Google Cloud and McKinsey Launch AI Transformation Group

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 6 days ago

0mins

Should l Buy GOOG?

Source: seekingalpha

- Strategic Partnership Launch: Google Cloud and McKinsey have launched the McKinsey Google Transformation Group, aiming to help enterprises achieve sustainable business value in the AI era by combining McKinsey's industry expertise with Google Cloud's AI technology stack.

- Value Delivery Model: The new group will provide an end-to-end experience through joint teams, co-funded value assessments, and outcome-based models, reducing upfront investment while ensuring measurable results, thereby enhancing clients' AI application capabilities.

- Integration of Industry Insights: Google Cloud and McKinsey teams will collaborate to develop AI-powered solutions built on Google Cloud, leveraging McKinsey's industry insights to create reusable proprietary assets that accelerate time to value and support scaled adoption.

- Investment and Expansion: McKinsey is investing to scale its expertise in Google Cloud infrastructure and AI delivery capabilities, further driving the reimagining of value chains and supporting the future development of global industries.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GOOG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GOOG

Wall Street analysts forecast GOOG stock price to fall

15 Analyst Rating

14 Buy

1 Hold

0 Sell

Strong Buy

Current: 348.520

Low

255.00

Averages

336.08

High

400.00

Current: 348.520

Low

255.00

Averages

336.08

High

400.00

About GOOG

Alphabet Inc. is a holding company. The Company's segments include Google Services, Google Cloud, and Other Bets. The Google Services segment includes products and services such as ads, Android, Chrome, devices, Google Maps, Google Play, Search, and YouTube. The Google Cloud segment includes infrastructure and platform services, collaboration tools, and other services for enterprise customers. Its Other Bets segment is engaged in the sale of healthcare-related services and Internet services. Its Google Cloud provides enterprise-ready cloud services, including Google Cloud Platform and Google Workspace. Google Cloud Platform provides access to solutions such as artificial intelligence (AI) offerings, including its AI infrastructure, Vertex AI platform, and Gemini for Google Cloud; cybersecurity, and data and analytics. Google Workspace includes cloud-based communication and collaboration tools for enterprises, such as Calendar, Gmail, Docs, Drive, and Meet.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Alphabet Set to Report Q1 2026 Earnings Amid AI Investment Focus

- Cloud Business Surge: Alphabet's Google Cloud revenue soared from $43.2 billion in 2024 to $58.7 billion in 2025, marking a 48% year-over-year growth, driven by strong demand for enterprise AI products, although its operating income only accounts for 11% of total operating income.

- Capital Expenditure Surge: Alphabet anticipates capital expenditures between $175 billion and $185 billion in 2026, nearly doubling from $91.4 billion in 2025, a significant investment aimed at maintaining its competitive edge in AI, but it also raises the stock's risk profile.

- Increased Depreciation Pressure: Depreciation expenses rose 38% to $21.1 billion in 2025, with expectations for further acceleration in 2026, making the upcoming earnings per share data critical; if growth does not offset rising costs, it could negatively impact the stock price.

- Long-Term Investment Appeal: Despite short-term risks, Alphabet's dominance in search, YouTube, and its rapidly growing cloud business make its stock attractive for long-term investors, trading at about 32 times earnings, reflecting market confidence in its future growth potential.

See More

Investing in Alphabet's AI Potential

- Strong Financial Position: Alphabet generated $132.2 billion in net income last year despite AI investments, showcasing its robust financial foundation that minimizes the likelihood of dramatic price swings, thus providing a stable return outlook for long-term investors.

- Growth in Advertising and Cloud: Alphabet's ad network and cloud platform achieved a 15% sales growth in 2025, with Google Cloud's revenue growing 48% year-over-year in Q4, yielding $5.3 billion in operating income, further solidifying its market position in the AI sector.

- Diverse AI Investments: Alphabet's AI model, Gemini, boasts over 750 million monthly active users, enhancing user experience through integration with Google Search, while Waymo's self-driving vehicles operate in multiple cities, increasing its competitive edge in the market.

