Nvidia's AI Infrastructure Market Outlook is Expanding

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy NVDA?

Source: Fool

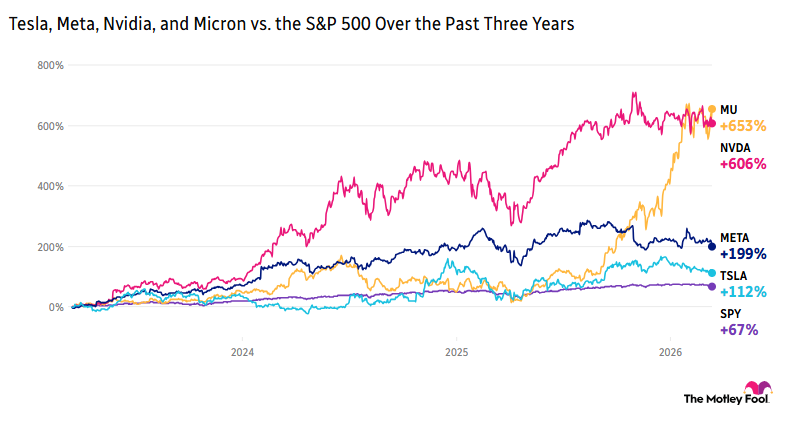

- Data Center Spending Forecast: Nvidia CEO Jensen Huang anticipates that data center spending will reach $3 trillion to $4 trillion annually by 2030, indicating sustained growth in AI spending that further solidifies Nvidia's leadership position in the AI infrastructure market.

- Surge in Demand for Reasoning Models: As the complexity of reasoning models increases, the demand for Nvidia GPUs is expected to rise, driving revenue growth in the data center segment, particularly as AI applications continue to expand.

- Cost Efficiency Advantage: Huang emphasized that Nvidia systems generate the lowest cost per token processed, and data centers running on Nvidia achieve the highest revenues, providing the company with a significant competitive edge in the cloud services market.

- Attractive Market Valuation: Wall Street estimates that Nvidia's earnings will grow at a rate of 38% annually over the next three years, making the current valuation of 37 times earnings appear very attractive, encouraging investors to consider increasing their positions in the stock.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 183.140

Low

200.00

Averages

264.97

High

352.00

Current: 183.140

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is a full-stack computing infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. The Company’s segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing platforms and artificial intelligence (AI) solutions and software; networking; automotive platforms and autonomous and electric vehicle solutions; Jetson for robotics and other embedded platforms, and DGX Cloud computing services. The Graphics segment includes GeForce GPUs for gaming and PCs, the GeForce NOW game streaming service and related infrastructure, and solutions for gaming platforms; Quadro/NVIDIA RTX GPUs for enterprise workstation graphics; virtual GPU software for cloud-based visual and virtual computing; automotive platforms for infotainment systems, and Omniverse Enterprise software for building and operating industrial AI and digital twin applications.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia GTC Conference Preview: Strong AI Demand Ahead

- Strong AI Demand: Gene Munster from Deepwater indicates that Nvidia will emphasize at the GTC conference that demand for AI infrastructure exceeds investor expectations, even as concerns about growth slowing in 2027 intensify, with Huang likely reiterating that AI's utility has reached an 'inflection point.'

- Economic Benefits of Rubin Architecture: Munster expects Nvidia to elaborate on how the Rubin architecture will enhance inference economics, with investors focusing on key metrics such as cost per token, throughput, and performance per watt, which could shape industry perceptions of inference infrastructure.

- Full-Stack AI Infrastructure Strategy: Analyst Patrick Moorhead notes that Nvidia is transitioning from a semiconductor company to a comprehensive AI infrastructure platform, with hyperscaler AI spending expected to exceed $600 billion this year, providing Nvidia with unusually strong demand visibility and enhancing its market position.

- Market Sentiment Shift: Despite NVDA stock rising 56% over the past year, sentiment among Stocktwits users has shifted from 'neutral' to 'bearish,' reflecting investor unease about future growth, particularly ahead of the GTC conference where signals on AI demand are closely watched.

See More

Nvidia Unveils 2026 AI Plans at GTC

- AI Infrastructure Investment: At the GTC conference in San Jose, Nvidia anticipates over $600 billion in AI infrastructure spending by 2026, which is expected to drive vertical integration from chips to full AI systems, further solidifying its leadership in the AI market.

- Meta Layoff Plans: Meta is planning to cut 20% of its workforce to offset substantial AI infrastructure costs, aiming to achieve savings through increased use of AI agents and assistance for human workers, thereby enhancing operational efficiency and profitability.

- Tesla Semiconductor Manufacturing: CEO Elon Musk announced the imminent launch of Tesla's in-house semiconductor manufacturing, which is expected to boost production capacity and reduce reliance on external suppliers, enhancing the company's technological autonomy.

- Market Volatility Impact: The S&P 500 fell 1.6% last week due to turmoil from the Middle East conflict, but Goldman Sachs predicts a potential rebound to 7,600 points by the end of 2026 driven by rising corporate earnings, indicating the market's underlying recovery potential.

