Nvidia Reaches $5 Trillion Valuation Again; When Will It Hit $6 Trillion?

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy NVDA?

Source: Yahoo Finance

- Valuation Recovery: Nvidia first crossed the $5 trillion valuation threshold in October 2025 and then retreated, but it rebounded to this level again in April 2026, demonstrating strong market recovery capabilities and indicating ongoing growth potential in the AI sector.

- Growth Target: To achieve a $6 trillion valuation, Nvidia's stock must rise by 20%, necessitating $200 billion in net income; with a projected revenue of $371 billion by the end of fiscal year 2027 and a 56% net income margin, Nvidia is expected to easily surpass this target.

- Valuation Analysis: Analysts suggest a fair valuation of 30 times earnings for Nvidia, while it currently trades at 43.5 times earnings, reflecting high market expectations for its future growth and solidifying the possibility of it becoming a $6 trillion company.

- Investment Advice: While Nvidia is considered a strong investment choice, the Motley Fool analyst team did not include it in their current list of top investment stocks, advising investors to carefully consider market dynamics before making investment decisions.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 199.570

Low

200.00

Averages

264.97

High

352.00

Current: 199.570

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia's Earnings Growth Expected to Accelerate Over Next Three Years

- Market Share Expansion: Nvidia's upcoming Vera Rubin processors are expected to reduce inference costs by 90%, significantly enhancing its competitiveness in the AI inference market, with projected data center sales reaching $1 trillion in 2026 and 2027, a substantial increase from the previous $500 billion forecast.

- Strong Profitability: Nvidia anticipates a 75% increase in earnings per share for the current fiscal year, reaching $8.34, far exceeding the tech sector's estimated 44% year-over-year growth, showcasing its robust profitability and market leadership in the AI sector.

- Partnership Growth: Nvidia has established partnerships with leading AI companies such as Anthropic, Meta, xAI, and OpenAI, providing a stable demand source as these companies see strong adoption of their AI inference applications, further solidifying Nvidia's market position.

- Long-Term Growth Potential: Despite Nvidia's current P/E ratio of 42.5, significantly higher than the Nasdaq-100's 33.4, its strong earnings growth potential justifies this valuation, with expectations of surpassing a $10 trillion market cap within the next three years, attracting more investor interest.

See More

NVIDIA Has Not Sold H200 Chips to Chinese Firms Amid Trade Concerns

- Sales Delay: NVIDIA has not sold its H200 AI chips to Chinese enterprises, as reported by Secretary Howard Lutnick, who attributed the delay to China's government banning acquisitions to favor domestic market investment, highlighting the tension in US-China trade relations.

- Policy Impact: The Trump administration approved shipments of H200 chips to China in January with conditions, raising concerns among US lawmakers about potential military applications, which has further complicated sales terms and slowed supply chains.

- Export Restrictions: Lutnick mentioned that the affiliates rule blocking exports to thousands of Chinese businesses is still under consideration, linked to broader trade negotiations, indicating that policy uncertainty may affect NVIDIA's market strategy.

- Investment Potential: While NVIDIA is recognized as one of the best data center hardware stocks, analysts suggest that certain AI stocks may offer greater upside potential and lower downside risk, reflecting a diverse outlook on the AI sector.

See More

Investment Recommendations for High-Yield Energy Stocks

- Strong Energy Stock Performance: High energy prices have led Wall Street to push energy stock prices up, with expectations of strong financial performance for these companies, although history suggests oil prices will eventually fall, necessitating caution among investors.

- Chevron vs. Exxon: Chevron offers a dividend yield of 3.6%, notably higher than Exxon's 2.6%, with both companies demonstrating reliability across the energy cycle and possessing strong balance sheets, making Chevron more attractive for income-focused investors.

- Midstream Energy Giants: Enterprise and Enbridge, as North American midstream energy companies, own energy infrastructure and charge fees for usage, ensuring their financial performance is not reliant on oil and gas prices, thus maintaining stable cash flows throughout the energy cycle.

