SpaceX Plans IPO with $1.75 Trillion Valuation

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 27 2026

0mins

Should l Buy WMT?

Source: Fool

- Market Valuation Analysis: SpaceX plans to go public with a valuation of $1.75 trillion, a figure that not only surpasses Tesla's market cap but also exceeds that of Walmart and Berkshire Hathaway, indicating strong market expectations for its future growth.

- Revenue and Valuation Ratio: Although SpaceX generated approximately $18.5 billion in revenue last year, leading to a price-to-sales ratio near 95, its potential Starlink business is projected to achieve $60 billion in annual revenue in the coming years, potentially lowering its P/S ratio to 29 and reflecting market recognition of its growth potential.

- Starlink User Growth: Starlink currently boasts over 10 million users globally, with projections of reaching 30 to 50 million users; if averaged at $100 per month, this could significantly boost Starlink's revenue, further supporting SpaceX's high valuation.

- Future Market Potential: SpaceX's Starship could unlock new markets such as asteroid mining, lunar bases, and space tourism, and if successful, could greatly enhance its market position, making the $1.75 trillion valuation seem like just the beginning.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy WMT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on WMT

Wall Street analysts forecast WMT stock price to fall

26 Analyst Rating

25 Buy

1 Hold

0 Sell

Strong Buy

Current: 131.450

Low

119.00

Averages

125.75

High

136.00

Current: 131.450

Low

119.00

Averages

125.75

High

136.00

About WMT

Walmart Inc. is a technology-powered omnichannel retailer. The Company is engaged in the operation of retail and wholesale stores and clubs, as well as eCommerce Websites and mobile applications, located throughout the United States (U.S.), Africa, Canada, Central America, Chile, China, India and Mexico. It operates in three reportable segments: Walmart U.S., Walmart International and Sam's Club U.S. The Walmart U.S. segment includes the Company's mass merchandising concept in the U.S., as well as eCommerce, which includes omni-channel initiatives and certain other business offerings such as advertising services. The Walmart International segment consists of the Company's operations outside of the U.S. through its subsidiaries, as well as eCommerce and omni-channel initiatives. The Sam's Club U.S. segment includes the warehouse membership clubs in the U.S., as well as samsclub.com and omni-channel initiatives.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Three High-Yield Safe Stocks to Consider

- Target Stock Recovery: Target's stock has risen 25% this year, yet it remains down over 40% in the past five years, indicating a significant valuation gap compared to rival Walmart, with expectations for future price increases, although economic conditions may delay this rebound.

- Bristol Myers Dividend Advantage: Bristol Myers offers a dividend yield of 4.4%, significantly higher than the S&P 500's 1.1%, and despite a 12% decline in stock price over the past five years, its free cash flow of $11.9 billion suggests it can sustain dividends while reducing debt.

- General Mills High-Yield Challenges: General Mills boasts a 7.4% dividend yield, but its stock has fallen 47% over the past five years, with projected organic net sales declines of 1.5% to 2% for the upcoming fiscal year; however, its free cash flow of $1.7 billion is sufficient to cover dividend payments, indicating financial resilience.

- Market Uncertainty: While all three stocks face unique challenges, the undervaluation of Target and Bristol Myers, along with their stable dividend payments, makes them attractive for long-term investment, particularly in the context of potential economic recovery.

See More

Retail Stocks Under Pressure as Earnings Reports Loom

- Retail Sector Decline: The S&P Retail Select Industry Index has dropped nearly 7% year-to-date, with the State Street SPDR S&P Retail ETF (XRT) following suit, indicating significant weakness in the retail sector and escalating investor concerns about consumer health.

- Consumer Sentiment Weakness: The University of Michigan's consumer sentiment survey hit an all-time low in May, reflecting a significant decline in consumer spending willingness under the pressures of high inflation and rising energy costs, which could adversely affect retailers' profitability.

- Pessimistic Earnings Outlook: Home Depot is expected to report first-quarter earnings per share of $3.41, while Lowe's and TJ Maxx are projected at $2.97 and $1.02 respectively, with analysts expressing skepticism about the retail sector's ability to achieve 20% earnings growth amid negative wage growth.

- Rising Consumer Credit Risks: The New York Fed reported that total household debt rose to $18.8 trillion in Q1, with credit card debt nearing all-time highs and personal savings rates dropping to 3.6%, indicating a deteriorating financial situation for consumers that may lead to further declines in demand.

See More

Analysis of Investment Prospects in AI Stocks

- SoundHound AI's Strong Earnings: SoundHound AI reported record revenue of $44.2 million for Q1 2026, a 52% increase year-over-year, yet the company maintained its full-year revenue guidance of $225-$260 million, indicating robust performance in the AI voice agent sector despite market expectations for an upward revision.

