Meta Acquires Assured Robot Intelligence, Restructures Teams

Catch up on the top artificial intelligence news and commentary by Wall Street analysts on publicly traded companies in the space with this daily recap compiled by The Fly.USE OF AI:In an internal Q&A with staff, MetaCEO Mark Zuckerberg said the Facebook parent intends to shrink teams and make more new apps as AI changes workflows at the company, The Wall Street Journal's Meghan Bobrowsky, citing a recording of the Q&A. The CEO attributed the 8% drop in shares to investor worries over an upward revision in its expected capex spending and to its outlook for slower growth in Q2, the author says. "I think the trajectory that we're seeing for our businesses is still very strong," he said on the call. "But I think Q1 was, like, really insanely strong and Q2 is merely strong, and I think the combination of that and the capex increase is what drove the near-term reaction. But I don't know." Zuckerberg added that there was a "trajectory change" in the company's ad business following the start of the U.S.-Iran war, the author notes. "If oil prices go up then consumers spend more of their money on oil, on gas, and less on things that they would just buy that are just kind of discretionary things that the advertising might serve," he said.ASSURED ROBOT INTELLIGENCE:Meta is acquiring Assured Robot Intelligence, a startup working on AI models for robots, Bloomberg's Mark Gurman. A spokesperson told Bloomberg that the Facebook parent closed the acquisition Friday, with terms not disclosed. The startup's team will join the Meta Superintelligence Labs research unit, the author notes.ADVANCED ACCOUNT SECURITY:OpenAI is introducing Advanced Account Security, a new opt-in setting for ChatGPT accounts, designed for people at increased risk of digital attacks, as well as for those who want the strongest account protections available. The company believes it brings together a set of heightened security measures that help safeguard against account takeover while making those protections easier to activate in one place. Once enrolled, Advanced Account Security protects users in Codex as well. an increased responsibility for account recovery. Advanced Account Security requires passkeys or physical security keys while disabling password-based login, helping make phishing-resistant sign-in the default for people who need it most. If a user's email account or phone number is compromised, an attacker may try to use one of them to gain access to their ChatGPT account via e-mail or SMS based recovery. To reduce this risk, Advanced Account Security disables email and SMS recovery and requires stronger recovery methods: backup passkeys, security keys, and recovery keys. Sign-in sessions are shortened to reduce the window of exposure if a device or active session is compromised. People working with especially sensitive information may opt not to have those conversations used for model training. "Using physical security keys, such as YubiKeys, is one of the strongest defenses against phishing. To make that level of protection easier to access, we have partnered with Yubico, a leader in hardware-based authentication and account protection, to offer our users preferred pricing on a customized bundle of best in class security keys. The YubiKey C Nano is designed to stay in your laptop for simple, low-friction daily authentication, and the YubiKey C NFC for backup, and use across laptops and mobile devices," OpenAI added.CLAUDE SECURITY:Anthropic said in aon X, formerly Twitter, that Claude Security is now in public beta for Claude Enterprise customers. "Claude scans your codebase for vulnerabilities, validates each finding to cut false positives, and suggests patches you can review and approve," the company said. "Many security teams have asked how to put Opus 4.7 to work on their code without standing up custom tooling. Claude Security is that on-ramp: no API integration or agent build required. Since the research preview in February, hundreds of organizations have used it on production code, catching issues existing scanners had missed. Based on early feedback, we've added scheduled scans, directory-level targeting, CSV and Markdown exports, webhook notifications for new findings, and dismissals that carry forward across scans." Publicly traded companies in the cybersecurity space include Check Point (CHKP), CrowdStrike, CyberArk, F5, Fortinet, Gen Digital, Okta, Palo Alto Networksand Qualys.

Trade with 70% Backtested Accuracy

Analyst Views on META

About META

About the author

Meta Plans to Rent Out AI Computing Capacity

- AI Infrastructure Expansion: Meta Platforms has aggressively built AI infrastructure over the past few years, particularly for training its Llama models, with capital expenditures expected to exceed $145 billion in 2026, indicating the company's ongoing investment and growth potential in the AI sector.

- New Revenue Stream: Meta may create a new revenue stream by renting out its excess computing capacity, a strategy similar to SpaceX's successful model, which could generate over $2 billion in monthly revenue, highlighting the profitability potential of this market.

- User Growth Challenges: Despite attracting over 3.5 billion users daily across its social media apps, Meta is addressing stagnant advertising growth by enhancing user engagement through AI, which helps increase ad revenue and mitigates growth stagnation in its advertising business.

- Attractive Market Valuation: With a current P/E ratio of 21.2, which is 25% lower than its 10-year average, Meta's stock appears undervalued, suggesting that investors may consider long-term investment despite uncertainties surrounding its potential cloud business.

