Pop Mart's Global Expansion and Challenges

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 25 2026

0mins

Source: CNBC

- Revenue Growth and Stock Volatility: In 2025, Pop Mart's revenue and net income surged by 185% and 309%, respectively, yet the stock plummeted over 22% post-earnings release, indicating market concerns about sustaining growth momentum.

- Global Market Strategy: By 2025, international markets accounted for 44% of Pop Mart's revenue, with expectations for increased contributions from the U.S. and Europe, reflecting the company's proactive global expansion strategy.

- Diversified Product Strategy: Collaborations with Uniqlo and Parisian luxury brand Moynat have led Pop Mart into new sectors like jewelry, with some Labubu gold necklaces priced above $2,000, aiming to enhance brand influence and market competitiveness.

- Theme Park Ambitions: Pop Mart's Pop Land theme park in Beijing is undergoing reconstruction and expansion, aiming for a 360-degree immersive experience that combines live performances and storytelling to deepen consumer brand loyalty.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DIS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DIS

Wall Street analysts forecast DIS stock price to rise

19 Analyst Rating

16 Buy

3 Hold

0 Sell

Strong Buy

Current: 97.410

Low

123.00

Averages

137.29

High

152.00

Current: 97.410

Low

123.00

Averages

137.29

High

152.00

About DIS

The Walt Disney Company is a diversified worldwide entertainment company. The Company's segments include Entertainment, Sports and Experiences. The Entertainment segment generally encompasses its non-sports focused global film and episodic content production and distribution activities. The lines of business within the Entertainment segment along with their business activities include Linear Networks, Direct-to-Consumer, and Content Sales/Licensing. The Sports segment encompasses its sports-focused global television and direct-to-consumer (DTC) video streaming content production and distribution activities. The lines of business within the Sports segment include ESPN and Star. The Experiences segment includes Parks and Experiences and Consumer Products. Parks and Experiences consists of Walt Disney World Resort in Florida, Disneyland Resort in California, Disney Cruise Line, and others. Consumer Products includes licensing of its trade names, characters, visual, literary and other IP.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Escalating Middle East Tensions and World Cup Broadcast Rights Battle

- Middle East Escalation: On June 8, clashes between Israel and Iran severely tested a fragile truce, with attacks from Iran and its backed Houthi rebels further heightening tensions and threatening hopes for an end to the Middle East war.

- U.S. Retaliation: The U.S. revoked Iran's oil sales authorization in response to attacks in the Strait of Hormuz, stating that Iran's actions were unacceptable and would face consequences, demonstrating a firm U.S. military stance in the region.

- Ukrainian Offensive Intensifies: Ukrainian drones struck a major oil refinery in western Siberia, marking a significant escalation in attacks on Russian oil facilities, indicating Ukraine's strategic initiative in the ongoing conflict.

- World Cup Rights Competition: Companies like Netflix, Disney, and YouTube are vying for U.S. broadcast rights to the 2030 and 2034 World Cups, potentially igniting a bidding war with Fox, with discussions expected to commence in the next three months.

See More

Streaming Giants Compete for FIFA Broadcast Rights

- Bidding War Begins: Companies like Netflix, Disney, YouTube, Amazon, and Apple are actively vying for the U.S. broadcast rights to the 2030 and 2034 FIFA World Cups, with media executives budgeting between $1.5 billion and $2 billion per tournament, significantly exceeding current rights costs, indicating a highly competitive landscape.

- Language Bundling Strategy: FIFA plans to bundle English and Spanish broadcast rights into a single package, a strategy that could substantially increase bids and potentially squeeze out traditional broadcasters like NBCUniversal, which is currently reassessing its financial position.

- Involvement of Tech Giants: Tech giants such as Amazon and Apple may emerge as potential bidders, unencumbered by traditional television distribution models, highlighting the increasing reliance on live sports as a key subscriber acquisition tool for digital platforms.

- Market Sentiment Analysis: While retail sentiment on Stocktwits is bullish for both Netflix and Disney, with low message volume for Netflix and high for Disney, Netflix has seen a 14% decline year-to-date, while Disney has dropped 19%, reflecting cautious market sentiment regarding the upcoming bidding for broadcast rights.

See More

Media Companies Compete for World Cup Broadcast Rights

- Broadcast Rights Bidding: Companies like Netflix, Disney, and YouTube are vying for U.S. broadcast rights to the 2030 and 2034 World Cups, with budgets expected between $1.5 billion and $2 billion for each tournament, significantly enhancing their streaming service appeal.