- Long-Term Dividend Sustainability: Exxon, Chevron, Enterprise, and Enbridge have all proven their ability to continue paying and increasing dividends despite fluctuations in oil prices, making them suitable for dividend investors focused on long-term returns.

See More

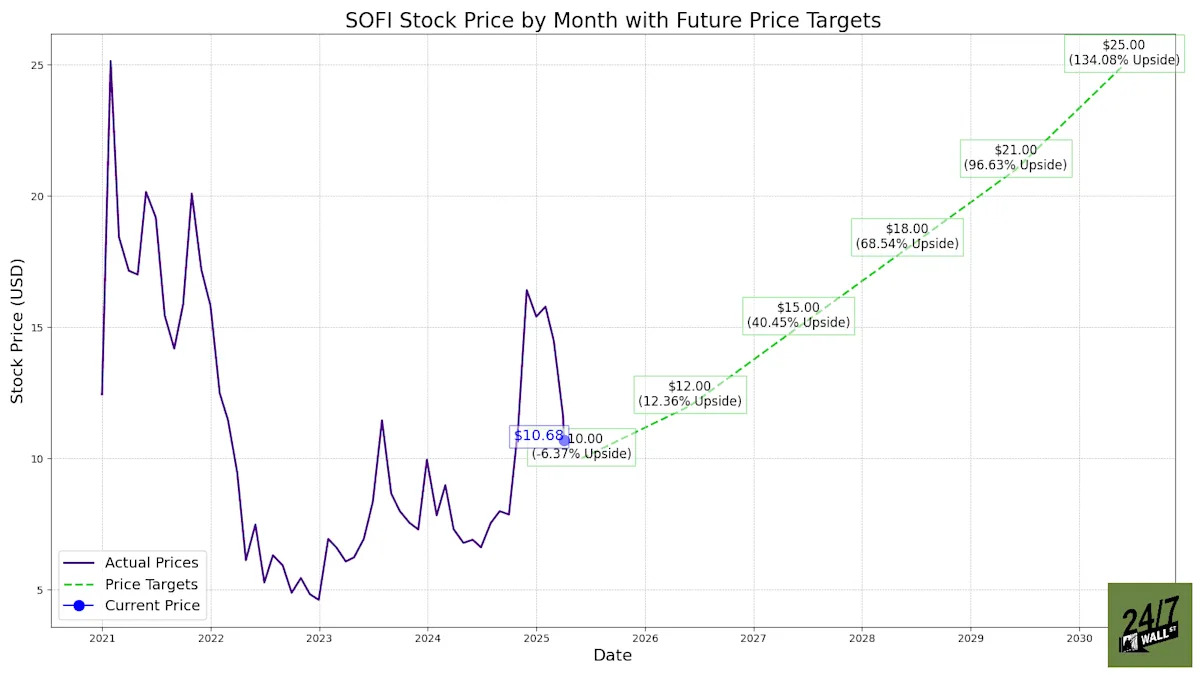

SoFi Q1 2026 Earnings Beat Estimates but Shares Drop

- Earnings Beat: SoFi reported Q1 2026 revenue of $1.10 billion, exceeding estimates by 5%, with record loan originations of $12.18 billion, up 68% year-over-year, indicating robust business growth potential.

- Stock Price Decline: Despite strong revenue, shares fell 15.44% post-earnings due to a 27% decline in Technology Platform revenue from a major client loss and a 63 basis point compression in net interest margin, suggesting an excessive market reaction to a single client issue.

- Positive Outlook: Management guided for FY2026 adjusted revenue of $4.66 billion, a 30% increase, with deposits reaching $40.24 billion, funding over 90% of liabilities, showcasing a strong funding base and ongoing growth potential.

- Investment Opportunity: Analysts see a 26.05% upside from the current price of $15.53 to the 12-month target of $19.57, recommending a buy with high conviction, reflecting confidence in SoFi's long-term growth despite current challenges.

