ServiceNow Faces AI Transition Challenges and Opportunities

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy NOW?

Source: Fool

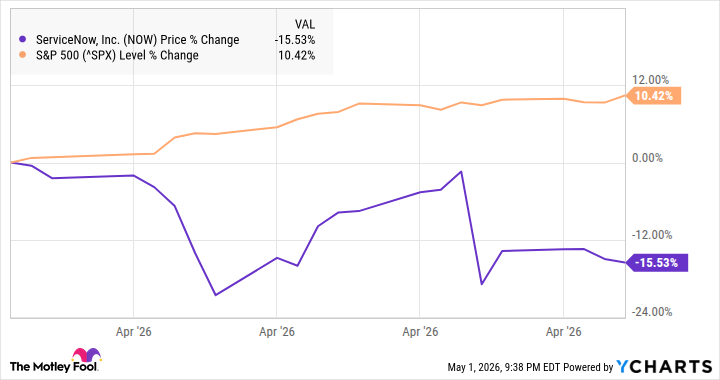

- Stock Price Decline: ServiceNow's stock plummeted 18% following its latest earnings report, now down 62.4% from its all-time high, reflecting investor concerns over AI's impact on the software sector, which may pressure future revenues and profits.

- Strong Revenue Growth: Despite challenges, ServiceNow reported a 22% year-over-year revenue increase, with remaining contract obligations growing by 25%, indicating robust market demand and a solid business foundation among large enterprises.

- AI Control Tower Launch: In May 2025, ServiceNow unveiled its AI Control Tower, enabling enterprises to manage AI agents, enhancing its competitiveness in the AI era, and demonstrating foresight by preparing the product before the surge in AI agent usage.

- Subscription Model Adjustment: Management noted that approximately 50% of new contracts are now sold on a usage basis rather than traditional seat subscriptions, a shift that could help ServiceNow sustain growth in the AI era and mitigate revenue risks associated with increased efficiency.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NOW?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NOW

Wall Street analysts forecast NOW stock price to rise

32 Analyst Rating

30 Buy

2 Hold

0 Sell

Strong Buy

Current: 88.310

Low

172.00

Averages

222.81

High

263.00

Current: 88.310

Low

172.00

Averages

222.81

High

263.00

About NOW

ServiceNow, Inc. provides an artificial intelligence (AI) platform for business transformation. The Company’s AI platform connects people, processes, data, and devices to increase productivity and maximize business outcomes. Its intelligent platform, the Now Platform, is a cloud-based solution that helps enterprises and organizations across public and private sectors digitize workflows. The workflow applications built on the Now Platform are organized into four primary areas: Technology, CRM and Industry, Core Business and Creator. Its products include IT Service Management, IT Operations Management, HR Service Delivery, ServiceNow AI Agents, AI Experience, Build Agent, ServiceNow AI Control Tower, AI Agent Fabric, RaptorDB, Workflow Data Fabric, Workplace Service Delivery, ServiceNow Platform Encryption, Telecommunications Service Operations Management, and others. The Company also offers identity security, helping organizations secure access across the enterprise.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

ServiceNow Faces AI Transition Challenges and Opportunities

- Stock Price Decline: ServiceNow's stock plummeted 18% following its latest earnings report, now down 62.4% from its all-time high, reflecting investor concerns over AI's impact on the software sector, which may pressure future revenues and profits.

- Strong Revenue Growth: Despite challenges, ServiceNow reported a 22% year-over-year revenue increase, with remaining contract obligations growing by 25%, indicating robust market demand and a solid business foundation among large enterprises.

- AI Control Tower Launch: In May 2025, ServiceNow unveiled its AI Control Tower, enabling enterprises to manage AI agents, enhancing its competitiveness in the AI era, and demonstrating foresight by preparing the product before the surge in AI agent usage.

- Subscription Model Adjustment: Management noted that approximately 50% of new contracts are now sold on a usage basis rather than traditional seat subscriptions, a shift that could help ServiceNow sustain growth in the AI era and mitigate revenue risks associated with increased efficiency.

See More

ServiceNow Shares Decline Amid AI Concerns

- Stock Decline: ServiceNow's shares fell by 15.5% last month, despite beating first-quarter estimates, indicating investor concerns about the sustainability of its business model amid broader software stock fears.

- AI Model Impact: The stock initially dropped in the second week of April following the announcement of its Mythos AI model, which was deemed too powerful and potentially exploitable, highlighting challenges in the AI sector for the company.

- Rating Downgrade: UBS downgraded ServiceNow from 'Buy' to 'Neutral', citing diminishing competitive advantages in application software, which contributed to further stock declines and reflected market concerns over budget pressures.

- Margin Pressure: Although first-quarter results met expectations, gross margins fell from 79% to 75%, indicating ongoing margin pressure as the company transitions from a seat-based model to AI products, which may affect future profitability.

