Morgan Stanley Earnings: What to Expect With the Stock Near a Record High

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Oct 15 2024

0mins

Source: Barron's

Earnings Expectations: Morgan Stanley is anticipated to report a net income of $2.6 billion for the third quarter, an increase from $2.4 billion last year, driven by strong investment banking and wealth management results.

Market Performance: The bank's stock recently reached an all-time high and has risen 20% this year, with analysts noting that its wealth management sector remains a significant revenue contributor amidst competitive pressures from firms like Goldman Sachs and JPMorgan Chase.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MS

Wall Street analysts forecast MS stock price to fall

14 Analyst Rating

7 Buy

7 Hold

0 Sell

Moderate Buy

Current: 200.510

Low

132.00

Averages

185.00

High

219.00

Current: 200.510

Low

132.00

Averages

185.00

High

219.00

About MS

Morgan Stanley is a global financial services company. The Company is engaged in providing a range of investment banking, securities, wealth management and investment management services. Its segments include Institutional Securities, Wealth Management and Investment Management. Its Institutional Securities segment provides a variety of products and services to corporations, governments, financial institutions and ultra-high net worth clients. Its Wealth Management segment provides an array of financial services and solutions to individual investors and small to medium-sized businesses and institutions. Its Investment Management segment provides a range of investment strategies and products that span geographies, asset classes, and public and private markets to a diverse group of clients across institutional and intermediary channels. Its investment banking services consist of capital raising and financial advisory services, including the underwriting of debt and other products.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Morgan Stanley Lowers Southern Company Target to $87

- Target Price Adjustment: Morgan Stanley analyst David Arcaro lowered the target price for Southern Company (NYSE:SO) from $92 to $87 while maintaining an Underweight rating, reflecting a cautious outlook on the utilities sector.

- Stable Dividend Yield: With an annual dividend yield of 3.22%, Southern Company is included among the 10 high-yield stocks for lasting retirement income, highlighting its appeal for stable income generation.

- Capital Expenditure Plan: The company has an $81 billion regulated capital expenditure plan expected to support 9% rate base growth through 2030, indicating strong demand visibility and growth potential.

- Market Performance Lag: Morgan Stanley noted that utilities lagged behind the S&P 500's performance during the month, indicating a lack of overall market confidence in the sector.

