Management Team Expects Continued Growth

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 4 days ago

0mins

Should l Buy INTC?

Source: NASDAQ.COM

- Future Growth Outlook: The management team anticipates that strong performance will continue into next year, indicating robust market presence and sustained profitability, which may attract more investor interest.

- Key Industry Technology: A report highlights a little-known company termed an 'Indispensable Monopoly' that provides critical technology needed by Nvidia and Intel, potentially positioning it as a significant player in future market competition.

- Investment Recommendation Analysis: The Motley Fool's analyst team notes that Intel was not included in the current list of the top 10 recommended stocks, suggesting a cautious market sentiment regarding its future performance, which could influence investor decisions.

- Historical Return Comparison: Stock Advisor's average return of 991% significantly outperforms the S&P 500's 201%, indicating that investors should consider historical performance when selecting stocks to achieve higher investment returns.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy INTC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on INTC

Wall Street analysts forecast INTC stock price to fall

29 Analyst Rating

5 Buy

19 Hold

5 Sell

Hold

Current: 94.480

Low

20.00

Averages

39.30

High

52.00

Current: 94.480

Low

20.00

Averages

39.30

High

52.00

About INTC

Intel Corporation is a global designer and manufacturer of semiconductor products. The Company's segments include Intel Products, Intel Foundry, and All Other. Its Intel Products comprise Client Computing Group (CCG) and Data Center and AI (DCAI). CCG delivers platforms and processors that power PCs and edge devices, enabling enhanced performance, connectivity and user experience for consumer and commercial markets with capabilities that also support retail, industrial robotics and AI ecosystems at the edge. DCAI delivers workload-optimized solutions based upon its x86 architecture for data centers, including CPUs, AI accelerators, NICs, IPUs and custom ASICs, enabling performance and scalability for cloud, enterprise, telecommunication and HPC environments. The Intel Foundry segment comprises technology development, manufacturing and foundry services, developing new semiconductor process technologies and advanced packaging technologies. All Other segments include Mobileye and Other.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Intel's Huge Opportunity in Data Center CPU Market

- Stock Price Surge: Intel's stock has surged over 350% in the past year and more than 150% year-to-date, reflecting market optimism about its growth potential, yet its high valuation may limit further upside.

- Government Investment Support: The U.S. government invested $8.9 billion in Intel last year, acquiring nearly a 10% stake, which not only bolstered the company's financial position but also provided funding for future technological advancements.

- Increasing Competition: With companies like Arm Holdings and Nvidia entering the data center CPU market, Intel faces intensifying competition; despite its advantages in high-performance CPU demand, it continues to lose market share.

- Profitability Challenges: Intel's foundry business reported an operating loss of $2.4 billion last quarter, and while revenue increased, the path to profitability remains slow, necessitating cautious evaluation from investors regarding its future performance.

See More

SpaceX IPO Valuation Could Reach $2 Trillion

- IPO Expectations Soar: SpaceX is anticipated to announce its IPO in June, with analysts estimating a valuation target between $1.5 trillion and $1.75 trillion, and rumors suggest it could even reach $2 trillion, making it the largest IPO in history.

- Significant Market Potential: SpaceX's Starlink project controls around 70% of global satellites, expected to generate substantial revenue, and despite regulatory risks, its market outlook continues to attract investor interest.

- Lack of Financial Transparency: Although SpaceX is preparing for its IPO, it has yet to disclose financial statements, with PitchBook analysis suggesting a reasonable valuation between $1.1 trillion and $1.7 trillion, posing challenges for investors in assessing the company's value.

- Future Growth Potential: SpaceX is expected to publicly file an investment prospectus in May, which will allow investors to better evaluate its financials and determine whether the $2 trillion valuation is reasonable and if a 10x return on investment is feasible.

See More

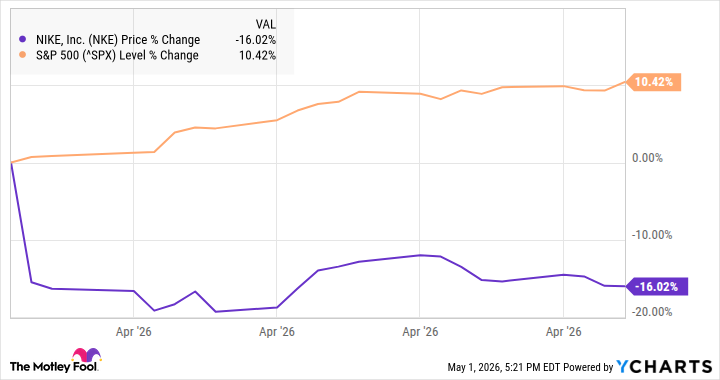

Nike Shares Drop 16% in April Amid Earnings Disappointment

- Earnings Disappointment: Nike reported third-quarter revenue of $11.3 billion, slightly above the $11.23 billion estimate, but a 3% decline on a currency-neutral basis indicates weak sales growth, undermining market confidence in its future performance.

