Duolingo Stock Plummets Despite Rising Revenue and Engagement

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 09 2026

0mins

Should l Buy DUOL?

Source: Fool

- Stock Price Crash: Duolingo's stock price faced a significant decline as of February 3, 2026, yet the company's revenue and user engagement continue to rise, indicating a potential misjudgment of its future prospects by the market.

- Revenue Growth: Despite the stock price drop, Duolingo's revenue is still on the rise, suggesting that its core business maintains strong market demand, potentially offering a buying opportunity for investors.

- Free Cash Flow Improvement: The company's free cash flow is consistently increasing, reflecting enhanced operational efficiency and successful cost control, which lays a solid foundation for future investments and expansion.

- User Engagement Increase: The rise in user engagement not only strengthens Duolingo's competitive position in the market but may also support its long-term growth, even though the stock has underperformed in the short term.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DUOL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DUOL

Wall Street analysts forecast DUOL stock price to rise

17 Analyst Rating

10 Buy

6 Hold

1 Sell

Moderate Buy

Current: 110.230

Low

160.00

Averages

260.36

High

330.00

Current: 110.230

Low

160.00

Averages

260.36

High

330.00

About DUOL

Duolingo, Inc. is a technology company. The Company is engaged in offering a mobile learning platform, as well as a digital English language proficiency assessment exam. It operates a freemium business model, namely, the app and the Website are accessible free of charge, although Duolingo also offers premium services for a subscription fee. Its solutions consist of the Duolingo App, Super Duolingo, Duolingo Max, Duolingo English Test: AI-Driven Language Assessment, Duolingo for Schools, and Duolingo ABC. The Duolingo App offers courses in over 40 different languages, including Spanish, English, French, German, Italian, Portuguese, Japanese and Chinese. Duolingo can also be accessed on desktop computers via a Web browser. Its subscription offering, Super Duolingo, offers learners additional features to enhance their learning experience. The Duolingo English Test is an online, on-demand, high-stakes English proficiency assessment. It also operates an animation and motion design studio.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Duolingo Reports Strong Q1 Earnings but Stock Drops on Strategic Shift

- Earnings Beat: Duolingo reported Q1 earnings per share of $0.89, exceeding Wall Street's expectation of $0.76, with revenue reaching $292 million, surpassing the anticipated $288.98 million, indicating strong performance in user growth.

- Significant User Growth: Daily active users (DAUs) increased by 21% year-over-year to 56.5 million, while paid subscribers also rose by 21% to 12.5 million, reflecting continued engagement across its global user base.

- Strategic Shift Impact: Despite strong Q1 results, Duolingo's stock dropped 13% in after-hours trading as the company pivots to prioritize user experience and long-term retention over short-term monetization, which may negatively impact financial results in the near term.

- Future Outlook: The company expects bookings growth of about 10.5% for 2026 and aims to reach 100 million daily active users by 2028, indicating that while short-term financial results may be affected, long-term investments are set to drive future growth.

See More

Duolingo's Earnings Miss Expectations, Shares Drop 14%

- Earnings Performance: Duolingo's Q1 results exceeded expectations; however, the disappointing growth outlook led to a 14% drop in shares during after-hours trading, reflecting market skepticism.

- Revenue Outlook: The company maintained its full-year revenue forecast at approximately $1.21 billion but guided for only 10-12% growth in bookings for the year and just 5.8% in Q2, indicating a significant deceleration from previous trends.

- Industry Valuation Rankings: With a D grade, Duolingo ranks at the bottom of the education sector's valuation rankings, while New Oriental Education and Stride lead with B- grades, highlighting the disparity in market confidence among different companies.

- Market Reaction: Investors remain skeptical about Duolingo's future growth prospects, particularly after the company failed to signal an acceleration in growth, which could adversely affect its long-term stock performance.

