Docusign Launches Intelligent Agreement Management Platform

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 21 2026

0mins

Source: Fool

- Surging Market Demand: Docusign's Intelligent Agreement Management (IAM) platform, launched in 2024, leverages AI to simplify contract management processes, which is expected to drive steady growth in overall revenue and earnings, reflecting strong market demand.

- Economic Loss Warning: A study by Deloitte indicates that businesses waste 55 billion hours annually due to poor contract management, costing up to $2 trillion in economic value, and Docusign aims to address this 'agreement trap' through the IAM platform, highlighting its market significance.

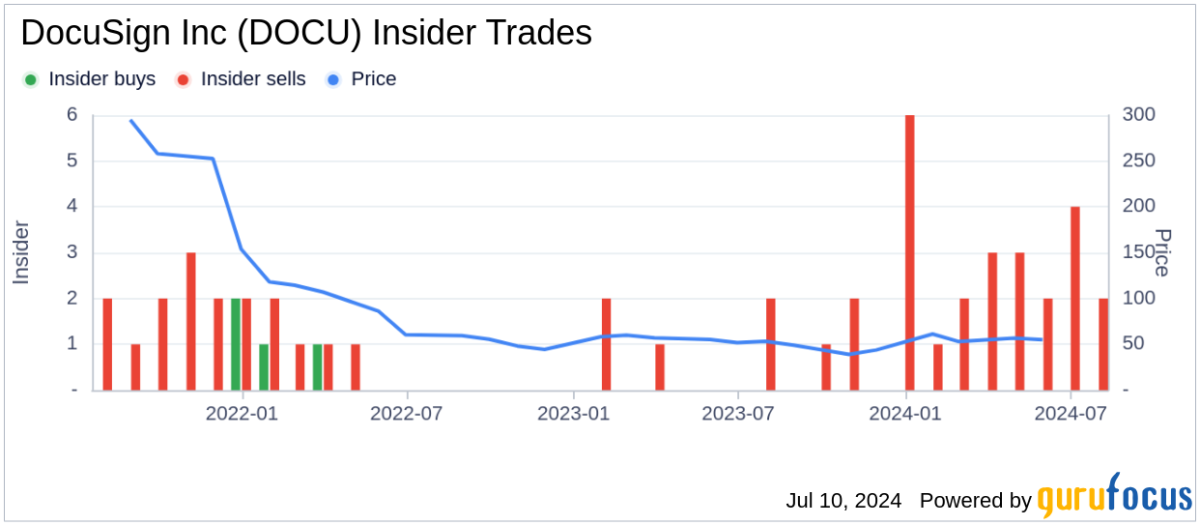

- Revenue Growth Highlights: Docusign generated $3.2 billion in total revenue for fiscal 2026, an 8% increase year-over-year, with the IAM platform contributing $350 million in annual recurring revenue, accounting for over 10% of total revenue, showcasing its positive impact on company growth.

- Attractive Stock Valuation: Docusign's current price-to-sales ratio stands at 3.1, close to its lowest since going public in 2018 and significantly below its long-term average of 12.4, suggesting the stock may be undervalued, making it appealing for long-term investors.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DOCU?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DOCU

Wall Street analysts forecast DOCU stock price to rise

16 Analyst Rating

3 Buy

13 Hold

0 Sell

Hold

Current: 46.900

Low

70.00

Averages

80.23

High

105.00

Current: 46.900

Low

70.00

Averages

80.23

High

105.00

About DOCU

DocuSign, Inc. provides intelligent agreement management (IAM) platform an eSignature solution, and contract lifecycle management (CLM) solution - allow organizations to increase productivity, accelerate contract review cycles, and transform agreement data into insights and actions. The Company’s IAM platform automates agreement workflows, uncovers actionable insights, and leverages artificial intelligence (AI) capabilities, enabling organizations to create, commit, and manage agreements virtually. Its products include eSignature, CLM, IAM Apps, and Add-on Products. Its Add-on Products include Payments to collect payments along with signed agreements; Identity and standards-based signature for enhanced signer-identification and signatures with digital certification; Notary for remote online notarization; Monitor for advanced analytics; Gen for Salesforce for automated agreement generation within Salesforce, among others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Analysis of Significant Decline in Tech Stocks

- Price Decline: As of the afternoon of June 27, 2026, this tech stock has significantly dropped from its historical peak, indicating market concerns about the industry's outlook, which may lead to decreased investor confidence.

- Market Reaction: Following the video release two days later, investor response to the stock has been lukewarm, reflecting uncertainty about future profitability, which could impact the company's ability to raise funds and its market valuation.

- Industry Trends: The tech sector is facing challenges, particularly amid economic slowdown and rising interest rates, leading to diminished investor interest in high-valuation tech companies, exacerbating the downward pressure on this stock.

