Projected Target Price for VONG Analysts: $139

Vanguard Russell 1000 Growth ETF Analysis: The Vanguard Russell 1000 Growth ETF (VONG) has an implied analyst target price of $138.70 per unit, indicating a potential upside of 10.53% from its current trading price of $125.49.

Notable Holdings with Upside Potential: Key underlying holdings of VONG, such as AAON, Alnylam Pharmaceuticals, and H & R Block, show significant upside potential based on analyst target prices, with expected increases of 12.25%, 11.38%, and 11.27% respectively.

Analyst Target Price Justification: The article raises questions about whether analysts' target prices are justified or overly optimistic, suggesting that high targets could lead to future downgrades if they do not align with recent developments.

Investor Research Recommendation: Investors are encouraged to conduct further research to assess the validity of analyst targets and their alignment with current company and industry trends.

Trade with 70% Backtested Accuracy

Analyst Views on ALNY

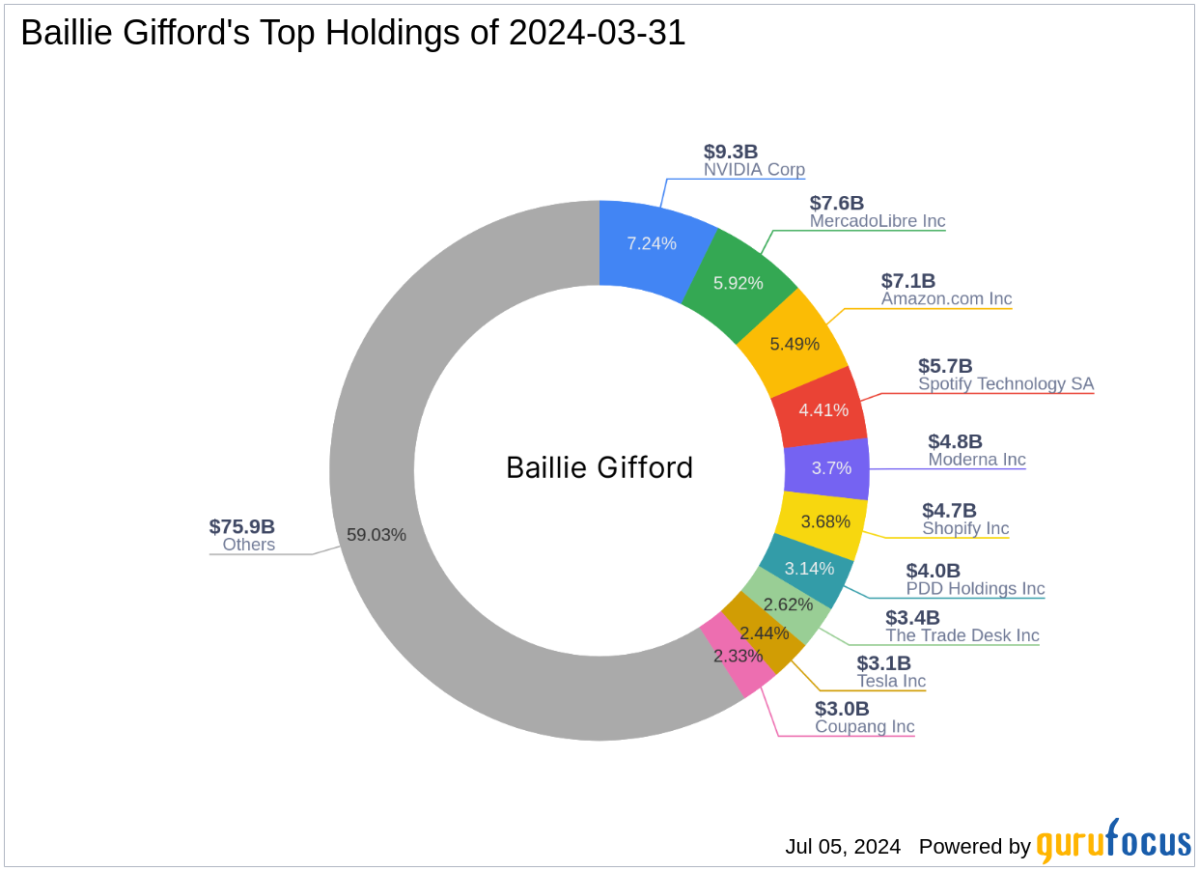

About ALNY

About the author

Alnylam Pharmaceuticals Shares Drop 24%, Yet Optimism Persists

- Significant Revenue Growth: Alnylam Pharmaceuticals reported a 121% year-over-year surge in product revenue to $1.04 billion in Q1, primarily driven by a 153% increase in its ATTR franchise, indicating strong market demand in the rare disease treatment sector.

