation levels, which have shifted it from a market leader to a laggard.

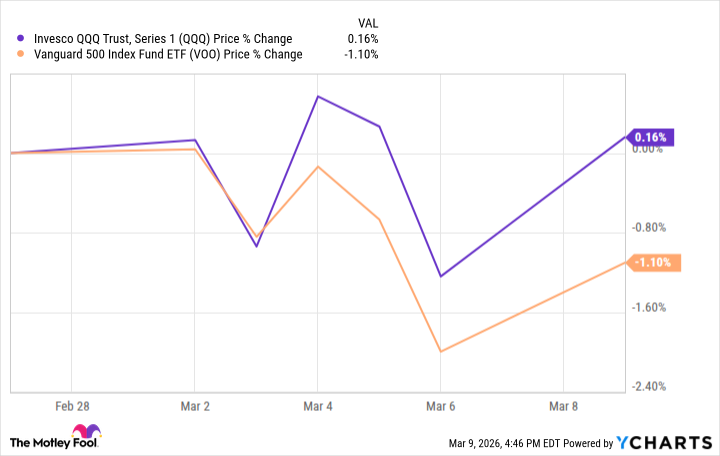

- ETF Performance Comparison: From February 27, the last trading day before the Israel-Iran war began, to March 9, the Invesco QQQ ETF, which tracks the Nasdaq-100, outperformed the Vanguard S&P 500 ETF, indicating short-term resilience in tech stocks, though overall market trends remain to be seen.

- Earnings Growth Expectations: The tech sector is projected to deliver the highest earnings and revenue growth among the S&P 500 sectors in 2026, with a slowdown to a 20% growth rate expected in 2027; however, long-term earnings growth remains a key driver of stock performance.

- Valuation Reasonableness: While U.S. stock valuations are above historical averages, the forward P/E ratio for the S&P 500 information technology sector stands at 24.2, down from 31 a year ago, suggesting that if companies meet current expectations, the Nasdaq-100's valuation may not be excessively high.

See More

Oracle's AI Investment Faces Challenges Ahead of Earnings

- Financing Impact: Oracle's announcement of a $50 billion financing plan in early February, which includes a $5 billion convertible preferred offering and approximately $25 billion in senior notes, highlights strong demand for its data center expansion but raises concerns about the pace of dilution for shareholders.

- Collaboration with OpenAI: Although talks to expand its deal with OpenAI in Texas fell through, Oracle is still on track to deliver eight data centers to OpenAI, ensuring its competitive position in the AI cloud computing space, particularly in maintaining strong relationships with key customers.

- Market Sensitivity: The news of Oracle's $300 billion deal with OpenAI previously boosted its stock by 35% last September, but subsequent debt increases have raised investor concerns about its financial health, leading to a widening of its five-year credit default swaps, reflecting skepticism about its investment-grade credit rating.

- Cost Control Measures: Analysts speculate that Oracle may implement workforce reductions and divestitures to address financing issues, with potential layoffs of 20,000 to 30,000 employees expected to generate $8 to $10 billion in incremental free cash flow, indicating urgency in cost management.

See More

Oracle's Q3 Earnings to Test AI Trade Viability

- Financing Overview: Oracle announced a $50 billion financing plan last month to support its data center buildout, with increasing market concern over the pace of dilution for shareholders, as analysts emphasize the importance of financing cadence.

- Debt Financing Details: The latest financing measures include a $5 billion convertible preferred offering and approximately $25 billion in senior notes with varying maturities, indicating strong market demand for Oracle, although investors remain cautious about its financial health.

- Collaboration with OpenAI: Oracle's relationship with OpenAI is under scrutiny; despite failed negotiations to expand in Texas, the delivery of eight sites to OpenAI remains on schedule, which is crucial for investor confidence.

- Market Reaction and Future Outlook: The news of Oracle's $300 billion deal initially boosted its stock by 35%, but subsequent debt increases raised concerns about its financial stability, leading analysts to speculate that the company may consider layoffs and divestitures to address financing challenges.

