xAI Loses Two Co-Founders in Two Days

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 11 2026

0mins

Should l Buy TSLA?

Source: seekingalpha

- Co-Founder Departures: Prominent AI researcher Jimmy Ba announced his resignation from xAI on Tuesday, expressing gratitude to Elon Musk for the opportunity to co-found the company.

- Internal Tensions: Ba's exit follows the departure of fellow co-founder Tony Wu, highlighting internal tensions within the technical team over demands to enhance AI model performance.

- Merger with SpaceX: xAI merged with Musk's aerospace company SpaceX earlier this month, yet the frequent executive turnover may impact the company's stability and strategic direction.

- Increased Competitive Pressure: Musk faces mounting pressure from rivals like OpenAI and Anthropic to accelerate improvements in AI model performance, but internal turmoil could hinder achieving these objectives.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TSLA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

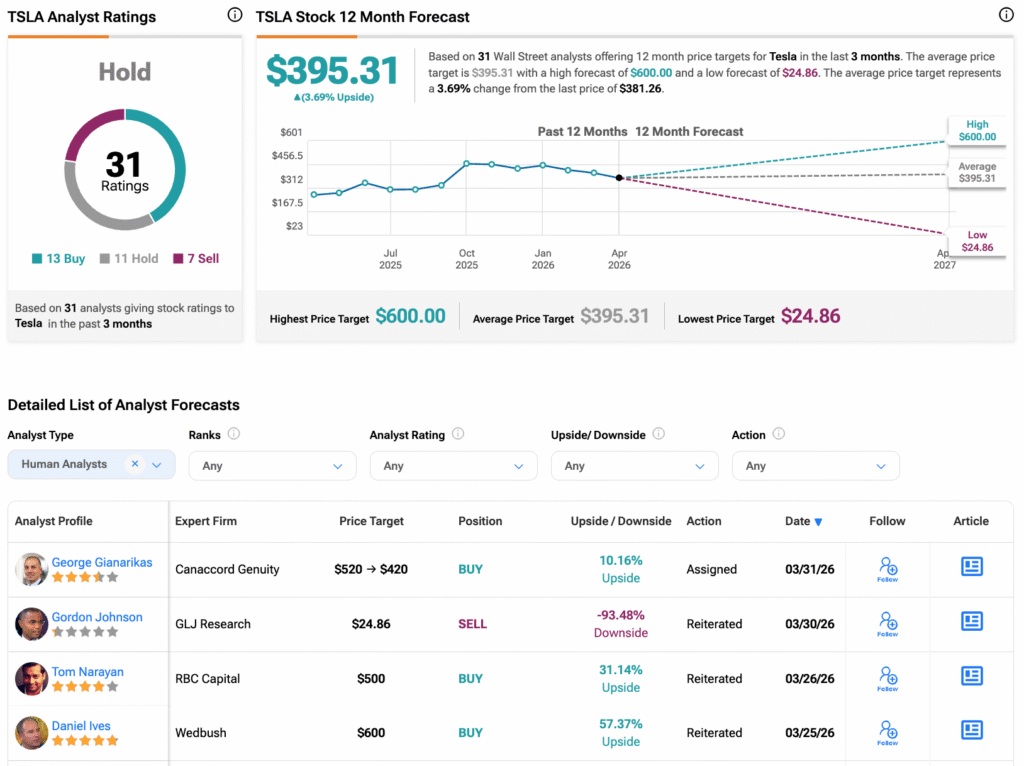

Analyst Views on TSLA

Wall Street analysts forecast TSLA stock price to rise

30 Analyst Rating

12 Buy

11 Hold

7 Sell

Hold

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

About TSLA

Tesla, Inc. designs, develops, manufactures, sells and leases high-performance fully electric vehicles and energy generation and storage systems, and offers services related to its products. Its segments include automotive, and energy generation and storage. The automotive segment includes the design, development, manufacturing, sales and leasing of high-performance fully electric vehicles, and sales of automotive regulatory credits. It also includes sales of used vehicles, non-warranty maintenance services and collisions, part sales, paid supercharging, insurance services revenue and retail merchandise sales. The energy generation and storage segment include the design, manufacture, installation, sales and leasing of solar energy generation and energy storage products and related services and sales of solar energy systems incentives. Its consumer vehicles include the Model 3, Y, S, X and Cybertruck. Its lithium-ion battery energy storage products include Powerwall and Megapack.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

SpaceX IPO Set to Become Largest in History

- Historic IPO: SpaceX's acquisition of xAI for $1.25 trillion sets the stage for an IPO valued at $1.75 trillion, making it the largest IPO in history, although only $40 billion to $80 billion in shares may be available for public sale.