See More

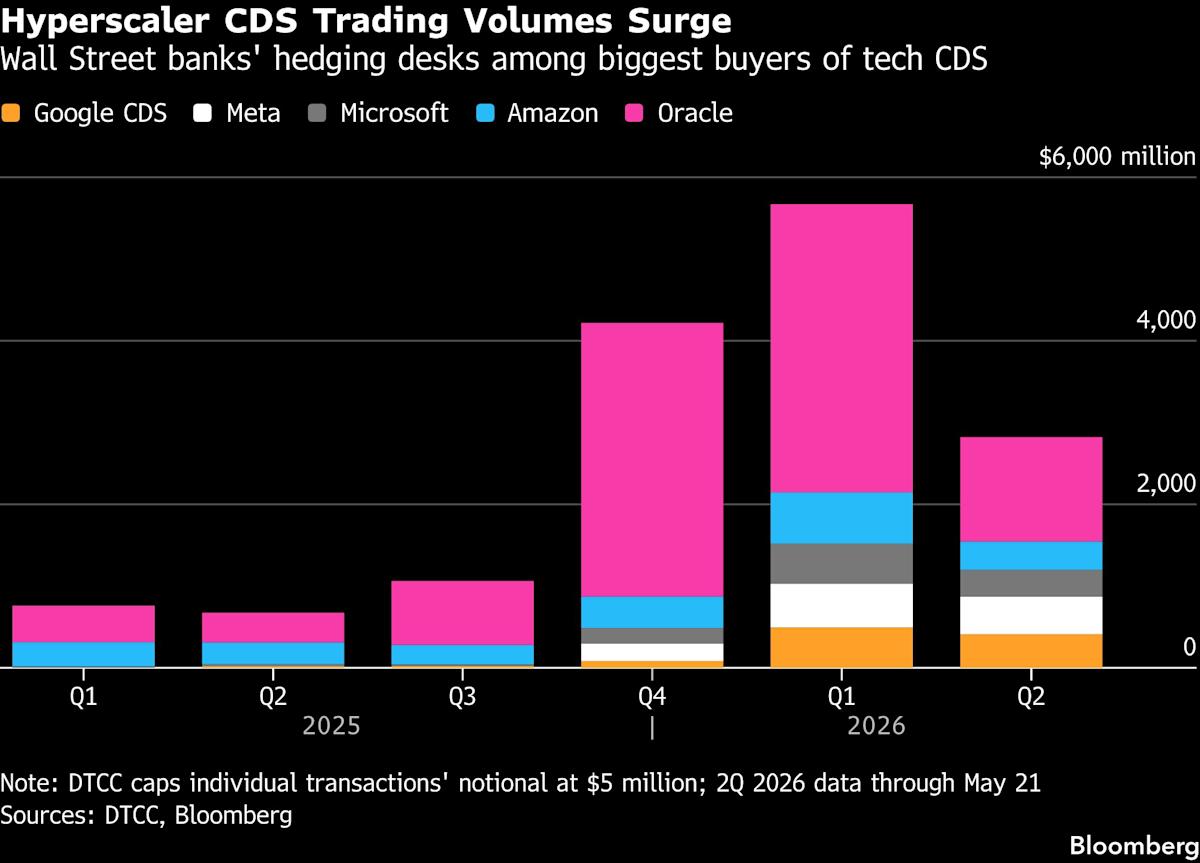

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More

Analysts Favor Investment in China's AI Stocks

- Clear Investment Theme: Analysts agree that despite slowing economic growth in China, AI-related stocks represent the most obvious investment theme right now, with over half of the holdings in new funds focused on semiconductors and high-tech manufacturing, indicating confidence in future growth.

- Weak Consumer Performance: China's retail sales growth in April marked the lowest since the end of the pandemic, highlighting ongoing weakness in the consumer market, while tech stocks exhibit uneven performance, reflecting challenges in the overall economic environment.

- Market Dynamics Shift: In the past two months, a rotation in tech stocks has occurred, with increased investor focus on semiconductors, hard tech, and software, indicating a growing demand for these segments, particularly in the A-share market.

- Divergent Investment Strategies: Mironov holds large positions in Tencent and Alibaba, while Morgan Stanley favors AI model companies like Zhipu and MiniMax, showcasing a divergence in market views on investment strategies and perceptions of sustainable business models.

See More

S&P 500 Index Approaches New Record High

- Market Rebound: The S&P 500 index has advanced for eight consecutive weeks, nearing its record close of 7,501 from May 14, indicating strong investor confidence in economic recovery despite earlier volatility.

- Oil and Bond Yield Impact: Although oil prices surged above $100 per barrel and the 30-year Treasury yield hit its highest level since 2007, the market rebounded on Wednesday, suggesting a restoration of investor optimism regarding economic prospects.

- Nvidia's Strong Earnings: Nvidia reported a blockbuster quarter on Wednesday, exceeding analyst expectations with CEO Jensen Huang stating that demand has gone parabolic, although the stock fell 2.6% post-earnings, highlighting its growth potential in the AI sector.

- CrowdStrike's Strong Performance: CrowdStrike shares climbed nearly 12% over the past week, with multiple Wall Street firms raising their price targets, reflecting optimistic market expectations for cybersecurity demand despite competitive pressures from AI technologies.

See More

Inflation Undermines Bond Stability in Portfolios

- Erosion of Bonds' Role: Morgan Stanley's analysis of 150 years of stock and bond data reveals that when inflation exceeds 2.4%, bonds significantly lose their function as a stock market shock absorber, with current inflation at 3.8% posing greater risks for investors.

- Portfolio Performance Decline: The classic 60/40 portfolio peaked at the end of 2021 and, while it has rebounded, the recovery in bonds has been much weaker than in stocks, as the Bloomberg Aggregate Bond Index has only returned to its starting level, indicating a decline in bond attractiveness.

- Disappearance of Negative Correlation: Morgan Stanley highlights that inflation is the primary driver of stock and bond movements together, with inflation above 2.4% leading to positive correlation, which diminishes the protective capacity of portfolios, prompting investors to reassess risks.

- Future Market Risks: While bonds still provide value for income-seeking investors, factors like inflation, rising oil prices, and fiscal stress may hinder bonds from delivering expected protection, necessitating cautious navigation of potential market shocks.

See More

Fanatics to Replace Panini as FIFA's Exclusive Licensee

- Market Share Expansion: Fanatics has secured an agreement with FIFA to become the exclusive licensee for World Cup collectibles starting in 2031, which is expected to further solidify its position in the $100 billion global sports collectibles market and drive revenue growth.

- Innovative Product Launch: Under the new agreement, debuting teams will wear 'debut patches' on matchday jerseys, which will be converted into exclusive trading cards, likely attracting more collectors and enhancing market demand and brand influence.

- Increased Legal Challenges: Fanatics' aggressive expansion has prompted an antitrust lawsuit from Panini, alleging attempts to monopolize the trading card market for major U.S. professional sports leagues, potentially leading to higher prices and fewer choices for consumers, impacting the company's reputation.

- Changing Competitive Landscape: With Fanatics' acquisition of Topps, competition has significantly diminished, leaving Upper Deck as the only major competitor; while Fanatics promises to continue driving innovation and improving consumer experience, concerns about its monopolistic behavior persist.