- Profitability Improvement: The company achieved earnings per share (EPS) of $1.51, a substantial turnaround from a loss of $0.14 per share in the same period last year, demonstrating Alnylam's rapid transition into a profitable commercial powerhouse, which boosts investor confidence.

- Expansion into New Indications: New data for Alnylam's Amvuttra reinforces its position as a first-line treatment for cardiomyopathy, setting the stage for a massive commercial launch and further market share expansion.

- Strong Technological Moat: Alnylam's RNA interference platform creates a deep technological moat, and its collaboration with Inceptive Nucleics on AI accelerates the discovery of next-generation RNAi structures, ensuring its competitive edge in the biotech industry.

Alnylam Pharmaceuticals Reports Strong Q1 Performance

- Significant Revenue Growth: Alnylam Pharmaceuticals reported a 121% year-over-year surge in product revenue to $1.04 billion in Q1, primarily driven by a 153% increase in its transthyretin amyloidosis (ATTR) franchise, indicating strong market demand in the rare disease treatment sector.

- Profitability Improvement: The company achieved earnings per share (EPS) of $1.51, a substantial turnaround from a loss of $0.14 per share in the same period last year, marking a significant improvement in profitability and showcasing its transition from a high-burn clinical biotech to a profitable commercial powerhouse.

- Broad Market Outlook: Alnylam's guidance for full-year 2026 net product revenue ranges between $4.9 billion and $5.3 billion, reflecting a 71% year-over-year growth at the midpoint, highlighting the company's potential to penetrate mainstream high-volume therapeutic markets, particularly in cardiomyopathy and hypertension.

- Strong Technological Moat: Alnylam's RNA interference (RNAi) drug delivery system creates a deep technological moat, and its strategic AI collaboration with Inceptive Nucleics accelerates the discovery of next-generation RNAi structures, ensuring the company's competitive edge in the rapidly evolving biotech landscape.

Komodo Expands Partnership with Alnylam to Enhance AI Decision-Making

- Partnership Expansion: Komodo Health has expanded its strategic partnership with Alnylam Pharmaceuticals to scale the Marmot analytics platform across key enterprise functions, enhancing AI-driven decision-making and improving overall operational efficiency.

- Real-Time Intelligence Transformation: The Marmot platform, built on the Healthcare Map, integrates over 330 million de-identified patient journeys, enabling Alnylam to break free from fragmented analytics and achieve real-time, transparent healthcare intelligence, significantly reducing reporting cycles from months to hours.

- New Feature Launch: Komodo has released new capabilities for Marmot aimed at making healthcare intelligence accessible to all users, ensuring that every analysis is reproducible and verifiable, thereby enhancing the scientific rigor and accuracy of decision-making while embedding AI into core enterprise processes.

- Industry Transformation Trend: This partnership reflects a broader shift in healthcare and life sciences, as organizations move beyond mere AI experimentation to adopt new operating models centered around real-time intelligence, addressing increasingly complex market demands.

Regeneron's Cemdisiran Marketing Applications Accepted by U.S. and European Regulators

- Drug Application Progress: Regeneron (REGN) and Alnylam Pharmaceuticals (ALNY) have had their marketing applications for the experimental therapy cemdisiran accepted by U.S. and European regulators, marking a significant advancement in treating myasthenia gravis.

- Priority Review Approval: The U.S. FDA has issued a priority review for cemdisiran's New Drug Application with a target action date in November, which will expedite the drug's market entry and is expected to significantly enhance Regeneron's competitive position.