- Stock Price Plunge: The stock fell sharply at the beginning of April due to disappointing earnings, finishing the month down 16%, and is now 75% below its all-time high, reflecting a collapse in business performance over the past five years.

- Leadership Changes: Nike's innovation chief, Tony Bignell, left the company after less than a year, highlighting challenges in its turnaround efforts, while the company announced 1,400 job cuts primarily in its technology department to implement structural changes.

- Cautious Future Outlook: Management expects revenue to decline in low single digits over the next three quarters and anticipates a return to gross margin expansion by Q2 2027, leading Wall Street analysts to downgrade their ratings, reflecting a pessimistic view on Nike's recovery.

See More

Amazon's Next Big Move in Cloud Computing

- Significant Revenue Growth: Amazon reported $181 billion in revenue for the recent quarter, a 17% increase year-over-year, with net income reaching $30 billion, demonstrating strong performance in both e-commerce and cloud computing, thereby solidifying its market leadership.

- Cloud Business Flourishing: Amazon Web Services (AWS) has benefited from the rapid growth of artificial intelligence, achieving an annual revenue run rate of $150 billion, indicating its robust capabilities in supporting AI projects and suggesting continued growth for the company.

- Potential in Proprietary Chip Business: The demand for Amazon's Graviton and Trainium chips has skyrocketed, generating an annual revenue of $20 billion, with projections suggesting it could reach $50 billion if sold to third parties, highlighting its competitive edge in cost-effectiveness.

- Future Strategic Plans: Amazon aims to establish a standalone chip business to meet market demand, and although current production capacity is limited, this strategy could significantly enhance the company's growth potential in the coming years, akin to its successes in e-commerce and cloud computing.

See More

Cloud Giants' Earnings Reveal AI Investment Trends

- Accelerated AI Investment: Alphabet, Microsoft, and Amazon are projected to spend $190 billion and $200 billion on capital expenditures in 2026, primarily focused on AI technologies, indicating strong confidence in future market growth and potentially driving rapid advancements in related technologies.

- Nvidia's Market Position: Although Nvidia's earnings report is not yet due, the ongoing investments from major clients like Amazon and Alphabet suggest that demand for Nvidia's AI chips will remain robust, allowing the company to continue benefiting from the spending of cloud giants.

- Amazon's Chip Demand: Amazon's Trainium chips are experiencing incredible demand, and despite the growth of its in-house chip business, CEO Andy Jassy stated that the company will continue to order substantial quantities of AI chips from Nvidia, ensuring stability in Nvidia's market share and revenue.

- Competition and Innovation: While competition in the AI sector is intensifying, Nvidia's high switching costs due to its CUDA platform and the upcoming Vera Rubin platform will further solidify its market leadership, with expectations of sustained revenue and earnings growth over the next decade.

See More

Comparing Micron and SanDisk: Which Stock to Buy in the AI Boom?

- Market Share and Product Diversity: Micron boasts a market cap exceeding $500 billion with $23.86 billion in revenue for Q2 FY 2026, while SanDisk surpassed $100 billion in market cap earlier this year, reporting $5.95 billion in Q3 FY 2026 revenue, highlighting Micron's advantage in market share and product mix, which positions it better to handle future demand fluctuations.

- SanDisk's Rapid Growth: SanDisk achieved a remarkable 97% sequential revenue growth and 251% year-over-year growth in Q3 FY 2026, with a midpoint revenue outlook of $8 billion for Q4, indicating strong demand in the NAND market, although potential demand slowdowns could pose risks in the future.

- Valuation Differences: SanDisk's forward P/E ratio stands at 21, attractive within the tech sector but still higher than Micron's 9, suggesting Micron is relatively undervalued, while SanDisk's rapid growth may lead to a more favorable valuation in the future.

- Future Growth Potential: While Micron currently holds a valuation advantage, SanDisk's higher growth rates could yield greater stock returns, especially as its high-growth segments increasingly dominate total revenue, making it essential for investors to monitor the long-term performance of both companies.

See More

Intel's Huge Opportunity in Data Center CPU Market

- Stock Price Surge: Intel's stock has surged over 350% in the past year and more than 150% year-to-date, reflecting market optimism about its growth potential, yet its high valuation may limit further upside.

- Government Investment Support: The U.S. government invested $8.9 billion in Intel last year, acquiring nearly a 10% stake, which not only bolstered the company's financial position but also provided funding for future technological advancements.

- Increasing Competition: With companies like Arm Holdings and Nvidia entering the data center CPU market, Intel faces intensifying competition; despite its advantages in high-performance CPU demand, it continues to lose market share.

- Profitability Challenges: Intel's foundry business reported an operating loss of $2.4 billion last quarter, and while revenue increased, the path to profitability remains slow, necessitating cautious evaluation from investors regarding its future performance.

See More

SpaceX IPO Valuation Could Reach $2 Trillion

- IPO Expectations Soar: SpaceX is anticipated to announce its IPO in June, with analysts estimating a valuation target between $1.5 trillion and $1.75 trillion, and rumors suggest it could even reach $2 trillion, making it the largest IPO in history.

