AeroVironment Shares Decline Following Mixed Earnings Report

Earnings Report: AeroVironment, Inc. reported adjusted earnings per share of 44 cents, missing estimates, while revenue of $472.50 million exceeded expectations, reflecting a 151% year-over-year increase due to the BlueHalo acquisition.

Financial Challenges: The company experienced a net loss due to increased SG&A and R&D expenses, along with significant intangible amortization charges, leading to a decline in gross margin.

Guidance Update: For FY26, AeroVironment lowered its adjusted earnings per share guidance to between $3.40 and $3.55, while raising its revenue guidance to between $1.95 billion and $2.00 billion.

Market Reaction: Following the earnings report, AeroVironment shares fell by 12.12% to $247.24, with analyst Colin Canfield maintaining an Overweight rating but reducing the price target from $335 to $315.

Trade with 70% Backtested Accuracy

Analyst Views on AVAV

About AVAV

About the author

Red Cat Holdings Reports Mixed Earnings, Stock Plummets 17.8%

- Sales Beat Expectations: Red Cat Holdings reported Q4 sales of $26.2 million, exceeding analyst expectations of $20.9 million, with a staggering year-over-year growth of nearly 2,000%, indicating robust demand in the military drone sector, although overall profitability remains a concern.

- Increased Losses: Despite the sales surge, the company posted a quarterly loss of $0.17 per share, worse than the anticipated $0.14, reflecting high production costs that hinder the company's ability to transition to profitability.

- Annual Performance Review: For fiscal year 2025, Red Cat achieved total revenue of $40.7 million against a cost of goods sold of $39.4 million, resulting in gross profits; however, after accounting for operating expenses, the company reported a yearly loss of $0.73 per share, highlighting ongoing cost control challenges.

- Optimistic Future Outlook: CEO Jeff Thompson expressed optimism about future growth, noting that the company is securing multiple contracts and expanding production space to 254,000 square feet, although it remains uncertain when the company will achieve profitability despite strong sales momentum.

VisionWave's Strategic Move in Latin American Market

- Market Potential: The global counter-UAS market is projected to reach $14 billion by 2030, growing at an annual rate of 26.5%, indicating a rapid increase in demand for drone technology in border monitoring and public safety across Latin America.

- Successful Tech Demonstration: VisionWave conducted technology briefings with government representatives in Latin America, showcasing its autonomous aerial technologies for disaster response and public safety applications, successfully garnering attention despite no contracts being signed yet.

- Acquisition Plans Advance: VisionWave's subsidiary SolarDrone is set to acquire a 51% controlling interest in Israeli Junko Solar Ltd., entering a solar O&M market projected to reach $60 billion by 2035, providing a stable revenue layer for the company.

- Financing and Partnerships: VisionWave closed $20 million in senior financing in February and signed MOUs with German and Israeli firms to explore non-explosive interception systems, further enhancing its competitiveness in the international market.

AeroVironment Faces Investigation Amid Financial Losses

- Financial Losses: AeroVironment reported earnings per share of only $0.44 for Q2 FY2026, significantly below the consensus estimate of $0.80, resulting in a quarterly loss of $67.4 million, a stark contrast to a profit of $21.2 million in the same quarter last year, indicating a severe deterioration in the company's profitability.

- Declining Margins: The company's gross margin plummeted from 43% in the prior year to 20.9%, with cost of goods sold rising to 79% of revenue, highlighting significant challenges in cost management that could impact future profitability and market confidence.

- Rating Downgrade: On March 2, 2026, Raymond James downgraded AeroVironment from Strong Buy to Underperform, citing uncertainties surrounding the U.S. Space Force's SCAR program, which had an expected value of approximately $1.4 billion, now at risk of being paused or reassigned to new vendors, exacerbating concerns over the company's future revenue.

- Stock Price Volatility: Following the financial losses and rating downgrade, AeroVironment's stock price fell by 12.85% on December 10, 2025, and by 17.42% on March 2, 2026, reflecting strong investor concerns about the company's outlook and potentially leading to further capital outflows.