- European Market Outlook: The European Medicines Agency has accepted the marketing authorization application for cemdisiran, with final approval from the European Commission anticipated in H2 2027, laying the groundwork for Regeneron's expansion in the European market.

- Clinical Trial Results: Based on 24-week data, Regeneron announced in August that the treatment arm testing cemdisiran as a single agent in adults with symptomatic myasthenia gravis met the primary goals of the NIMBLE trial, further validating the drug's efficacy and safety.

Dyne Therapeutics Appoints Barry Greene to Board of Directors

- New Board Appointment: Dyne Therapeutics has appointed Barry Greene to its Board of Directors, bringing over 30 years of biopharmaceutical experience focused on the development and commercialization of therapies for rare diseases, neuroscience, and oncology, which is expected to provide strategic guidance for the company.

- Rich Leadership Experience: Greene currently serves as the lead independent director at Karyopharm Therapeutics and has been on the Board since 2013, and his extensive leadership experience will aid Dyne in navigating the complex biopharmaceutical market.

- Former CEO Background: Greene previously held the position of CEO at Sage Therapeutics from December 2020 to July 2025, and his expertise in drug development and commercialization will support Dyne's future growth initiatives.

- Positive Stock Performance: Dyne shares closed at $20.87 on Monday, reflecting a 5.40% increase, indicating a positive market reaction to the new appointment, which may enhance investor confidence and drive future growth.

Alnylam to Host 10th RNAi Roundtable Series

- RNAi Roundtable Series: Alnylam Pharmaceuticals announced its plan to host the 10th series of 'RNAi Roundtable' webinars in the coming months, featuring presentations from scientists and medical experts discussing recent advancements in the company's pipeline programs to address unmet clinical needs.

- Live Webcast Arrangement: Each event will be webcast live on the company's investor website, with replays available approximately three hours after each session, ensuring timely access to critical information for investors.

- 2030 Strategic Goals: Alnylam aims to increase its clinical programs from over 25 to more than 40 by 2030, demonstrating its commitment to sustainable innovation and market expansion in the RNAi therapeutics sector.

- Increased R&D Investment: The company is significantly ramping up its R&D investments to extend the application of RNAi technology, aiming to deliver multiple new transformative medicines for patients with serious diseases, thereby reinforcing its market leadership position.

Alnylam Pharmaceuticals Shares Drop 24%, Yet Optimism Persists

- Significant Revenue Growth: Alnylam Pharmaceuticals reported a 121% year-over-year surge in product revenue to $1.04 billion in Q1, primarily driven by a 153% increase in its ATTR franchise, indicating strong market demand in the rare disease treatment sector.

- Profitability Improvement: The company achieved earnings per share (EPS) of $1.51, a substantial turnaround from a loss of $0.14 per share in the same period last year, demonstrating Alnylam's rapid transition into a profitable commercial powerhouse, which boosts investor confidence.

- Expansion into New Indications: New data for Alnylam's Amvuttra reinforces its position as a first-line treatment for cardiomyopathy, setting the stage for a massive commercial launch and further market share expansion.

- Strong Technological Moat: Alnylam's RNA interference platform creates a deep technological moat, and its collaboration with Inceptive Nucleics on AI accelerates the discovery of next-generation RNAi structures, ensuring its competitive edge in the biotech industry.

Alnylam Pharmaceuticals Reports Strong Q1 Performance

- Significant Revenue Growth: Alnylam Pharmaceuticals reported a 121% year-over-year surge in product revenue to $1.04 billion in Q1, primarily driven by a 153% increase in its transthyretin amyloidosis (ATTR) franchise, indicating strong market demand in the rare disease treatment sector.

- Profitability Improvement: The company achieved earnings per share (EPS) of $1.51, a substantial turnaround from a loss of $0.14 per share in the same period last year, marking a significant improvement in profitability and showcasing its transition from a high-burn clinical biotech to a profitable commercial powerhouse.

- Broad Market Outlook: Alnylam's guidance for full-year 2026 net product revenue ranges between $4.9 billion and $5.3 billion, reflecting a 71% year-over-year growth at the midpoint, highlighting the company's potential to penetrate mainstream high-volume therapeutic markets, particularly in cardiomyopathy and hypertension.

