What Caused Dell's Stock to Drop in Premarket Trading Today?

Dell's Stock Decline: Dell Technologies Inc. saw a significant drop of over 5% in premarket trading on November 17, 2025, following a downgrade from Morgan Stanley, which lowered its rating from Overweight to Underweight and cut the price target from $144 to $110 due to concerns over AI server mix and rising component costs.

Impact of Rising Costs: Morgan Stanley analyst Erik Woodring highlighted that surging memory costs, particularly in DRAM and NAND, are expected to negatively impact Dell's profitability, leading to a projected 12% hit to earnings per share and a reduction in gross and operating margin estimates by 150-220 basis points for fiscal year 2027.

Recent Stock Performance: Despite the downgrade, Dell has shown resilience with year-to-date returns of 18.18% and a one-year return of 1.31%. However, the stock has faced a 6.26% decline over the past week, trading at $125.01 in premarket, down from a previous close of $133.94.

Market Outlook: Morgan Stanley's bearish outlook underscores the challenges Dell faces in the near term due to component cost inflation, which threatens to pressure margins and overall valuation, even as the stock has a 52-week range of $66.25 to $168.08 and an average analyst price target suggesting potential upside.

Trade with 70% Backtested Accuracy

Analyst Views on AI

About AI

About the author

C3.ai Shares Drop After Executive Stock Sale Amid Weak Financials

- Executive Sell-off Impact: C3.ai's Executive Chairman Thomas M. Siebel sold over $4.1 million in company stock on April 13 and 14, leading to a 1.8% drop in share price during the afternoon session, which heightened investor concerns regarding the company's weak financial performance.

- Declining Financial Performance: The company reported a staggering 46% revenue decline to $53.3 million for its fiscal third quarter, missing its own projections, and subsequently lowered its fiscal year 2026 revenue guidance by approximately $51 million, indicating a troubling 36% negative growth rate attributed to poor sales execution.

- Deteriorating Cash Flow: C3.ai reported a negative free cash flow of $56.2 million and forecasted a 54% year-over-year revenue decline for the fourth quarter, which deepened worries about its financial stability and significantly impacted investor confidence in the company's future.

- Increased Market Volatility: C3.ai's shares have dropped 32.7% since the beginning of the year, currently trading at $9.26 per share, which is 68.3% below its 52-week high of $29.16, reflecting a pessimistic sentiment in the market regarding its future prospects.

Analysts Bullish on Nebius and Linde's Future Prospects

- Nebius Group Potential: Nebius Group (NBIS), focusing on AI cloud infrastructure, recently secured a $2 billion investment from Nvidia and a $27 billion contract with Meta, projecting future revenues nearing $50 billion, indicating strong market demand and growth potential.

- Linde's Strategic Advantage: Linde (LIN) holds enough helium reserves to cover six months of global demand amid tightening supply, expected to leverage this advantage to enhance pricing power in the semiconductor sector, thereby expanding profit margins.

- C3.ai's Challenges: C3.ai (AI) faces significant declines with shares down over 55% year-to-date, and management has lowered fiscal 2026 guidance, reflecting execution issues and deteriorating cash flow, leading analysts to generally assign sell ratings.

- Market Response and Outlook: Despite C3.ai's struggles, the strong performance of Nebius and Linde, along with positive analyst ratings, suggests ongoing market interest in AI-related companies, prompting investors to monitor industry dynamics and fundamental changes.

C3.ai Faces Revenue Plunge and Executive Transition

- Revenue Plunge: C3.ai's revenue fell 46% in Q3 of fiscal 2026 to $53.3 million, significantly below management's forecast of $72 million to $80 million, highlighting the substantial impact of founder Siebel's departure on sales performance.

- Massive Losses: The company reported a staggering loss of $133.4 million for the quarter, a 66% increase from the previous year, as the sudden revenue drop did not allow sufficient time to adjust operating expenses, indicating urgent financial management needs.

- New CEO Challenges: New CEO Stephen Ehikian has initiated a restructuring of the sales department to lower costs and enhance oversight on deals, yet the company must quickly reduce losses to avoid potential cash injection needs in the coming years.

