Lexicon Presents Sotagliflozin Clinical Data Analysis Results

Lexicon Pharmaceuticals announced that results of a post hoc analysis of clinical data evaluating the impact of kidney function on the long-term efficacy and safety of sotagliflozin on people with type 1 diabetes will be delivered as a short oral presentation tomorrow, March 12, during the 19th International Conference on Advanced Technologies & Treatments for Diabetes. The congress is being held March 11-14, 2026, in Barcelona, Spain. "Recognizing that a patient's kidney function can impact the efficacy of SGLT inhibitors, we conducted this post hoc analysis of clinical data from two identically-designed trials in patients with type 1 diabetes and were encouraged to find that treatment with sotagliflozin resulted in improvements in multiple efficacy measures after one year in both those with normal kidney function and those with mildly reduced kidney function," said Craig Granowitz, M.D., Ph.D., Lexicon's senior vice president and chief medical officer. "Not only was sotagliflozin shown to improve cardiometabolic parameters in this patient population, but it also reduced clinically important hypoglycemia events, which are a leading cause of acute mortality and morbidity and can be life-threatening." Lexicon remains on track to resubmit the New Drug Application for ZYNQUISTA glycemic control in patients with type 1 diabetes in 2026 based upon U.S. Food and Drug Administration feedback and additional clinical data received to date from the STENO1 study

Trade with 70% Backtested Accuracy

Analyst Views on LXRX

About LXRX

About the author

Novo Nordisk Advances Next-Gen Obesity Treatments with LX9851 Trial

- Clinical Trial Initiation: Novo Nordisk has announced the initiation of a Phase 1 study for LX9851, an oral non-incretin drug candidate from Lexicon Pharmaceuticals aimed at treating obesity and related metabolic disorders, marking a significant advancement in the company's obesity treatment efforts.

- Milestone Payment Triggered: The start of this trial triggers a second $10 million milestone payment to Lexicon under their licensing agreement signed in March 2025, granting Novo Nordisk exclusive global rights to develop and commercialize the drug, with Lexicon eligible for up to $1 billion in total milestone payments and royalties on future sales.

- Trial Scale and Timeline: The Phase 1 study will evaluate safety and dosing in 96 overweight or obese participants, expected to be completed by early 2027, demonstrating Novo Nordisk's commitment and strategic planning in advancing its drug pipeline.

- Market Reaction and Outlook: While NVO shares fell 1.5%, LXRX's stock rose about 1% in pre-market trading, reflecting market optimism regarding the new drug development and enhancing Novo Nordisk's competitive position in the obesity treatment market.

Lexicon Pharmaceuticals and Novo Nordisk Launch Phase 1 Study for Oral Obesity Drug Candidate LX9851

Announcement of Phase 1 Study: Lexicon Pharmaceuticals and Novartis have announced the initiation of a Phase 1 study for the oral obesity drug candidate, LX9851.

Focus on Obesity Treatment: The study aims to evaluate the safety and efficacy of LX9851 as a potential treatment for obesity, highlighting the ongoing efforts in developing innovative therapies in this area.

Lexicon Pharmaceuticals Q4 2025 Earnings Call Insights

- Core Program Progress: Lexicon Pharmaceuticals is advancing three late-stage programs in cardiometabolic disease and chronic pain, with significant progress in the development of sotagliflozin for hypertrophic cardiomyopathy, expected to submit an NDA in 2026, indicating a strategic focus on critical therapeutic areas.

- Financial Position Improvement: Total revenues for Q4 2025 were $5.5 million, with full-year revenues reaching $49.8 million, showing significant improvement from 2024, while net loss decreased from $33.8 million in 2024 to $15.5 million, reflecting successful cost control and operational efficiency.

- R&D Expense Optimization: R&D expenses for Q4 dropped to $11.3 million, halving compared to 2024, indicating Lexicon's more efficient resource allocation and continued focus on advancing core programs in the future.

- Future Outlook: Management expects operating expenses in 2026 to range between $100 million and $110 million, with R&D expenses projected at $63 million to $68 million, demonstrating confidence in future growth while emphasizing the smooth progress of the SONATA-HCM trial and plans for NDA resubmission for Zynquista.

Lexicon Pharmaceuticals Q4 Earnings Beat Expectations

- Earnings Highlights: Lexicon Pharmaceuticals reported a Q4 GAAP EPS of -$0.04, beating expectations by $0.03, indicating potential improvements in profitability despite ongoing challenges.

- Revenue Performance: The company generated $5.49 million in revenue, a 79.3% year-over-year decline, yet it exceeded expectations by $2.35 million, suggesting some resilience in market demand amid adversity.

- Liquidity Position: As of December 31, 2025, Lexicon's total cash, investments, and restricted cash amounted to $125.2 million, down from $238.0 million in the same period of 2024, highlighting pressures on the company's financial management.