See More

Anthropic's Mythos AI Triggers Software Sector Sell-Off

- Sector Sell-Off: The introduction of Anthropic's Mythos AI has triggered a sell-off in the software sector, with ServiceNow's stock falling 15.5% last month, reflecting investor concerns about the sustainability of its business model despite beating Q1 expectations.

- Margin Compression: ServiceNow's gross margin decreased from 79% to 75%, indicating profit pressure as the company pivots towards AI products, which may impact its future profitability and competitive position in the market.

- Market Reaction Volatility: Following the announcement of the Mythos AI model, ServiceNow's stock experienced two waves of decline, first due to market concerns over the new product and then again after UBS downgraded its rating from buy to neutral, highlighting a lack of confidence in its future growth.

- Investor Confidence Erosion: Although ServiceNow's revenue continues to grow at 20%, its price-to-earnings ratio stands at 54, leading to investor doubts about its ability to sustain this growth rate, which is causing its competitive edge in the software industry to diminish.

See More

ServiceNow Shares Drop 16% Amid AI Concerns

- Stock Price Decline: ServiceNow's shares fell by 15.5% in April, primarily due to investor skepticism regarding the sustainability of its business model, despite beating earnings estimates in the first quarter, which failed to alleviate concerns.

- AI Model Impact: The announcement of ServiceNow's Mythos AI model, deemed too powerful to be released publicly due to cybersecurity vulnerabilities, led to a significant stock drop in the second week of April, reflecting market apprehension about its AI products.

- Rating Downgrade Effects: UBS downgraded ServiceNow from 'Buy' to 'Neutral', citing diminished competitive advantages in the application software sector, which further fueled investor doubts about its future growth prospects.

- Margin Pressure: Although ServiceNow reported a 20% year-over-year revenue growth, its gross margin decreased from 79% to 75%, indicating the profit margin pressures faced during its transition to AI products, which could impact long-term profitability.

See More

U.S. Stocks Close: S&P 500 Hits All-Time High

- S&P 500 Strong Performance: The S&P 500 index rose by 0.29%, reaching an all-time high, driven by Apple's forecast of stronger-than-expected Q2 revenue, which boosted market sentiment and indicated increased investor confidence in tech stocks.

- Atlassian Stock Surge: Atlassian's stock soared over 29% after reporting Q3 revenue of $1.79 billion, exceeding the market expectation of $1.69 billion, highlighting a robust recovery in the software sector that may attract more investor interest.

- Oil Price Volatility Impacting Markets: WTI crude oil prices fell more than 3%, easing inflation concerns, although trade tensions resurfaced with President Trump's threat to raise tariffs on EU auto imports, potentially negatively affecting market sentiment.

- Economic Data Influencing Stocks: The April ISM manufacturing index remained unchanged at 52.7, below the expected 53.2, indicating signs of economic slowdown, despite the majority of companies reporting Q1 earnings that exceeded expectations, leaving the overall market facing uncertainty.

See More

Mixed Performance in US Indices as Apple’s Strong Earnings Boost Market

- Apple's Strong Earnings: Apple Inc. (AAPL) reported Q2 revenue of $111.18 billion, exceeding the consensus of $109.66 billion, and forecasted Q3 revenue growth of 14% to 17%, significantly above the expected 9.1%, which propelled the Dow Jones Industrial Average up over 4%.

- Software Stocks Surge: Atlassian (TEAM) posted Q3 revenue of $1.79 billion, surpassing the consensus of $1.69 billion, leading to a stock price increase of over 20%, which not only boosted the software sector but also enhanced investor confidence in tech stocks.

- Oil Price Volatility: WTI crude oil prices fell more than 3% due to developments in the US-Iran agreement, temporarily easing inflation concerns and contributing to stock market gains, highlighting the energy market's influence on the overall economy.

- Weak Manufacturing Data: The April ISM manufacturing index remained unchanged at 52.7, below the expected 53.2, while the prices paid sub-index rose to a four-year high of 84.6, indicating increasing price pressures that could impact Federal Reserve policy decisions.

See More

ServiceNow Faces AI Transition Challenges and Opportunities

- Stock Price Decline: ServiceNow's stock plummeted 18% following its latest earnings report, now down 62.4% from its all-time high, reflecting investor concerns over AI's impact on the software sector, which may pressure future revenues and profits.

- Strong Revenue Growth: Despite challenges, ServiceNow reported a 22% year-over-year revenue increase, with remaining contract obligations growing by 25%, indicating robust market demand and a solid business foundation among large enterprises.

- AI Control Tower Launch: In May 2025, ServiceNow unveiled its AI Control Tower, enabling enterprises to manage AI agents, enhancing its competitiveness in the AI era, and demonstrating foresight by preparing the product before the surge in AI agent usage.

- Subscription Model Adjustment: Management noted that approximately 50% of new contracts are now sold on a usage basis rather than traditional seat subscriptions, a shift that could help ServiceNow sustain growth in the AI era and mitigate revenue risks associated with increased efficiency.

