Nvidia Stock Hits Historic Highs Amid AI Boom

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Should l Buy NVDA?

Source: Fool

- Stock Volatility Analysis: Nvidia's stock soared 1,320% since early 2023 but faced a 20% decline by late October due to uncertainties surrounding AI adoption and rising competition, highlighting significant market sentiment fluctuations.

- Historic Surge: On Wednesday, Nvidia achieved its longest streak of 11 consecutive trading days of gains since its IPO in 1999, reflecting strong investor confidence in its future growth potential amid a booming AI market.

- Impressive Financial Performance: In Q4 of fiscal 2026, Nvidia reported record revenue of $68 billion, a 73% year-over-year increase, with adjusted EPS of $1.62, up 82%, and management forecasts Q1 revenue of $78 billion, accelerating year-over-year growth to 77%.

- Future Sales Expectations: Nvidia anticipates selling at least $1 trillion worth of AI chips by 2027, which would significantly boost sales over the next two years, further solidifying its market leadership position.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 198.350

Low

200.00

Averages

264.97

High

352.00

Current: 198.350

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia Set to Release Q1 2027 Fiscal Results Amid AI Dominance

- Earnings Forecast: Nvidia anticipates Q1 2027 sales of $78 billion, representing a 77% increase year-over-year, with a projected gross margin of 74.9%, indicating robust market demand and profitability.

- Competitive Advantage: Despite increasing external competition, Nvidia's GPUs maintain clear advantages in computational power, and persistent GPU scarcity allows the company to sell hardware at premium prices, solidifying its market position in enterprise data centers.

- Stock Volatility: Historical data shows that Nvidia's stock typically declines after earnings releases, with five out of the last seven quarters experiencing a drop, averaging a 3% loss, reflecting overly optimistic market expectations.

- Investor Caution: While Nvidia's results often exceed analyst forecasts, the optimistic sentiment surrounding AI technology may pose bubble risks, prompting investors to carefully consider their investment decisions following the earnings report.

See More

AI Startup Cursor in Talks for $2B Fundraising at $50B Valuation

- Fundraising Plans: AI startup Cursor is in discussions to raise a $2 billion funding round, with an expected valuation exceeding $50 billion, which will further propel its market expansion and technological innovation.

- Investor Lineup: Andreessen Horowitz is set to co-lead this funding round, with Nvidia and Thrive Capital also expected to participate, reflecting strong confidence in Cursor's future growth from these previously involved investors.

- Historical Funding Review: Last November, Cursor raised approximately $2.3 billion in a Series D funding round, achieving a post-money valuation of $29.3 billion, attracting existing investors like Accel, Thrive, and Andreessen Horowitz, along with new partners such as Coatue, Nvidia, and Alphabet.

- Technology Updates: In February, Cursor released various updates aimed at assisting software developers, including enabling AI agents to test coding changes and record their actions through videos, logs, and screenshots, thereby enhancing development efficiency.

See More

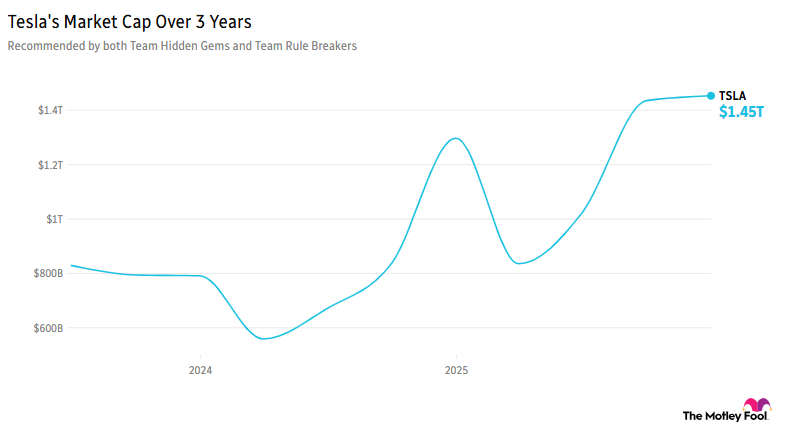

Tesla Set to Report Q1 Earnings Amid Market Surge

- Tesla Earnings Outlook: Tesla is set to report its Q1 fiscal 2026 earnings on Wednesday, with the stock down 11% year-to-date; however, it has shown recovery in April as CEO Elon Musk garners attention for the upcoming SpaceX IPO, and analysts predict profit growth despite vehicle deliveries of 358,000 falling short of the 370,000 expected.

- Terafab Project Acceleration: Musk is urging potential suppliers to expedite the Terafab AI chip-making project, which is estimated to cost over $25 billion and aims to achieve an annual computing capacity of one terawatt, highlighting Tesla's ambitions in the AI sector.