- Market Reaction: Lexicon Pharmaceuticals showcased FDA feedback on Pilavapadin at the J.P. Morgan Healthcare Conference, and despite facing challenges, the market remains cautiously optimistic about its future prospects.

Lexicon Pharmaceuticals to Announce Q4 Earnings on March 5

- Earnings Announcement: Lexicon Pharmaceuticals is set to release its Q4 earnings on March 5 before market open, with a consensus EPS estimate of -$0.07, indicating ongoing challenges in profitability.

- Revenue Decline: The anticipated revenue of $3.14 million for Q4 represents an 88.2% year-over-year decline, highlighting significant pressures in market competition and product sales that could impact future liquidity.

- Positive FDA Feedback: Despite financial hurdles, Lexicon's Pilavapadin drug has received FDA feedback allowing it to proceed, providing potential growth opportunities for the company's product pipeline and possibly improving its market outlook.

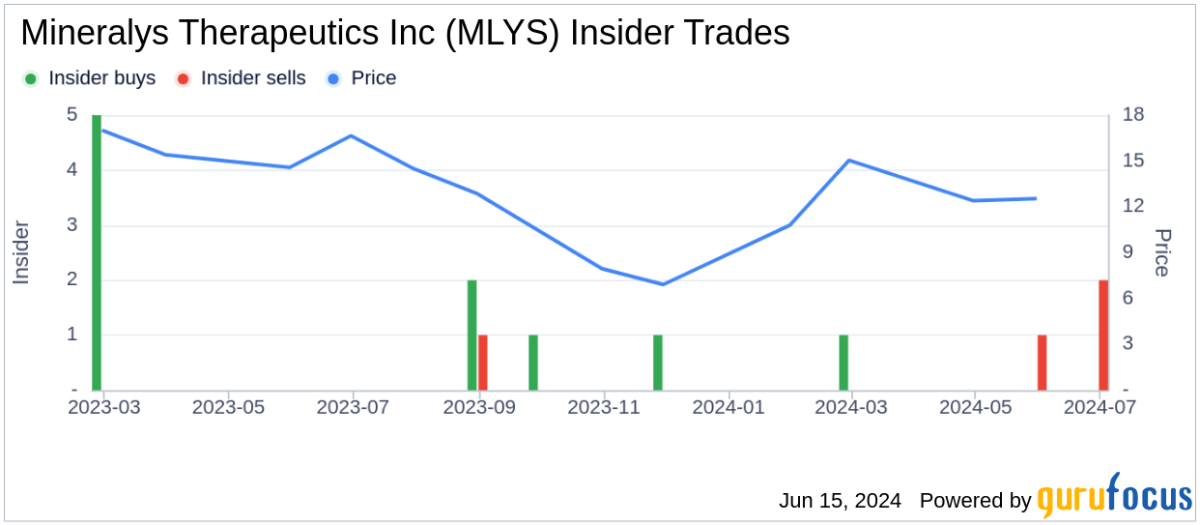

- Active Insider Trading: Lexicon's stock recently spiked following insider buying, reflecting management's confidence in the company's future, which may attract more investor interest in its stock performance.

Chronic Kidney Disease Market Growth Drivers

- Market Size Growth: According to analysis, the chronic kidney disease (CKD) market size was approximately $4.8 billion in 2024 and is expected to grow further by 2034, reflecting increased demand for new therapies and an expanding patient base.

- Rising Patient Numbers: In 2024, there were about 82 million prevalent cases of CKD across the 7 major markets (7MM), with projections indicating continued growth from 2025 to 2034, primarily driven by an aging population and the rising prevalence of diabetes and hypertension.

- Launch of New Therapies: The introduction of emerging therapies such as AstraZeneca's Zibotentan/Dapagliflozin and Boehringer Ingelheim's Vicadrostat + Empagliflozin is expected to significantly boost market growth and improve treatment outcomes for patients.

- Advancements in Biomarkers: Progress in biomarkers like KIM-1 and NGAL enables more precise early detection of CKD, thereby enhancing the potential for timely interventions and improving overall patient prognosis.

Novo Nordisk Advances Next-Gen Obesity Treatments with LX9851 Trial

- Clinical Trial Initiation: Novo Nordisk has announced the initiation of a Phase 1 study for LX9851, an oral non-incretin drug candidate from Lexicon Pharmaceuticals aimed at treating obesity and related metabolic disorders, marking a significant advancement in the company's obesity treatment efforts.

- Milestone Payment Triggered: The start of this trial triggers a second $10 million milestone payment to Lexicon under their licensing agreement signed in March 2025, granting Novo Nordisk exclusive global rights to develop and commercialize the drug, with Lexicon eligible for up to $1 billion in total milestone payments and royalties on future sales.