- Long-Term Strategic Vision: With ample cash and resources, Alphabet can afford to make long-term investments in AI, similar to the decade-long wait for Google Cloud to become profitable, indicating its patience and strategic foresight in emerging technologies.

See More

Meta Shifts to Commercial AI Strategy Amid Earnings Call

- Commercial Shift: During the latest earnings call, CEO Mark Zuckerberg announced Meta's pivot from open-source to a commercial AI strategy with the launch of its first closed-source model, Muse Spark, aimed at competing with paid services from Google and OpenAI, with Q1 revenue expected to rise 31% to $55.6 billion, highlighting the company's commitment to the AI market.

- Talent Investment: Zuckerberg's $14.3 billion investment in Scale AI and the hiring of former GitHub CEO Nat Friedman signal an aggressive rebuild of Meta's internal AI team to bridge the gap with market leaders and enhance technological capabilities.

- Advertising Revenue Potential: While vision models currently lag behind text in hype, analysts believe Meta's superior image generation tools will unlock advertising budgets by automating high-performing creative, driving short-term revenue growth and further solidifying its market position.

- Capital Expenditure Pressure: With projected capital expenditures hitting $135 billion, investors are concerned about the company's massive infrastructure spending and recent 10% workforce reduction, demanding a clear roadmap for profitability to support its long-term growth strategy.

See More

Alphabet Faces Risks and Opportunities in AI Investment

- Surge in Capital Expenditure: Alphabet plans to increase its capital expenditures to between $175 billion and $185 billion by 2026, nearly doubling from last year's $91 billion, indicating a strong commitment to AI investment, although this may pressure future cash flows.

- Expansion of Technical Infrastructure: CFO Anat Ashkenazi stated that approximately 60% of the investment will be allocated to servers and 40% to data centers and networking equipment, suggesting that Alphabet's ongoing expansion in technical infrastructure will enhance its competitive position in the market.

- Investment Return Risks: Despite optimistic views on capital spending, analysts expect free cash flow to decline by 70% year-over-year in 2026, which could prevent shareholders from benefiting from more aggressive stock buybacks or higher dividends.

- Challenges of AI Innovation: With the rapid evolution of AI technology, Alphabet faces the risk of shortened asset lifespans; if hardware and software become obsolete within three years, it will necessitate continuous replacements and upgrades, adding unpredictability to future investments.

See More

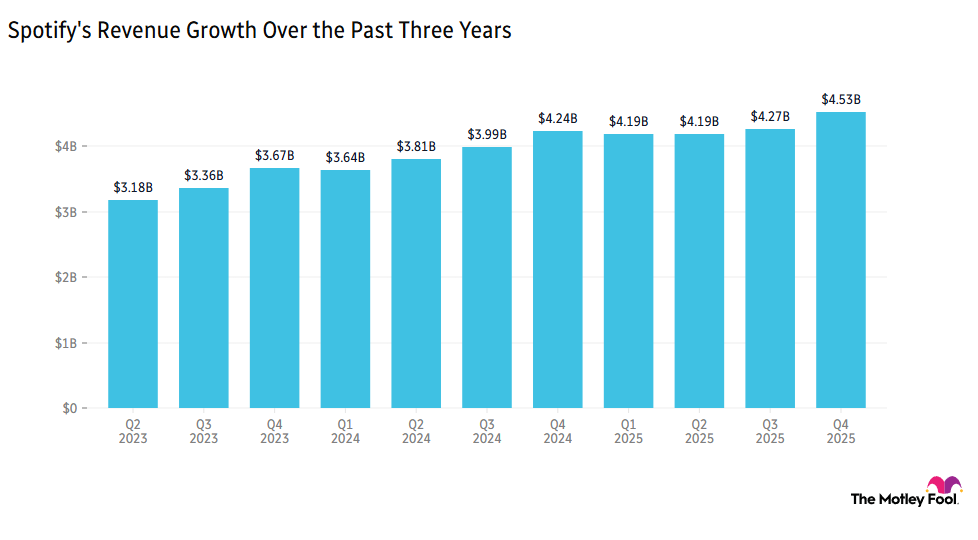

Spotify's Profit Forecast Falls Short of Expectations

- Ad Revenue Decline: Spotify's ad-supported revenue fell by 5% year-over-year, causing the stock to drop over 9% ahead of market open, reflecting concerns about growth, particularly in major markets like the U.S.