- Significant Acquisition Risks: SoundHound's planned $43 million all-stock acquisition of LivePerson raises concerns due to LivePerson's recent struggles, although management anticipates the deal could add $100 million in annual revenue by 2027, highlighting the execution risks involved in the integration process.

- Aurora's Growth Potential: Aurora Innovation focuses on autonomous trucking technology and expects over 200 driverless trucks to be operational by the end of 2026; despite only generating $3 million in revenue in 2025, the expansion of its agreement with Berkshire Hathaway's McLane indicates growing market confidence.

- High Market Volatility: Aurora's stock is more than two and a half times as volatile as the broader market, and while facing challenges like driver shortages and rising gas prices, its AI technology's application in complex scenarios could yield potential long-term gains for investors willing to endure the volatility.

See More

Trump Warns Iran of Possible Conflict Resurgence

- Oil Price Surge: Trump's social media comments urging Iran to 'get moving' have led to a spike in oil prices overnight, raising concerns about a potential resurgence of conflict that could destabilize global energy markets.

- Market Volatility: Following Trump's remarks, stock futures have fallen, setting Wall Street up for another day of significant losses, highlighting the direct impact of political factors on market sentiment.

- Delta Air Lines Investment: Berkshire Hathaway's announcement of a $2.6 billion stake in Delta Air Lines, making it the company's 14th largest holding, reflects confidence in the airline industry's recovery and may drive Delta's stock price higher.

- Meta Layoff Plans: Meta is expected to lay off about 10% of its workforce this week, amidst widespread layoffs in the tech sector, which could dampen employee morale and underscores the company's urgent need for cost control.

See More

Trump Warns Iran Amid Rising Tensions

- Oil Price Surge: Trump's statement urging Iran to 'get moving' has led to a sharp increase in oil prices overnight, raising concerns that the conflict could reignite, which may impact global energy markets and investor confidence.

- Market Volatility: Following Trump's comments, stock futures fell, setting Wall Street up for potentially significant losses again, despite the S&P 500 managing to achieve its seventh consecutive winning week, indicating market fragility.

- Delta Airlines Stock Rise: Delta Airlines shares rose over 2% before the bell after Berkshire Hathaway revealed a $2.6 billion stake in the carrier, marking a return to the airline sector and potentially boosting market confidence in airline stocks.

- Lululemon's Shareholder Pressure: Lululemon's letter to shareholders criticized founder Chip Wilson's outdated views, which could derail the company's turnaround plan, urging shareholders to support its strategy at the upcoming annual meeting, highlighting the urgency of corporate governance issues.

See More

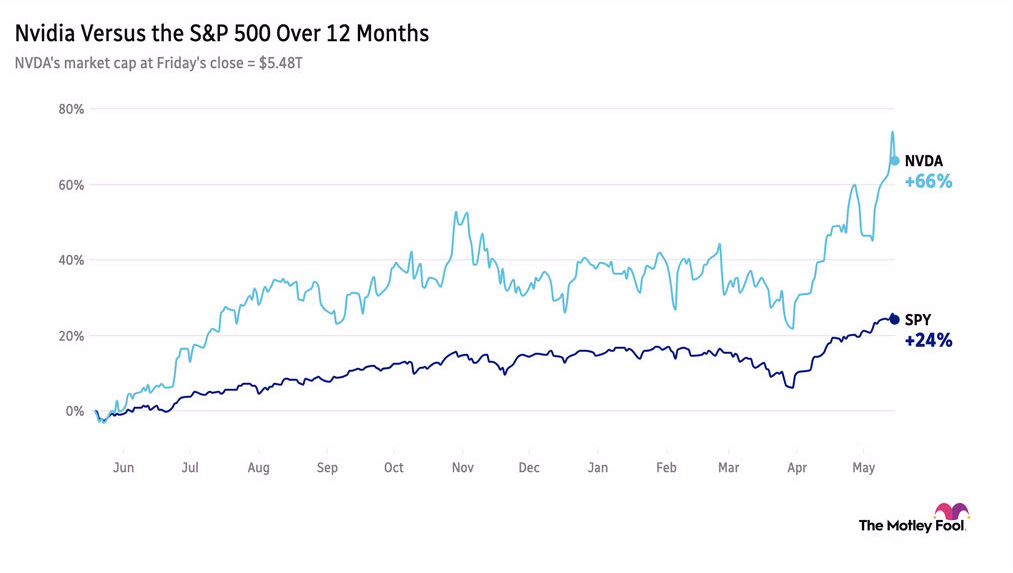

Nvidia Earnings in Focus as Market Reacts Mutedly

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More

Three High-Yield Safe Stocks to Consider

- Target Stock Recovery: Target's stock has risen 25% this year, yet it remains down over 40% in the past five years, indicating a significant valuation gap compared to rival Walmart, with expectations for future price increases, although economic conditions may delay this rebound.