- Investor Strategy Shift: With the ongoing price decline, investors may reassess their portfolios and shift towards more defensive assets, further affecting the liquidity and market performance of this tech stock.

See More

Docusign Excluded from Top Investment Stocks List

- Poor Market Performance: Docusign's stock is significantly down from its historical highs, reflecting market concerns about its future growth potential, which may lead to decreased investor confidence and negatively impact short-term stock performance.

- Lack of Investment Recommendations: The Motley Fool's analyst team has excluded Docusign from their list of the top 10 stocks to buy, indicating a cautious outlook on the company's prospects, which could hinder its ability to attract new investors.

- Historical Comparison: Compared to the recommendations of Netflix in 2004 and Nvidia in 2005, Docusign's exclusion from similar lists shows a decline in its standing among investors, potentially leading to capital outflows and affecting its long-term growth.

- Investment Return Comparison: With Stock Advisor's average return at 892%, significantly surpassing the S&P 500's 205%, Docusign's absence from the recommended list suggests limited future investment return potential, impacting its market competitiveness.

See More

Docusign Partners with Perplexity to Enhance Contract Management

- Intelligent Contract Management: Docusign's Intelligent Agreement Management platform is now integrated with Perplexity Computer, enabling legal teams to automate contract workflows using AI, thereby reducing time spent on manual tasks and enhancing efficiency.

- Cross-Department Collaboration: By collaborating with sales, procurement, and HR, legal teams can process contracts faster, ensuring critical contract information is no longer scattered across multiple systems, thus accelerating business operations.

- End-to-End Automation: The integration allows legal teams to automate agreement workflows from start to finish, increasing contract execution speed and enabling them to focus more on strategic legal work, thereby enhancing business support capabilities.

- Global User Base: Docusign serves nearly 1.9 million customers across over 180 countries, and through its intelligent agreement management platform, businesses can unlock critical data trapped in documents, saving time and costs while improving market competitiveness.

See More

Docusign Partners with Perplexity to Enhance Contract Management Efficiency

- Intelligent Contract Management: Docusign's Intelligent Agreement Management platform is now available on Perplexity Computer, enabling legal teams to automate contract workflows with AI, thereby reducing time spent on manual tasks and enhancing strategic work efficiency.

- Accelerated Contract Execution: By connecting Docusign with Perplexity's tools, legal teams can not only speed up contract execution but also automate end-to-end agreement workflows, significantly improving operational efficiency.

- Streamlined Compliance Reviews: Legal and procurement teams can quickly identify clauses that do not align with company policies and automatically review suggested edits without manual comparisons, saving time and reducing error risks.

- Optimized HR Agreements: Legal teams can operationalize HR agreements throughout the entire hiring lifecycle, including reviewing and signing employment agreements, identifying missing employee documents, and flagging compliance issues, further enhancing HR management efficiency.

See More

DocuSign Launches Slack App for Agreement Management Integration

- App Launch: DocuSign has launched a Slack app that integrates its agreement management tools, allowing users to access contract data and automate workflows directly within workplace messaging, thereby enhancing operational efficiency.

- Intelligent Agreement Management: The app connects DocuSign's Intelligent Agreement Management platform to Slack using Model Context Protocol, enabling users to query contract information through natural language prompts, significantly reducing fragmentation in contract-related work.

- Process Automation: Users can automate processes such as approvals, contract reviews, and signatures directly within Slack conversations, improving team collaboration and minimizing manual tasks.

- Data Synchronization and Alerts: The system can synchronize agreement data with Salesforce and provide alerts on deadlines, renewals, and compliance obligations, further optimizing contract management workflows.

See More

Docusign Launches Slackbot Integration App for Agreement Management

- Intelligent Agreement Management: Docusign's new Slackbot app integrates its Intelligent Agreement Management platform directly into Slack via Model Context Protocol (MCP), enabling teams to quickly access agreement intelligence in their daily workflows, thereby enhancing operational efficiency.

- Workflow Automation: Powered by the Docusign Iris AI engine, the app allows users to ask natural language questions about agreements and receive instant answers based on chat history and CRM data, streamlining workflows for sales, legal, and HR departments.

- Enhanced Collaboration: Docusign CEO Allan Thygesen noted that this integration will enable teams to take action directly within Slack, reducing time spent switching between multiple tools and improving cross-departmental collaboration efficiency.

- Global Availability: The Slackbot app is now available globally in the Slack Marketplace for English users, marking a significant step in Docusign's push for digital transformation in agreement management, expected to attract attention from nearly 1.9 million customers.

See More

Analysis of Significant Decline in Tech Stocks

- Price Decline: As of the afternoon of June 27, 2026, this tech stock has significantly dropped from its historical peak, indicating market concerns about the industry's outlook, which may lead to decreased investor confidence.

