Analyzing the Investment Potential of Snap Inc. Stock

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 9 hours ago

0mins

Should l Buy SNAP?

Source: Yahoo Finance

- Profit Growth Potential: Snap Inc.'s 'Other Revenues' segment grew approximately 67% year-over-year to $745 million in FY25, which is expected to significantly enhance the company's profitability, especially amid weak advertising growth.

- High-Quality Revenue Source: The memory storage plans impose a 5GB free storage limit, compelling users to subscribe to retain excess memories, creating a utility-like revenue source that is decoupled from engagement metrics and applicable to Snap's 946 million MAUs.

- Market Underestimation Opportunity: Snap's long-dated $5 strike call options reflect the market's underappreciation of its platform and subscription monetization potential, and combined with near-zero distribution costs, this high-quality revenue segment could drive a substantial re-rating of the business.

- Comparison with Other Investment Choices: While Snap shows investment potential, it is considered less attractive compared to certain AI stocks, which are believed to offer greater upside potential and carry less downside risk in the current market environment.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SNAP?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SNAP

Wall Street analysts forecast SNAP stock price to rise

28 Analyst Rating

2 Buy

24 Hold

2 Sell

Hold

Current: 4.010

Low

7.00

Averages

9.57

High

13.00

Current: 4.010

Low

7.00

Averages

9.57

High

13.00

About SNAP

Snap Inc. is a technology company. Its flagship product, Snapchat, is a visual messaging application that enhances relationships with friends, family, and the world. Snapchat is the Company's core mobile device application and contains five tabs, complemented by additional tools that function outside the application. Snapchatters can interact with any or all the five tabs. Additionally, it offers Snapchat+, its subscription product that provides subscribers access to exclusive, experimental, and pre-release features. Snapchat+ offers a range of features, from allowing Snapchatters to customize the look and feel of their application, to giving special insights into their friendships. The Company also offers Snapchat for Web, a browser-based product that brings Snapchats calling and messaging capabilities to the Web. Its advertising products include AR Ads and Snap Ads. Snap Ads include Single Image or Video Ads, Story Ads, Collection Ads, Dynamic Ads, Commercials, and Sponsored Snaps.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Investment Opportunities Amid Nasdaq Correction

- Memory Chip Industry Growth: Micron Technology holds a significant position in the memory chip industry, and despite its stock being 23% below its high, the company reported nearly tripled revenue last quarter due to strong demand from data centers, highlighting its critical role in AI infrastructure development.

- Optimistic Earnings Forecast: Analysts expect Micron's adjusted earnings to grow 13% annually through fiscal 2029, making the current valuation of 16 times adjusted earnings reasonable, with a median target price of $550 per share implying a 56% upside from the current price of $352.

- Ad Tech Innovation: AppLovin's stock is 48% below its high, yet its newly launched self-service platform provides robust advertising technology support for e-commerce, with the CEO stating it serves as the foundation for the next decade of growth, showcasing the company's leading position in AI innovation.

- Undervalued Market Position: Despite facing short-term challenges, AppLovin's earnings are projected to increase by 44% annually through 2027, with the current valuation of 38 times earnings considered cheap; the median target price among 32 analysts is $650 per share, indicating a 71% upside from its current price of $380.

See More

Nasdaq Faces Correction Amid Rising Oil Prices

- Nasdaq Correction: The Nasdaq Composite index has corrected over 10% due to soaring oil prices, entering correction territory; however, historical data shows that the index has averaged a 22% return in the 12 months following such corrections, presenting a buying opportunity for investors.

- Micron Technology Outlook: Cantor Fitzgerald has set a target price of $700 per share for Micron Technology, implying a 98% upside from its current price of $352, with the company benefiting significantly from strong growth in the data center segment amid a memory chip supply shortage.

- AppLovin Growth Potential: Citigroup has set a target price of $820 per share for AppLovin, indicating a 115% upside from its current price of $380; despite concerns about AI disrupting traditional advertising models, the company is at the forefront of ad tech innovation.

