Earnings Reports Drive Stock Price Movements for Multiple Companies

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 2 days ago

0mins

Should l Buy BKNG?

Source: CNBC

- Booking Holdings Adjusts Outlook: Booking Holdings lowered its full-year adjusted earnings per share growth forecast to the 'low to mid-teens' from the previous 'mid-teens,' primarily due to lagging impacts from the Middle East conflict, resulting in a nearly 4% drop in shares.

- Mondelez Exceeds Expectations: Mondelez International reported first-quarter adjusted earnings of 67 cents per share and revenue of $10.08 billion, both surpassing analyst expectations, which led to a 2% increase in its stock price.

- Starbucks Raises Forecast: Starbucks increased its global and U.S. same-store sales outlook to at least 5% and raised its adjusted earnings forecast to a range of $2.25 to $2.45 per share, causing its stock to jump nearly 5%.

- O-I Glass Lowers Guidance: O-I Glass slashed its full-year earnings guidance to a range of $1 to $1.50 per share from a previous estimate of $1.65 to $1.90, resulting in a 19% plunge in its stock price.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BKNG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BKNG

Wall Street analysts forecast BKNG stock price to rise

25 Analyst Rating

18 Buy

7 Hold

0 Sell

Moderate Buy

Current: 168.360

Low

5407

Averages

6153

High

6850

Current: 168.360

Low

5407

Averages

6153

High

6850

About BKNG

Booking Holdings Inc. is a provider of travel and restaurant online reservation and related services. The Company offers its services through five primary consumer-facing brands: Booking.com, Priceline, Agoda, KAYAK, and OpenTable. Through its brands, consumers can book an array of accommodations (including hotels, motels, resorts, homes, apartments, bed and breakfasts, hostels, and other alternative and traditional accommodation properties) and a flight to their destinations; make a car rental reservation or arrange for an airport taxi; make a dinner reservation; or book a vacation package, tour, activity, or cruise. Consumers can also use its meta-search services to easily compare travel reservation information, such as flight, hotel, and rental car reservations from hundreds of online travel platforms at once. Booking.com offers accommodation reservation services for approximately 4.0 million properties in over 220 countries and territories and in over 40 languages.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Investment Opportunity Analysis for Booking Holdings Stock

- Market Leadership: Booking Holdings, as the largest travel company globally, boasts a market cap of approximately $138 billion, significantly surpassing second-place Marriott International at $95 billion, highlighting its dominant position in the online travel sector.

- Strong Financial Performance: In Q1 2023, Booking reported a 16% year-over-year revenue increase, with bookings rising 15% and room nights up 6%, demonstrating robust business resilience despite challenges from geopolitical conflicts.

- Attractive Valuation: Currently, Booking's stock trades at a P/E ratio of 16, near its lowest level in a decade, and its five-year PEG ratio of 0.73 indicates significant undervaluation relative to its long-term earnings potential, presenting a compelling buying opportunity.

- Analyst Optimism: With 83% of Wall Street analysts rating Booking stock as a buy and a median price target of $235, suggesting a 32% upside, there is strong market confidence in its long-term value despite short-term volatility.

See More

Booking Holdings Reports Q1 EPS Beat Amid Middle East Conflict

- Earnings Beat: Booking Holdings reported Q1 EPS exceeding market expectations, demonstrating the company's ability to maintain profitability despite adverse conditions in the Middle East, reflecting strong market adaptability and operational resilience.

- Analyst Ratings Hold: Analysts continue to maintain 'Buy' ratings on the stock, indicating confidence in the company's future growth potential, particularly as travel demand continues to recover.

- Strong Room Night Trends: The company reported a sustained increase in room nights, indicating robust consumer demand for travel, which will support future revenue growth and further solidify its market leadership.

- Market Adaptability: Amid the Middle East conflict, Booking Holdings has shown strong market adaptability, effectively managing external risks, thereby instilling confidence in investors and signaling ongoing growth potential in a complex environment.

See More

Uber Introduces Hotel Bookings and AI Voice Features

- Hotel Booking Feature: Uber partners with Expedia Group to offer over 700,000 hotel options for U.S. users, with plans to add home rentals via Vrbo, directly competing with Booking and Airbnb, enhancing user experience and expanding market share.

- AI Voice Booking: Uber introduces a voice booking chatbot powered by OpenAI models, allowing users to book rides through voice prompts, enhancing the platform's intelligence and convenience, thereby attracting more customers.

- Shopping Feature Expansion: Uber launches a shopping feature where users can send photos and details to a personal shopper and pay the store price, further diversifying its business scope and increasing user engagement.