- Market Reaction: Following the video release two days later, investor response to the stock has been lukewarm, reflecting uncertainty about future profitability, which could impact the company's ability to raise funds and its market valuation.

- Industry Trends: The tech sector is facing challenges, particularly amid economic slowdown and rising interest rates, leading to diminished investor interest in high-valuation tech companies, exacerbating the downward pressure on this stock.

- Investor Strategy Shift: With the ongoing price decline, investors may reassess their portfolios and shift towards more defensive assets, further affecting the liquidity and market performance of this tech stock.

See More

Docusign Excluded from Top Investment Stocks List

- Poor Market Performance: Docusign's stock is significantly down from its historical highs, reflecting market concerns about its future growth potential, which may lead to decreased investor confidence and negatively impact short-term stock performance.

- Lack of Investment Recommendations: The Motley Fool's analyst team has excluded Docusign from their list of the top 10 stocks to buy, indicating a cautious outlook on the company's prospects, which could hinder its ability to attract new investors.

- Historical Comparison: Compared to the recommendations of Netflix in 2004 and Nvidia in 2005, Docusign's exclusion from similar lists shows a decline in its standing among investors, potentially leading to capital outflows and affecting its long-term growth.

- Investment Return Comparison: With Stock Advisor's average return at 892%, significantly surpassing the S&P 500's 205%, Docusign's absence from the recommended list suggests limited future investment return potential, impacting its market competitiveness.

See More

Docusign Partners with Perplexity to Enhance Contract Management

- Intelligent Contract Management: Docusign's Intelligent Agreement Management platform is now integrated with Perplexity Computer, enabling legal teams to automate contract workflows using AI, thereby reducing time spent on manual tasks and enhancing efficiency.

- Cross-Department Collaboration: By collaborating with sales, procurement, and HR, legal teams can process contracts faster, ensuring critical contract information is no longer scattered across multiple systems, thus accelerating business operations.

- End-to-End Automation: The integration allows legal teams to automate agreement workflows from start to finish, increasing contract execution speed and enabling them to focus more on strategic legal work, thereby enhancing business support capabilities.

- Global User Base: Docusign serves nearly 1.9 million customers across over 180 countries, and through its intelligent agreement management platform, businesses can unlock critical data trapped in documents, saving time and costs while improving market competitiveness.

See More

Docusign Partners with Perplexity to Enhance Contract Management Efficiency

- Intelligent Contract Management: Docusign's Intelligent Agreement Management platform is now available on Perplexity Computer, enabling legal teams to automate contract workflows with AI, thereby reducing time spent on manual tasks and enhancing strategic work efficiency.

- Accelerated Contract Execution: By connecting Docusign with Perplexity's tools, legal teams can not only speed up contract execution but also automate end-to-end agreement workflows, significantly improving operational efficiency.

- Streamlined Compliance Reviews: Legal and procurement teams can quickly identify clauses that do not align with company policies and automatically review suggested edits without manual comparisons, saving time and reducing error risks.

- Optimized HR Agreements: Legal teams can operationalize HR agreements throughout the entire hiring lifecycle, including reviewing and signing employment agreements, identifying missing employee documents, and flagging compliance issues, further enhancing HR management efficiency.

See More

DocuSign Launches Slack App for Agreement Management Integration

- App Launch: DocuSign has launched a Slack app that integrates its agreement management tools, allowing users to access contract data and automate workflows directly within workplace messaging, thereby enhancing operational efficiency.

- Intelligent Agreement Management: The app connects DocuSign's Intelligent Agreement Management platform to Slack using Model Context Protocol, enabling users to query contract information through natural language prompts, significantly reducing fragmentation in contract-related work.

- Process Automation: Users can automate processes such as approvals, contract reviews, and signatures directly within Slack conversations, improving team collaboration and minimizing manual tasks.

- Data Synchronization and Alerts: The system can synchronize agreement data with Salesforce and provide alerts on deadlines, renewals, and compliance obligations, further optimizing contract management workflows.

See More

Docusign Launches Slackbot Integration App for Agreement Management

- Intelligent Agreement Management: Docusign's new Slackbot app integrates its Intelligent Agreement Management platform directly into Slack via Model Context Protocol (MCP), enabling teams to quickly access agreement intelligence in their daily workflows, thereby enhancing operational efficiency.

- Workflow Automation: Powered by the Docusign Iris AI engine, the app allows users to ask natural language questions about agreements and receive instant answers based on chat history and CRM data, streamlining workflows for sales, legal, and HR departments.

- Enhanced Collaboration: Docusign CEO Allan Thygesen noted that this integration will enable teams to take action directly within Slack, reducing time spent switching between multiple tools and improving cross-departmental collaboration efficiency.

- Global Availability: The Slackbot app is now available globally in the Slack Marketplace for English users, marking a significant step in Docusign's push for digital transformation in agreement management, expected to attract attention from nearly 1.9 million customers.

See More