See More

ServiceNow Shares Decline Amid AI Concerns

- Stock Decline: ServiceNow's shares fell by 15.5% last month, despite beating first-quarter estimates, indicating investor concerns about the sustainability of its business model amid broader software stock fears.

- AI Model Impact: The stock initially dropped in the second week of April following the announcement of its Mythos AI model, which was deemed too powerful and potentially exploitable, highlighting challenges in the AI sector for the company.

- Rating Downgrade: UBS downgraded ServiceNow from 'Buy' to 'Neutral', citing diminishing competitive advantages in application software, which contributed to further stock declines and reflected market concerns over budget pressures.

- Margin Pressure: Although first-quarter results met expectations, gross margins fell from 79% to 75%, indicating ongoing margin pressure as the company transitions from a seat-based model to AI products, which may affect future profitability.

See More

Anthropic's Mythos AI Triggers Software Sector Sell-Off

- Sector Sell-Off: The introduction of Anthropic's Mythos AI has triggered a sell-off in the software sector, with ServiceNow's stock falling 15.5% last month, reflecting investor concerns about the sustainability of its business model despite beating Q1 expectations.

- Margin Compression: ServiceNow's gross margin decreased from 79% to 75%, indicating profit pressure as the company pivots towards AI products, which may impact its future profitability and competitive position in the market.

- Market Reaction Volatility: Following the announcement of the Mythos AI model, ServiceNow's stock experienced two waves of decline, first due to market concerns over the new product and then again after UBS downgraded its rating from buy to neutral, highlighting a lack of confidence in its future growth.

- Investor Confidence Erosion: Although ServiceNow's revenue continues to grow at 20%, its price-to-earnings ratio stands at 54, leading to investor doubts about its ability to sustain this growth rate, which is causing its competitive edge in the software industry to diminish.

See More

ServiceNow Shares Drop 16% Amid AI Concerns

- Stock Price Decline: ServiceNow's shares fell by 15.5% in April, primarily due to investor skepticism regarding the sustainability of its business model, despite beating earnings estimates in the first quarter, which failed to alleviate concerns.

- AI Model Impact: The announcement of ServiceNow's Mythos AI model, deemed too powerful to be released publicly due to cybersecurity vulnerabilities, led to a significant stock drop in the second week of April, reflecting market apprehension about its AI products.

- Rating Downgrade Effects: UBS downgraded ServiceNow from 'Buy' to 'Neutral', citing diminished competitive advantages in the application software sector, which further fueled investor doubts about its future growth prospects.

- Margin Pressure: Although ServiceNow reported a 20% year-over-year revenue growth, its gross margin decreased from 79% to 75%, indicating the profit margin pressures faced during its transition to AI products, which could impact long-term profitability.

See More

U.S. Stocks Close: S&P 500 Hits All-Time High

- S&P 500 Strong Performance: The S&P 500 index rose by 0.29%, reaching an all-time high, driven by Apple's forecast of stronger-than-expected Q2 revenue, which boosted market sentiment and indicated increased investor confidence in tech stocks.

- Atlassian Stock Surge: Atlassian's stock soared over 29% after reporting Q3 revenue of $1.79 billion, exceeding the market expectation of $1.69 billion, highlighting a robust recovery in the software sector that may attract more investor interest.

- Oil Price Volatility Impacting Markets: WTI crude oil prices fell more than 3%, easing inflation concerns, although trade tensions resurfaced with President Trump's threat to raise tariffs on EU auto imports, potentially negatively affecting market sentiment.

- Economic Data Influencing Stocks: The April ISM manufacturing index remained unchanged at 52.7, below the expected 53.2, indicating signs of economic slowdown, despite the majority of companies reporting Q1 earnings that exceeded expectations, leaving the overall market facing uncertainty.

See More

Mixed Performance in US Indices as Apple’s Strong Earnings Boost Market

- Apple's Strong Earnings: Apple Inc. (AAPL) reported Q2 revenue of $111.18 billion, exceeding the consensus of $109.66 billion, and forecasted Q3 revenue growth of 14% to 17%, significantly above the expected 9.1%, which propelled the Dow Jones Industrial Average up over 4%.

- Software Stocks Surge: Atlassian (TEAM) posted Q3 revenue of $1.79 billion, surpassing the consensus of $1.69 billion, leading to a stock price increase of over 20%, which not only boosted the software sector but also enhanced investor confidence in tech stocks.

- Oil Price Volatility: WTI crude oil prices fell more than 3% due to developments in the US-Iran agreement, temporarily easing inflation concerns and contributing to stock market gains, highlighting the energy market's influence on the overall economy.

- Weak Manufacturing Data: The April ISM manufacturing index remained unchanged at 52.7, below the expected 53.2, while the prices paid sub-index rose to a four-year high of 84.6, indicating increasing price pressures that could impact Federal Reserve policy decisions.

See More