- Market Performance Surge: Despite uncertainties surrounding dealings with Iran, both the S&P 500 and Nasdaq reached new all-time highs, rising 4.5% and 6.8% respectively, while the Dow Jones increased by 3.2%, indicating a robust market recovery.

- Oil Price Impact: Following the U.S. Navy's seizure of an Iranian-flagged ship, benchmark crude prices surged over 6%, with West Texas Intermediate surpassing $88 and Brent crude exceeding $95, which could influence market sentiment.

See More

Cursor's Funding Round Could Reach $2 Billion, Valuation Exceeds $50 Billion

- Funding Scale Expansion: Cursor's new funding round is expected to reach $2 billion at a pre-money valuation exceeding $50 billion, a figure that excludes the new capital, indicating strong investor confidence in its future growth.

- Returning Investors: Andreessen Horowitz, Nvidia, and Thrive Capital are set to continue their involvement in this funding round, with Andreessen Horowitz expected to co-lead, demonstrating ongoing support and trust in Cursor's potential.

- Revenue Growth Expectations: Cursor projects that by year-end, its annualized revenue will surpass $6 billion, which represents a tripling of the $2 billion annualized run rate achieved in February, reflecting rapid market expansion and successful business model transformation.

- Intensifying Market Competition: As competitors like Anthropic, OpenAI, and Google offer similar AI coding tools, Cursor faces increasing competition; however, its enterprise customers are now generating positive gross margins, showcasing the potential of its business model.

See More

Nvidia Faces Stock Price Pressure Ahead of Earnings

- Strong Earnings Forecast: Nvidia anticipates $78 billion in sales for Q1 2027, reflecting a 77% year-over-year growth, with a projected gross margin of 74.9%, indicating robust market demand and profitability.

- Clear Competitive Advantages: Despite increasing external competition, Nvidia's GPUs maintain significant advantages in computing power, and ongoing GPU scarcity allows the company to sell hardware at a premium, solidifying its dominance in enterprise data centers.

- Stock Price Volatility Trends: Although Nvidia often exceeds Wall Street analysts' expectations, its stock has averaged a 3% decline following earnings releases over the past seven quarters, suggesting that investor expectations may be overly optimistic.

- Historical Lessons as Warning: Since the rise of the internet, all disruptive technologies have faced bubble bursts; while Nvidia's results indicate no adoption issues for AI infrastructure, businesses still struggle to optimize AI solutions and achieve positive returns on their investments.

See More

Google Partners with Marvell to Develop AI Chips

- AI Chip Development Partnership: Google is reportedly in discussions with Marvell to develop two chips aimed at enhancing AI model operational efficiency, including a memory-focused processor and a next-generation TPU specifically designed for AI inference workloads, indicating a growing demand for customized semiconductors from Google.

- Positive Market Reaction: Marvell's shares rose 5.8% in early premarket trading on Monday despite a broader market decline, reflecting investor optimism regarding its collaboration with Google, particularly against the backdrop of a rebound in chip stocks, suggesting potential value in this partnership.

- Retail Investor Sentiment: On Stocktwits, retail sentiment for Marvell remains ‘bullish,’ although some investors express skepticism about the stock's continued rise, suggesting it may be overvalued and at risk of a pullback, highlighting the complexity of market sentiment surrounding the stock.

- Geopolitical Impact: Escalating tensions between the U.S. and Iran have led to declines in U.S. futures early Monday, yet Marvell's stock continues to perform strongly, demonstrating resilience in an uncertain market environment and potentially attracting more investor interest in its future performance.

See More

Nvidia Set to Release Q1 2027 Fiscal Results Amid AI Dominance

- Earnings Forecast: Nvidia anticipates Q1 2027 sales of $78 billion, representing a 77% increase year-over-year, with a projected gross margin of 74.9%, indicating robust market demand and profitability.

- Competitive Advantage: Despite increasing external competition, Nvidia's GPUs maintain clear advantages in computational power, and persistent GPU scarcity allows the company to sell hardware at premium prices, solidifying its market position in enterprise data centers.

- Stock Volatility: Historical data shows that Nvidia's stock typically declines after earnings releases, with five out of the last seven quarters experiencing a drop, averaging a 3% loss, reflecting overly optimistic market expectations.

- Investor Caution: While Nvidia's results often exceed analyst forecasts, the optimistic sentiment surrounding AI technology may pose bubble risks, prompting investors to carefully consider their investment decisions following the earnings report.

See More

AI Startup Cursor in Talks for $2B Fundraising at $50B Valuation

- Fundraising Plans: AI startup Cursor is in discussions to raise a $2 billion funding round, with an expected valuation exceeding $50 billion, which will further propel its market expansion and technological innovation.

- Investor Lineup: Andreessen Horowitz is set to co-lead this funding round, with Nvidia and Thrive Capital also expected to participate, reflecting strong confidence in Cursor's future growth from these previously involved investors.