- Significant Market Potential: SpaceX's Starlink project controls around 70% of global satellites, expected to generate substantial revenue, and despite regulatory risks, its market outlook continues to attract investor interest.

- Lack of Financial Transparency: Although SpaceX is preparing for its IPO, it has yet to disclose financial statements, with PitchBook analysis suggesting a reasonable valuation between $1.1 trillion and $1.7 trillion, posing challenges for investors in assessing the company's value.

- Future Growth Potential: SpaceX is expected to publicly file an investment prospectus in May, which will allow investors to better evaluate its financials and determine whether the $2 trillion valuation is reasonable and if a 10x return on investment is feasible.

See More

Nike Shares Drop 16% in April Amid Earnings Disappointment

- Earnings Disappointment: Nike reported third-quarter revenue of $11.3 billion, slightly above the $11.23 billion estimate, but a 3% decline on a currency-neutral basis indicates weak sales growth, undermining market confidence in its future performance.

- Stock Price Plunge: The stock fell sharply at the beginning of April due to disappointing earnings, finishing the month down 16%, and is now 75% below its all-time high, reflecting a collapse in business performance over the past five years.

- Leadership Changes: Nike's innovation chief, Tony Bignell, left the company after less than a year, highlighting challenges in its turnaround efforts, while the company announced 1,400 job cuts primarily in its technology department to implement structural changes.

- Cautious Future Outlook: Management expects revenue to decline in low single digits over the next three quarters and anticipates a return to gross margin expansion by Q2 2027, leading Wall Street analysts to downgrade their ratings, reflecting a pessimistic view on Nike's recovery.

See More

Amazon's Next Big Move in Cloud Computing

- Significant Revenue Growth: Amazon reported $181 billion in revenue for the recent quarter, a 17% increase year-over-year, with net income reaching $30 billion, demonstrating strong performance in both e-commerce and cloud computing, thereby solidifying its market leadership.

- Cloud Business Flourishing: Amazon Web Services (AWS) has benefited from the rapid growth of artificial intelligence, achieving an annual revenue run rate of $150 billion, indicating its robust capabilities in supporting AI projects and suggesting continued growth for the company.

- Potential in Proprietary Chip Business: The demand for Amazon's Graviton and Trainium chips has skyrocketed, generating an annual revenue of $20 billion, with projections suggesting it could reach $50 billion if sold to third parties, highlighting its competitive edge in cost-effectiveness.

- Future Strategic Plans: Amazon aims to establish a standalone chip business to meet market demand, and although current production capacity is limited, this strategy could significantly enhance the company's growth potential in the coming years, akin to its successes in e-commerce and cloud computing.

See More

Cloud Giants' Earnings Reveal AI Investment Trends

- Accelerated AI Investment: Alphabet, Microsoft, and Amazon are projected to spend $190 billion and $200 billion on capital expenditures in 2026, primarily focused on AI technologies, indicating strong confidence in future market growth and potentially driving rapid advancements in related technologies.

- Nvidia's Market Position: Although Nvidia's earnings report is not yet due, the ongoing investments from major clients like Amazon and Alphabet suggest that demand for Nvidia's AI chips will remain robust, allowing the company to continue benefiting from the spending of cloud giants.

- Amazon's Chip Demand: Amazon's Trainium chips are experiencing incredible demand, and despite the growth of its in-house chip business, CEO Andy Jassy stated that the company will continue to order substantial quantities of AI chips from Nvidia, ensuring stability in Nvidia's market share and revenue.

- Competition and Innovation: While competition in the AI sector is intensifying, Nvidia's high switching costs due to its CUDA platform and the upcoming Vera Rubin platform will further solidify its market leadership, with expectations of sustained revenue and earnings growth over the next decade.

See More

Comparing Micron and SanDisk: Which Stock to Buy in the AI Boom?

- Market Share and Product Diversity: Micron boasts a market cap exceeding $500 billion with $23.86 billion in revenue for Q2 FY 2026, while SanDisk surpassed $100 billion in market cap earlier this year, reporting $5.95 billion in Q3 FY 2026 revenue, highlighting Micron's advantage in market share and product mix, which positions it better to handle future demand fluctuations.

- SanDisk's Rapid Growth: SanDisk achieved a remarkable 97% sequential revenue growth and 251% year-over-year growth in Q3 FY 2026, with a midpoint revenue outlook of $8 billion for Q4, indicating strong demand in the NAND market, although potential demand slowdowns could pose risks in the future.

- Valuation Differences: SanDisk's forward P/E ratio stands at 21, attractive within the tech sector but still higher than Micron's 9, suggesting Micron is relatively undervalued, while SanDisk's rapid growth may lead to a more favorable valuation in the future.

- Future Growth Potential: While Micron currently holds a valuation advantage, SanDisk's higher growth rates could yield greater stock returns, especially as its high-growth segments increasingly dominate total revenue, making it essential for investors to monitor the long-term performance of both companies.

See More