- Travel Experience Upgrades: Uber One members can earn ride credits and $0 delivery fees abroad, while a new room service feature delivers commonly forgotten travel essentials, enhancing the overall travel experience and increasing user satisfaction.

See More

Uber Enters Travel Industry with New Offerings

- Hotel Booking Service: Uber partners with Expedia to offer over 700,000 hotel options for U.S. users, with Uber One members receiving a 20% discount and 10% cashback, directly competing with Booking Holdings and Airbnb, significantly expanding its market share.

- AI Voice Booking Feature: Uber introduces a voice chatbot powered by OpenAI models, allowing users to book rides through voice commands, enhancing user experience and increasing the platform's intelligence, further solidifying its leadership in the mobility sector.

- Shopping Feature Expansion: The new shopping feature enables users to purchase items by sending photos and details to a personal shopper, broadening Uber's service offerings and aiming to attract more users while enhancing platform diversity.

- Travel Experience Enhancements: Uber provides ride credits and zero delivery fees for Uber One members abroad, along with hotel delivery services for forgotten essentials, aiming to improve user convenience and satisfaction, further strengthening its positioning as an all-in-one app.

See More

Booking Holdings Stock Drops 2.7% Following Company’s Reduction of Annual Revenue Growth Outlook

Stock Performance: Booking Holdings shares have decreased by 2.7%.

Revenue Growth Forecast: The company has made adjustments to its annual revenue growth forecast.

See More

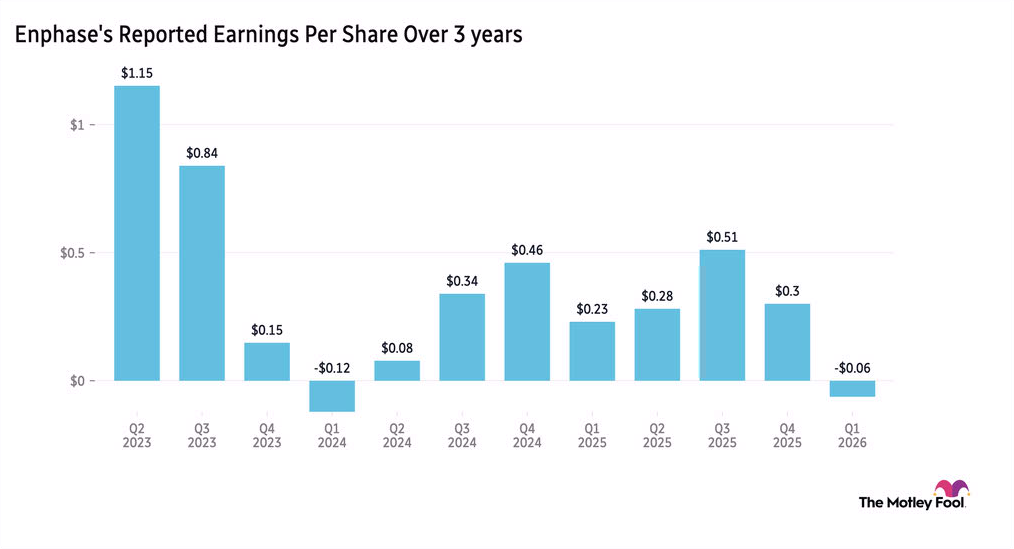

Enphase Energy Drops as Solar Demand Weakens

- Earnings Decline: Enphase Energy reported a 31% year-over-year drop in non-GAAP earnings per share for Q1, leading to a more than 10% decline in pre-market trading, highlighting significant challenges in the U.S. market amid tariff costs and oil-centric energy policies.

- International Market Expansion: Despite domestic struggles, CEO Kothandaraman noted healthy double-digit growth in battery demand across Europe, which is expected to drive revenue growth; however, to combat competition, the company plans to reduce distributor prices for batteries by approximately 10% in May.

- Revenue Outlook: Management anticipates Q2 revenue between $280 million and $310 million, following Q1 revenue of $282.9 million, while maintaining non-GAAP gross margins between 44% and 47%, indicating confidence in the commercialization of next-generation products.

- Intensifying Market Competition: With a prior 20% price reduction on microinverters implemented last December, the upcoming price adjustments may impact short-term margins but could pave the way for long-term market share gains, reflecting the company's adaptability in the rapidly evolving solar market.

See More

Investment Opportunity Analysis for Booking Holdings Stock

- Market Leadership: Booking Holdings, as the largest travel company globally, boasts a market cap of approximately $138 billion, significantly surpassing second-place Marriott International at $95 billion, highlighting its dominant position in the online travel sector.

