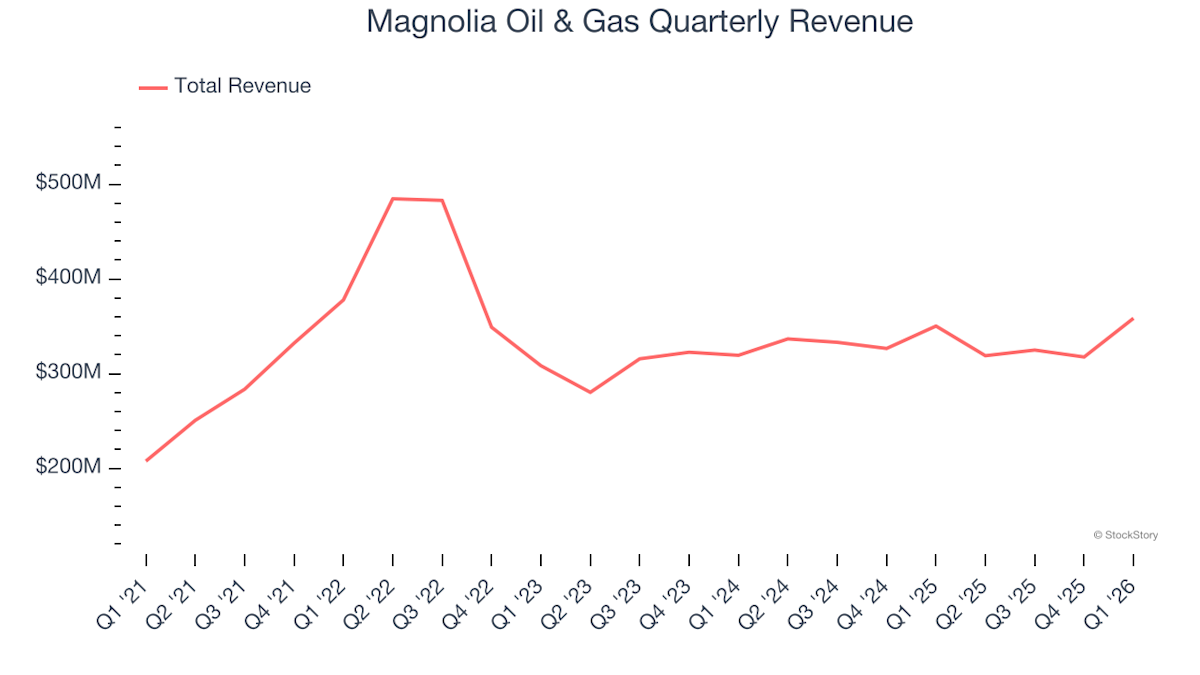

Magnolia Reports Q1 Revenue of $358.5M, Exceeds Expectations

Reports Q1 revenue $358.5M, consensus $354.4M. "Magnolia's first quarter financial and operating metrics delivered a strong start to 2026," said Chairman, President and CEO Chris Stavros. "Our consistent and disciplined business model, characterized by a low reinvestment rate, high operating margins and moderate production growth delivered over $145 million of free cash flow during the quarter. Our operations rebounded nicely after being affected by the freezing weather in January showing total year-over-year production growth of 6 percent and oil production growth of 4 percent during the quarter. Magnolia returned $83 million of this free cash flow back to shareholders through our dividend and share repurchase program in addition to closing several bolt-on oil and gas property acquisitions in areas where we operate. These numerous bolt-on purchases comprised approximately 6,200 net acres, encompassing acreage in both the Karnes area and in Giddings for what turned out to be a flurry of acquisition activity in the quarter. These assets were acquired for a total of $155 million and included approximately 500 boe per day of low decline production with significant undeveloped upside opportunities located in highly productive areas. In the Karnes area, the acquired acreage creates a large, contiguous block of approximately 10,000 gross acres across Karnes and Gonzales counties, increasing the working interest to 93 percent in existing Magnolia and acquired tracts and in primarily undeveloped acreage. In Giddings, we were able to increase our working interest in approximately 45,000 gross acres, along with purchasing some additional contiguous acreage, and continuing with our strategy of buying more of what we already own."

Trade with 70% Backtested Accuracy

Analyst Views on MGY

About MGY

About the author

Magnolia Oil & Gas Q1 2026 Earnings Call Insights

- Production Growth: In Q1 2026, Magnolia Oil & Gas reported a 6% year-over-year increase in total production volumes to 102,600 barrels of oil equivalent per day, with oil production rising by 4% to an average of 40,700 barrels per day, indicating the company's stable growth potential in the oil and gas market.

- Financial Performance: The company achieved a net income of approximately $101 million, translating to $0.54 per diluted share, with adjusted EBITDAX at $253 million, reflecting strong profitability and cash flow that are expected to drive future investments and shareholder returns.

- Acquisition Activity: During the first quarter, Magnolia completed several small bolt-on oil and gas property acquisitions totaling $155 million, adding roughly 6,200 net acres and approximately 500 BOE per day of low-decline production, further solidifying its market position in the Karnes and Giddings areas.