- Language Rights Integration: FIFA plans to bundle English and Spanish broadcast rights, a strategy that could drive up bidding prices and attract more media partners, especially given that U.S. viewership has rivaled NFL playoff ratings.

- Viewership Potential: This year's World Cup has seen record viewership, with the U.S. match against Bosnia and Herzegovina attracting 26 million viewers, highlighting the immense advertising opportunities in the U.S. market and further boosting the value of broadcast rights.

- Time Zone Challenges: The 2030 and 2034 World Cups will be held in Morocco, Portugal, Spain, and Saudi Arabia, where time zone differences may affect U.S. viewership; however, the success of this year's tournament is likely to drive up broadcast rights prices.

See More

Media Giants Compete for World Cup Broadcast Rights

- Massive Budgets: Media companies like Netflix, Disney, and YouTube are budgeting between $1.5 billion and $2 billion for the U.S. broadcast rights to the 2030 and 2034 World Cups, indicating their recognition of the event's immense market potential and viewer engagement.

- Combined Rights Strategy: FIFA's plan to sell English and Spanish broadcast rights as a single package could drive up prices, attracting more media companies to bid, thereby enhancing the overall value of the tournaments and fostering competitive bidding.

- Viewership Surge: This year's World Cup has seen record viewership, with the U.S. match against Bosnia and Herzegovina drawing over 26 million viewers, highlighting significant advertising opportunities and a robust audience base that could lead to a substantial increase in broadcast rights prices.

- Time Zone Challenges: Although the 2030 and 2034 World Cups will be held in less favorable time zones for U.S. viewers, the success of this year's tournament is expected to drive up broadcast rights prices, as media companies remain optimistic about future viewership potential.