See More

Nvidia Reaches $5 Trillion Valuation Again, Eyes $6 Trillion

- Valuation Recovery: Nvidia first crossed the $5 trillion valuation threshold in October 2025 and retreated, but it bounced back to this level in April 2026, demonstrating strong market resilience and indicating the company's ongoing leadership in technology.

- Growth Potential: To grow from $5 trillion to $6 trillion, Nvidia's stock needs to rise by 20%, which is significantly higher than the average annual return of the S&P 500, highlighting its strong appeal as an investment choice that may attract more investor attention.

- Earnings Forecast: Analysts project Nvidia will achieve $371 billion in revenue by the end of fiscal year 2027, and with a 56% net income margin over the past 12 months, net income is expected to exceed $200 billion, indicating the company can easily surpass the $6 trillion valuation threshold by year-end.

- Valuation Advantage: Although Nvidia currently trades at a price-to-earnings ratio of 43.5, significantly above the conservative estimate of 30, its sustained high profitability and market demand may allow it to continue trading at a premium, further solidifying its market position.

See More

Nvidia's Market Cap Poised to Exceed $6 Trillion

- Valuation Growth Potential: Nvidia first crossed the $5 trillion market cap in October 2025 and is poised to reach $6 trillion within 2026, requiring a 20% stock price increase, which highlights its robust growth potential.

- Profitability Analysis: Analysts project Nvidia's revenue will hit $371 billion by the end of fiscal year 2027, and with a 56% net income margin, it could exceed $208 billion in net income, comfortably surpassing the $200 billion needed for a $6 trillion valuation.

- Valuation Comparison: Currently trading at a P/E ratio of 43.5, Nvidia is significantly above the 30 times earnings valuation of its peers, indicating strong market expectations for its future growth and reinforcing its potential to become a $6 trillion company.

- Investment Advice: While Nvidia is considered a strong investment choice, the Motley Fool analyst team has identified 10 stocks deemed more valuable, advising investors to carefully consider their options before making decisions.

See More

Nvidia's Earnings Growth Expected to Accelerate Over Next Three Years

- Market Share Expansion: Nvidia's upcoming Vera Rubin processors are expected to reduce inference costs by 90%, significantly enhancing its competitiveness in the AI inference market, with projected data center sales reaching $1 trillion in 2026 and 2027, a substantial increase from the previous $500 billion forecast.

- Strong Profitability: Nvidia anticipates a 75% increase in earnings per share for the current fiscal year, reaching $8.34, far exceeding the tech sector's estimated 44% year-over-year growth, showcasing its robust profitability and market leadership in the AI sector.

- Partnership Growth: Nvidia has established partnerships with leading AI companies such as Anthropic, Meta, xAI, and OpenAI, providing a stable demand source as these companies see strong adoption of their AI inference applications, further solidifying Nvidia's market position.

- Long-Term Growth Potential: Despite Nvidia's current P/E ratio of 42.5, significantly higher than the Nasdaq-100's 33.4, its strong earnings growth potential justifies this valuation, with expectations of surpassing a $10 trillion market cap within the next three years, attracting more investor interest.

See More

NVIDIA Has Not Sold H200 Chips to Chinese Firms Amid Trade Concerns

- Sales Delay: NVIDIA has not sold its H200 AI chips to Chinese enterprises, as reported by Secretary Howard Lutnick, who attributed the delay to China's government banning acquisitions to favor domestic market investment, highlighting the tension in US-China trade relations.

- Policy Impact: The Trump administration approved shipments of H200 chips to China in January with conditions, raising concerns among US lawmakers about potential military applications, which has further complicated sales terms and slowed supply chains.

- Export Restrictions: Lutnick mentioned that the affiliates rule blocking exports to thousands of Chinese businesses is still under consideration, linked to broader trade negotiations, indicating that policy uncertainty may affect NVIDIA's market strategy.

- Investment Potential: While NVIDIA is recognized as one of the best data center hardware stocks, analysts suggest that certain AI stocks may offer greater upside potential and lower downside risk, reflecting a diverse outlook on the AI sector.