See More

Serious Mistake to Avoid with Dogecoin Right Now

- Continuous Supply Increase: Dogecoin mints approximately 5 billion new coins annually, with a current circulation of about 169 billion, resulting in an annual supply expansion rate near 3%, which means investors face value dilution without any demand force to support price increases.

- Lack of Investment Thesis: Despite its ability to periodically attract investors, Dogecoin lacks scarcity and a solid business model, leading investors to buy based solely on speculation, which incurs high opportunity costs and significant long-term holding risks.

- Social Media Influence: For instance, a single social media post by Elon Musk in early 2021 caused Dogecoin's price to surge 80% in one day, but such volatility is extreme and often reverses quickly, prompting investors to be wary of the risks associated with short-term hype.

- Alternative Investment Recommendations: The analyst team has identified 10 stocks deemed better investment choices, with historical data showing these stocks significantly outperform Dogecoin, suggesting investors should consider allocating funds to more promising assets.

See More

Tesla May Drop Out of $1 Trillion Club by 2026

- Declining Sales: Tesla delivered 1.63 million EVs in 2025, a 9% drop from 2024, leading to a 10% decline in automotive revenue and a significant 47% impact on earnings, highlighting the vulnerability of its core business.

- Intensifying Competition: By phasing out the Model X and Model S, Tesla aims to focus on higher-volume models like the Model Y and Model 3 to counter competition from low-cost manufacturers like BYD, which outsold Tesla globally for the first time in 2025.

- Future Product Potential: While Tesla's Cybercab and Optimus robots could generate high-margin revenue streams, regulatory hurdles for FSD technology may delay the Cybercab's rollout, impacting future revenue growth.

- Significant Valuation Risks: With a P/E ratio of 377, Tesla's stock is heavily overvalued compared to other trillion-dollar companies, and if EV sales continue to decline, a 34% drop in stock price could lead to its exit from the trillion-dollar club.

See More

Cardano's 42% Drop: Is It Still a Buy?

- Insufficient Economic Activity: Cardano's total value locked (TVL) stands at approximately $141 million, significantly lower than many lesser-known chains, indicating a lack of appeal in the decentralized finance (DeFi) space and limited future growth potential.

- Poor Chain Revenue: During the 24-hour period ending March 8, Cardano generated only $270 in chain revenue from $1,350 in transaction fees, while Ethereum earned $77,095 in the same timeframe, highlighting its sluggish economic activity.

- Low User Engagement: Cardano's daily active wallet addresses fluctuate between 30,000 and 40,000, compared to Ethereum's 700,000, suggesting a weak user base and an inability to attract developers and capital effectively.

- Bleak Development Outlook: Although Cardano has the potential to develop new features to attract users, its current roadmap lacks innovations of sufficient scale and impact, making it unlikely to change its fortunes in the short term.

See More

Nasdaq-100 Index Faces Challenges Amid AI Concerns

- Market Stagnation: After three consecutive years of significant gains, the Nasdaq-100 index has stagnated in 2026, primarily due to concerns about the negative impact of artificial intelligence on the global economy and valuation levels, which have shifted it from a market leader to a laggard.

- ETF Performance Comparison: From February 27, the last trading day before the Israel-Iran war began, to March 9, the Invesco QQQ ETF, which tracks the Nasdaq-100, outperformed the Vanguard S&P 500 ETF, indicating short-term resilience in tech stocks, though overall market trends remain to be seen.

- Earnings Growth Expectations: The tech sector is projected to deliver the highest earnings and revenue growth among the S&P 500 sectors in 2026, with a slowdown to a 20% growth rate expected in 2027; however, long-term earnings growth remains a key driver of stock performance.

- Valuation Reasonableness: While U.S. stock valuations are above historical averages, the forward P/E ratio for the S&P 500 information technology sector stands at 24.2, down from 31 a year ago, suggesting that if companies meet current expectations, the Nasdaq-100's valuation may not be excessively high.

See More