See More

Broadcom's AI Revenue Soars, Bright Future Ahead

- AI Revenue Surge: Broadcom's AI revenue soared to $8.4 billion in the recent quarter, marking over 100% growth year-over-year, with expectations to exceed $10 billion in the next reporting period, indicating robust market demand and growth potential.

- Strategic Customer Orders: The company has established deep strategic partnerships with six major clients, including Anthropic and OpenAI, which placed orders of $10 billion and $11 billion respectively, showcasing Broadcom's strong market position in the AI sector.

- Market Share Growth: Networking revenue accounted for about one-third of total AI revenue, with projections to rise to 40% in the current quarter, reflecting strong demand for AI accelerators and networking equipment.

- Attractive Valuation: Broadcom's stock trades at 29 times forward earnings, down from over 50 times a few months ago, with a market value of approximately $1.5 trillion, providing room for future growth and potentially attracting more investors to this promising stock.

See More

Broadcom's AI Revenue Expected to Reach $100 Billion

- Surging AI Revenue: Broadcom's AI revenue skyrocketed over 100% in the recent quarter to $8.4 billion, with expectations to exceed $10 billion in the next reporting period, driven by robust demand for AI accelerators and networking equipment, highlighting the company's strong potential in the AI market.

- Strategic Customer Orders: Broadcom has established deep strategic partnerships with six major customers, including Anthropic and OpenAI, which placed orders of $10 billion and $11 billion respectively, providing substantial support for the company's future growth through these long-term collaborations.

- Market Share Growth: Networking revenue accounted for one-third of total AI revenue and is expected to rise to 40% in the current quarter, indicating sustained demand in the networking equipment sector, particularly for the Tomahawk 6 switch, which is seeing high demand.

- Attractive Valuation: Broadcom's stock is currently trading at 29 times forward earnings estimates, significantly lower than over 50 times a few months ago, offering investors a compelling entry point, especially with the company's market value around $1.5 trillion, indicating substantial room for future growth.

See More

Nvidia's Optimistic Outlook on AI Spending

- Data Center Spending Outlook: CEO Jensen Huang anticipates that data center spending could reach $3 trillion to $4 trillion by 2030, indicating that rapid AI demand will drive market expansion, potentially achieving annual growth rates between 32% and 41%.

- Evolution of Reasoning Models: As the complexity of reasoning models increases, demand for Nvidia's GPUs is expected to rise significantly; Huang noted that these models not only solve multistep problems but also broaden AI use cases, further solidifying Nvidia's leadership in AI infrastructure.

- Strengthened Competitive Advantage: By providing comprehensive data center solutions, Nvidia optimizes performance and energy efficiency, ensuring the lowest cost per processing unit, which enhances cloud service providers' profitability and creates a strong competitive moat.

- Broad Market Prospects: Wall Street estimates Nvidia's earnings will grow at 38% annually over the next three years, making the current valuation of 37 times earnings very attractive, suggesting that long-term investors should consider increasing their positions in the stock to capitalize on future growth opportunities.

See More

Nebius Partners with Meta for $12 Billion AI Infrastructure Deal

- Nebius Partnership: Nebius Group's stock surged 14% following its announcement of a $12 billion AI infrastructure deal with Meta, which is expected to significantly enhance its market position and strengthen ties with tech giants.

- Micron Expansion: Micron Technology's shares rose 4% as the company revealed plans to build a second manufacturing site in Taiwan, aimed at expanding supply of leading-edge DRAM products to meet increasing market demand.

- Crypto Stocks Rally: Stocks of Mara Holdings and Strategy increased by 4% each, while Circle rose 5.4%, driven by a rebound in Bitcoin prices, indicating a potential resurgence in the crypto market that may attract more investor interest.

- Dollar Tree Earnings Reaction: Dollar Tree's stock fell 6% after reporting mixed fourth-quarter results, with earnings per share of $2.56 beating expectations but revenue of $5.45 billion falling short of forecasts, reflecting market concerns about future growth prospects.

See More

Nvidia GTC Conference Preview: Strong AI Demand Ahead

- Strong AI Demand: Gene Munster from Deepwater indicates that Nvidia will emphasize at the GTC conference that demand for AI infrastructure exceeds investor expectations, even as concerns about growth slowing in 2027 intensify, with Huang likely reiterating that AI's utility has reached an 'inflection point.'

- Economic Benefits of Rubin Architecture: Munster expects Nvidia to elaborate on how the Rubin architecture will enhance inference economics, with investors focusing on key metrics such as cost per token, throughput, and performance per watt, which could shape industry perceptions of inference infrastructure.

- Full-Stack AI Infrastructure Strategy: Analyst Patrick Moorhead notes that Nvidia is transitioning from a semiconductor company to a comprehensive AI infrastructure platform, with hyperscaler AI spending expected to exceed $600 billion this year, providing Nvidia with unusually strong demand visibility and enhancing its market position.

- Market Sentiment Shift: Despite NVDA stock rising 56% over the past year, sentiment among Stocktwits users has shifted from 'neutral' to 'bearish,' reflecting investor unease about future growth, particularly ahead of the GTC conference where signals on AI demand are closely watched.