- Industry Cyclicality Risks: Although Micron's stock is currently 23% below its historical high, analysts generally believe it is undervalued, with expectations of a 13% annual growth in adjusted earnings through fiscal 2029, making the current valuation of 16 times adjusted earnings appear reasonable.

See More

Analyzing the Investment Potential of Snap Inc. Stock

- Profit Growth Potential: Snap Inc.'s 'Other Revenues' segment grew approximately 67% year-over-year to $745 million in FY25, which is expected to significantly enhance the company's profitability, especially amid weak advertising growth.

- High-Quality Revenue Source: The memory storage plans impose a 5GB free storage limit, compelling users to subscribe to retain excess memories, creating a utility-like revenue source that is decoupled from engagement metrics and applicable to Snap's 946 million MAUs.

- Market Underestimation Opportunity: Snap's long-dated $5 strike call options reflect the market's underappreciation of its platform and subscription monetization potential, and combined with near-zero distribution costs, this high-quality revenue segment could drive a substantial re-rating of the business.

- Comparison with Other Investment Choices: While Snap shows investment potential, it is considered less attractive compared to certain AI stocks, which are believed to offer greater upside potential and carry less downside risk in the current market environment.

See More

Meta Faces Legal Setbacks in Social Media Addiction Trials

- Internal Research Backfire: Meta's losses in trials in Los Angeles and New Mexico revealed the company's failure to adequately police its platform, exposing teenagers to sexual harassment risks, highlighting a stark contradiction between internal research findings and public image, which could undermine future user trust and market performance.

- Lack of Research Transparency: The jury evaluated millions of corporate documents, including internal surveys indicating concerning percentages of teenage users facing unwanted sexual advances, while Meta's defense argued that the research was outdated and misleading, reflecting insufficient transparency on safety issues that may invite further regulatory scrutiny.

- Industry Reflection and Change: Following the revelations from Frances Haugen's leaked documents indicating Meta's awareness of potential harms, the tech industry is reassessing the value of internal research, leading to cuts in many research teams, which could diminish focus on user safety and impact the industry's overall sense of social responsibility.

- Concerns Over AI Research: As AI technology rapidly evolves, companies like Meta prioritize product development over safety research, with experts warning that the lack of independent studies on AI product impacts may repeat the mistakes of social media, urging the establishment of transparency and independent evaluation mechanisms to protect user rights.

See More

NASDAQ 100 Pre-Market Indicator Declines Significantly

- Market Indicator Decline: The NASDAQ 100 Pre-Market Indicator has dropped by 150.28 points to 23,436.71, indicating weakened market sentiment that could impact investor confidence and lead to further selling pressure.

- Active Stock Performance: ProShares UltraPro QQQ (TQQQ) fell by $0.74 to $40.49 with a trading volume of 9,484,281 shares, representing a 131.37% increase from its 52-week low, demonstrating strong investor interest in this ETF.

- ETF Trading Dynamics: Direxion Daily TSLA Bull 2X ETF (TSLL) decreased by $0.16 to $12.09, with 6,547,620 shares traded, reflecting a 92.21% increase from its 52-week low, indicating market expectations of volatility in Tesla's stock.

- Stock Recommendation Status: OnKure Therapeutics, Inc. (OKUR) declined by $0.44 to $4.15, with a trading volume of 3,653,160 shares, and Zacks reports its current mean recommendation is in the 'buy range', potentially attracting more investor attention.

