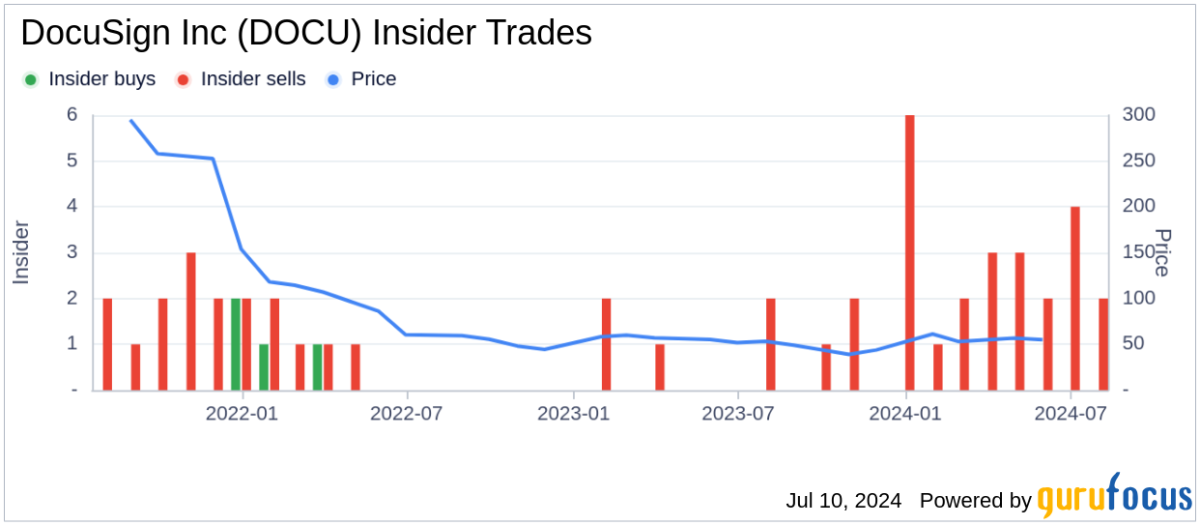

DOCU Overview

-

$

0.000

0.000(0.000%)

At close0.000(0.000%)Aft-market

ET

Loading chart...

The current price of DOCU is 43.47 USD — it has increased 2.09

DocuSign, Inc. provides intelligent agreement management (IAM) platform an eSignature solution, and contract lifecycle management (CLM) solution - allow organizations to increase productivity, accelerate contract review cycles, and transform agreement data into insights and actions. The Company’s IAM platform automates agreement workflows, uncovers actionable insights, and leverages artificial intelligence (AI) capabilities, enabling organizations to create, commit, and manage agreements virtually. Its products include eSignature, CLM, IAM Apps, and Add-on Products. Its Add-on Products include Payments to collect payments along with signed agreements; Identity and standards-based signature for enhanced signer-identification and signatures with digital certification; Notary for remote online notarization; Monitor for advanced analytics; Gen for Salesforce for automated agreement generation within Salesforce, among others.

Wall Street analysts forecast DOCU stock price to rise over the next 12 months. According to Wall Street analysts, the average 1-year price target for DOCU is80.23 USD with a low forecast of 70.00 USD and a high forecast of 105.00 USD. However, analyst price targets are subjective and often lag stock prices, so investors should focus on the objective reasons behind analyst rating changes, which better reflect the company's fundamentals.

DocuSign Inc revenue for the last quarter amounts to 830.24M USD, increased 8.72

DocuSign Inc. EPS for the last quarter amounts to 0.40 USD, increased 17.65

DocuSign Inc (DOCU) has 7044 emplpoyees as of June 21 2026.

Today DOCU has the market capitalization of 8.30B USD.