Microsoft's Quarterly Results Disappoint Investors

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 6 days ago

0mins

Should l Buy MSFT?

Source: CNBC

- Disappointing Performance: Microsoft's latest quarterly report revealed that, despite Azure's growth forecast of 39% to 40% exceeding the market consensus of 37%, the overall performance was disappointing, leading to a 5% drop in stock price and a year-to-date decline of over 16%.

- Lackluster Market Reaction: Although cloud revenue reached $54 billion, up 29% year-over-year, analyst Jim Cramer pointed out that Microsoft's traditional software business is threatened by AI code-writing, which has dampened market confidence in its future performance.

- Divergent Analyst Ratings: While Cramer remains cautious about Microsoft, advising against buying at this time, the majority of Wall Street analysts maintain a bullish outlook, particularly with positive ratings from Bank of America, Morgan Stanley, and Goldman Sachs, indicating continued market confidence in Microsoft.

- Investor Sentiment Shift: Cramer reiterated his stance during CNBC's Investing Club meeting, suggesting that investors should refrain from purchasing Microsoft shares, reflecting a tension between investor concerns over future growth potential and analysts' optimistic projections.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 411.380

Low

500.00

Averages

631.36

High

678.00

Current: 411.380

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company. The Company develops and supports software, services, devices, and solutions. The Company’s segments include Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services. This segment primarily comprises: Office Commercial, Office Consumer, LinkedIn, and Dynamics business solutions. The Intelligent Cloud segment consists of server products and cloud services, including Azure and other cloud services, SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), and Nuance and GitHub; and Enterprise Services, including enterprise support services, industry solutions and Nuance professional services. The More Personal Computing segment primarily comprises Windows, Devices, Gaming, and search and news advertising.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft's Strong Earnings Amidst Stock Slump Suggests Potential Comeback

- Strong Earnings Report: Microsoft reported an 18% year-over-year revenue increase and a 20% rise in operating income for Q3 of fiscal 2026, indicating robust performance in the AI sector, despite a declining stock price.

- Cloud Computing Growth: Azure's revenue surged by 40% this quarter as clients utilize its computing power for AI model training, solidifying Microsoft's position as a key player in the cloud market and driving significant revenue growth.

- Booming AI Business: Microsoft's non-cloud AI segment achieved a $37 billion annual run rate with a staggering 123% year-over-year growth, showcasing the substantial returns from its AI investments, even as the stock price fails to reflect this success.

- Attractive Valuation: With an operating price-to-earnings ratio of about 21, Microsoft is trading at its lowest valuation in a decade, and given its strong business fundamentals, a stock rebound is anticipated, presenting a compelling buying opportunity for investors.

See More

Microsoft: A Blue-Chip Stock for Generations

- Financial Robustness: Microsoft reported $82.9 billion in revenue for the most recent quarter, surpassing the combined revenues of Broadcom, Lenovo, and IBM over the past four quarters, demonstrating its strong profitability and market leadership, which ensures resilience during economic fluctuations.

- Diversified Business Model: As the world's largest enterprise software provider, Microsoft's operations span operating systems, cloud platforms, hardware, and social media, creating a robust ecosystem that businesses heavily rely on for daily operations, enhancing its strategic significance.

- Stable Dividend Growth: Although Microsoft has a modest dividend yield of 0.8%, it has increased its dividend by 152% over the past decade and has raised its dividend for 21 consecutive years, showcasing its stable cash flow and commitment to shareholders, positioning it to potentially become a Dividend King.

- Cash Reserve Advantage: With $78.3 billion in cash reserves, Microsoft has a safety net that allows it to navigate economic uncertainties while actively pursuing new technologies, particularly in artificial intelligence, thereby enhancing its competitive edge in the tech industry.

See More

Meta's Investments and Challenges in AI Sector

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, reflecting a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core advertising business and providing funding for future investments.

- AI Model Launch: The introduction of Meta's new AI model, Muse Spark, claims to outperform common models in several areas, showcasing the company's potential and commitment in the AI sector, although its market adoption remains to be seen.

- Capital Expenditure Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which has raised skepticism among investors, yet remains conservative compared to other tech giants.

- Vertical Integration Goal: By developing custom AI chips in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration process, although this requires substantial investment, it will enhance control over its AI ecosystem in the long run.