- Valuation Risks: While C3.ai's stock has dropped 40% in 2026 and 95% from its 2020 peak, resulting in a price-to-sales ratio of 3.7, analysts predict further revenue declines in the next two years, suggesting investors should carefully assess the timing for potential investments.

Palantir Technologies Stock Rises 3.33% Amid Political Endorsements

- Stock Price Increase: Palantir Technologies closed at $132.37 on Monday, up 3.33%, driven by political endorsements and ongoing purchases by ARK Invest, indicating strong market interest in its AI defense and commercial applications.

- Surge in Trading Volume: The company's trading volume reached 65.2 million shares, nearly 23% above the three-month average of 51.6 million shares, reflecting renewed investor interest, particularly after a sharp sell-off.

- Long-Term Contracts Support: Palantir's business remains anchored by long-term government contracts, reinforced by the Pentagon's decision to designate the Maven Smart System as a program of record, which solidifies its position in the defense sector while its commercial business is expected to drive future growth.

- Market Focus on Future Contracts: Investors are looking for Palantir to quickly secure new commercial contracts to support its recovery rather than relying solely on defense deals, making its stock price highly sensitive to shifts in confidence regarding growth and competition.

Palantir Stock Rises 3.4% Amid Political Endorsements

- Stock Recovery: Palantir Technologies (PLTR) shares rose 3.4% to $132.37, reflecting investor optimism driven by political endorsements and ongoing ARK Invest purchases, highlighting market interest in its AI defense and commercial applications.

- Surge in Trading Volume: The company saw a trading volume of 65.2 million shares, nearly 23% above the three-month average of 51.6 million shares, indicating a significant increase in investor interest that may signal future market activity.

- Long-Term Contract Support: Palantir's business remains anchored by long-term government contracts, with the Pentagon designating the Maven Smart System as a program of record, further solidifying its position in the defense sector and expected to provide stable support for future growth.

- Commercial Growth Potential: Investors are keen to see if Palantir can quickly secure new commercial contracts to aid recovery rather than relying solely on defense deals, as the current stock price already reflects expectations of ongoing AI leadership, making it sensitive to any shifts in confidence.