See More

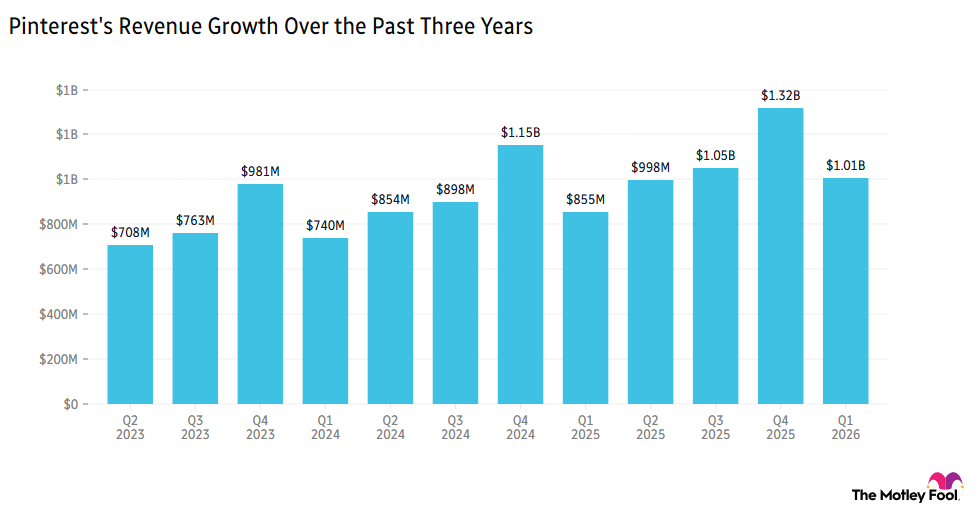

Pinterest Surges on Record User Growth and Positive Revenue Guidance

- Strong User Growth: Pinterest (PINS) surged over 15% ahead of market open, driven by an 11% year-over-year increase in monthly active users (MAU), marking the tenth consecutive quarter of double-digit growth, indicating that enhanced user engagement will support future profitability.

- Optimistic Revenue Guidance: Pinterest's revenue guidance exceeded expectations, with CEO Bill Ready emphasizing the company's commitment to aligning profitability with user engagement, thereby boosting investor confidence and driving stock price increases.

- Positive Market Reaction: Analyst Rich Greifner highlighted that Pinterest's large and engaged user base, characterized by high commercial intent, makes it an attractive platform for advertisers, further solidifying its competitive position in the advertising market.

- Favorable Industry Outlook: As Pinterest's user growth and revenue expectations improve, market confidence in its future performance is likely to attract more investor interest, propelling further development in the social media sector.

See More

PayPal and Anheuser-Busch Beat Earnings Expectations

- PayPal Earnings Surprise: PayPal reported first-quarter earnings of $1.34 per share, exceeding analyst expectations of $1.27, with revenues of $8.35 billion surpassing the $8.05 billion forecast, indicating strong performance in the payments sector that could drive stock price increases.

- Anheuser-Busch Strong Growth: Anheuser-Busch reported earnings of $0.97 per share, beating the expected $0.89, with revenues of $15.27 billion significantly above the $14.87 billion forecast, demonstrating sustained competitiveness in the beer market that may attract more investor interest.

- Pfizer Exceeds Expectations: Pfizer's first-quarter earnings came in at $0.75 per share, above the $0.72 expected, with revenues of $14.45 billion, reflecting robust growth in the pharmaceutical sector that could enhance market confidence in its future products.

- Pinterest Optimistic Revenue Guidance: Pinterest's second-quarter revenue guidance of $1.13 billion to $1.15 billion exceeded the $1.11 billion expected, with first-quarter adjusted earnings of $0.27 per share and revenues of $1.01 billion, showcasing strong growth potential in the social media space that is likely to improve market perceptions of its long-term value.

See More

Pinterest Surges on Strong Q1 Earnings Beat

- Pinterest's Strong Performance: Pinterest reported Q1 revenue of $1 billion, a 17% year-over-year increase, with adjusted EPS of $0.27 exceeding expectations, while global monthly active users grew 11% to 631 million, marking the tenth consecutive quarter of double-digit user growth, indicating robust momentum in its advertising platform.