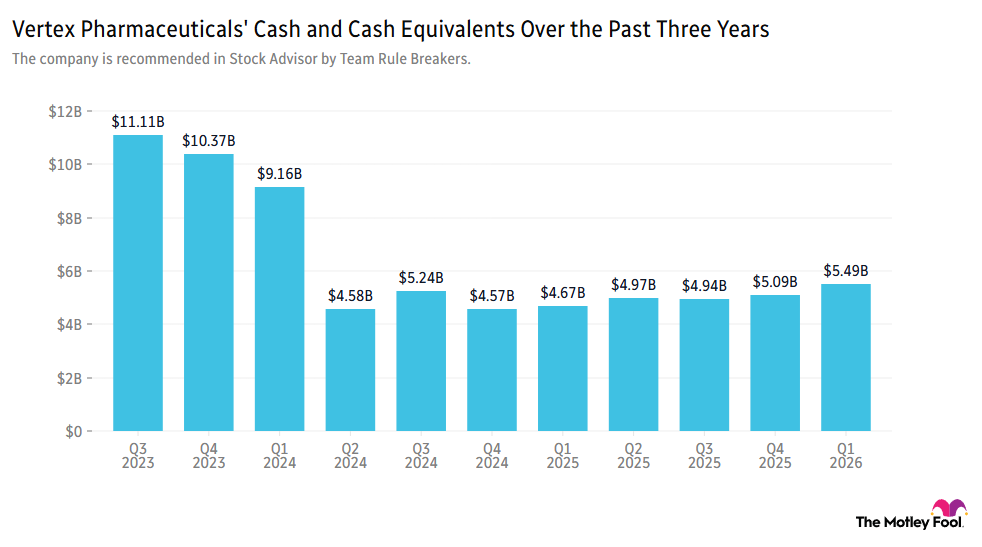

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

SpaceX IPO Sets Record but Faces Challenges Ahead

- Record IPO Financing: SpaceX raised $85.7 billion in its IPO, nearly tripling Saudi Aramco's previous record of $29.4 billion, demonstrating strong market confidence in its AI and space infrastructure ventures.

- Significant Valuation Fluctuations: Although SpaceX's valuation approached $3 trillion post-IPO, it has since retraced to $2.13 trillion as of July 2, with a share price still 20% above its IPO listing, reflecting cautious market sentiment regarding its future performance.

- Complex Lockup Period: SpaceX sold only about 5% of its outstanding shares in its IPO, with the float expected to increase rapidly in the coming months as insiders become eligible to sell, potentially exerting downward pressure on the stock price.

- High Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical average of 30, SpaceX's stock faces substantial correction risks, particularly amid fluctuating market emotions and investor sentiment.

Meta's Plans to Compete in Cloud Computing Market Impact Neocloud Providers

- Stock Price Volatility: Following news of Meta's plans to enter the cloud computing market, CoreWeave's stock plummeted nearly 14% in a single day, while Nebius dropped 17%, reflecting market concerns about the future prospects of both companies, especially with Meta as a customer.

- Massive Contract Expansion: CoreWeave expanded its agreement with Meta in April 2023 to provide cloud computing capacity through 2032, valued at $21 billion, while Nebius announced in March it would provide $12 billion in cloud capacity, showcasing the strong collaborative potential in the AI data center sector.

- Sustained Demand Growth: Despite the competitive threat from Meta, demand for AI data centers from CoreWeave and Nebius remains robust, with CoreWeave noting that its 2026 capacity is largely sold out and 30% of its $99.4 billion revenue backlog comes from foundational AI labs, indicating urgent market demand for their services.

- Investment Opportunity Emerges: Although Meta's plans could impact CoreWeave and Nebius, the demand for AI data centers far exceeds supply, making the current stock price pullback a buying opportunity, particularly as CoreWeave's price-to-sales ratio is only 6.6, indicating potential investment value.

SpaceX IPO Raises Record $85.7 Billion

- Record IPO Financing: SpaceX's IPO on June 12 raised an unprecedented $85.7 billion, nearly tripling Saudi Aramco's previous record of $29.4 billion, indicating strong market confidence in its future potential.

- Market Performance Volatility: Although the company's market cap briefly approached $3 trillion post-IPO, it retraced to $2.13 trillion by July 2, with a share price still 20% above the IPO price, reflecting investor caution regarding long-term performance.

- Lockup Period Challenges: SpaceX's staggered lockup schedule allowed only about 5% of shares to be sold initially, with a significant number of insiders expected to sell their shares in the coming months, which could exert downward pressure on the stock price.

- Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical threshold of 30, SpaceX faces substantial challenges in sustaining profitability, leading to market expectations that its stock price may fall below $100 before the end of 2026.

Meta Enters AI Data Center Market, Impact on CoreWeave and Nebius

- Increased Competition: Meta's plan to enter the AI data center market led to a 14% and 17% drop in CoreWeave and Nebius shares respectively, indicating market concerns over new competition that could impact future revenue growth for both companies.

- Shifting Customer Dynamics: CoreWeave's agreement with Meta has been extended to 2032, valued at $21 billion, while Nebius has committed to providing $12 billion in cloud computing capacity, highlighting the importance of their business relationships despite increased competition.

- Strong Demand Continues: CoreWeave's AI cloud platform demand is nearing saturation for 2026, with 30% of its $99.4 billion revenue backlog coming from foundational AI labs, showcasing its robust market position and growth potential.