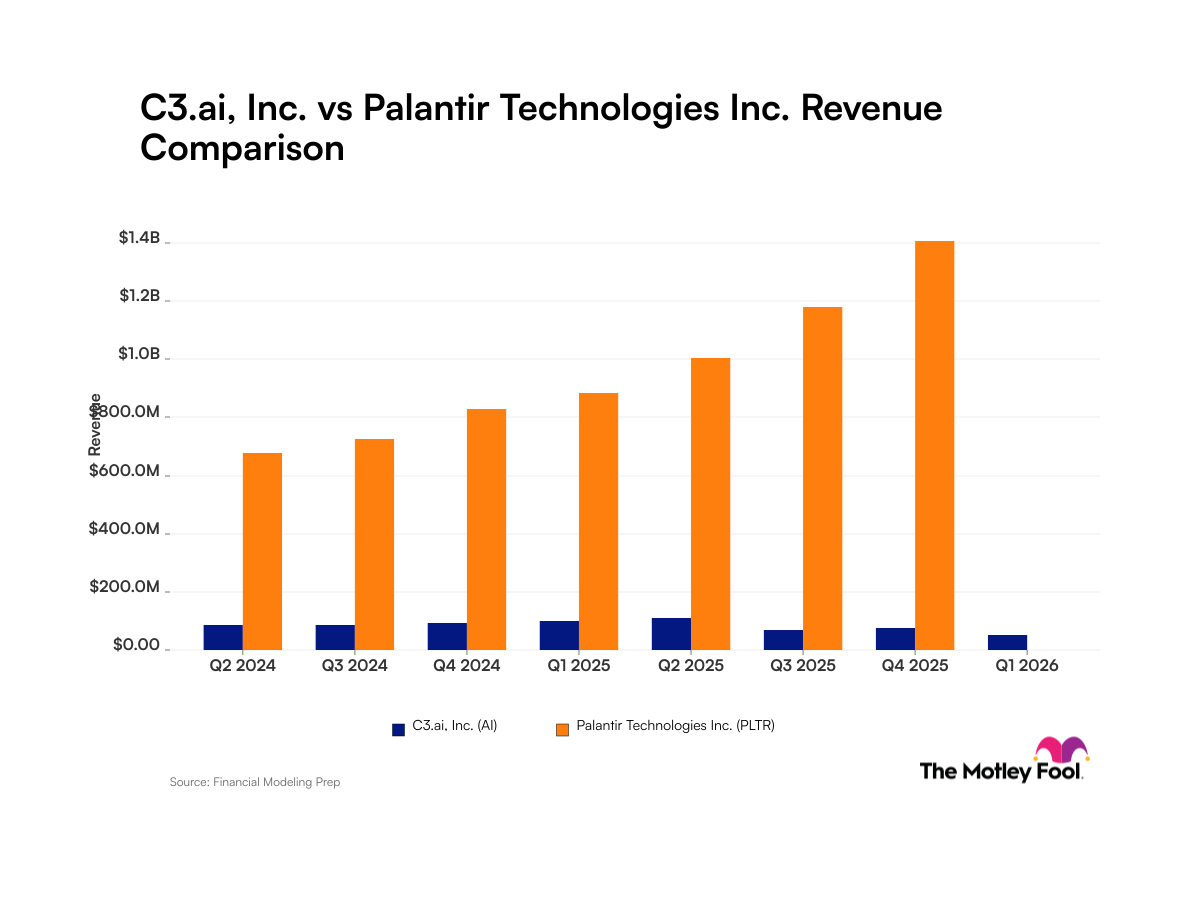

C3.ai vs Palantir: A Financial Comparison

- C3.ai Revenue Decline: C3.ai reported a revenue of $53.3 million for the quarter ending January 2026, with a net income margin of -250%, indicating severe financial challenges during a leadership transition that could impact its competitive position.

- Palantir Revenue Growth: Palantir achieved approximately $1.4 billion in revenue for the quarter ending December 2025, with a net income margin of 43%, showcasing strong growth momentum in the AI software market and attracting more customer interest.

- Market Performance Comparison: C3.ai's stock fell by 3.36% to $8.48, while Palantir's stock decreased by 7.45% to $130.28, reflecting differing investor expectations regarding the future performance of the two companies.

- Competitive Position Disparity: C3.ai has reported GAAP net losses in every quarter over the past two years, highlighting its competitive disadvantage, whereas Palantir continues to grow, indicating significant potential and strong customer demand in the AI platform market.

C3.ai Shares Drop After Executive Stock Sale Amid Weak Financials

- Executive Sell-off Impact: C3.ai's Executive Chairman Thomas M. Siebel sold over $4.1 million in company stock on April 13 and 14, leading to a 1.8% drop in share price during the afternoon session, which heightened investor concerns regarding the company's weak financial performance.

- Declining Financial Performance: The company reported a staggering 46% revenue decline to $53.3 million for its fiscal third quarter, missing its own projections, and subsequently lowered its fiscal year 2026 revenue guidance by approximately $51 million, indicating a troubling 36% negative growth rate attributed to poor sales execution.

- Deteriorating Cash Flow: C3.ai reported a negative free cash flow of $56.2 million and forecasted a 54% year-over-year revenue decline for the fourth quarter, which deepened worries about its financial stability and significantly impacted investor confidence in the company's future.

- Increased Market Volatility: C3.ai's shares have dropped 32.7% since the beginning of the year, currently trading at $9.26 per share, which is 68.3% below its 52-week high of $29.16, reflecting a pessimistic sentiment in the market regarding its future prospects.

Analysts Bullish on Nebius and Linde's Future Prospects

- Nebius Group Potential: Nebius Group (NBIS), focusing on AI cloud infrastructure, recently secured a $2 billion investment from Nvidia and a $27 billion contract with Meta, projecting future revenues nearing $50 billion, indicating strong market demand and growth potential.

- Linde's Strategic Advantage: Linde (LIN) holds enough helium reserves to cover six months of global demand amid tightening supply, expected to leverage this advantage to enhance pricing power in the semiconductor sector, thereby expanding profit margins.