See More

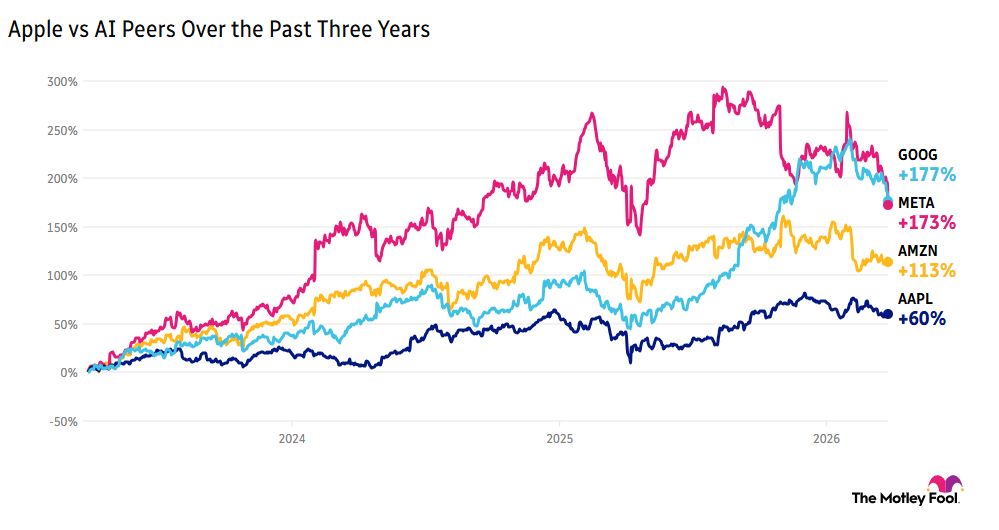

Apple Plans Major Overhaul for Siri AI Integration

- Siri System Opening: Apple plans to open the Siri operating system to third-party AI assistants in the upcoming iOS 27 release, which not only enhances user experience but also has the potential to increase service revenue through subscription fees, significantly boosting the company's revenue prospects.

- AI Assistant Integration: The new system will allow users to query AI chatbots like Anthropic's Claude and Alphabet's Gemini, making Apple less reliant on OpenAI's ChatGPT and further strengthening its competitive position in the AI market.

- Social Media Stocks Decline: Reddit and Snap fell over 8% due to the implications of a lawsuit regarding youth social media addiction, which could trigger more similar cases, impacting the future development of the entire social media industry, prompting investors to be wary of potential legal risks.

- Anthropic IPO Prospects: Anthropic is considering going public in October, potentially raising over $60 billion, with a court ruling against the government's ban on its technology usage enhancing its market credibility and providing funding for future development.

See More

Investment Opportunities Amid Nasdaq Correction

- Memory Chip Industry Growth: Micron Technology holds a significant position in the memory chip industry, and despite its stock being 23% below its high, the company reported nearly tripled revenue last quarter due to strong demand from data centers, highlighting its critical role in AI infrastructure development.

- Optimistic Earnings Forecast: Analysts expect Micron's adjusted earnings to grow 13% annually through fiscal 2029, making the current valuation of 16 times adjusted earnings reasonable, with a median target price of $550 per share implying a 56% upside from the current price of $352.

- Ad Tech Innovation: AppLovin's stock is 48% below its high, yet its newly launched self-service platform provides robust advertising technology support for e-commerce, with the CEO stating it serves as the foundation for the next decade of growth, showcasing the company's leading position in AI innovation.

- Undervalued Market Position: Despite facing short-term challenges, AppLovin's earnings are projected to increase by 44% annually through 2027, with the current valuation of 38 times earnings considered cheap; the median target price among 32 analysts is $650 per share, indicating a 71% upside from its current price of $380.

See More

Nasdaq Faces Correction Amid Rising Oil Prices

- Nasdaq Correction: The Nasdaq Composite index has corrected over 10% due to soaring oil prices, entering correction territory; however, historical data shows that the index has averaged a 22% return in the 12 months following such corrections, presenting a buying opportunity for investors.

- Micron Technology Outlook: Cantor Fitzgerald has set a target price of $700 per share for Micron Technology, implying a 98% upside from its current price of $352, with the company benefiting significantly from strong growth in the data center segment amid a memory chip supply shortage.

- AppLovin Growth Potential: Citigroup has set a target price of $820 per share for AppLovin, indicating a 115% upside from its current price of $380; despite concerns about AI disrupting traditional advertising models, the company is at the forefront of ad tech innovation.

- Industry Cyclicality Risks: Although Micron's stock is currently 23% below its historical high, analysts generally believe it is undervalued, with expectations of a 13% annual growth in adjusted earnings through fiscal 2029, making the current valuation of 16 times adjusted earnings appear reasonable.

