Market Update: Nvidia and Software Sector Insights

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy NVDA?

Source: CNBC

- Nvidia Stock Fluctuations: Nvidia's shares have fallen 13.5% from their October peak, and while they have gained 50% over the past year, they are down 1.76% so far in 2026, indicating market caution regarding its future performance.

- Software Sector Struggles: The S&P Software & Services Index has dropped 26% from its October 28 high and is down 18% year-to-date in 2026, reflecting concerns that artificial intelligence may replace traditional software, leading to poor overall sector performance.

- Vertiv's Strong Performance: Vertiv's stock has surged nearly 203% over the past year, despite a 4% decline from last week's high, as demand for its cooling equipment and power management systems for data centers continues to grow, showcasing the positive impact of the AI wave.

- Lululemon Earnings Outlook: Lululemon is set to report earnings after the bell on Tuesday, having lost 22% in the past three months and 54% from last March's high, with market expectations for its future performance being relatively low.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 180.250

Low

200.00

Averages

264.97

High

352.00

Current: 180.250

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is a full-stack computing infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. The Company’s segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing platforms and artificial intelligence (AI) solutions and software; networking; automotive platforms and autonomous and electric vehicle solutions; Jetson for robotics and other embedded platforms, and DGX Cloud computing services. The Graphics segment includes GeForce GPUs for gaming and PCs, the GeForce NOW game streaming service and related infrastructure, and solutions for gaming platforms; Quadro/NVIDIA RTX GPUs for enterprise workstation graphics; virtual GPU software for cloud-based visual and virtual computing; automotive platforms for infotainment systems, and Omniverse Enterprise software for building and operating industrial AI and digital twin applications.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia Projects Over $1 Trillion Revenue by 2027

- Revenue Surge Expected: Nvidia anticipates generating at least $1 trillion in revenue by 2027, driven by accelerating demand for artificial intelligence computing infrastructure, indicating strong market confidence and growth in AI technology.

- CEO Keynote Highlights: Founder and CEO Jensen Huang emphasized at GTC 2026 that the shift of AI systems from training to large-scale inference has led to a significant increase in computing requirements, marking a pivotal moment for the industry.

- Demand Comparison Analysis: Huang noted that last year at this time, the company projected a demand of $500 billion, which has now doubled, showcasing robust purchase orders and confidence in the Blackwell and Ruben products.

- Stock Price Reaction: At the time of the announcement, Nvidia's shares rose approximately 1%, reflecting the market's positive outlook on the company's future growth potential and further solidifying its leadership position in the AI sector.

See More

Nvidia GTC Conference Preview: Strong AI Demand Ahead

- Strong AI Demand: Gene Munster from Deepwater indicates that Nvidia will emphasize at the GTC conference that demand for AI infrastructure exceeds investor expectations, even as concerns about growth slowing in 2027 intensify, with Huang likely reiterating that AI's utility has reached an 'inflection point.'

- Economic Benefits of Rubin Architecture: Munster expects Nvidia to elaborate on how the Rubin architecture will enhance inference economics, with investors focusing on key metrics such as cost per token, throughput, and performance per watt, which could shape industry perceptions of inference infrastructure.

- Full-Stack AI Infrastructure Strategy: Analyst Patrick Moorhead notes that Nvidia is transitioning from a semiconductor company to a comprehensive AI infrastructure platform, with hyperscaler AI spending expected to exceed $600 billion this year, providing Nvidia with unusually strong demand visibility and enhancing its market position.

- Market Sentiment Shift: Despite NVDA stock rising 56% over the past year, sentiment among Stocktwits users has shifted from 'neutral' to 'bearish,' reflecting investor unease about future growth, particularly ahead of the GTC conference where signals on AI demand are closely watched.

See More

Oracle's Cloud Infrastructure Outlook Brightens

- Cloud Infrastructure Revenue Outlook: Oracle anticipates a 77% revenue growth in its cloud infrastructure division for fiscal 2026, reaching $18 billion, with projections soaring to $144 billion by fiscal 2030, indicating robust market demand and growth potential.

- Remaining Performance Obligations Risk: While Oracle reported $455 billion in remaining performance obligations, $300 billion of which is tied to OpenAI, concerns arose regarding OpenAI's ability to fulfill its $1.4 trillion commitments, increasing Oracle's financial risk profile.

- Capital Expenditure Increase: In its fiscal 2026 second-quarter earnings report, Oracle raised its full-year capital expenditure guidance from $35 billion to $50 billion, and despite reporting negative free cash flow, investor concerns about risk remained unaddressed.