- Optimistic Future Outlook: The company anticipates Q2 revenue between $1.13 billion and $1.15 billion, surpassing the $1.12 billion consensus, with adjusted EBITDA projected between $256 million and $276 million, highlighting its ongoing growth potential driven by AI-powered advertising.

- Intel's Collaboration Potential: Intel shares rose 4% following reports that Apple is in early-stage talks with Intel and Samsung Electronics to potentially manufacture processors in the U.S. as an alternative to TSMC, reflecting Apple's strategic consideration for supply chain diversification despite no orders being placed yet.

- Duolingo's Slowing Growth: Duolingo's shares fell 13% despite a 27% year-over-year revenue increase to $292 million in Q1, as a softer growth outlook and increased investments weighed on sentiment, with management maintaining a FY2026 revenue outlook of approximately $1.21 billion, indicating market caution regarding future growth.

See More

Duolingo Reports Strong Q1 but Soft Growth Outlook Pressures Stock

- Significant Revenue Growth: Duolingo's Q1 revenue rose approximately 27% year-over-year to $292 million, exceeding expectations by $3.42 million, indicating sustained user engagement and growth potential on the platform.

- User Engagement Increase: Both paid subscribers and daily active users grew roughly 21% year-over-year, demonstrating effective strategies in user retention and engagement, despite challenges in future growth outlook.

- Adjusted Guidance: The company maintained its full-year revenue outlook at around $1.21 billion but guided for bookings growth to slow to 10-12%, reflecting a moderation in near-term momentum that may impact investor confidence.

- Future Investments: Management emphasized prioritizing user engagement and retention over immediate monetization, with increased spending on AI features likely to compress margins in the short term, but expected to yield returns post-2027.

See More

Duolingo Reports Strong Q1 Earnings but Stock Drops on Strategic Shift

- Earnings Beat: Duolingo reported Q1 earnings per share of $0.89, exceeding Wall Street's expectation of $0.76, with revenue reaching $292 million, surpassing the anticipated $288.98 million, indicating strong performance in user growth.

- Significant User Growth: Daily active users (DAUs) increased by 21% year-over-year to 56.5 million, while paid subscribers also rose by 21% to 12.5 million, reflecting continued engagement across its global user base.

- Strategic Shift Impact: Despite strong Q1 results, Duolingo's stock dropped 13% in after-hours trading as the company pivots to prioritize user experience and long-term retention over short-term monetization, which may negatively impact financial results in the near term.

- Future Outlook: The company expects bookings growth of about 10.5% for 2026 and aims to reach 100 million daily active users by 2028, indicating that while short-term financial results may be affected, long-term investments are set to drive future growth.

See More

Duolingo's Earnings Miss Expectations, Shares Drop 14%

- Earnings Performance: Duolingo's Q1 results exceeded expectations; however, the disappointing growth outlook led to a 14% drop in shares during after-hours trading, reflecting market skepticism.

- Revenue Outlook: The company maintained its full-year revenue forecast at approximately $1.21 billion but guided for only 10-12% growth in bookings for the year and just 5.8% in Q2, indicating a significant deceleration from previous trends.

- Industry Valuation Rankings: With a D grade, Duolingo ranks at the bottom of the education sector's valuation rankings, while New Oriental Education and Stride lead with B- grades, highlighting the disparity in market confidence among different companies.

- Market Reaction: Investors remain skeptical about Duolingo's future growth prospects, particularly after the company failed to signal an acceleration in growth, which could adversely affect its long-term stock performance.

See More

Pinterest Surges on Record User Growth and Positive Revenue Guidance

- Strong User Growth: Pinterest (PINS) surged over 15% ahead of market open, driven by an 11% year-over-year increase in monthly active users (MAU), marking the tenth consecutive quarter of double-digit growth, indicating that enhanced user engagement will support future profitability.