- Trial Scale and Timeline: The Phase 1 study will evaluate safety and dosing in 96 overweight or obese participants, expected to be completed by early 2027, demonstrating Novo Nordisk's commitment and strategic planning in advancing its drug pipeline.

- Market Reaction and Outlook: While NVO shares fell 1.5%, LXRX's stock rose about 1% in pre-market trading, reflecting market optimism regarding the new drug development and enhancing Novo Nordisk's competitive position in the obesity treatment market.

Lexicon Pharmaceuticals and Novo Nordisk Launch Phase 1 Study for Oral Obesity Drug Candidate LX9851

Announcement of Phase 1 Study: Lexicon Pharmaceuticals and Novartis have announced the initiation of a Phase 1 study for the oral obesity drug candidate, LX9851.

Focus on Obesity Treatment: The study aims to evaluate the safety and efficacy of LX9851 as a potential treatment for obesity, highlighting the ongoing efforts in developing innovative therapies in this area.

Lexicon Pharmaceuticals Q4 2025 Earnings Call Insights

- Core Program Progress: Lexicon Pharmaceuticals is advancing three late-stage programs in cardiometabolic disease and chronic pain, with significant progress in the development of sotagliflozin for hypertrophic cardiomyopathy, expected to submit an NDA in 2026, indicating a strategic focus on critical therapeutic areas.

- Financial Position Improvement: Total revenues for Q4 2025 were $5.5 million, with full-year revenues reaching $49.8 million, showing significant improvement from 2024, while net loss decreased from $33.8 million in 2024 to $15.5 million, reflecting successful cost control and operational efficiency.

- R&D Expense Optimization: R&D expenses for Q4 dropped to $11.3 million, halving compared to 2024, indicating Lexicon's more efficient resource allocation and continued focus on advancing core programs in the future.

- Future Outlook: Management expects operating expenses in 2026 to range between $100 million and $110 million, with R&D expenses projected at $63 million to $68 million, demonstrating confidence in future growth while emphasizing the smooth progress of the SONATA-HCM trial and plans for NDA resubmission for Zynquista.

Lexicon Pharmaceuticals Q4 Earnings Beat Expectations

- Earnings Highlights: Lexicon Pharmaceuticals reported a Q4 GAAP EPS of -$0.04, beating expectations by $0.03, indicating potential improvements in profitability despite ongoing challenges.

- Revenue Performance: The company generated $5.49 million in revenue, a 79.3% year-over-year decline, yet it exceeded expectations by $2.35 million, suggesting some resilience in market demand amid adversity.

- Liquidity Position: As of December 31, 2025, Lexicon's total cash, investments, and restricted cash amounted to $125.2 million, down from $238.0 million in the same period of 2024, highlighting pressures on the company's financial management.

- Market Reaction: Lexicon Pharmaceuticals showcased FDA feedback on Pilavapadin at the J.P. Morgan Healthcare Conference, and despite facing challenges, the market remains cautiously optimistic about its future prospects.

Lexicon Pharmaceuticals to Announce Q4 Earnings on March 5

- Earnings Announcement: Lexicon Pharmaceuticals is set to release its Q4 earnings on March 5 before market open, with a consensus EPS estimate of -$0.07, indicating ongoing challenges in profitability.

- Revenue Decline: The anticipated revenue of $3.14 million for Q4 represents an 88.2% year-over-year decline, highlighting significant pressures in market competition and product sales that could impact future liquidity.

- Positive FDA Feedback: Despite financial hurdles, Lexicon's Pilavapadin drug has received FDA feedback allowing it to proceed, providing potential growth opportunities for the company's product pipeline and possibly improving its market outlook.

- Active Insider Trading: Lexicon's stock recently spiked following insider buying, reflecting management's confidence in the company's future, which may attract more investor interest in its stock performance.

Chronic Kidney Disease Market Growth Drivers

- Market Size Growth: According to analysis, the chronic kidney disease (CKD) market size was approximately $4.8 billion in 2024 and is expected to grow further by 2034, reflecting increased demand for new therapies and an expanding patient base.

- Rising Patient Numbers: In 2024, there were about 82 million prevalent cases of CKD across the 7 major markets (7MM), with projections indicating continued growth from 2025 to 2034, primarily driven by an aging population and the rising prevalence of diabetes and hypertension.

- Launch of New Therapies: The introduction of emerging therapies such as AstraZeneca's Zibotentan/Dapagliflozin and Boehringer Ingelheim's Vicadrostat + Empagliflozin is expected to significantly boost market growth and improve treatment outcomes for patients.

- Advancements in Biomarkers: Progress in biomarkers like KIM-1 and NGAL enables more precise early detection of CKD, thereby enhancing the potential for timely interventions and improving overall patient prognosis.