See More

Meta's Advertising Revenue Sees Significant Growth

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core business that funds other ventures.

- Skepticism Over Capex Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, although this increased forecast still raises skepticism among investors due to past missteps.

- AI Strategic Development: The recent launch of Meta's AI model Muse Spark, which outperforms common models, signifies its growing competitiveness in AI, while partnerships with Broadcom for custom chips aim to reduce reliance on external GPUs and cut computing costs.

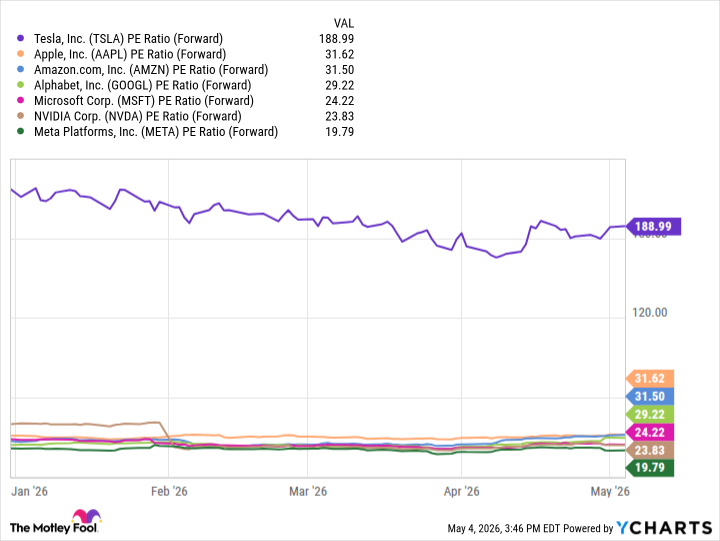

- Market Valuation Shift: Despite a nearly 6% decline in Meta's stock this year, its price-to-earnings ratio stands at 19.8, lower than other

See More

Meta Platforms Stock Slides into Value Territory

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating that its core advertising business remains robust and can fund future investments.

- AI Investment Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which, despite raising investor skepticism, is crucial for maintaining a competitive edge in the AI race.

- AI Model Launch: The recent release of Meta's AI model, Muse Spark, which outperforms common models in several areas, suggests potential in the AI space, although its adoption remains to be seen, indicating a shift in market perception of Meta's capabilities.

- Vertical Integration Strategy: By developing custom application-specific integrated circuits in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration within the AI ecosystem.

See More

Iran and US Peace Talks Spark Market Optimism

- Peace Proposal Review: A spokesperson for Iran's foreign ministry announced that Iran is reviewing a U.S. peace proposal, indicating that both nations are nearing an agreement to end the war and address key issues, which could positively impact market sentiment.

- Oil Price Fluctuations: Reports of a potential agreement between the U.S. and Iran led to a sharp decline in crude oil prices on Wednesday, although prices have stabilized since, as traders continue to monitor developments in the Middle East closely.

- Global Stock Market Rally: Global stocks are experiencing a relief rally, with Japan's Nikkei 225 index reopening after a holiday and surpassing 62,000 for the first time, driven by a 16% surge in Softbank shares, reflecting strong investor confidence in tech stocks.

- Corporate Growth Challenges: Anthropic's CEO stated that the company faced an 80-fold increase in revenue and usage in Q1, which has made it difficult to keep up with demand, highlighting the intense market appetite for AI technology despite challenges in computing capacity.

See More

Microsoft's Strong Earnings Amidst Stock Slump Suggests Potential Comeback

- Strong Earnings Report: Microsoft reported an 18% year-over-year revenue increase and a 20% rise in operating income for Q3 of fiscal 2026, indicating robust performance in the AI sector, despite a declining stock price.

- Cloud Computing Growth: Azure's revenue surged by 40% this quarter as clients utilize its computing power for AI model training, solidifying Microsoft's position as a key player in the cloud market and driving significant revenue growth.

- Booming AI Business: Microsoft's non-cloud AI segment achieved a $37 billion annual run rate with a staggering 123% year-over-year growth, showcasing the substantial returns from its AI investments, even as the stock price fails to reflect this success.

- Attractive Valuation: With an operating price-to-earnings ratio of about 21, Microsoft is trading at its lowest valuation in a decade, and given its strong business fundamentals, a stock rebound is anticipated, presenting a compelling buying opportunity for investors.