- Market Impact Analysis: While SpaceX's IPO valuation is projected at $1.75 trillion, the actual shares available for public purchase will be significantly lower compared to Saudi Aramco's $25.6 billion IPO in 2019, potentially affecting investor expectations.

- IPO Process Overview: The IPO will involve months of planning, starting with the confidential submission of an initial prospectus to the SEC, a process expected to take about three months before entering the “Roadshow” phase to disclose financials.

- Investor Preparation Time: Investors will have ample time to assess whether to buy SpaceX shares on the IPO date, and the scale of the IPO ensures it will be a major news event even before its official launch.

See More

SpaceX Set for IPO Valued at $1.75 Trillion

- Historic IPO: SpaceX is expected to launch its IPO with a valuation of $1.75 trillion, making it the largest IPO in history, surpassing the $25.6 billion record set by Saudi Aramco in 2019, reflecting immense market confidence in the aerospace sector.

- Merger Impact: The acquisition of xAI for $1.25 trillion enhances SpaceX's market position, and the anticipated IPO is likely to attract significant investor interest, particularly from Musk's supporters and Tesla shareholders, providing a new investment avenue.

- Share Supply Expectations: Despite SpaceX's valuation reaching $1.75 trillion, only $40 billion to $80 billion in shares are expected to be available for public sale, indicating that while the IPO is massive, the actual tradable shares will be limited, potentially leading to heightened demand.

- Complex Listing Process: The IPO process for SpaceX involves submitting a preliminary prospectus to the SEC, which may take about three months, followed by a “Roadshow” that will provide investors with the first real insight into the company's financials, ensuring a smooth IPO execution.

See More

Rivian's Strategic Partnership with Volkswagen

- Capital Injection: Volkswagen's $1 billion investment in Rivian signifies a successful collaboration at a key development milestone, expected to provide crucial funding for Rivian's electric truck launch, helping it establish a foothold in the competitive EV market.

- Technological Collaboration: This investment not only offers financial support but also indicates Volkswagen's successful testing of Rivian's technology, as Rivian aims to broaden its sales opportunities by becoming an industry supplier, thereby enhancing its market competitiveness.

- Strategic Differentiation: Unlike Tesla, Rivian adopts a dual strategy as both an electric vehicle manufacturer and a technology supplier, a strategy that helps it stand out in an increasingly competitive market and increases the likelihood of long-term success.

- Market Outlook: Facing competition from major automakers and other EV startups, Rivian's partnership with Volkswagen not only secures funding but also gains technological validation, laying a foundation for future market expansion.

See More

Rivian Secures $1 Billion Investment from Volkswagen

- Capital Injection: Rivian has secured a $1 billion investment from Volkswagen as part of a larger $5.8 billion funding plan, which will support the launch of a more affordable electric truck, enhancing its market competitiveness.

- Technological Collaboration: Volkswagen's successful testing of Rivian's technology not only provides financial backing but also indicates the recognition of Rivian's technology within the industry, further advancing its supplier strategy.

- Market Positioning: Unlike Tesla, Rivian aims to be both a vehicle manufacturer and an industry supplier, which broadens its sales opportunities and enhances the returns on its technology investments through this dual strategy.

- Competitive Landscape: In an increasingly competitive electric vehicle market, Rivian's success hinges not only on financial support but also on the effective execution of its supplier strategy to ensure long-term survival and growth.

See More

Leasing Market Faces Challenges for EVs

- Leasing Market Risks: A wave of off-lease EVs is expected to return with values approximately $10,000 lower than projected, potentially costing the finance arms up to $8 billion, which could significantly impact overall industry profitability.

- Surge in Supply: By 2028, around 800,000 EVs are projected to hit the used market, leading to oversupply and further price depreciation, which may put additional financial strain on leasing companies.

- Tesla's Market Dominance: Tesla's leasing volume is substantial, with nearly 229,000 EVs leased last year, far exceeding the combined totals of General Motors and Ford, highlighting its strong influence in the industry.

- Financial Management Strategy: Despite industry challenges, Tesla mitigates its financial risk by managing a portion of its lease portfolio through partnerships with third-party lenders, allowing investors to remain cautiously optimistic while monitoring market developments in the coming years.