- Optimistic Industry Outlook: According to Goldman Sachs, U.S. data center power demand is projected to double to 66GW by 2027, indicating that the demand for AI data centers will continue to grow, positioning CoreWeave and Nebius to benefit from this trend.

Meta Plans to Rent Out AI Computing Capacity

- AI Infrastructure Expansion: Meta Platforms has aggressively built AI infrastructure over the past few years, particularly for training its Llama models, with capital expenditures expected to exceed $145 billion in 2026, indicating the company's ongoing investment and growth potential in the AI sector.

- New Revenue Stream: Meta may create a new revenue stream by renting out its excess computing capacity, a strategy similar to SpaceX's successful model, which could generate over $2 billion in monthly revenue, highlighting the profitability potential of this market.

- User Growth Challenges: Despite attracting over 3.5 billion users daily across its social media apps, Meta is addressing stagnant advertising growth by enhancing user engagement through AI, which helps increase ad revenue and mitigates growth stagnation in its advertising business.

- Attractive Market Valuation: With a current P/E ratio of 21.2, which is 25% lower than its 10-year average, Meta's stock appears undervalued, suggesting that investors may consider long-term investment despite uncertainties surrounding its potential cloud business.

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

SpaceX IPO Sets Record but Faces Challenges Ahead

- Record IPO Financing: SpaceX raised $85.7 billion in its IPO, nearly tripling Saudi Aramco's previous record of $29.4 billion, demonstrating strong market confidence in its AI and space infrastructure ventures.

- Significant Valuation Fluctuations: Although SpaceX's valuation approached $3 trillion post-IPO, it has since retraced to $2.13 trillion as of July 2, with a share price still 20% above its IPO listing, reflecting cautious market sentiment regarding its future performance.

- Complex Lockup Period: SpaceX sold only about 5% of its outstanding shares in its IPO, with the float expected to increase rapidly in the coming months as insiders become eligible to sell, potentially exerting downward pressure on the stock price.

- High Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical average of 30, SpaceX's stock faces substantial correction risks, particularly amid fluctuating market emotions and investor sentiment.

Meta's Plans to Compete in Cloud Computing Market Impact Neocloud Providers

- Stock Price Volatility: Following news of Meta's plans to enter the cloud computing market, CoreWeave's stock plummeted nearly 14% in a single day, while Nebius dropped 17%, reflecting market concerns about the future prospects of both companies, especially with Meta as a customer.

- Massive Contract Expansion: CoreWeave expanded its agreement with Meta in April 2023 to provide cloud computing capacity through 2032, valued at $21 billion, while Nebius announced in March it would provide $12 billion in cloud capacity, showcasing the strong collaborative potential in the AI data center sector.

- Sustained Demand Growth: Despite the competitive threat from Meta, demand for AI data centers from CoreWeave and Nebius remains robust, with CoreWeave noting that its 2026 capacity is largely sold out and 30% of its $99.4 billion revenue backlog comes from foundational AI labs, indicating urgent market demand for their services.

- Investment Opportunity Emerges: Although Meta's plans could impact CoreWeave and Nebius, the demand for AI data centers far exceeds supply, making the current stock price pullback a buying opportunity, particularly as CoreWeave's price-to-sales ratio is only 6.6, indicating potential investment value.

SpaceX IPO Raises Record $85.7 Billion

- Record IPO Financing: SpaceX's IPO on June 12 raised an unprecedented $85.7 billion, nearly tripling Saudi Aramco's previous record of $29.4 billion, indicating strong market confidence in its future potential.

- Market Performance Volatility: Although the company's market cap briefly approached $3 trillion post-IPO, it retraced to $2.13 trillion by July 2, with a share price still 20% above the IPO price, reflecting investor caution regarding long-term performance.

- Lockup Period Challenges: SpaceX's staggered lockup schedule allowed only about 5% of shares to be sold initially, with a significant number of insiders expected to sell their shares in the coming months, which could exert downward pressure on the stock price.

- Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical threshold of 30, SpaceX faces substantial challenges in sustaining profitability, leading to market expectations that its stock price may fall below $100 before the end of 2026.

Meta Enters AI Data Center Market, Impact on CoreWeave and Nebius

- Increased Competition: Meta's plan to enter the AI data center market led to a 14% and 17% drop in CoreWeave and Nebius shares respectively, indicating market concerns over new competition that could impact future revenue growth for both companies.

- Shifting Customer Dynamics: CoreWeave's agreement with Meta has been extended to 2032, valued at $21 billion, while Nebius has committed to providing $12 billion in cloud computing capacity, highlighting the importance of their business relationships despite increased competition.

- Strong Demand Continues: CoreWeave's AI cloud platform demand is nearing saturation for 2026, with 30% of its $99.4 billion revenue backlog coming from foundational AI labs, showcasing its robust market position and growth potential.

- Optimistic Industry Outlook: According to Goldman Sachs, U.S. data center power demand is projected to double to 66GW by 2027, indicating that the demand for AI data centers will continue to grow, positioning CoreWeave and Nebius to benefit from this trend.