- Disappointing Profit Guidance: While overall revenue grew by 10%, the outlook for operating income and premium subscriber growth for the upcoming quarter disappointed investors, indicating challenges in major markets.

- User Growth Drivers: All key performance indicators met or exceeded expectations, with advanced AI-powered personalization tools and enhancements to the mobile free tier driving accelerated user growth, despite a weak overall growth outlook.

- Strong Market Performance: Since January 2022, Spotify's stock has outperformed the S&P 500 by 78%, demonstrating robust performance under specific market conditions, even as current profit forecasts raise investor concerns.

See More

Amazon vs. Microsoft: AI Investment Performance Comparison

- Amazon's AI Investment Returns: Amazon is set to invest $200 billion in AI capital expenditures this year, with CEO Andy Jassy stating that AI investments are already yielding returns, as AWS AI services achieved a $15 billion annual revenue run rate in Q1 2026, indicating strong profitability potential in the AI sector.

- Microsoft's Challenges: Microsoft is lagging in the AI race; despite generating $7.58 billion from its partnership with OpenAI, its Copilot AI tools are struggling, with only 3% of commercial customers purchasing licenses, highlighting difficulties in product adoption.

- Market Performance Divergence: Over the past five years, Amazon's stock has risen 52% while Microsoft's has increased 68%, but year-to-date, Amazon is up 14% while Microsoft has declined by 12%, reflecting Amazon's strong momentum in the AI space.

- Investor Confidence: Although Microsoft's P/E ratio stands at 26.6, lower than Amazon's 36.8, recent trends and news suggest that investors are more optimistic about Amazon's AI growth story, anticipating that Amazon will outperform Microsoft in the upcoming earnings reports.

See More

Alphabet Set to Report Q1 2026 Earnings Amid AI Investment Focus

- Cloud Business Surge: Alphabet's Google Cloud revenue soared from $43.2 billion in 2024 to $58.7 billion in 2025, marking a 48% year-over-year growth, driven by strong demand for enterprise AI products, although its operating income only accounts for 11% of total operating income.

- Capital Expenditure Surge: Alphabet anticipates capital expenditures between $175 billion and $185 billion in 2026, nearly doubling from $91.4 billion in 2025, a significant investment aimed at maintaining its competitive edge in AI, but it also raises the stock's risk profile.

- Increased Depreciation Pressure: Depreciation expenses rose 38% to $21.1 billion in 2025, with expectations for further acceleration in 2026, making the upcoming earnings per share data critical; if growth does not offset rising costs, it could negatively impact the stock price.

- Long-Term Investment Appeal: Despite short-term risks, Alphabet's dominance in search, YouTube, and its rapidly growing cloud business make its stock attractive for long-term investors, trading at about 32 times earnings, reflecting market confidence in its future growth potential.

See More

Investing in Alphabet's AI Potential

- Strong Financial Position: Alphabet generated $132.2 billion in net income last year despite AI investments, showcasing its robust financial foundation that minimizes the likelihood of dramatic price swings, thus providing a stable return outlook for long-term investors.

- Growth in Advertising and Cloud: Alphabet's ad network and cloud platform achieved a 15% sales growth in 2025, with Google Cloud's revenue growing 48% year-over-year in Q4, yielding $5.3 billion in operating income, further solidifying its market position in the AI sector.

- Diverse AI Investments: Alphabet's AI model, Gemini, boasts over 750 million monthly active users, enhancing user experience through integration with Google Search, while Waymo's self-driving vehicles operate in multiple cities, increasing its competitive edge in the market.

- Long-Term Strategic Vision: With ample cash and resources, Alphabet can afford to make long-term investments in AI, similar to the decade-long wait for Google Cloud to become profitable, indicating its patience and strategic foresight in emerging technologies.