- Future Outlook: Total production for Q2 is estimated to be around 105,000 barrels per day, with the full-year capital expenditure budget reiterated at $440 million to $480 million, demonstrating the company's confidence in sustained growth while maintaining a disciplined approach to capital spending.

Magnolia Oil & Gas Q1 Earnings Miss Expectations

- Earnings Performance: Magnolia Oil & Gas reported a Q1 GAAP EPS of $0.54, missing expectations by $0.23, indicating pressure on profitability that may affect investor confidence.

- Revenue Shortfall: The revenue for Q1 was $358.51 million, a 2.3% year-over-year increase, yet it fell short of expectations by $71.97 million, reflecting weak market demand that could lead to future performance declines.

- Capital Expenditure Overview: The D&C capital spending for Q1 was $128.7 million, representing approximately 51% of adjusted EBITDAX, indicating a cautious approach to expansion that may impact long-term growth potential.

- Production Growth Slowdown: Total production volumes grew by 6% year-over-year to 102.6 Mboe/d in Q1, but the growth rate is slowing, with an estimated production of 105 Mboe/d for Q2, suggesting insufficient growth momentum.

Magnolia Oil & Gas Q1 Results Exceed Expectations

- Revenue Growth: Magnolia Oil & Gas reported Q1 revenue of $358.5 million, reflecting a 2.3% year-on-year increase that surpassed analyst expectations of $351.7 million, indicating the company's resilience and appeal in a competitive energy market.

- Earnings Per Share Beat: The GAAP EPS of $0.54 exceeded analysts' expectations of $0.51 by 5.3%, showcasing effective management in cost control and profitability.

- Free Cash Flow Performance: The company generated $197.6 million in free cash flow with a margin of 55.1%, up 28.5 percentage points from the same quarter last year, highlighting its strong capacity for capital return and reinvestment.

- Profitability Stability: Although the EBITDA margin decreased by 7.9 percentage points to 70.7% year-on-year, it remains above industry averages, demonstrating Magnolia's ability to maintain profitability amid market fluctuations.

Magnolia Oil & Gas Set to Announce Q1 Earnings on May 7

- Earnings Announcement: Magnolia Oil & Gas is set to release its Q1 2023 earnings report on May 7 before market open, with consensus estimates predicting an EPS of $0.52 and revenue of $354.39 million, reflecting a 1.3% year-over-year growth, which will provide critical insights into the company's financial health.

- Performance Beat Record: Over the past year, MGY has exceeded EPS estimates 50% of the time and revenue estimates 75% of the time, demonstrating the company's resilience and profitability amid market fluctuations, thereby boosting investor confidence.

- Revision Trends: In the last three months, EPS estimates have seen 13 upward revisions and 1 downward revision, while revenue estimates have experienced 9 upward revisions with no downward adjustments, indicating analysts' optimistic outlook on the company's future performance, which could drive stock price increases.

- Future Growth Targets: Magnolia aims for a 5% production growth in 2026 while maintaining disciplined capital spending, a strategy that will help the company sustain its growth in a competitive market environment.

Magnolia Oil & Gas Declares Quarterly Dividend of $0.165

- Quarterly Dividend Announcement: Magnolia Oil & Gas has declared a quarterly dividend of $0.165 per share, consistent with previous distributions, indicating the company's stable cash flow and profitability, which is likely to attract more investor interest.

- Yield Analysis: The forward yield of 2.18% reflects the company's appeal in the current market environment, potentially boosting shareholder confidence and stabilizing the stock price.

- Financial Performance Beats Expectations: Magnolia reported a GAAP EPS of $0.37 for Q4 2025, exceeding expectations by $0.01, with revenue of $317.62 million surpassing forecasts by $3.88 million, demonstrating strong performance in both revenue and profitability.

- Production Growth Target: The company aims for a 5% production growth in 2026 while maintaining disciplined capital spending, a strategy that will help sustain its competitive edge in future market conditions.

Magnolia Oil & Gas Declares Quarterly Cash Dividend

- Quarterly Cash Dividend: Magnolia Oil & Gas has declared a cash dividend of $0.165 per share, payable on June 1, 2026, demonstrating the company's ongoing commitment to returning value to shareholders.

- Dividend Growth Trend: Since 2021, Magnolia has consistently increased its dividend per share, reflecting stable financial performance and a strong focus on shareholder value, which enhances investor confidence.

- Core Business Focus: Magnolia specializes in oil and gas exploration and production in South Texas, particularly in the Eagle Ford Shale and Austin Chalk formations, aiming for steady annual production growth through disciplined capital spending.

- Financial Health: The company strives to achieve high pre-tax margins and consistent free cash flow, allowing for strong cash returns to shareholders, thereby reinforcing its competitive position within the industry.

Magnolia Oil & Gas Q1 2026 Earnings Call Insights

- Production Growth: In Q1 2026, Magnolia Oil & Gas reported a 6% year-over-year increase in total production volumes to 102,600 barrels of oil equivalent per day, with oil production rising by 4% to an average of 40,700 barrels per day, indicating the company's stable growth potential in the oil and gas market.