See More

Microsoft: A Blue-Chip Stock for Generations

- Financial Robustness: Microsoft reported $82.9 billion in revenue for the most recent quarter, surpassing the combined revenues of Broadcom, Lenovo, and IBM over the past four quarters, demonstrating its strong profitability and market leadership, which ensures resilience during economic fluctuations.

- Diversified Business Model: As the world's largest enterprise software provider, Microsoft's operations span operating systems, cloud platforms, hardware, and social media, creating a robust ecosystem that businesses heavily rely on for daily operations, enhancing its strategic significance.

- Stable Dividend Growth: Although Microsoft has a modest dividend yield of 0.8%, it has increased its dividend by 152% over the past decade and has raised its dividend for 21 consecutive years, showcasing its stable cash flow and commitment to shareholders, positioning it to potentially become a Dividend King.

- Cash Reserve Advantage: With $78.3 billion in cash reserves, Microsoft has a safety net that allows it to navigate economic uncertainties while actively pursuing new technologies, particularly in artificial intelligence, thereby enhancing its competitive edge in the tech industry.

See More

Meta's Investments and Challenges in AI Sector

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, reflecting a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core advertising business and providing funding for future investments.

- AI Model Launch: The introduction of Meta's new AI model, Muse Spark, claims to outperform common models in several areas, showcasing the company's potential and commitment in the AI sector, although its market adoption remains to be seen.

- Capital Expenditure Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which has raised skepticism among investors, yet remains conservative compared to other tech giants.

- Vertical Integration Goal: By developing custom AI chips in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration process, although this requires substantial investment, it will enhance control over its AI ecosystem in the long run.

See More

Meta's Advertising Revenue Sees Significant Growth

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating the strength of its core business that funds other ventures.

- Skepticism Over Capex Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, although this increased forecast still raises skepticism among investors due to past missteps.

- AI Strategic Development: The recent launch of Meta's AI model Muse Spark, which outperforms common models, signifies its growing competitiveness in AI, while partnerships with Broadcom for custom chips aim to reduce reliance on external GPUs and cut computing costs.

- Market Valuation Shift: Despite a nearly 6% decline in Meta's stock this year, its price-to-earnings ratio stands at 19.8, lower than other

See More

Meta Platforms Stock Slides into Value Territory

- Advertising Revenue Surge: Meta's advertising revenue reached $55 billion in Q1, marking a 33% year-over-year increase and accounting for nearly 98% of total revenue, indicating that its core advertising business remains robust and can fund future investments.

- AI Investment Plans: Meta expects capital expenditures to range between $125 billion and $145 billion in 2023, primarily for new data centers and AI infrastructure, which, despite raising investor skepticism, is crucial for maintaining a competitive edge in the AI race.

- AI Model Launch: The recent release of Meta's AI model, Muse Spark, which outperforms common models in several areas, suggests potential in the AI space, although its adoption remains to be seen, indicating a shift in market perception of Meta's capabilities.

- Vertical Integration Strategy: By developing custom application-specific integrated circuits in partnership with Broadcom, Meta aims to reduce reliance on Nvidia and AMD, thereby lowering computing costs and accelerating its vertical integration within the AI ecosystem.

See More

Iran and US Peace Talks Spark Market Optimism

- Peace Proposal Review: A spokesperson for Iran's foreign ministry announced that Iran is reviewing a U.S. peace proposal, indicating that both nations are nearing an agreement to end the war and address key issues, which could positively impact market sentiment.

- Oil Price Fluctuations: Reports of a potential agreement between the U.S. and Iran led to a sharp decline in crude oil prices on Wednesday, although prices have stabilized since, as traders continue to monitor developments in the Middle East closely.

- Global Stock Market Rally: Global stocks are experiencing a relief rally, with Japan's Nikkei 225 index reopening after a holiday and surpassing 62,000 for the first time, driven by a 16% surge in Softbank shares, reflecting strong investor confidence in tech stocks.

- Corporate Growth Challenges: Anthropic's CEO stated that the company faced an 80-fold increase in revenue and usage in Q1, which has made it difficult to keep up with demand, highlighting the intense market appetite for AI technology despite challenges in computing capacity.

See More