- Strong Financial Performance: In Q1 2023, Booking reported a 16% year-over-year revenue increase, with bookings rising 15% and room nights up 6%, demonstrating robust business resilience despite challenges from geopolitical conflicts.

- Attractive Valuation: Currently, Booking's stock trades at a P/E ratio of 16, near its lowest level in a decade, and its five-year PEG ratio of 0.73 indicates significant undervaluation relative to its long-term earnings potential, presenting a compelling buying opportunity.

- Analyst Optimism: With 83% of Wall Street analysts rating Booking stock as a buy and a median price target of $235, suggesting a 32% upside, there is strong market confidence in its long-term value despite short-term volatility.

See More

Booking Holdings Reports Q1 EPS Beat Amid Middle East Conflict

- Earnings Beat: Booking Holdings reported Q1 EPS exceeding market expectations, demonstrating the company's ability to maintain profitability despite adverse conditions in the Middle East, reflecting strong market adaptability and operational resilience.

- Analyst Ratings Hold: Analysts continue to maintain 'Buy' ratings on the stock, indicating confidence in the company's future growth potential, particularly as travel demand continues to recover.

- Strong Room Night Trends: The company reported a sustained increase in room nights, indicating robust consumer demand for travel, which will support future revenue growth and further solidify its market leadership.

- Market Adaptability: Amid the Middle East conflict, Booking Holdings has shown strong market adaptability, effectively managing external risks, thereby instilling confidence in investors and signaling ongoing growth potential in a complex environment.

See More

Uber Introduces Hotel Bookings and AI Voice Features

- Hotel Booking Feature: Uber partners with Expedia Group to offer over 700,000 hotel options for U.S. users, with plans to add home rentals via Vrbo, directly competing with Booking and Airbnb, enhancing user experience and expanding market share.

- AI Voice Booking: Uber introduces a voice booking chatbot powered by OpenAI models, allowing users to book rides through voice prompts, enhancing the platform's intelligence and convenience, thereby attracting more customers.

- Shopping Feature Expansion: Uber launches a shopping feature where users can send photos and details to a personal shopper and pay the store price, further diversifying its business scope and increasing user engagement.

- Travel Experience Upgrades: Uber One members can earn ride credits and $0 delivery fees abroad, while a new room service feature delivers commonly forgotten travel essentials, enhancing the overall travel experience and increasing user satisfaction.

See More

Uber Enters Travel Industry with New Offerings

- Hotel Booking Service: Uber partners with Expedia to offer over 700,000 hotel options for U.S. users, with Uber One members receiving a 20% discount and 10% cashback, directly competing with Booking Holdings and Airbnb, significantly expanding its market share.

- AI Voice Booking Feature: Uber introduces a voice chatbot powered by OpenAI models, allowing users to book rides through voice commands, enhancing user experience and increasing the platform's intelligence, further solidifying its leadership in the mobility sector.

- Shopping Feature Expansion: The new shopping feature enables users to purchase items by sending photos and details to a personal shopper, broadening Uber's service offerings and aiming to attract more users while enhancing platform diversity.

- Travel Experience Enhancements: Uber provides ride credits and zero delivery fees for Uber One members abroad, along with hotel delivery services for forgotten essentials, aiming to improve user convenience and satisfaction, further strengthening its positioning as an all-in-one app.

See More

Booking Holdings Stock Drops 2.7% Following Company’s Reduction of Annual Revenue Growth Outlook

Stock Performance: Booking Holdings shares have decreased by 2.7%.

Revenue Growth Forecast: The company has made adjustments to its annual revenue growth forecast.

See More

Enphase Energy Drops as Solar Demand Weakens

- Earnings Decline: Enphase Energy reported a 31% year-over-year drop in non-GAAP earnings per share for Q1, leading to a more than 10% decline in pre-market trading, highlighting significant challenges in the U.S. market amid tariff costs and oil-centric energy policies.

- International Market Expansion: Despite domestic struggles, CEO Kothandaraman noted healthy double-digit growth in battery demand across Europe, which is expected to drive revenue growth; however, to combat competition, the company plans to reduce distributor prices for batteries by approximately 10% in May.

- Revenue Outlook: Management anticipates Q2 revenue between $280 million and $310 million, following Q1 revenue of $282.9 million, while maintaining non-GAAP gross margins between 44% and 47%, indicating confidence in the commercialization of next-generation products.

- Intensifying Market Competition: With a prior 20% price reduction on microinverters implemented last December, the upcoming price adjustments may impact short-term margins but could pave the way for long-term market share gains, reflecting the company's adaptability in the rapidly evolving solar market.

See More