- Strong Technological Moat: Alnylam's RNA interference (RNAi) drug delivery system creates a deep technological moat, and its strategic AI collaboration with Inceptive Nucleics accelerates the discovery of next-generation RNAi structures, ensuring the company's competitive edge in the rapidly evolving biotech landscape.

Komodo Expands Partnership with Alnylam to Enhance AI Decision-Making

- Partnership Expansion: Komodo Health has expanded its strategic partnership with Alnylam Pharmaceuticals to scale the Marmot analytics platform across key enterprise functions, enhancing AI-driven decision-making and improving overall operational efficiency.

- Real-Time Intelligence Transformation: The Marmot platform, built on the Healthcare Map, integrates over 330 million de-identified patient journeys, enabling Alnylam to break free from fragmented analytics and achieve real-time, transparent healthcare intelligence, significantly reducing reporting cycles from months to hours.

- New Feature Launch: Komodo has released new capabilities for Marmot aimed at making healthcare intelligence accessible to all users, ensuring that every analysis is reproducible and verifiable, thereby enhancing the scientific rigor and accuracy of decision-making while embedding AI into core enterprise processes.

- Industry Transformation Trend: This partnership reflects a broader shift in healthcare and life sciences, as organizations move beyond mere AI experimentation to adopt new operating models centered around real-time intelligence, addressing increasingly complex market demands.

Regeneron's Cemdisiran Marketing Applications Accepted by U.S. and European Regulators

- Drug Application Progress: Regeneron (REGN) and Alnylam Pharmaceuticals (ALNY) have had their marketing applications for the experimental therapy cemdisiran accepted by U.S. and European regulators, marking a significant advancement in treating myasthenia gravis.

- Priority Review Approval: The U.S. FDA has issued a priority review for cemdisiran's New Drug Application with a target action date in November, which will expedite the drug's market entry and is expected to significantly enhance Regeneron's competitive position.

- European Market Outlook: The European Medicines Agency has accepted the marketing authorization application for cemdisiran, with final approval from the European Commission anticipated in H2 2027, laying the groundwork for Regeneron's expansion in the European market.

- Clinical Trial Results: Based on 24-week data, Regeneron announced in August that the treatment arm testing cemdisiran as a single agent in adults with symptomatic myasthenia gravis met the primary goals of the NIMBLE trial, further validating the drug's efficacy and safety.

Dyne Therapeutics Appoints Barry Greene to Board of Directors

- New Board Appointment: Dyne Therapeutics has appointed Barry Greene to its Board of Directors, bringing over 30 years of biopharmaceutical experience focused on the development and commercialization of therapies for rare diseases, neuroscience, and oncology, which is expected to provide strategic guidance for the company.

- Rich Leadership Experience: Greene currently serves as the lead independent director at Karyopharm Therapeutics and has been on the Board since 2013, and his extensive leadership experience will aid Dyne in navigating the complex biopharmaceutical market.

- Former CEO Background: Greene previously held the position of CEO at Sage Therapeutics from December 2020 to July 2025, and his expertise in drug development and commercialization will support Dyne's future growth initiatives.

- Positive Stock Performance: Dyne shares closed at $20.87 on Monday, reflecting a 5.40% increase, indicating a positive market reaction to the new appointment, which may enhance investor confidence and drive future growth.

Alnylam to Host 10th RNAi Roundtable Series

- RNAi Roundtable Series: Alnylam Pharmaceuticals announced its plan to host the 10th series of 'RNAi Roundtable' webinars in the coming months, featuring presentations from scientists and medical experts discussing recent advancements in the company's pipeline programs to address unmet clinical needs.

- Live Webcast Arrangement: Each event will be webcast live on the company's investor website, with replays available approximately three hours after each session, ensuring timely access to critical information for investors.

- 2030 Strategic Goals: Alnylam aims to increase its clinical programs from over 25 to more than 40 by 2030, demonstrating its commitment to sustainable innovation and market expansion in the RNAi therapeutics sector.

- Increased R&D Investment: The company is significantly ramping up its R&D investments to extend the application of RNAi technology, aiming to deliver multiple new transformative medicines for patients with serious diseases, thereby reinforcing its market leadership position.