- OpenAI Financing Boost: OpenAI's recent successful $110 billion financing round, with a valuation of $730 billion, provides a solid runway for its future IPO and advertising initiatives, potentially enabling it to meet its infrastructure commitments with Oracle, thereby enhancing market confidence in Oracle's prospects.

See More

Oracle Expands Data Centers Amid AI Contracts

- Data Center Expansion: Oracle is building data centers that rent chips to companies seeking to run AI solutions, with projections indicating cloud infrastructure revenue could reach $158 billion by fiscal year 2030, reflecting strong market demand.

- Partnership with OpenAI: Oracle's performance is heavily reliant on a multi-year contract with OpenAI, which recently raised $110 billion, bolstering Oracle's confidence in future revenues, despite OpenAI's annual revenue being only $20 billion.

- Increased Capital Expenditure: In its fiscal 2026 second-quarter report, Oracle raised its capital expenditure guidance from $35 billion to $50 billion; although negative free cash flow raised investor concerns, strong remaining performance obligations (RPOs) of $553 billion indicate significant future growth potential.

- Positive Market Reaction: Following OpenAI's successful financing, Oracle's stock rebounded, with increased investor confidence in demand for its cloud infrastructure, and projections suggest it will exceed $18 billion in revenue this quarter, aligning with management's guidance.

See More

Asia-Pacific Markets Rise Amid Iran War Developments

- Market Rebound: Asia-Pacific markets broadly rose as investors monitored the latest developments in the Iran war, with Australia's S&P/ASX 200 index gaining 0.27%, indicating market resilience to geopolitical risks.

- Oil Price Fluctuations: International benchmark Brent crude futures fell 2.84% to $100.21 per barrel but rebounded to $101.58, reflecting market sensitivity to supply chain stability and short-term price volatility.

- Japanese Stock Performance: Japan's Nikkei 225 index rose 0.75%, while the Topix jumped over 1%, showcasing investor confidence in Japan's economic recovery amid increasing global economic uncertainty.

- Tech Stock Gains: Memory makers SK Hynix and Samsung Electronics rose over 3% and 4%, respectively, benefiting from Nvidia's CEO's forecast of $1 trillion in chip orders over the next few years, indicating strong demand in the tech sector.