- Financial Performance: The company achieved a net income of approximately $101 million, translating to $0.54 per diluted share, with adjusted EBITDAX at $253 million, reflecting strong profitability and cash flow that are expected to drive future investments and shareholder returns.

- Acquisition Activity: During the first quarter, Magnolia completed several small bolt-on oil and gas property acquisitions totaling $155 million, adding roughly 6,200 net acres and approximately 500 BOE per day of low-decline production, further solidifying its market position in the Karnes and Giddings areas.

- Future Outlook: Total production for Q2 is estimated to be around 105,000 barrels per day, with the full-year capital expenditure budget reiterated at $440 million to $480 million, demonstrating the company's confidence in sustained growth while maintaining a disciplined approach to capital spending.

Magnolia Oil & Gas Q1 Earnings Miss Expectations

- Earnings Performance: Magnolia Oil & Gas reported a Q1 GAAP EPS of $0.54, missing expectations by $0.23, indicating pressure on profitability that may affect investor confidence.

- Revenue Shortfall: The revenue for Q1 was $358.51 million, a 2.3% year-over-year increase, yet it fell short of expectations by $71.97 million, reflecting weak market demand that could lead to future performance declines.

- Capital Expenditure Overview: The D&C capital spending for Q1 was $128.7 million, representing approximately 51% of adjusted EBITDAX, indicating a cautious approach to expansion that may impact long-term growth potential.

- Production Growth Slowdown: Total production volumes grew by 6% year-over-year to 102.6 Mboe/d in Q1, but the growth rate is slowing, with an estimated production of 105 Mboe/d for Q2, suggesting insufficient growth momentum.

Magnolia Oil & Gas Q1 Results Exceed Expectations

- Revenue Growth: Magnolia Oil & Gas reported Q1 revenue of $358.5 million, reflecting a 2.3% year-on-year increase that surpassed analyst expectations of $351.7 million, indicating the company's resilience and appeal in a competitive energy market.

- Earnings Per Share Beat: The GAAP EPS of $0.54 exceeded analysts' expectations of $0.51 by 5.3%, showcasing effective management in cost control and profitability.

- Free Cash Flow Performance: The company generated $197.6 million in free cash flow with a margin of 55.1%, up 28.5 percentage points from the same quarter last year, highlighting its strong capacity for capital return and reinvestment.

- Profitability Stability: Although the EBITDA margin decreased by 7.9 percentage points to 70.7% year-on-year, it remains above industry averages, demonstrating Magnolia's ability to maintain profitability amid market fluctuations.

Magnolia Oil & Gas Set to Announce Q1 Earnings on May 7

- Earnings Announcement: Magnolia Oil & Gas is set to release its Q1 2023 earnings report on May 7 before market open, with consensus estimates predicting an EPS of $0.52 and revenue of $354.39 million, reflecting a 1.3% year-over-year growth, which will provide critical insights into the company's financial health.

- Performance Beat Record: Over the past year, MGY has exceeded EPS estimates 50% of the time and revenue estimates 75% of the time, demonstrating the company's resilience and profitability amid market fluctuations, thereby boosting investor confidence.

- Revision Trends: In the last three months, EPS estimates have seen 13 upward revisions and 1 downward revision, while revenue estimates have experienced 9 upward revisions with no downward adjustments, indicating analysts' optimistic outlook on the company's future performance, which could drive stock price increases.

- Future Growth Targets: Magnolia aims for a 5% production growth in 2026 while maintaining disciplined capital spending, a strategy that will help the company sustain its growth in a competitive market environment.

Magnolia Oil & Gas Declares Quarterly Dividend of $0.165

- Quarterly Dividend Announcement: Magnolia Oil & Gas has declared a quarterly dividend of $0.165 per share, consistent with previous distributions, indicating the company's stable cash flow and profitability, which is likely to attract more investor interest.

- Yield Analysis: The forward yield of 2.18% reflects the company's appeal in the current market environment, potentially boosting shareholder confidence and stabilizing the stock price.

- Financial Performance Beats Expectations: Magnolia reported a GAAP EPS of $0.37 for Q4 2025, exceeding expectations by $0.01, with revenue of $317.62 million surpassing forecasts by $3.88 million, demonstrating strong performance in both revenue and profitability.

- Production Growth Target: The company aims for a 5% production growth in 2026 while maintaining disciplined capital spending, a strategy that will help sustain its competitive edge in future market conditions.

Magnolia Oil & Gas Declares Quarterly Cash Dividend

- Quarterly Cash Dividend: Magnolia Oil & Gas has declared a cash dividend of $0.165 per share, payable on June 1, 2026, demonstrating the company's ongoing commitment to returning value to shareholders.

- Dividend Growth Trend: Since 2021, Magnolia has consistently increased its dividend per share, reflecting stable financial performance and a strong focus on shareholder value, which enhances investor confidence.

- Core Business Focus: Magnolia specializes in oil and gas exploration and production in South Texas, particularly in the Eagle Ford Shale and Austin Chalk formations, aiming for steady annual production growth through disciplined capital spending.

- Financial Health: The company strives to achieve high pre-tax margins and consistent free cash flow, allowing for strong cash returns to shareholders, thereby reinforcing its competitive position within the industry.