See More

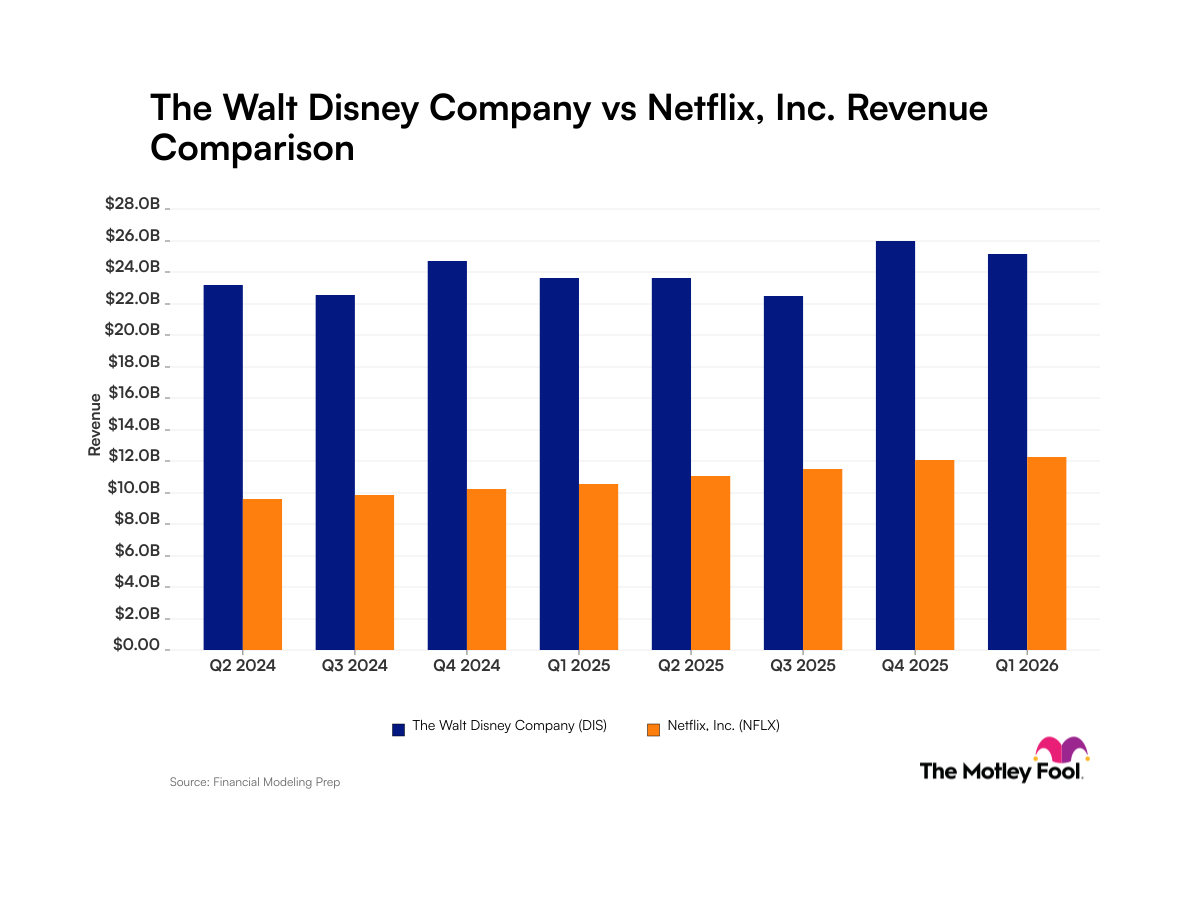

Comparison of Revenue Trends Between Disney and Netflix

- Disney's Revenue Performance: In Q1 2026, Disney reported revenue of $25.2 billion, reflecting a 7% year-over-year growth, and despite the leadership transition to new CEO Josh D'Amaro, its diversified business model in theme parks and entertainment content continues to support strong revenue growth.

- Netflix's Steady Revenue: Netflix achieved $12.2 billion in revenue for Q1 2026, marking a 16% year-over-year increase, and its 43% net income margin underscores its strong competitive position in the streaming market, despite navigating regulatory challenges and expanding its ad-supported subscription tier.

- Market Reaction Analysis: Despite Netflix's strong Q1 sales performance, its stock fell to a 52-week low of $70.86 on June 25, indicating investor concerns over potential growth slowdowns, particularly in light of the co-founder's retirement.

- Leadership Transition Impact: Disney's new CEO Josh D'Amaro took office on March 18, and while the company performed well under former CEO Bob Iger, the upcoming quarters will be critical to assess how the new leadership influences future performance.

See More

Financial Comparison Between Disney and Netflix

- Revenue Growth Trends: Netflix has shown steady quarter-over-quarter growth over the past eight quarters, with first-quarter sales of $12.2 billion reflecting a 16% year-over-year increase, yet management forecasts a slowdown to 13.5% growth for Q2, raising concerns about growth deceleration.

- Net Income Margin Comparison: Netflix boasts a net income margin of 43%, significantly higher than Disney's 9%, highlighting the advantages of Netflix's focused streaming service model, while Disney's revenue streams are more diversified, including theme parks and merchandise sales.

- Leadership Change Impact: Disney's new CEO, Josh D'Amaro, took over on March 18, and while the company reported second-quarter sales of $25.2 billion, a 7% year-over-year increase under former CEO Bob Iger, the performance under new leadership remains to be seen.

- Investor Focus: As the revenue gap between Disney and Netflix narrows, investors should monitor upcoming quarters closely, particularly as Netflix navigates regulatory challenges in Europe and expands its advertising-supported subscription tier.

See More

Escalating Middle East Tensions and World Cup Broadcast Rights Battle

- Middle East Escalation: On June 8, clashes between Israel and Iran severely tested a fragile truce, with attacks from Iran and its backed Houthi rebels further heightening tensions and threatening hopes for an end to the Middle East war.

- U.S. Retaliation: The U.S. revoked Iran's oil sales authorization in response to attacks in the Strait of Hormuz, stating that Iran's actions were unacceptable and would face consequences, demonstrating a firm U.S. military stance in the region.

- Ukrainian Offensive Intensifies: Ukrainian drones struck a major oil refinery in western Siberia, marking a significant escalation in attacks on Russian oil facilities, indicating Ukraine's strategic initiative in the ongoing conflict.

- World Cup Rights Competition: Companies like Netflix, Disney, and YouTube are vying for U.S. broadcast rights to the 2030 and 2034 World Cups, potentially igniting a bidding war with Fox, with discussions expected to commence in the next three months.

See More

Streaming Giants Compete for FIFA Broadcast Rights

- Bidding War Begins: Companies like Netflix, Disney, YouTube, Amazon, and Apple are actively vying for the U.S. broadcast rights to the 2030 and 2034 FIFA World Cups, with media executives budgeting between $1.5 billion and $2 billion per tournament, significantly exceeding current rights costs, indicating a highly competitive landscape.

- Language Bundling Strategy: FIFA plans to bundle English and Spanish broadcast rights into a single package, a strategy that could substantially increase bids and potentially squeeze out traditional broadcasters like NBCUniversal, which is currently reassessing its financial position.