See More

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

SpaceX IPO Set to Become Largest in History

- Historic IPO: SpaceX's acquisition of xAI for $1.25 trillion sets the stage for an IPO valued at $1.75 trillion, making it the largest IPO in history, although only $40 billion to $80 billion in shares may be available for public sale.

- Market Impact Analysis: While SpaceX's IPO valuation is projected at $1.75 trillion, the actual shares available for public purchase will be significantly lower compared to Saudi Aramco's $25.6 billion IPO in 2019, potentially affecting investor expectations.

- IPO Process Overview: The IPO will involve months of planning, starting with the confidential submission of an initial prospectus to the SEC, a process expected to take about three months before entering the “Roadshow” phase to disclose financials.

- Investor Preparation Time: Investors will have ample time to assess whether to buy SpaceX shares on the IPO date, and the scale of the IPO ensures it will be a major news event even before its official launch.

See More

SpaceX Set for IPO Valued at $1.75 Trillion

- Historic IPO: SpaceX is expected to launch its IPO with a valuation of $1.75 trillion, making it the largest IPO in history, surpassing the $25.6 billion record set by Saudi Aramco in 2019, reflecting immense market confidence in the aerospace sector.

- Merger Impact: The acquisition of xAI for $1.25 trillion enhances SpaceX's market position, and the anticipated IPO is likely to attract significant investor interest, particularly from Musk's supporters and Tesla shareholders, providing a new investment avenue.

- Share Supply Expectations: Despite SpaceX's valuation reaching $1.75 trillion, only $40 billion to $80 billion in shares are expected to be available for public sale, indicating that while the IPO is massive, the actual tradable shares will be limited, potentially leading to heightened demand.

- Complex Listing Process: The IPO process for SpaceX involves submitting a preliminary prospectus to the SEC, which may take about three months, followed by a “Roadshow” that will provide investors with the first real insight into the company's financials, ensuring a smooth IPO execution.

See More

Rivian's Strategic Partnership with Volkswagen

- Capital Injection: Volkswagen's $1 billion investment in Rivian signifies a successful collaboration at a key development milestone, expected to provide crucial funding for Rivian's electric truck launch, helping it establish a foothold in the competitive EV market.

- Technological Collaboration: This investment not only offers financial support but also indicates Volkswagen's successful testing of Rivian's technology, as Rivian aims to broaden its sales opportunities by becoming an industry supplier, thereby enhancing its market competitiveness.

- Strategic Differentiation: Unlike Tesla, Rivian adopts a dual strategy as both an electric vehicle manufacturer and a technology supplier, a strategy that helps it stand out in an increasingly competitive market and increases the likelihood of long-term success.

- Market Outlook: Facing competition from major automakers and other EV startups, Rivian's partnership with Volkswagen not only secures funding but also gains technological validation, laying a foundation for future market expansion.

See More

Rivian Secures $1 Billion Investment from Volkswagen

- Capital Injection: Rivian has secured a $1 billion investment from Volkswagen as part of a larger $5.8 billion funding plan, which will support the launch of a more affordable electric truck, enhancing its market competitiveness.

- Technological Collaboration: Volkswagen's successful testing of Rivian's technology not only provides financial backing but also indicates the recognition of Rivian's technology within the industry, further advancing its supplier strategy.

- Market Positioning: Unlike Tesla, Rivian aims to be both a vehicle manufacturer and an industry supplier, which broadens its sales opportunities and enhances the returns on its technology investments through this dual strategy.

- Competitive Landscape: In an increasingly competitive electric vehicle market, Rivian's success hinges not only on financial support but also on the effective execution of its supplier strategy to ensure long-term survival and growth.

See More

Leasing Market Faces Challenges for EVs

- Leasing Market Risks: A wave of off-lease EVs is expected to return with values approximately $10,000 lower than projected, potentially costing the finance arms up to $8 billion, which could significantly impact overall industry profitability.

- Surge in Supply: By 2028, around 800,000 EVs are projected to hit the used market, leading to oversupply and further price depreciation, which may put additional financial strain on leasing companies.

- Tesla's Market Dominance: Tesla's leasing volume is substantial, with nearly 229,000 EVs leased last year, far exceeding the combined totals of General Motors and Ford, highlighting its strong influence in the industry.

- Financial Management Strategy: Despite industry challenges, Tesla mitigates its financial risk by managing a portion of its lease portfolio through partnerships with third-party lenders, allowing investors to remain cautiously optimistic while monitoring market developments in the coming years.

See More