- Optimistic Revenue Guidance: Pinterest's revenue guidance exceeded expectations, with CEO Bill Ready emphasizing the company's commitment to aligning profitability with user engagement, thereby boosting investor confidence and driving stock price increases.

- Positive Market Reaction: Analyst Rich Greifner highlighted that Pinterest's large and engaged user base, characterized by high commercial intent, makes it an attractive platform for advertisers, further solidifying its competitive position in the advertising market.

- Favorable Industry Outlook: As Pinterest's user growth and revenue expectations improve, market confidence in its future performance is likely to attract more investor interest, propelling further development in the social media sector.

See More

PayPal and Anheuser-Busch Beat Earnings Expectations

- PayPal Earnings Surprise: PayPal reported first-quarter earnings of $1.34 per share, exceeding analyst expectations of $1.27, with revenues of $8.35 billion surpassing the $8.05 billion forecast, indicating strong performance in the payments sector that could drive stock price increases.

- Anheuser-Busch Strong Growth: Anheuser-Busch reported earnings of $0.97 per share, beating the expected $0.89, with revenues of $15.27 billion significantly above the $14.87 billion forecast, demonstrating sustained competitiveness in the beer market that may attract more investor interest.

- Pfizer Exceeds Expectations: Pfizer's first-quarter earnings came in at $0.75 per share, above the $0.72 expected, with revenues of $14.45 billion, reflecting robust growth in the pharmaceutical sector that could enhance market confidence in its future products.

- Pinterest Optimistic Revenue Guidance: Pinterest's second-quarter revenue guidance of $1.13 billion to $1.15 billion exceeded the $1.11 billion expected, with first-quarter adjusted earnings of $0.27 per share and revenues of $1.01 billion, showcasing strong growth potential in the social media space that is likely to improve market perceptions of its long-term value.

See More

Pinterest Surges on Strong Q1 Earnings Beat

- Pinterest's Strong Performance: Pinterest reported Q1 revenue of $1 billion, a 17% year-over-year increase, with adjusted EPS of $0.27 exceeding expectations, while global monthly active users grew 11% to 631 million, marking the tenth consecutive quarter of double-digit user growth, indicating robust momentum in its advertising platform.

- Optimistic Future Outlook: The company anticipates Q2 revenue between $1.13 billion and $1.15 billion, surpassing the $1.12 billion consensus, with adjusted EBITDA projected between $256 million and $276 million, highlighting its ongoing growth potential driven by AI-powered advertising.

- Intel's Collaboration Potential: Intel shares rose 4% following reports that Apple is in early-stage talks with Intel and Samsung Electronics to potentially manufacture processors in the U.S. as an alternative to TSMC, reflecting Apple's strategic consideration for supply chain diversification despite no orders being placed yet.

- Duolingo's Slowing Growth: Duolingo's shares fell 13% despite a 27% year-over-year revenue increase to $292 million in Q1, as a softer growth outlook and increased investments weighed on sentiment, with management maintaining a FY2026 revenue outlook of approximately $1.21 billion, indicating market caution regarding future growth.

See More

Duolingo Reports Strong Q1 but Soft Growth Outlook Pressures Stock

- Significant Revenue Growth: Duolingo's Q1 revenue rose approximately 27% year-over-year to $292 million, exceeding expectations by $3.42 million, indicating sustained user engagement and growth potential on the platform.

- User Engagement Increase: Both paid subscribers and daily active users grew roughly 21% year-over-year, demonstrating effective strategies in user retention and engagement, despite challenges in future growth outlook.

- Adjusted Guidance: The company maintained its full-year revenue outlook at around $1.21 billion but guided for bookings growth to slow to 10-12%, reflecting a moderation in near-term momentum that may impact investor confidence.

- Future Investments: Management emphasized prioritizing user engagement and retention over immediate monetization, with increased spending on AI features likely to compress margins in the short term, but expected to yield returns post-2027.

See More