See More

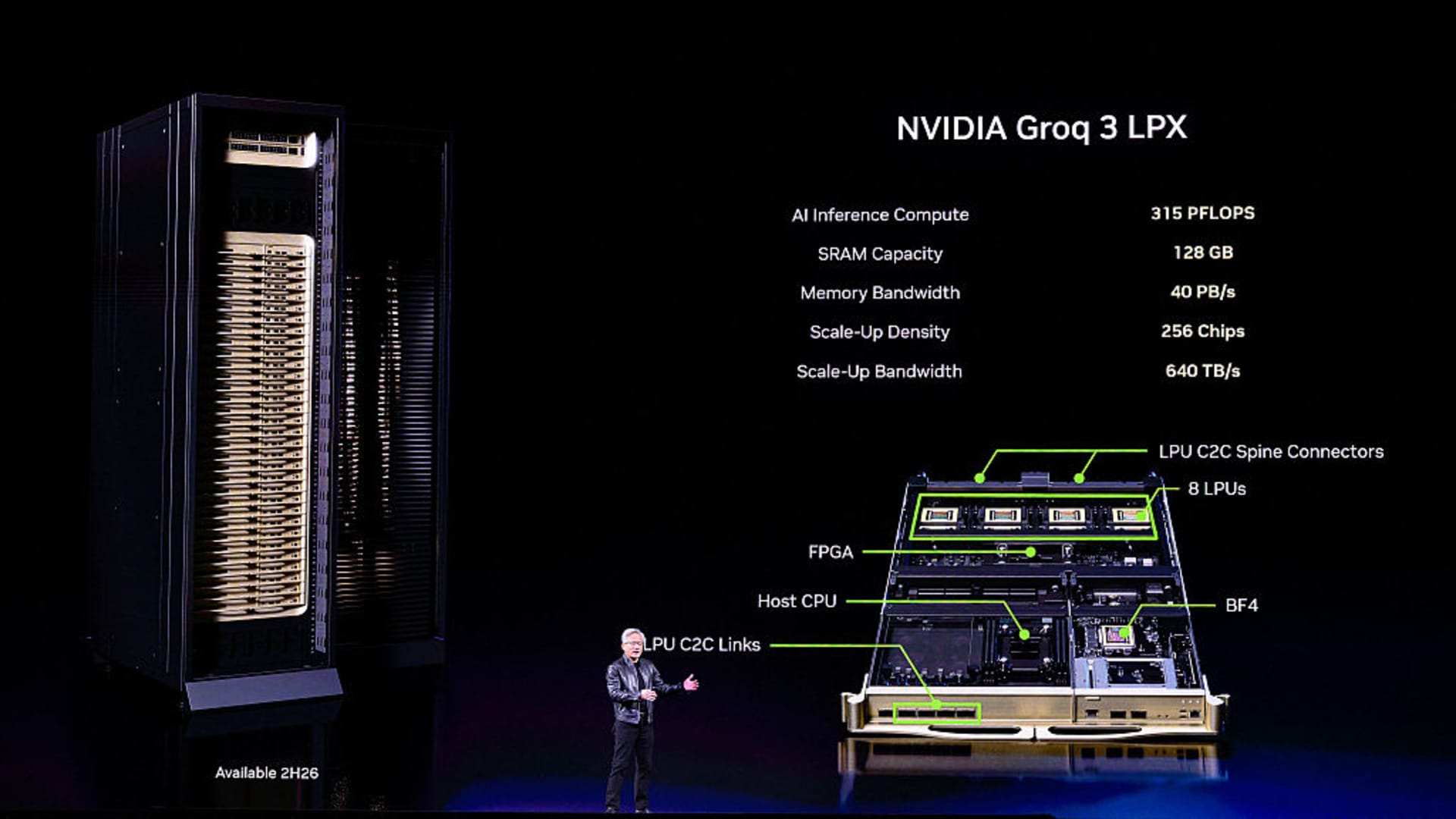

Nvidia Unveils New Inference Chip and Revenue Outlook

- New Inference Chip Launch: Nvidia unveiled its LPX inference chip, built on a $20 billion technology licensing deal with AI startup Groq, aimed at enhancing performance for low-latency inference tasks, and is set to launch alongside the Vera Rubin chip series, solidifying its market position in inference computing.

- Production and Market Strategy: The LPX chip is currently in volume production at third-party manufacturer Samsung and will be offered in server racks containing 256 LPX processors, with Nvidia planning to enhance overall data center performance by integrating LPX with Vera Rubin servers to meet diverse workload demands.

- Revenue Outlook Update: Nvidia expects orders for its Blackwell and Vera Rubin chips to reach $1 trillion by 2027, a significant increase from the $500 billion previously mentioned, reflecting strong confidence in future demand and potentially leading to upward revisions in market expectations for its 2027 data center revenue.

- Market Reaction and Analysis: Following Jensen Huang's announcement of the $1 trillion order outlook, Nvidia's stock briefly rose to $188.88 before closing at $183.22, with analysts suggesting that this news will bolster investor confidence in the sustainability of future AI spending, particularly in an active capital market environment.

See More

Nvidia Projects Over $1 Trillion Revenue by 2027

- Revenue Surge Expected: Nvidia anticipates generating at least $1 trillion in revenue by 2027, driven by accelerating demand for artificial intelligence computing infrastructure, indicating strong market confidence and growth in AI technology.

- CEO Keynote Highlights: Founder and CEO Jensen Huang emphasized at GTC 2026 that the shift of AI systems from training to large-scale inference has led to a significant increase in computing requirements, marking a pivotal moment for the industry.

- Demand Comparison Analysis: Huang noted that last year at this time, the company projected a demand of $500 billion, which has now doubled, showcasing robust purchase orders and confidence in the Blackwell and Ruben products.

- Stock Price Reaction: At the time of the announcement, Nvidia's shares rose approximately 1%, reflecting the market's positive outlook on the company's future growth potential and further solidifying its leadership position in the AI sector.

See More

Nvidia GTC Conference Preview: Strong AI Demand Ahead

- Strong AI Demand: Gene Munster from Deepwater indicates that Nvidia will emphasize at the GTC conference that demand for AI infrastructure exceeds investor expectations, even as concerns about growth slowing in 2027 intensify, with Huang likely reiterating that AI's utility has reached an 'inflection point.'

- Economic Benefits of Rubin Architecture: Munster expects Nvidia to elaborate on how the Rubin architecture will enhance inference economics, with investors focusing on key metrics such as cost per token, throughput, and performance per watt, which could shape industry perceptions of inference infrastructure.

- Full-Stack AI Infrastructure Strategy: Analyst Patrick Moorhead notes that Nvidia is transitioning from a semiconductor company to a comprehensive AI infrastructure platform, with hyperscaler AI spending expected to exceed $600 billion this year, providing Nvidia with unusually strong demand visibility and enhancing its market position.