- Involvement of Tech Giants: Tech giants such as Amazon and Apple may emerge as potential bidders, unencumbered by traditional television distribution models, highlighting the increasing reliance on live sports as a key subscriber acquisition tool for digital platforms.

- Market Sentiment Analysis: While retail sentiment on Stocktwits is bullish for both Netflix and Disney, with low message volume for Netflix and high for Disney, Netflix has seen a 14% decline year-to-date, while Disney has dropped 19%, reflecting cautious market sentiment regarding the upcoming bidding for broadcast rights.

See More

Media Companies Compete for World Cup Broadcast Rights

- Broadcast Rights Bidding: Companies like Netflix, Disney, and YouTube are vying for U.S. broadcast rights to the 2030 and 2034 World Cups, with budgets expected between $1.5 billion and $2 billion for each tournament, significantly enhancing their streaming service appeal.

- Language Rights Integration: FIFA plans to bundle English and Spanish broadcast rights, a strategy that could drive up bidding prices and attract more media partners, especially given that U.S. viewership has rivaled NFL playoff ratings.

- Viewership Potential: This year's World Cup has seen record viewership, with the U.S. match against Bosnia and Herzegovina attracting 26 million viewers, highlighting the immense advertising opportunities in the U.S. market and further boosting the value of broadcast rights.

- Time Zone Challenges: The 2030 and 2034 World Cups will be held in Morocco, Portugal, Spain, and Saudi Arabia, where time zone differences may affect U.S. viewership; however, the success of this year's tournament is likely to drive up broadcast rights prices.

See More

Media Giants Compete for World Cup Broadcast Rights

- Massive Budgets: Media companies like Netflix, Disney, and YouTube are budgeting between $1.5 billion and $2 billion for the U.S. broadcast rights to the 2030 and 2034 World Cups, indicating their recognition of the event's immense market potential and viewer engagement.

- Combined Rights Strategy: FIFA's plan to sell English and Spanish broadcast rights as a single package could drive up prices, attracting more media companies to bid, thereby enhancing the overall value of the tournaments and fostering competitive bidding.

- Viewership Surge: This year's World Cup has seen record viewership, with the U.S. match against Bosnia and Herzegovina drawing over 26 million viewers, highlighting significant advertising opportunities and a robust audience base that could lead to a substantial increase in broadcast rights prices.

- Time Zone Challenges: Although the 2030 and 2034 World Cups will be held in less favorable time zones for U.S. viewers, the success of this year's tournament is expected to drive up broadcast rights prices, as media companies remain optimistic about future viewership potential.

See More

Comparison of Revenue Trends Between Disney and Netflix

- Disney's Revenue Performance: In Q1 2026, Disney reported revenue of $25.2 billion, reflecting a 7% year-over-year growth, and despite the leadership transition to new CEO Josh D'Amaro, its diversified business model in theme parks and entertainment content continues to support strong revenue growth.

- Netflix's Steady Revenue: Netflix achieved $12.2 billion in revenue for Q1 2026, marking a 16% year-over-year increase, and its 43% net income margin underscores its strong competitive position in the streaming market, despite navigating regulatory challenges and expanding its ad-supported subscription tier.

- Market Reaction Analysis: Despite Netflix's strong Q1 sales performance, its stock fell to a 52-week low of $70.86 on June 25, indicating investor concerns over potential growth slowdowns, particularly in light of the co-founder's retirement.

- Leadership Transition Impact: Disney's new CEO Josh D'Amaro took office on March 18, and while the company performed well under former CEO Bob Iger, the upcoming quarters will be critical to assess how the new leadership influences future performance.

See More

Financial Comparison Between Disney and Netflix

- Revenue Growth Trends: Netflix has shown steady quarter-over-quarter growth over the past eight quarters, with first-quarter sales of $12.2 billion reflecting a 16% year-over-year increase, yet management forecasts a slowdown to 13.5% growth for Q2, raising concerns about growth deceleration.

- Net Income Margin Comparison: Netflix boasts a net income margin of 43%, significantly higher than Disney's 9%, highlighting the advantages of Netflix's focused streaming service model, while Disney's revenue streams are more diversified, including theme parks and merchandise sales.

- Leadership Change Impact: Disney's new CEO, Josh D'Amaro, took over on March 18, and while the company reported second-quarter sales of $25.2 billion, a 7% year-over-year increase under former CEO Bob Iger, the performance under new leadership remains to be seen.

- Investor Focus: As the revenue gap between Disney and Netflix narrows, investors should monitor upcoming quarters closely, particularly as Netflix navigates regulatory challenges in Europe and expands its advertising-supported subscription tier.

See More