- C3.ai's Challenges: C3.ai (AI) faces significant declines with shares down over 55% year-to-date, and management has lowered fiscal 2026 guidance, reflecting execution issues and deteriorating cash flow, leading analysts to generally assign sell ratings.

- Market Response and Outlook: Despite C3.ai's struggles, the strong performance of Nebius and Linde, along with positive analyst ratings, suggests ongoing market interest in AI-related companies, prompting investors to monitor industry dynamics and fundamental changes.

C3.ai Faces Revenue Plunge and Executive Transition

- Revenue Plunge: C3.ai's revenue fell 46% in Q3 of fiscal 2026 to $53.3 million, significantly below management's forecast of $72 million to $80 million, highlighting the substantial impact of founder Siebel's departure on sales performance.

- Massive Losses: The company reported a staggering loss of $133.4 million for the quarter, a 66% increase from the previous year, as the sudden revenue drop did not allow sufficient time to adjust operating expenses, indicating urgent financial management needs.

- New CEO Challenges: New CEO Stephen Ehikian has initiated a restructuring of the sales department to lower costs and enhance oversight on deals, yet the company must quickly reduce losses to avoid potential cash injection needs in the coming years.

- Valuation Risks: While C3.ai's stock has dropped 40% in 2026 and 95% from its 2020 peak, resulting in a price-to-sales ratio of 3.7, analysts predict further revenue declines in the next two years, suggesting investors should carefully assess the timing for potential investments.

Palantir Technologies Stock Rises 3.33% Amid Political Endorsements

- Stock Price Increase: Palantir Technologies closed at $132.37 on Monday, up 3.33%, driven by political endorsements and ongoing purchases by ARK Invest, indicating strong market interest in its AI defense and commercial applications.

- Surge in Trading Volume: The company's trading volume reached 65.2 million shares, nearly 23% above the three-month average of 51.6 million shares, reflecting renewed investor interest, particularly after a sharp sell-off.

- Long-Term Contracts Support: Palantir's business remains anchored by long-term government contracts, reinforced by the Pentagon's decision to designate the Maven Smart System as a program of record, which solidifies its position in the defense sector while its commercial business is expected to drive future growth.

- Market Focus on Future Contracts: Investors are looking for Palantir to quickly secure new commercial contracts to support its recovery rather than relying solely on defense deals, making its stock price highly sensitive to shifts in confidence regarding growth and competition.

Palantir Stock Rises 3.4% Amid Political Endorsements

- Stock Recovery: Palantir Technologies (PLTR) shares rose 3.4% to $132.37, reflecting investor optimism driven by political endorsements and ongoing ARK Invest purchases, highlighting market interest in its AI defense and commercial applications.

- Surge in Trading Volume: The company saw a trading volume of 65.2 million shares, nearly 23% above the three-month average of 51.6 million shares, indicating a significant increase in investor interest that may signal future market activity.

- Long-Term Contract Support: Palantir's business remains anchored by long-term government contracts, with the Pentagon designating the Maven Smart System as a program of record, further solidifying its position in the defense sector and expected to provide stable support for future growth.

- Commercial Growth Potential: Investors are keen to see if Palantir can quickly secure new commercial contracts to aid recovery rather than relying solely on defense deals, as the current stock price already reflects expectations of ongoing AI leadership, making it sensitive to any shifts in confidence.

C3.ai vs Palantir: A Financial Comparison

- C3.ai Revenue Decline: C3.ai reported a revenue of $53.3 million for the quarter ending January 2026, with a net income margin of -250%, indicating severe financial challenges during a leadership transition that could impact its competitive position.

- Palantir Revenue Growth: Palantir achieved approximately $1.4 billion in revenue for the quarter ending December 2025, with a net income margin of 43%, showcasing strong growth momentum in the AI software market and attracting more customer interest.

- Market Performance Comparison: C3.ai's stock fell by 3.36% to $8.48, while Palantir's stock decreased by 7.45% to $130.28, reflecting differing investor expectations regarding the future performance of the two companies.

- Competitive Position Disparity: C3.ai has reported GAAP net losses in every quarter over the past two years, highlighting its competitive disadvantage, whereas Palantir continues to grow, indicating significant potential and strong customer demand in the AI platform market.