See More

Morgan Stanley Lowers Southern Company Target to $87

- Target Price Adjustment: Morgan Stanley analyst David Arcaro lowered the target price for Southern Company (NYSE:SO) from $92 to $87 while maintaining an Underweight rating, reflecting a cautious outlook on the utilities sector.

- Stable Dividend Yield: With an annual dividend yield of 3.22%, Southern Company is included among the 10 high-yield stocks for lasting retirement income, highlighting its appeal for stable income generation.

- Capital Expenditure Plan: The company has an $81 billion regulated capital expenditure plan expected to support 9% rate base growth through 2030, indicating strong demand visibility and growth potential.

- Market Performance Lag: Morgan Stanley noted that utilities lagged behind the S&P 500's performance during the month, indicating a lack of overall market confidence in the sector.

See More

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More

Analysts Favor Investment in China's AI Stocks

- Clear Investment Theme: Analysts agree that despite slowing economic growth in China, AI-related stocks represent the most obvious investment theme right now, with over half of the holdings in new funds focused on semiconductors and high-tech manufacturing, indicating confidence in future growth.

- Weak Consumer Performance: China's retail sales growth in April marked the lowest since the end of the pandemic, highlighting ongoing weakness in the consumer market, while tech stocks exhibit uneven performance, reflecting challenges in the overall economic environment.

- Market Dynamics Shift: In the past two months, a rotation in tech stocks has occurred, with increased investor focus on semiconductors, hard tech, and software, indicating a growing demand for these segments, particularly in the A-share market.

- Divergent Investment Strategies: Mironov holds large positions in Tencent and Alibaba, while Morgan Stanley favors AI model companies like Zhipu and MiniMax, showcasing a divergence in market views on investment strategies and perceptions of sustainable business models.

See More

S&P 500 Index Approaches New Record High

- Market Rebound: The S&P 500 index has advanced for eight consecutive weeks, nearing its record close of 7,501 from May 14, indicating strong investor confidence in economic recovery despite earlier volatility.

- Oil and Bond Yield Impact: Although oil prices surged above $100 per barrel and the 30-year Treasury yield hit its highest level since 2007, the market rebounded on Wednesday, suggesting a restoration of investor optimism regarding economic prospects.

- Nvidia's Strong Earnings: Nvidia reported a blockbuster quarter on Wednesday, exceeding analyst expectations with CEO Jensen Huang stating that demand has gone parabolic, although the stock fell 2.6% post-earnings, highlighting its growth potential in the AI sector.

- CrowdStrike's Strong Performance: CrowdStrike shares climbed nearly 12% over the past week, with multiple Wall Street firms raising their price targets, reflecting optimistic market expectations for cybersecurity demand despite competitive pressures from AI technologies.

See More

Inflation Undermines Bond Stability in Portfolios

- Erosion of Bonds' Role: Morgan Stanley's analysis of 150 years of stock and bond data reveals that when inflation exceeds 2.4%, bonds significantly lose their function as a stock market shock absorber, with current inflation at 3.8% posing greater risks for investors.

- Portfolio Performance Decline: The classic 60/40 portfolio peaked at the end of 2021 and, while it has rebounded, the recovery in bonds has been much weaker than in stocks, as the Bloomberg Aggregate Bond Index has only returned to its starting level, indicating a decline in bond attractiveness.

- Disappearance of Negative Correlation: Morgan Stanley highlights that inflation is the primary driver of stock and bond movements together, with inflation above 2.4% leading to positive correlation, which diminishes the protective capacity of portfolios, prompting investors to reassess risks.

- Future Market Risks: While bonds still provide value for income-seeking investors, factors like inflation, rising oil prices, and fiscal stress may hinder bonds from delivering expected protection, necessitating cautious navigation of potential market shocks.

See More

Fanatics to Replace Panini as FIFA's Exclusive Licensee

- Market Share Expansion: Fanatics has secured an agreement with FIFA to become the exclusive licensee for World Cup collectibles starting in 2031, which is expected to further solidify its position in the $100 billion global sports collectibles market and drive revenue growth.

- Innovative Product Launch: Under the new agreement, debuting teams will wear 'debut patches' on matchday jerseys, which will be converted into exclusive trading cards, likely attracting more collectors and enhancing market demand and brand influence.

- Increased Legal Challenges: Fanatics' aggressive expansion has prompted an antitrust lawsuit from Panini, alleging attempts to monopolize the trading card market for major U.S. professional sports leagues, potentially leading to higher prices and fewer choices for consumers, impacting the company's reputation.

- Changing Competitive Landscape: With Fanatics' acquisition of Topps, competition has significantly diminished, leaving Upper Deck as the only major competitor; while Fanatics promises to continue driving innovation and improving consumer experience, concerns about its monopolistic behavior persist.

See More