See More

Nvidia Unveils 2026 AI Plans at GTC

- AI Infrastructure Investment: At the GTC conference in San Jose, Nvidia anticipates over $600 billion in AI infrastructure spending by 2026, which is expected to drive vertical integration from chips to full AI systems, further solidifying its leadership in the AI market.

- Meta Layoff Plans: Meta is planning to cut 20% of its workforce to offset substantial AI infrastructure costs, aiming to achieve savings through increased use of AI agents and assistance for human workers, thereby enhancing operational efficiency and profitability.

- Tesla Semiconductor Manufacturing: CEO Elon Musk announced the imminent launch of Tesla's in-house semiconductor manufacturing, which is expected to boost production capacity and reduce reliance on external suppliers, enhancing the company's technological autonomy.

- Market Volatility Impact: The S&P 500 fell 1.6% last week due to turmoil from the Middle East conflict, but Goldman Sachs predicts a potential rebound to 7,600 points by the end of 2026 driven by rising corporate earnings, indicating the market's underlying recovery potential.

See More

Broadcom's AI Revenue Soars, Bright Future Ahead

- AI Revenue Surge: Broadcom's AI revenue soared to $8.4 billion in the recent quarter, marking over 100% growth year-over-year, with expectations to exceed $10 billion in the next reporting period, indicating robust market demand and growth potential.

- Strategic Customer Orders: The company has established deep strategic partnerships with six major clients, including Anthropic and OpenAI, which placed orders of $10 billion and $11 billion respectively, showcasing Broadcom's strong market position in the AI sector.

- Market Share Growth: Networking revenue accounted for about one-third of total AI revenue, with projections to rise to 40% in the current quarter, reflecting strong demand for AI accelerators and networking equipment.

- Attractive Valuation: Broadcom's stock trades at 29 times forward earnings, down from over 50 times a few months ago, with a market value of approximately $1.5 trillion, providing room for future growth and potentially attracting more investors to this promising stock.

See More

Broadcom's AI Revenue Expected to Reach $100 Billion

- Surging AI Revenue: Broadcom's AI revenue skyrocketed over 100% in the recent quarter to $8.4 billion, with expectations to exceed $10 billion in the next reporting period, driven by robust demand for AI accelerators and networking equipment, highlighting the company's strong potential in the AI market.

- Strategic Customer Orders: Broadcom has established deep strategic partnerships with six major customers, including Anthropic and OpenAI, which placed orders of $10 billion and $11 billion respectively, providing substantial support for the company's future growth through these long-term collaborations.

- Market Share Growth: Networking revenue accounted for one-third of total AI revenue and is expected to rise to 40% in the current quarter, indicating sustained demand in the networking equipment sector, particularly for the Tomahawk 6 switch, which is seeing high demand.

- Attractive Valuation: Broadcom's stock is currently trading at 29 times forward earnings estimates, significantly lower than over 50 times a few months ago, offering investors a compelling entry point, especially with the company's market value around $1.5 trillion, indicating substantial room for future growth.

See More

Nvidia's Optimistic Outlook on AI Spending

- Data Center Spending Outlook: CEO Jensen Huang anticipates that data center spending could reach $3 trillion to $4 trillion by 2030, indicating that rapid AI demand will drive market expansion, potentially achieving annual growth rates between 32% and 41%.

- Evolution of Reasoning Models: As the complexity of reasoning models increases, demand for Nvidia's GPUs is expected to rise significantly; Huang noted that these models not only solve multistep problems but also broaden AI use cases, further solidifying Nvidia's leadership in AI infrastructure.

- Strengthened Competitive Advantage: By providing comprehensive data center solutions, Nvidia optimizes performance and energy efficiency, ensuring the lowest cost per processing unit, which enhances cloud service providers' profitability and creates a strong competitive moat.

- Broad Market Prospects: Wall Street estimates Nvidia's earnings will grow at 38% annually over the next three years, making the current valuation of 37 times earnings very attractive, suggesting that long-term investors should consider increasing their positions in the stock to capitalize on future growth opportunities.

See More

Nebius Partners with Meta for $12 Billion AI Infrastructure Deal

- Nebius Partnership: Nebius Group's stock surged 14% following its announcement of a $12 billion AI infrastructure deal with Meta, which is expected to significantly enhance its market position and strengthen ties with tech giants.

- Micron Expansion: Micron Technology's shares rose 4% as the company revealed plans to build a second manufacturing site in Taiwan, aimed at expanding supply of leading-edge DRAM products to meet increasing market demand.

- Crypto Stocks Rally: Stocks of Mara Holdings and Strategy increased by 4% each, while Circle rose 5.4%, driven by a rebound in Bitcoin prices, indicating a potential resurgence in the crypto market that may attract more investor interest.

- Dollar Tree Earnings Reaction: Dollar Tree's stock fell 6% after reporting mixed fourth-quarter results, with earnings per share of $2.56 beating expectations but revenue of $5.45 billion falling short of forecasts, reflecting market concerns about future growth prospects.

See More