- Market Sentiment Shift: Despite NVDA stock rising 56% over the past year, sentiment among Stocktwits users has shifted from 'neutral' to 'bearish,' reflecting investor unease about future growth, particularly ahead of the GTC conference where signals on AI demand are closely watched.

See More

Oracle's Cloud Infrastructure Outlook Brightens

- Cloud Infrastructure Revenue Outlook: Oracle anticipates a 77% revenue growth in its cloud infrastructure division for fiscal 2026, reaching $18 billion, with projections soaring to $144 billion by fiscal 2030, indicating robust market demand and growth potential.

- Remaining Performance Obligations Risk: While Oracle reported $455 billion in remaining performance obligations, $300 billion of which is tied to OpenAI, concerns arose regarding OpenAI's ability to fulfill its $1.4 trillion commitments, increasing Oracle's financial risk profile.

- Capital Expenditure Increase: In its fiscal 2026 second-quarter earnings report, Oracle raised its full-year capital expenditure guidance from $35 billion to $50 billion, and despite reporting negative free cash flow, investor concerns about risk remained unaddressed.

- OpenAI Financing Boost: OpenAI's recent successful $110 billion financing round, with a valuation of $730 billion, provides a solid runway for its future IPO and advertising initiatives, potentially enabling it to meet its infrastructure commitments with Oracle, thereby enhancing market confidence in Oracle's prospects.

See More

Oracle Expands Data Centers Amid AI Contracts

- Data Center Expansion: Oracle is building data centers that rent chips to companies seeking to run AI solutions, with projections indicating cloud infrastructure revenue could reach $158 billion by fiscal year 2030, reflecting strong market demand.

- Partnership with OpenAI: Oracle's performance is heavily reliant on a multi-year contract with OpenAI, which recently raised $110 billion, bolstering Oracle's confidence in future revenues, despite OpenAI's annual revenue being only $20 billion.

- Increased Capital Expenditure: In its fiscal 2026 second-quarter report, Oracle raised its capital expenditure guidance from $35 billion to $50 billion; although negative free cash flow raised investor concerns, strong remaining performance obligations (RPOs) of $553 billion indicate significant future growth potential.

- Positive Market Reaction: Following OpenAI's successful financing, Oracle's stock rebounded, with increased investor confidence in demand for its cloud infrastructure, and projections suggest it will exceed $18 billion in revenue this quarter, aligning with management's guidance.

See More

Asia-Pacific Markets Rise Amid Iran War Developments

- Market Rebound: Asia-Pacific markets broadly rose as investors monitored the latest developments in the Iran war, with Australia's S&P/ASX 200 index gaining 0.27%, indicating market resilience to geopolitical risks.

- Oil Price Fluctuations: International benchmark Brent crude futures fell 2.84% to $100.21 per barrel but rebounded to $101.58, reflecting market sensitivity to supply chain stability and short-term price volatility.

- Japanese Stock Performance: Japan's Nikkei 225 index rose 0.75%, while the Topix jumped over 1%, showcasing investor confidence in Japan's economic recovery amid increasing global economic uncertainty.

- Tech Stock Gains: Memory makers SK Hynix and Samsung Electronics rose over 3% and 4%, respectively, benefiting from Nvidia's CEO's forecast of $1 trillion in chip orders over the next few years, indicating strong demand in the tech sector.

See More

Nvidia Unveils New Inference Chip and Revenue Outlook

- New Inference Chip Launch: Nvidia unveiled its LPX inference chip, built on a $20 billion technology licensing deal with AI startup Groq, aimed at enhancing performance for low-latency inference tasks, and is set to launch alongside the Vera Rubin chip series, solidifying its market position in inference computing.

- Production and Market Strategy: The LPX chip is currently in volume production at third-party manufacturer Samsung and will be offered in server racks containing 256 LPX processors, with Nvidia planning to enhance overall data center performance by integrating LPX with Vera Rubin servers to meet diverse workload demands.

- Revenue Outlook Update: Nvidia expects orders for its Blackwell and Vera Rubin chips to reach $1 trillion by 2027, a significant increase from the $500 billion previously mentioned, reflecting strong confidence in future demand and potentially leading to upward revisions in market expectations for its 2027 data center revenue.

- Market Reaction and Analysis: Following Jensen Huang's announcement of the $1 trillion order outlook, Nvidia's stock briefly rose to $188.88 before closing at $183.22, with analysts suggesting that this news will bolster investor confidence in the sustainability of future AI spending, particularly in an active capital market environment.

See More