See More

Analyzing the Investment Potential of Snap Inc. Stock

- Profit Growth Potential: Snap Inc.'s 'Other Revenues' segment grew approximately 67% year-over-year to $745 million in FY25, which is expected to significantly enhance the company's profitability, especially amid weak advertising growth.

- High-Quality Revenue Source: The memory storage plans impose a 5GB free storage limit, compelling users to subscribe to retain excess memories, creating a utility-like revenue source that is decoupled from engagement metrics and applicable to Snap's 946 million MAUs.

- Market Underestimation Opportunity: Snap's long-dated $5 strike call options reflect the market's underappreciation of its platform and subscription monetization potential, and combined with near-zero distribution costs, this high-quality revenue segment could drive a substantial re-rating of the business.

- Comparison with Other Investment Choices: While Snap shows investment potential, it is considered less attractive compared to certain AI stocks, which are believed to offer greater upside potential and carry less downside risk in the current market environment.

See More

Meta Faces Legal Setbacks in Social Media Addiction Trials

- Internal Research Backfire: Meta's losses in trials in Los Angeles and New Mexico revealed the company's failure to adequately police its platform, exposing teenagers to sexual harassment risks, highlighting a stark contradiction between internal research findings and public image, which could undermine future user trust and market performance.

- Lack of Research Transparency: The jury evaluated millions of corporate documents, including internal surveys indicating concerning percentages of teenage users facing unwanted sexual advances, while Meta's defense argued that the research was outdated and misleading, reflecting insufficient transparency on safety issues that may invite further regulatory scrutiny.

- Industry Reflection and Change: Following the revelations from Frances Haugen's leaked documents indicating Meta's awareness of potential harms, the tech industry is reassessing the value of internal research, leading to cuts in many research teams, which could diminish focus on user safety and impact the industry's overall sense of social responsibility.

- Concerns Over AI Research: As AI technology rapidly evolves, companies like Meta prioritize product development over safety research, with experts warning that the lack of independent studies on AI product impacts may repeat the mistakes of social media, urging the establishment of transparency and independent evaluation mechanisms to protect user rights.

See More

NASDAQ 100 Pre-Market Indicator Declines Significantly

- Market Indicator Decline: The NASDAQ 100 Pre-Market Indicator has dropped by 150.28 points to 23,436.71, indicating weakened market sentiment that could impact investor confidence and lead to further selling pressure.

- Active Stock Performance: ProShares UltraPro QQQ (TQQQ) fell by $0.74 to $40.49 with a trading volume of 9,484,281 shares, representing a 131.37% increase from its 52-week low, demonstrating strong investor interest in this ETF.

- ETF Trading Dynamics: Direxion Daily TSLA Bull 2X ETF (TSLL) decreased by $0.16 to $12.09, with 6,547,620 shares traded, reflecting a 92.21% increase from its 52-week low, indicating market expectations of volatility in Tesla's stock.

- Stock Recommendation Status: OnKure Therapeutics, Inc. (OKUR) declined by $0.44 to $4.15, with a trading volume of 3,653,160 shares, and Zacks reports its current mean recommendation is in the 'buy range', potentially attracting more investor attention.

See More

Apple Plans Major Overhaul for Siri AI Integration

- Siri System Opening: Apple plans to open the Siri operating system to third-party AI assistants in the upcoming iOS 27 release, which not only enhances user experience but also has the potential to increase service revenue through subscription fees, significantly boosting the company's revenue prospects.

- AI Assistant Integration: The new system will allow users to query AI chatbots like Anthropic's Claude and Alphabet's Gemini, making Apple less reliant on OpenAI's ChatGPT and further strengthening its competitive position in the AI market.

- Social Media Stocks Decline: Reddit and Snap fell over 8% due to the implications of a lawsuit regarding youth social media addiction, which could trigger more similar cases, impacting the future development of the entire social media industry, prompting investors to be wary of potential legal risks.

- Anthropic IPO Prospects: Anthropic is considering going public in October, potentially raising over $60 billion, with a court ruling against the government's ban on its technology usage enhancing its market credibility and providing funding for future development.

See More