Nvidia Unveils Major GTC Updates

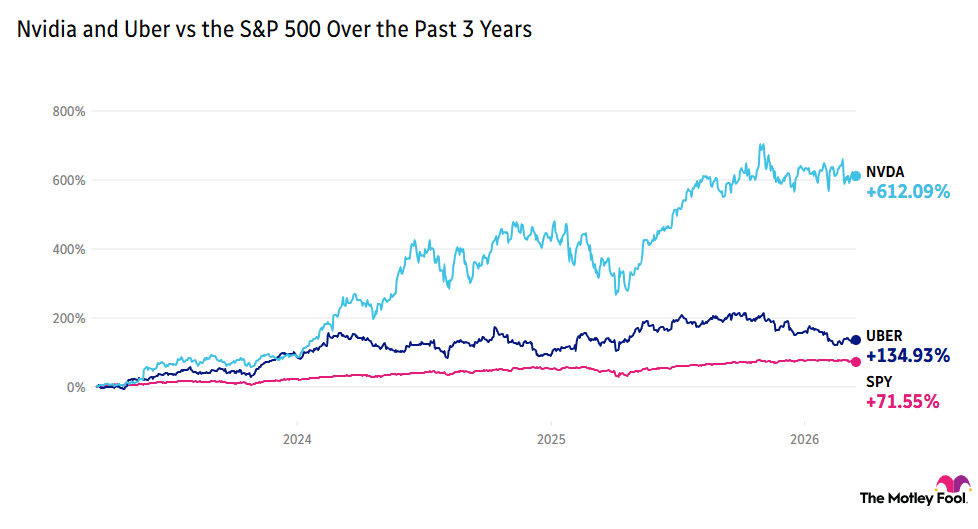

- Self-Driving Project Progress: Nvidia announced at the GTC conference that its joint self-driving car project with Uber is set to launch in 2027, with Los Angeles and San Francisco as testing cities, expanding to 28 cities, showcasing the company's strategic positioning and market potential in autonomous driving.

- AI Software Security Enhancement: The launch of the NemoClaw platform provides enhanced privacy and security controls for OpenClaw software, allowing self-evolving AI agents to be more scalable and trusted, further solidifying Nvidia's leadership in the AI sector.

- Alphabet Seeks Chinese Supply Chain: Alphabet is in discussions with Chinese suppliers for liquid cooling hardware to address tight supply in AI data center construction, with the liquid cooling market expected to grow from $8.9 billion in 2025 to $17 billion, highlighting the urgent demand for efficient cooling systems.

- Defense Stocks Rally: Defense stocks like AeroVironment and L3Harris Technologies rose over 2% following reports on low-cost weapon systems, indicating the market's growing interest in cost-effective technologies and increased investor confidence in the defense sector.

AeroVironment Acquires Empirical Systems Aerospace for Approximately $200 Million

- Acquisition Overview: AeroVironment announced the acquisition of leading unmanned aircraft systems producer Empirical Systems Aerospace for approximately $200 million, with about $160 million in stock and the remainder in cash, which is expected to positively impact adjusted EBITDA in the first year post-close.

- Subsidiary Integration: ESAero will operate as a subsidiary under AeroVironment's Precision Strike and Defense Systems group, enhancing production capabilities in loitering munitions, missiles, and drones, thereby strengthening the overall competitive position in these sectors.

- Employee Integration Plan: Following the acquisition, ESAero's leadership and employees are expected to integrate into AeroVironment's operations and culture, ensuring a smooth transition and fostering collaboration that enhances internal innovation capabilities.

- Financial Outlook Update: AeroVironment updated its FY26 guidance, projecting revenues between $1.85 billion and $1.95 billion, reflecting strong market demand amid the conclusion of the SCAR contract and accelerated commercial transition.

AeroVironment and Kratos Defense Growth Analysis

- Market Demand Surge: Defense stocks are experiencing a resurgence due to the Iran war and the Ukraine conflict, with AeroVironment and Kratos seeing stock price increases of 68% and 200%, respectively, indicating strong market demand for small drones and rapidly developed military technologies.

- Earnings Report Volatility: AeroVironment reported a loss of $0.06 per share in Q3 FY2026, despite a 143% year-over-year revenue increase to $4.08 million, primarily driven by the acquisition of BlueHalo, highlighting the company's potential in expanding its market presence in larger drones and space technology.

- Strong Growth Forecast: AeroVironment forecasts revenue between $1.85 billion and $1.95 billion for 2026, a significant increase from $820.6 million last year, with adjusted EBITDA expected to be between $265 million and $285 million, showcasing robust growth prospects in the defense sector.

- Acquisitions and Contracts: Kratos is in the process of acquiring Israeli company Orbit Technologies for $356.3 million and has secured a $7 million contract for a counter-UAS system, reflecting its strategic positioning and competitiveness in rapidly developing military technology.

Red Cat Holdings Reports Mixed Earnings, Stock Plummets 17.8%

- Sales Beat Expectations: Red Cat Holdings reported Q4 sales of $26.2 million, exceeding analyst expectations of $20.9 million, with a staggering year-over-year growth of nearly 2,000%, indicating robust demand in the military drone sector, although overall profitability remains a concern.

- Increased Losses: Despite the sales surge, the company posted a quarterly loss of $0.17 per share, worse than the anticipated $0.14, reflecting high production costs that hinder the company's ability to transition to profitability.

- Annual Performance Review: For fiscal year 2025, Red Cat achieved total revenue of $40.7 million against a cost of goods sold of $39.4 million, resulting in gross profits; however, after accounting for operating expenses, the company reported a yearly loss of $0.73 per share, highlighting ongoing cost control challenges.

- Optimistic Future Outlook: CEO Jeff Thompson expressed optimism about future growth, noting that the company is securing multiple contracts and expanding production space to 254,000 square feet, although it remains uncertain when the company will achieve profitability despite strong sales momentum.

VisionWave's Strategic Move in Latin American Market

- Market Potential: The global counter-UAS market is projected to reach $14 billion by 2030, growing at an annual rate of 26.5%, indicating a rapid increase in demand for drone technology in border monitoring and public safety across Latin America.