- Bristol Myers Dividend Advantage: Bristol Myers offers a dividend yield of 4.4%, significantly higher than the S&P 500's 1.1%, and despite a 12% decline in stock price over the past five years, its free cash flow of $11.9 billion suggests it can sustain dividends while reducing debt.

- General Mills High-Yield Challenges: General Mills boasts a 7.4% dividend yield, but its stock has fallen 47% over the past five years, with projected organic net sales declines of 1.5% to 2% for the upcoming fiscal year; however, its free cash flow of $1.7 billion is sufficient to cover dividend payments, indicating financial resilience.

- Market Uncertainty: While all three stocks face unique challenges, the undervaluation of Target and Bristol Myers, along with their stable dividend payments, makes them attractive for long-term investment, particularly in the context of potential economic recovery.

See More

Retail Stocks Under Pressure as Earnings Reports Loom

- Retail Sector Decline: The S&P Retail Select Industry Index has dropped nearly 7% year-to-date, with the State Street SPDR S&P Retail ETF (XRT) following suit, indicating significant weakness in the retail sector and escalating investor concerns about consumer health.

- Consumer Sentiment Weakness: The University of Michigan's consumer sentiment survey hit an all-time low in May, reflecting a significant decline in consumer spending willingness under the pressures of high inflation and rising energy costs, which could adversely affect retailers' profitability.

- Pessimistic Earnings Outlook: Home Depot is expected to report first-quarter earnings per share of $3.41, while Lowe's and TJ Maxx are projected at $2.97 and $1.02 respectively, with analysts expressing skepticism about the retail sector's ability to achieve 20% earnings growth amid negative wage growth.

- Rising Consumer Credit Risks: The New York Fed reported that total household debt rose to $18.8 trillion in Q1, with credit card debt nearing all-time highs and personal savings rates dropping to 3.6%, indicating a deteriorating financial situation for consumers that may lead to further declines in demand.

See More

Analysis of Investment Prospects in AI Stocks

- SoundHound AI's Strong Earnings: SoundHound AI reported record revenue of $44.2 million for Q1 2026, a 52% increase year-over-year, yet the company maintained its full-year revenue guidance of $225-$260 million, indicating robust performance in the AI voice agent sector despite market expectations for an upward revision.

- Significant Acquisition Risks: SoundHound's planned $43 million all-stock acquisition of LivePerson raises concerns due to LivePerson's recent struggles, although management anticipates the deal could add $100 million in annual revenue by 2027, highlighting the execution risks involved in the integration process.

- Aurora's Growth Potential: Aurora Innovation focuses on autonomous trucking technology and expects over 200 driverless trucks to be operational by the end of 2026; despite only generating $3 million in revenue in 2025, the expansion of its agreement with Berkshire Hathaway's McLane indicates growing market confidence.

- High Market Volatility: Aurora's stock is more than two and a half times as volatile as the broader market, and while facing challenges like driver shortages and rising gas prices, its AI technology's application in complex scenarios could yield potential long-term gains for investors willing to endure the volatility.

See More

Trump Warns Iran of Possible Conflict Resurgence

- Oil Price Surge: Trump's social media comments urging Iran to 'get moving' have led to a spike in oil prices overnight, raising concerns about a potential resurgence of conflict that could destabilize global energy markets.

- Market Volatility: Following Trump's remarks, stock futures have fallen, setting Wall Street up for another day of significant losses, highlighting the direct impact of political factors on market sentiment.

- Delta Air Lines Investment: Berkshire Hathaway's announcement of a $2.6 billion stake in Delta Air Lines, making it the company's 14th largest holding, reflects confidence in the airline industry's recovery and may drive Delta's stock price higher.

- Meta Layoff Plans: Meta is expected to lay off about 10% of its workforce this week, amidst widespread layoffs in the tech sector, which could dampen employee morale and underscores the company's urgent need for cost control.

See More

Trump Warns Iran Amid Rising Tensions

- Oil Price Surge: Trump's statement urging Iran to 'get moving' has led to a sharp increase in oil prices overnight, raising concerns that the conflict could reignite, which may impact global energy markets and investor confidence.

- Market Volatility: Following Trump's comments, stock futures fell, setting Wall Street up for potentially significant losses again, despite the S&P 500 managing to achieve its seventh consecutive winning week, indicating market fragility.

- Delta Airlines Stock Rise: Delta Airlines shares rose over 2% before the bell after Berkshire Hathaway revealed a $2.6 billion stake in the carrier, marking a return to the airline sector and potentially boosting market confidence in airline stocks.

- Lululemon's Shareholder Pressure: Lululemon's letter to shareholders criticized founder Chip Wilson's outdated views, which could derail the company's turnaround plan, urging shareholders to support its strategy at the upcoming annual meeting, highlighting the urgency of corporate governance issues.

See More

Nvidia Earnings in Focus as Market Reacts Mutedly

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More