See More

Meta Shifts to Commercial AI Strategy Amid Earnings Call

- Commercial Shift: During the latest earnings call, CEO Mark Zuckerberg announced Meta's pivot from open-source to a commercial AI strategy with the launch of its first closed-source model, Muse Spark, aimed at competing with paid services from Google and OpenAI, with Q1 revenue expected to rise 31% to $55.6 billion, highlighting the company's commitment to the AI market.

- Talent Investment: Zuckerberg's $14.3 billion investment in Scale AI and the hiring of former GitHub CEO Nat Friedman signal an aggressive rebuild of Meta's internal AI team to bridge the gap with market leaders and enhance technological capabilities.

- Advertising Revenue Potential: While vision models currently lag behind text in hype, analysts believe Meta's superior image generation tools will unlock advertising budgets by automating high-performing creative, driving short-term revenue growth and further solidifying its market position.

- Capital Expenditure Pressure: With projected capital expenditures hitting $135 billion, investors are concerned about the company's massive infrastructure spending and recent 10% workforce reduction, demanding a clear roadmap for profitability to support its long-term growth strategy.

See More

Alphabet Faces Risks and Opportunities in AI Investment

- Surge in Capital Expenditure: Alphabet plans to increase its capital expenditures to between $175 billion and $185 billion by 2026, nearly doubling from last year's $91 billion, indicating a strong commitment to AI investment, although this may pressure future cash flows.

- Expansion of Technical Infrastructure: CFO Anat Ashkenazi stated that approximately 60% of the investment will be allocated to servers and 40% to data centers and networking equipment, suggesting that Alphabet's ongoing expansion in technical infrastructure will enhance its competitive position in the market.

- Investment Return Risks: Despite optimistic views on capital spending, analysts expect free cash flow to decline by 70% year-over-year in 2026, which could prevent shareholders from benefiting from more aggressive stock buybacks or higher dividends.

- Challenges of AI Innovation: With the rapid evolution of AI technology, Alphabet faces the risk of shortened asset lifespans; if hardware and software become obsolete within three years, it will necessitate continuous replacements and upgrades, adding unpredictability to future investments.

See More

Spotify's Profit Forecast Falls Short of Expectations

- Ad Revenue Decline: Spotify's ad-supported revenue fell by 5% year-over-year, causing the stock to drop over 9% ahead of market open, reflecting concerns about growth, particularly in major markets like the U.S.

- Disappointing Profit Guidance: While overall revenue grew by 10%, the outlook for operating income and premium subscriber growth for the upcoming quarter disappointed investors, indicating challenges in major markets.

- User Growth Drivers: All key performance indicators met or exceeded expectations, with advanced AI-powered personalization tools and enhancements to the mobile free tier driving accelerated user growth, despite a weak overall growth outlook.

- Strong Market Performance: Since January 2022, Spotify's stock has outperformed the S&P 500 by 78%, demonstrating robust performance under specific market conditions, even as current profit forecasts raise investor concerns.

See More

Amazon vs. Microsoft: AI Investment Performance Comparison

- Amazon's AI Investment Returns: Amazon is set to invest $200 billion in AI capital expenditures this year, with CEO Andy Jassy stating that AI investments are already yielding returns, as AWS AI services achieved a $15 billion annual revenue run rate in Q1 2026, indicating strong profitability potential in the AI sector.

- Microsoft's Challenges: Microsoft is lagging in the AI race; despite generating $7.58 billion from its partnership with OpenAI, its Copilot AI tools are struggling, with only 3% of commercial customers purchasing licenses, highlighting difficulties in product adoption.

- Market Performance Divergence: Over the past five years, Amazon's stock has risen 52% while Microsoft's has increased 68%, but year-to-date, Amazon is up 14% while Microsoft has declined by 12%, reflecting Amazon's strong momentum in the AI space.

- Investor Confidence: Although Microsoft's P/E ratio stands at 26.6, lower than Amazon's 36.8, recent trends and news suggest that investors are more optimistic about Amazon's AI growth story, anticipating that Amazon will outperform Microsoft in the upcoming earnings reports.

See More