See More

Investment Recommendations for High-Yield Energy Stocks

- Strong Energy Stock Performance: High energy prices have led Wall Street to push energy stock prices up, with expectations of strong financial performance for these companies, although history suggests oil prices will eventually fall, necessitating caution among investors.

- Chevron vs. Exxon: Chevron offers a dividend yield of 3.6%, notably higher than Exxon's 2.6%, with both companies demonstrating reliability across the energy cycle and possessing strong balance sheets, making Chevron more attractive for income-focused investors.

- Midstream Energy Giants: Enterprise and Enbridge, as North American midstream energy companies, own energy infrastructure and charge fees for usage, ensuring their financial performance is not reliant on oil and gas prices, thus maintaining stable cash flows throughout the energy cycle.

- Long-Term Dividend Sustainability: Exxon, Chevron, Enterprise, and Enbridge have all proven their ability to continue paying and increasing dividends despite fluctuations in oil prices, making them suitable for dividend investors focused on long-term returns.

See More

SoFi Q1 2026 Earnings Beat Estimates but Shares Drop

- Earnings Beat: SoFi reported Q1 2026 revenue of $1.10 billion, exceeding estimates by 5%, with record loan originations of $12.18 billion, up 68% year-over-year, indicating robust business growth potential.

- Stock Price Decline: Despite strong revenue, shares fell 15.44% post-earnings due to a 27% decline in Technology Platform revenue from a major client loss and a 63 basis point compression in net interest margin, suggesting an excessive market reaction to a single client issue.

- Positive Outlook: Management guided for FY2026 adjusted revenue of $4.66 billion, a 30% increase, with deposits reaching $40.24 billion, funding over 90% of liabilities, showcasing a strong funding base and ongoing growth potential.

- Investment Opportunity: Analysts see a 26.05% upside from the current price of $15.53 to the 12-month target of $19.57, recommending a buy with high conviction, reflecting confidence in SoFi's long-term growth despite current challenges.

See More

Nvidia Reaches $5 Trillion Valuation Again, Eyes $6 Trillion

- Valuation Recovery: Nvidia first crossed the $5 trillion valuation threshold in October 2025 and retreated, but it bounced back to this level in April 2026, demonstrating strong market resilience and indicating the company's ongoing leadership in technology.

- Growth Potential: To grow from $5 trillion to $6 trillion, Nvidia's stock needs to rise by 20%, which is significantly higher than the average annual return of the S&P 500, highlighting its strong appeal as an investment choice that may attract more investor attention.

- Earnings Forecast: Analysts project Nvidia will achieve $371 billion in revenue by the end of fiscal year 2027, and with a 56% net income margin over the past 12 months, net income is expected to exceed $200 billion, indicating the company can easily surpass the $6 trillion valuation threshold by year-end.

- Valuation Advantage: Although Nvidia currently trades at a price-to-earnings ratio of 43.5, significantly above the conservative estimate of 30, its sustained high profitability and market demand may allow it to continue trading at a premium, further solidifying its market position.

See More

Nvidia's Market Cap Poised to Exceed $6 Trillion

- Valuation Growth Potential: Nvidia first crossed the $5 trillion market cap in October 2025 and is poised to reach $6 trillion within 2026, requiring a 20% stock price increase, which highlights its robust growth potential.

- Profitability Analysis: Analysts project Nvidia's revenue will hit $371 billion by the end of fiscal year 2027, and with a 56% net income margin, it could exceed $208 billion in net income, comfortably surpassing the $200 billion needed for a $6 trillion valuation.

- Valuation Comparison: Currently trading at a P/E ratio of 43.5, Nvidia is significantly above the 30 times earnings valuation of its peers, indicating strong market expectations for its future growth and reinforcing its potential to become a $6 trillion company.

- Investment Advice: While Nvidia is considered a strong investment choice, the Motley Fool analyst team has identified 10 stocks deemed more valuable, advising investors to carefully consider their options before making decisions.

See More