- Historical Funding Review: Last November, Cursor raised approximately $2.3 billion in a Series D funding round, achieving a post-money valuation of $29.3 billion, attracting existing investors like Accel, Thrive, and Andreessen Horowitz, along with new partners such as Coatue, Nvidia, and Alphabet.

- Technology Updates: In February, Cursor released various updates aimed at assisting software developers, including enabling AI agents to test coding changes and record their actions through videos, logs, and screenshots, thereby enhancing development efficiency.

See More

Tesla Set to Report Q1 Earnings Amid Market Surge

- Tesla Earnings Outlook: Tesla is set to report its Q1 fiscal 2026 earnings on Wednesday, with the stock down 11% year-to-date; however, it has shown recovery in April as CEO Elon Musk garners attention for the upcoming SpaceX IPO, and analysts predict profit growth despite vehicle deliveries of 358,000 falling short of the 370,000 expected.

- Terafab Project Acceleration: Musk is urging potential suppliers to expedite the Terafab AI chip-making project, which is estimated to cost over $25 billion and aims to achieve an annual computing capacity of one terawatt, highlighting Tesla's ambitions in the AI sector.

- Market Performance Surge: Despite uncertainties surrounding dealings with Iran, both the S&P 500 and Nasdaq reached new all-time highs, rising 4.5% and 6.8% respectively, while the Dow Jones increased by 3.2%, indicating a robust market recovery.

- Oil Price Impact: Following the U.S. Navy's seizure of an Iranian-flagged ship, benchmark crude prices surged over 6%, with West Texas Intermediate surpassing $88 and Brent crude exceeding $95, which could influence market sentiment.

See More

Cursor's Funding Round Could Reach $2 Billion, Valuation Exceeds $50 Billion

- Funding Scale Expansion: Cursor's new funding round is expected to reach $2 billion at a pre-money valuation exceeding $50 billion, a figure that excludes the new capital, indicating strong investor confidence in its future growth.

- Returning Investors: Andreessen Horowitz, Nvidia, and Thrive Capital are set to continue their involvement in this funding round, with Andreessen Horowitz expected to co-lead, demonstrating ongoing support and trust in Cursor's potential.

- Revenue Growth Expectations: Cursor projects that by year-end, its annualized revenue will surpass $6 billion, which represents a tripling of the $2 billion annualized run rate achieved in February, reflecting rapid market expansion and successful business model transformation.

- Intensifying Market Competition: As competitors like Anthropic, OpenAI, and Google offer similar AI coding tools, Cursor faces increasing competition; however, its enterprise customers are now generating positive gross margins, showcasing the potential of its business model.

See More

Nvidia Faces Stock Price Pressure Ahead of Earnings

- Strong Earnings Forecast: Nvidia anticipates $78 billion in sales for Q1 2027, reflecting a 77% year-over-year growth, with a projected gross margin of 74.9%, indicating robust market demand and profitability.

- Clear Competitive Advantages: Despite increasing external competition, Nvidia's GPUs maintain significant advantages in computing power, and ongoing GPU scarcity allows the company to sell hardware at a premium, solidifying its dominance in enterprise data centers.

- Stock Price Volatility Trends: Although Nvidia often exceeds Wall Street analysts' expectations, its stock has averaged a 3% decline following earnings releases over the past seven quarters, suggesting that investor expectations may be overly optimistic.

- Historical Lessons as Warning: Since the rise of the internet, all disruptive technologies have faced bubble bursts; while Nvidia's results indicate no adoption issues for AI infrastructure, businesses still struggle to optimize AI solutions and achieve positive returns on their investments.

See More

Google Partners with Marvell to Develop AI Chips

- AI Chip Development Partnership: Google is reportedly in discussions with Marvell to develop two chips aimed at enhancing AI model operational efficiency, including a memory-focused processor and a next-generation TPU specifically designed for AI inference workloads, indicating a growing demand for customized semiconductors from Google.

- Positive Market Reaction: Marvell's shares rose 5.8% in early premarket trading on Monday despite a broader market decline, reflecting investor optimism regarding its collaboration with Google, particularly against the backdrop of a rebound in chip stocks, suggesting potential value in this partnership.

- Retail Investor Sentiment: On Stocktwits, retail sentiment for Marvell remains ‘bullish,’ although some investors express skepticism about the stock's continued rise, suggesting it may be overvalued and at risk of a pullback, highlighting the complexity of market sentiment surrounding the stock.

- Geopolitical Impact: Escalating tensions between the U.S. and Iran have led to declines in U.S. futures early Monday, yet Marvell's stock continues to perform strongly, demonstrating resilience in an uncertain market environment and potentially attracting more investor interest in its future performance.

See More