- Successful Tech Demonstration: VisionWave conducted technology briefings with government representatives in Latin America, showcasing its autonomous aerial technologies for disaster response and public safety applications, successfully garnering attention despite no contracts being signed yet.

- Acquisition Plans Advance: VisionWave's subsidiary SolarDrone is set to acquire a 51% controlling interest in Israeli Junko Solar Ltd., entering a solar O&M market projected to reach $60 billion by 2035, providing a stable revenue layer for the company.

- Financing and Partnerships: VisionWave closed $20 million in senior financing in February and signed MOUs with German and Israeli firms to explore non-explosive interception systems, further enhancing its competitiveness in the international market.

AeroVironment Faces Investigation Amid Financial Losses

- Financial Losses: AeroVironment reported earnings per share of only $0.44 for Q2 FY2026, significantly below the consensus estimate of $0.80, resulting in a quarterly loss of $67.4 million, a stark contrast to a profit of $21.2 million in the same quarter last year, indicating a severe deterioration in the company's profitability.

- Declining Margins: The company's gross margin plummeted from 43% in the prior year to 20.9%, with cost of goods sold rising to 79% of revenue, highlighting significant challenges in cost management that could impact future profitability and market confidence.

- Rating Downgrade: On March 2, 2026, Raymond James downgraded AeroVironment from Strong Buy to Underperform, citing uncertainties surrounding the U.S. Space Force's SCAR program, which had an expected value of approximately $1.4 billion, now at risk of being paused or reassigned to new vendors, exacerbating concerns over the company's future revenue.

- Stock Price Volatility: Following the financial losses and rating downgrade, AeroVironment's stock price fell by 12.85% on December 10, 2025, and by 17.42% on March 2, 2026, reflecting strong investor concerns about the company's outlook and potentially leading to further capital outflows.

Nvidia Unveils Major GTC Updates

- Self-Driving Project Progress: Nvidia announced at the GTC conference that its joint self-driving car project with Uber is set to launch in 2027, with Los Angeles and San Francisco as testing cities, expanding to 28 cities, showcasing the company's strategic positioning and market potential in autonomous driving.

- AI Software Security Enhancement: The launch of the NemoClaw platform provides enhanced privacy and security controls for OpenClaw software, allowing self-evolving AI agents to be more scalable and trusted, further solidifying Nvidia's leadership in the AI sector.

- Alphabet Seeks Chinese Supply Chain: Alphabet is in discussions with Chinese suppliers for liquid cooling hardware to address tight supply in AI data center construction, with the liquid cooling market expected to grow from $8.9 billion in 2025 to $17 billion, highlighting the urgent demand for efficient cooling systems.

- Defense Stocks Rally: Defense stocks like AeroVironment and L3Harris Technologies rose over 2% following reports on low-cost weapon systems, indicating the market's growing interest in cost-effective technologies and increased investor confidence in the defense sector.

AeroVironment Acquires Empirical Systems Aerospace for Approximately $200 Million

- Acquisition Overview: AeroVironment announced the acquisition of leading unmanned aircraft systems producer Empirical Systems Aerospace for approximately $200 million, with about $160 million in stock and the remainder in cash, which is expected to positively impact adjusted EBITDA in the first year post-close.

- Subsidiary Integration: ESAero will operate as a subsidiary under AeroVironment's Precision Strike and Defense Systems group, enhancing production capabilities in loitering munitions, missiles, and drones, thereby strengthening the overall competitive position in these sectors.

- Employee Integration Plan: Following the acquisition, ESAero's leadership and employees are expected to integrate into AeroVironment's operations and culture, ensuring a smooth transition and fostering collaboration that enhances internal innovation capabilities.

- Financial Outlook Update: AeroVironment updated its FY26 guidance, projecting revenues between $1.85 billion and $1.95 billion, reflecting strong market demand amid the conclusion of the SCAR contract and accelerated commercial transition.

AeroVironment and Kratos Defense Growth Analysis

- Market Demand Surge: Defense stocks are experiencing a resurgence due to the Iran war and the Ukraine conflict, with AeroVironment and Kratos seeing stock price increases of 68% and 200%, respectively, indicating strong market demand for small drones and rapidly developed military technologies.

- Earnings Report Volatility: AeroVironment reported a loss of $0.06 per share in Q3 FY2026, despite a 143% year-over-year revenue increase to $4.08 million, primarily driven by the acquisition of BlueHalo, highlighting the company's potential in expanding its market presence in larger drones and space technology.

- Strong Growth Forecast: AeroVironment forecasts revenue between $1.85 billion and $1.95 billion for 2026, a significant increase from $820.6 million last year, with adjusted EBITDA expected to be between $265 million and $285 million, showcasing robust growth prospects in the defense sector.

- Acquisitions and Contracts: Kratos is in the process of acquiring Israeli company Orbit Technologies for $356.3 million and has secured a $7 million contract for a counter-UAS system, reflecting its strategic positioning and competitiveness in rapidly developing military technology.